Delivering the promised returns: Post-Merger Integration (PMI)

Understanding the M&A lifecycle

Closing the deal - getting signatures on the dotted line - is often celebrated as the defining milestone in an acquisition. It is the result of months of effort, and for good reason: it is a moment worthy of recognition. But this is merely one step in a bigger scheme: the M&A lifecycle. A successful acquisition hinges on the many steps and decisions made both before and after signing. In this article we will take a closer look at the final step of delivering the promised returns: Post-Merger Integration (PMI).

Highlights

- Post-Merger Integration (PMI) starts during the initial phases of the M&A lifecycle. Synergies are identified, risks assessed, and governance frameworks established to ensure smooth execution and value creation.

- Involving the integration director early in the M&A process helps optimise valuation, prioritise synergies, and uncover potential dis-synergies—enhancing strategic decision-making.

- Setting up a “clean room” pre-close can be instrumental in involving the integration team early in the process.

- Protecting critical infrastructure is crucial in industries like TMT. Proactive assessments and planning are key to overcoming obstacles.

- Successful preparation for Day 1 (the day the ‘keys’ are handed over to the buyer, i.e., closing) ensures uninterrupted operations during the legal and financial ownership transfer. Long-term integration efforts are critical, requiring a clear strategy to deliver the promised returns.

- Integration approaches vary—from full assimilation to partial integration or add-ons—depending on the acquisition's strategic rationale and the target company’s role in transforming the buyer’s business.

- Prioritising synergies in the first 100 days: developing an integration blueprint and tracking KPIs ensures alignment, focuses efforts on capturing key synergies, and maintains momentum during the critical initial phase of the integration.

Mergers & Acquisitions

Why the earlier stages are vital

Post-Merger Integration (PMI) should start well before closing the deal. As discussed before, synergies between the buyer and the target company should have been identified and evaluated early in the process. The integration director assesses these synergies in detail, determining the timing and feasibility of capturing them. Additionally, preparations for governance, management structures, and control mechanisms are laid out to ensure a smoother transition post-transaction.

The integration director’s role: maximising synergies and minimising risks

To clarify the integration director's role, let’s consider – again - the analogy of buying a house. Just as your construction advisor offers insights into necessary renovations before the deal is signed, a contractor is needed to provide detailed cost estimates. Similarly, involving the integration director is essential during the initial stages - not as an afterthought, but as a strategic partner in optimising the target’s value. Integration directors can play a vital role in forecasting when specific synergies will materialise and incorporating these insights into valuation models. They can also uncover risks and dis-synergies, such as potential customer losses due to the deal, to ensure that value capture is realistic and comprehensive.

Pre-close preparation: The power of a “clean room”

Setting up a “clean room” pre-close can be instrumental in involving the integration team early in the process. Especially when competitors are planning a merger, strict antitrust regulations govern the exchange of sensitive information. The clean room, comprising external advisors and representatives from both parties, serves as an independent entity. It identifies priorities for the merged company in the first 100 days, facilitating a quick start to capture any synergies. However, there are risks to consider. Should the deal collapse, participants in the clean room may be barred from returning to their original roles due to their exposure to competitive information – in other words, they will have to leave the company. This means that a careful selection of representatives is pivotal.

Day 1

Day 1 marks the legal and financial transfer of ownership, but careful preparation is needed to ensure uninterrupted operations. Before closing, all legal and statutory requirements must be met, financial controls must be in place, and the two companies must be able to continue day-to-day operations successfully and without interruption. Integrations often require 200 to 350 tasks, ranging from logistical activities like changing bank accounts and aligning branding to strategic efforts like renegotiating customer contracts and implementing a communication plan. A dedicated integration team should oversee progress and manage interdependencies across deliverables.

Long-term integration efforts

A successful Day 1 sets the tone for the broader integration programme, providing momentum and positive direction. However, merging two organisations is rarely completed in a single day. Long-term efforts are essential to achieving the acquisition’s objectives. As integration carries the greatest risk of value destruction in deals, developing a clear strategy is pivotal for delivering the promised returns.

Integration tactics: tailoring approaches to deal rationale

Successful integration depends on reflecting the acquisition’s rationale. This may involve full assimilation, partial integration, or treating the target as an add-on business.

- Add-On strategy: Acquiring companies to transform core businesses.

- Partial integration: Integrating back-office functions while maintaining autonomy in departments like product development and sales.

- Full integration: Best suited when buyer and target company operate in similar markets.

Timely involvement of the integration director ensures these tactics are executed effectively.

How to preserve innovation and leadership

Acquisitions, particularly of innovative firms, often hinge on retaining key talent and leadership. Identifying these individuals early and involving them from Day 1 post-deal is crucial. While appointing them to clean room roles is possible, regulatory concerns may complicate this approach (see above; they might have to leave the company). A robust talent management strategy is indispensable.

Governance and the Integration Management Office (IMO)

Large-scale integrations demand clear governance structures. Establishing an Integration Management Office (IMO) headed by the integration director ensures alignment across the various workstreams, regions, and functions. The IMO enables cross-functional coordination, addressing aspects like change management and communication. This matrix governance model fosters commitment and involvement at all organisational levels.

The first 100 Days: capturing synergies and maintaining momentum

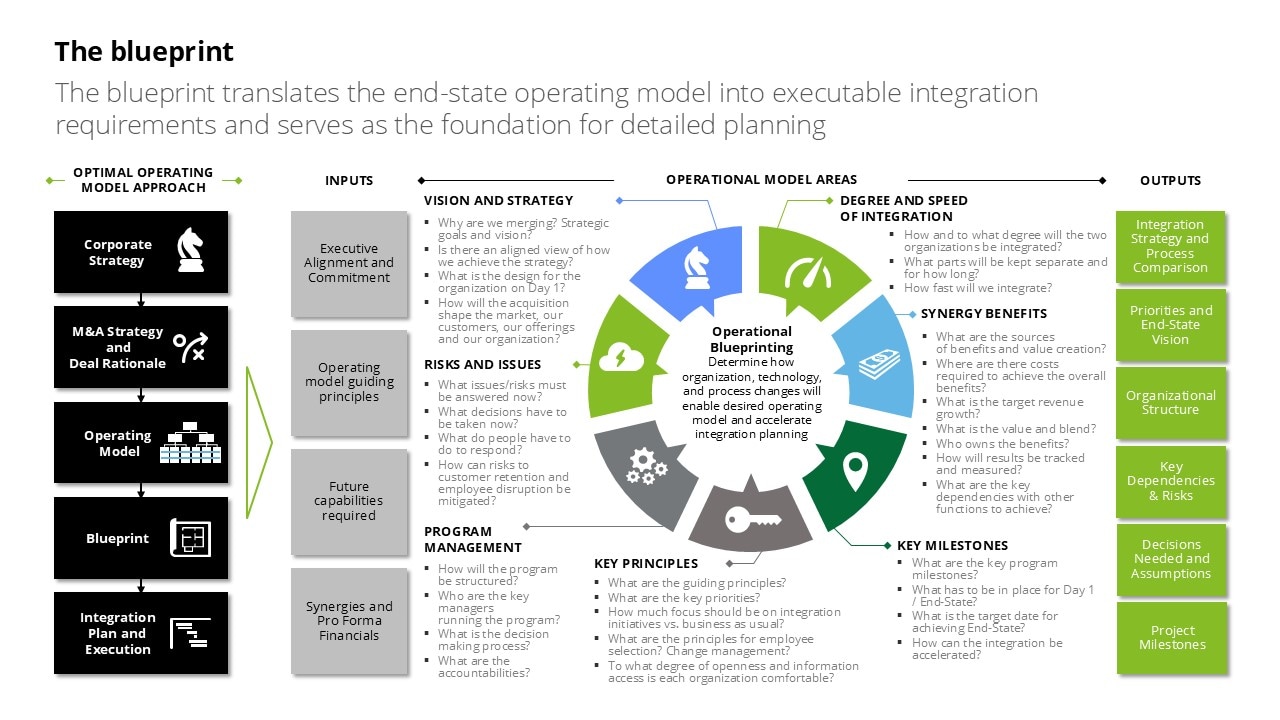

The first 100 days are pivotal in showcasing the synergies of the M&A deal, setting the tone for a successful integration journey. An integration blueprint (see picture below), developed in the early weeks, is vital. It aligns both sides and sets a roadmap for Day 1 preparations. It outlines the strategic rationale, degree of integration, milestones for the first 12 months, risk management strategies, and effective resourcing to align both organisations. Depending on the complexity of the transaction, the integration blueprint can be addressed before signing – but no later than between signing and closing. Prioritising synergy initiatives - such as up- and cross-selling opportunities in telco mergers - is also crucial. Clear KPIs tailored to the target’s business model ensure focused tracking of results and accurate value assessment. Effective communication of the deal rationale and integration tactics enhances organisational commitment and ensures credibility.

Click or tap the image below to view a larger version.

At this point, the M&A lifecycle moves back to the first stage again. Going through the cycle, you have maximised returns and made your transaction a success – not just for now, but for the long term. Your company is ready again to transform and realise greater value, assessing potential disruptors and transformational opportunities.

The M&A cycle in a nutshell

Viewing an acquisition as a series of interconnected phases rather than a one-off transaction is key. From identifying the right deal to integrating the new business into your company. Each decision you make along the way shapes the outcome. Below we have embedded a picture of the M&A lifecycle and a short description of each phase. In a series of articles we delve into each step of the M&A lifecycle, sharing stories and thoughts about each of these phases.

How Deloitte helps TMT companies

We provide comprehensive support throughout the critical post-deal period, ensuring a smooth transition and maximising value creation from Day 1. Our M&A, Strategy & Business Design and Restructuring, Turnaround & Cost Transformation teams can help you to ensure seamless post-deal integration.

Would you like to know more? Please contact us via the contact details below.