Kilometre rates get an overhaul

Tax Alert - June 2025

Update: View the 2026 Inland Revenue mileage rate

By Amy Sexton & Andrea Scatchard

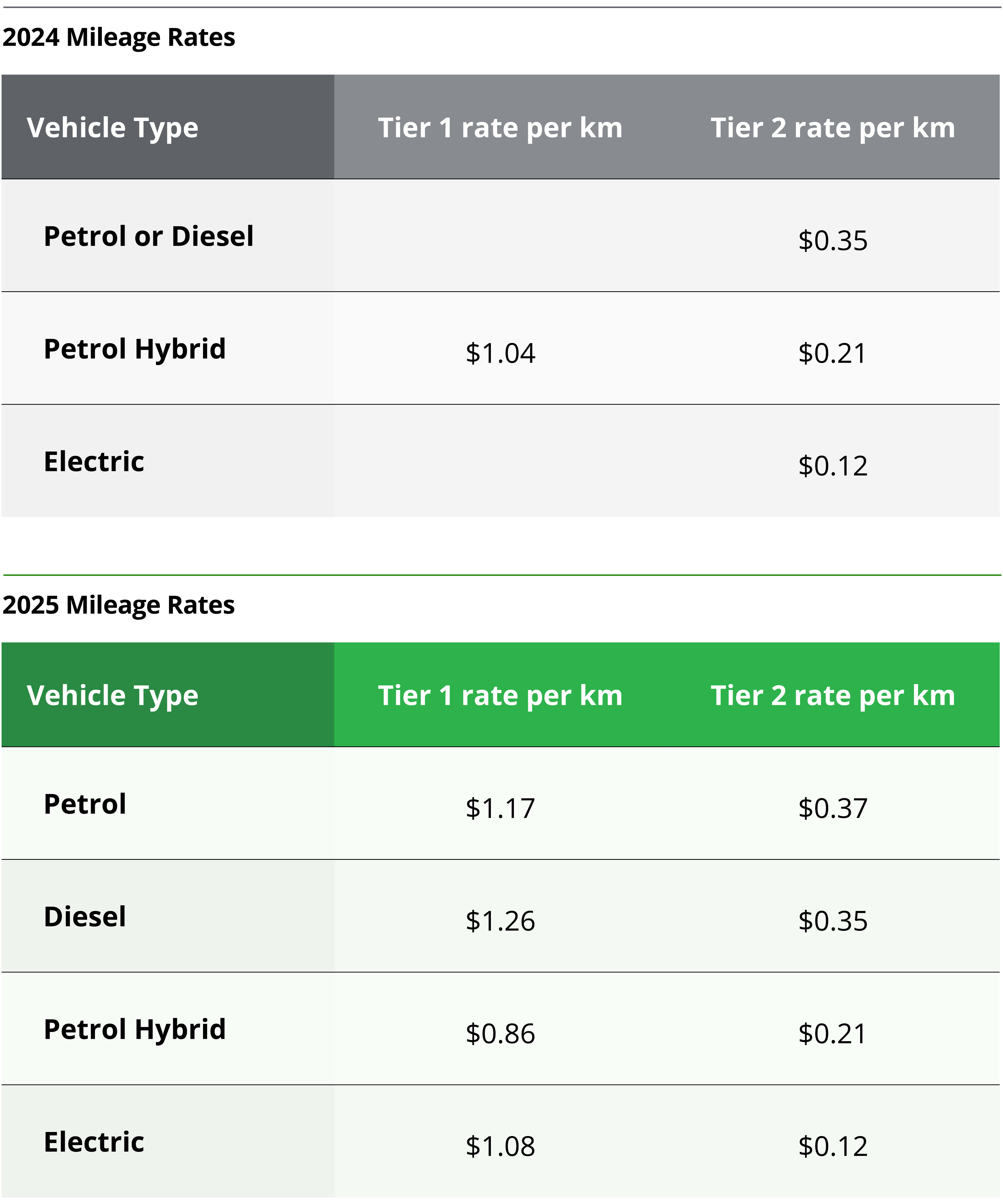

Every year one of our most popular Tax Alert articles is the annual mileage reimbursement update. Normally these articles give an update on the new kilometre rates and a refresh of the rules. However this year Inland Revenue has decided to give the approach to the 2025 kilometre rates an overhaul, expanding out the number of rates from four to eight. This is likely to be a source of annoyance for businesses undertaking mileage reimbursements.

What has changed?

The Inland Revenue has conducted a review of the published vehicle kilometre rates, due to a significant difference in vehicle running costs between the different vehicle types (Petrol, Diesel, Petrol Hybrid and Electric). Traditionally the Commissioner of the Inland Revenue has set a single Tier One rate, however, due to the significant difference in running costs different rates have been set for four vehicle categories to ensure the rates more accurately reflect a reasonable estimate of the expenditure related to the business use of that particular vehicle.

So, in practice, this means than instead of the previous single Tier One and three Tier Two rates, there are now eight different rates, with the prior combined Petrol/Diesel category being separated.

What does Tier One and Tier Two mean?

The Tier One rates reflect the fixed and variable costs of running a vehicle and can be used for the business portion of the first 14,000km of total travel in the vehicle. After these limits, the lower Tier Two rates apply (which only reflect variable costs).

What do I need to remember?

The Commissioner is required to regularly set kilometre rates so that these can be used by self-employed business owners or close companies to determine available tax deductions for business use of a vehicle (if they choose to use the kilometre rate method). In practice, the same rates are often also used by businesses that reimburse employees for the use of personal vehicles for work purposes. Provided reimbursements are made at or below the specified rates, they can be paid “tax-free” without the employer doing further analysis.

Use of these rates is not compulsory. Business owners can instead claim deductions for actual costs incurred (the cost method), and likewise, employers can reimburse employees at higher rates, but records would need to be kept substantiating that the rate of reimbursement is a “reasonable estimate of expenditure”. The move to require information about engine type from the first kilometre of travel reimbursed is likely to see more employers opting out of using these rates for reimbursements and incurring the compliance costs of determining something more practicable.

Self-employed and close companies

If you are a sole trader or qualifying close company and use the kilometre rate method to claim business vehicle costs, the new rates apply for the 2025 year, that is, 1 April 2024 - 31 March 2025 (if you have a standard balance date).

If you have already filed your 2025 income tax return relying on the 2024 kilometre rates, you may be able to self-correct the difference in your 2026 income return, depending on the amount of the difference between the two amounts claimed. If the difference between what was originally claimed, and what can now be claimed is material, you can file a Notice of Proposed Adjustment (this is only available within four months after the filing of an income tax return).

Employers

If you are an employer and are reimbursing employees for work-related travel, the new rates apply to reimbursements made from the date that the rates were issued – 30 May 2025. If your reimbursement policy states that you will reimburse employees at the Inland Revenue rate, you will need to update the rate you pay as soon as practically possible. When rates are increased, a lag in updating rates paid to employees, while potentially disadvantageous to employees, does not cause a PAYE problem. While most rates have stayed the same or increased compared to from last year, note that for this year, the new Tier One rate for Petrol Hybrid vehicles is lower than last year’s single Tier One rate.

If your reimbursement policy states a set rate at which you will reimburse work-related mileage, and this is lower than the new rate, you do not need to do anything as the amount you pay will be tax-free, but you may get pressure from employees to increase the reimbursement rate.

New guidance provided

Along with the new rates, the guidance (OS 19 04 KM 2025) includes a new section to provide additional guidance on the use of the kilometre rates. Confusingly, this additional guidance does not reference the 3,500km Tier One safe harbour threshold in the examples presented.

The standard rule remains, that the Tier One rates can be used for the business portion of the first 14,000km of travel, technically requiring logbooks to be kept establishing that business portion of travel. Operational statements 19/04a and 19/04b both allowed, in the absence of a logbook, for the Tier One rate to be used for the first 3,500 km of business travel. This new guidance and its examples (reproduced below) make no mention at all of this 3,500km threshold, but does refer to 19/04a and 19/04b as providing more detailed information which leave us questioning the continued applicability of the safe harbour.

Example two in particular is relevant – 5,000km of employee travel is reimbursed in this example all at the Tier One rate, with no mention of the work related portion of total travel.

Use of motor vehicle for both business and private (non-taxable) purposes

Businesses that use a motor vehicle for both business and private purposes must calculate the proportion of business use, whether using actual motor vehicle costs (cost method) or the kilometre rates. The new guidance includes a worked example of using the kilometre rates in practice:

Example one – business vehicle (petrol) greater than 14,000 kms travelled - logbook maintained

The business taxpayer uses their petrol car for both business and private purposes. The previous logbook test period calculates that 60% of the travel is for business purposes. The car travelled a total of 20,000 kilometres for the 2024-2025 income year.

Deduction

Tier 1 14,000 x $1.17 x 60% = 9,828.00

Tier 2 6,000 x $0.37 x 60% = 1,332.00

Total deduction = $11,160.00

Source: Inland Revenue Kilometre rates for the business use of vehicles for the 2025 income year

Use of the rates for employee reimbursement for a use of a vehicle

There is a requirement that employee reimbursement for business use of a private motor vehicle be a “reasonable estimate of expenditure” and the kilometre rates have long been accepted by the Commissioner as being a “reasonable estimate of expenditure”, but Inland Revenue now advise that employers need to be aware of factors that may mean this is no longer reasonable.

The kilometre rates are set for a particular income year based on factors that impact expenditure in that period. The rates just published reflect the actual costs of running vehicles in the March 2025 tax year. Reimbursement of expenditure using the 2025 mileage rates is likely to occur in the current (2026) income year. There is potential for actual running costs in the 2026 year to shift in a way that suggests the 2025 rates are no longer a reasonable estimate of the expenditure incurred by employees in the 2026 year. This seems to reflect an extremely micro approach by Inland Revenue which is hard to reconcile with a Government which has a focus on reducing red tape.

The guidance notes that the use of these rates may not be practical based on an employer not knowing the vehicle type that each of their employees are using. In these circumstances the Commissioner accepts a reasonable estimate that may be a blended average of the published kilometre rates, in order to reduce any compliance costs. However, employers need to be comfortable that this is still appropriate in the circumstances and timing of any reimbursement payment. The guidance includes two worked examples of employee reimbursement which may leave you more confused than enlightened:

Example two – reimbursement payment to employee for business use of their own electric vehicle – logbook maintained

A business makes a reimbursement payment to an employee that has a logbook recorded that they travelled 5,000km for business use in their own electric vehicle in the 2025-2026 income year. The employer considers that the Commissioner’s kilometre rates for the 2024-2025 are still a reasonable estimate of expenditure that has been incurred by the employee and decides to use these rates to calculate the reimbursement payment.

Reimbursement payment

Tier 1 5,000 x $1.08 = $5,400

However, the employer is not required to calculate the reimbursement based on the Commissioner’s published kilometre rates and may consider a better reasonable estimate is available from third-party published running costs, actual expenditure or other reasonable sources.

Source: Inland Revenue Kilometre rates for the business use of vehicles for the 2025 income year

Example three – reimbursement payment to employee for business use of their own vehicle (unknown type) – no logbook maintained

A business makes a reimbursement payment to an employee that has used their own vehicle for business use in the 2025-2026 income year. No logbook has been maintained, but evidence is provided of ad hoc short distances travelled for business purposes. The employer has many employees and does not track, nor have records of, the type of vehicle the employee uses.

In this instance the employer is only required to determine a reasonable estimate of the expenditure incurred by the employee for the business use of their vehicle. The employer considers that the Commissioner’s kilometre rates for 2024-2025 are still a reasonable estimate of expenditure that has been incurred by the employee and decides to use an estimate based on these rates to calculate the reimbursement payment. The employer uses an average of the four Tier 1 rates (as the employee has only travelled for business a total of 1,000km in the year) and applies a rate of $1.09 per km for the reimbursement payment (1.17 + 1.26 + 1.08 + 0.86/4).

The Commissioner does not expect the employer to have additional compliance costs and track vehicle types where that is not practical. However, the employer is not required to calculate the reimbursement based on the Commissioner’s published kilometre rates and may consider a better reasonable estimate is available from third-party published running costs, actual expenditure or other reasonable sources.

Source: Inland Revenue Kilometre rates for the business use of vehicles for the 2025 income year.

For more information about applying the new kilometre rates or mileage reimbursement options please contact your usual Deloitte advisor.

June 2025 - Tax Alerts

- Investment Boost: Frequently asked tax questions

- Infrastructure tax changes mooted

- Kilometre rates get an overhaul

- Out with the old, in with IS 25/16: Updated guidance on tax residency

- New Product Ruling opens up public transport FBT exemption

- To be or not to be a mutual association – Inland Revenue proposal to hit not-for-profits

- Navigating the everchanging tides of tariff

- The One, Big, Beautiful Bill – the potential tax impacts for New Zealand residents

- Tax losses and anti-avoidance: Decoding Inland Revenue’s finalised guidance

- Snapshot of recent developments