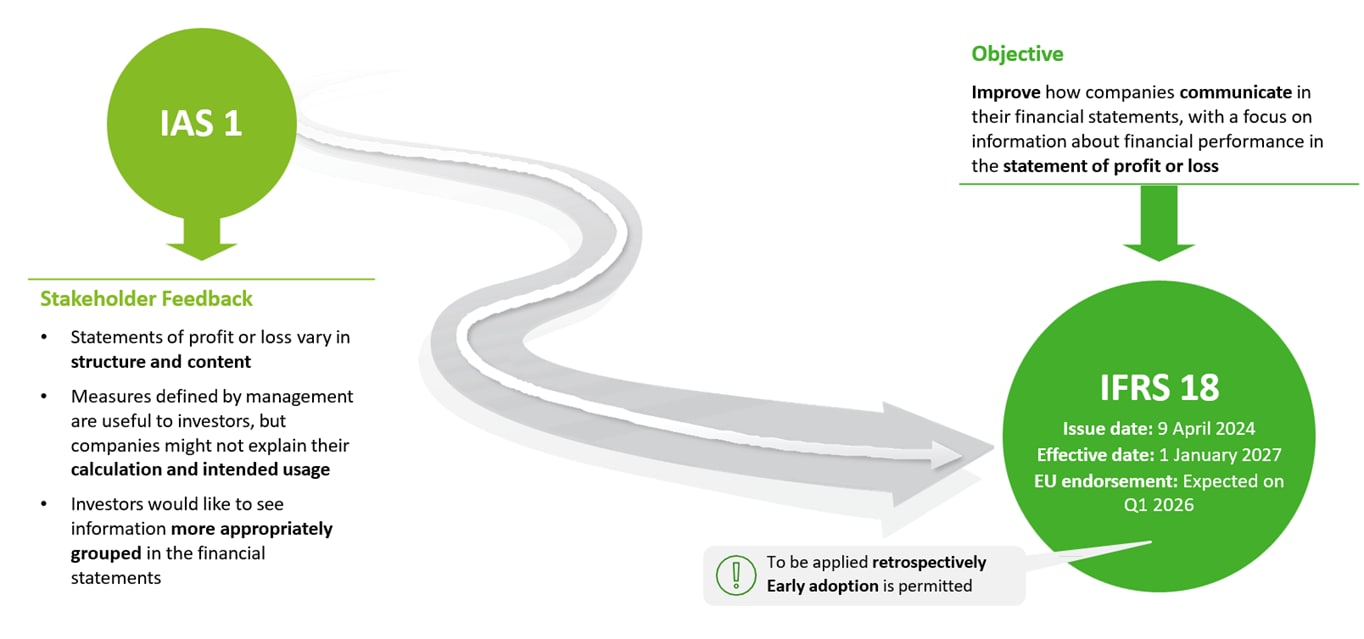

IFRS 18: A new era of transparency and comparability

IFRS 18 marks a new chapter in financial reporting, replacing IAS 1 and introducing significant changes to the presentation and disclosure of financial statements. Issued on 9 April 2024 and effective from 1 January 2027—with endorsement expected for end of the current year—the standard responds to stakeholder feedback calling for greater consistency, clarity, and comparability.

While IFRS 18 doesn’t change how results are measured, it significantly reshapes how performance is presented and interpreted, offering investors a clearer, more structured view of entity’s financial performance. As shown below, entities should prepared for major updates to the statement of profit and/or loss and the notes, some adjustments in the statement of financial position and cash flows, and only minor refinements to the statement of other comprehensive income and statement of changes in equity.

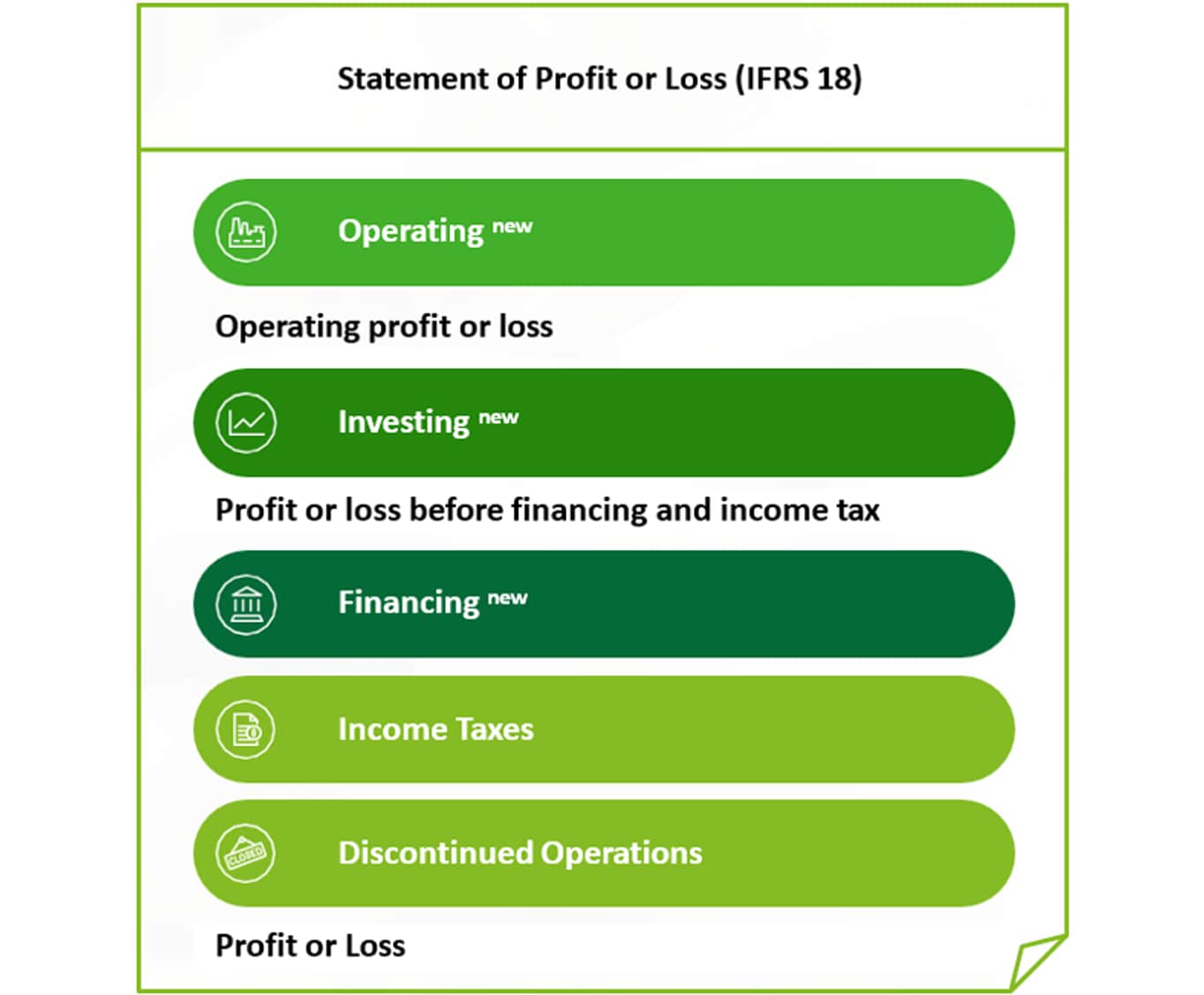

Redefining the statement of profit or loss

Under IFRS 18, income and expenses must now be classified into five categories: operating investing, financing, income taxes, and discontinued operations.

The standard also introduces two mandatory subtotals:

- Operating profit or loss, and

- Profit or loss before financing and income taxes

To help visualize these changes, here’s an example of a Statement of Profit and Loss under IFRS 18.

The distinction between operating, investing, and financing depends largely on an entity’s main business activity, which defines its core operations. For example, interest income may be classified as operating for a bank but as investing for a manufacturer.

Tip: To determine an entity’s main business activity under IFRS 18, focus on the activity that generates most of its revenue and profit, aligns with its management strategy, business purpose, legal documentation, and use of operational resources, and reflects investor expectations.

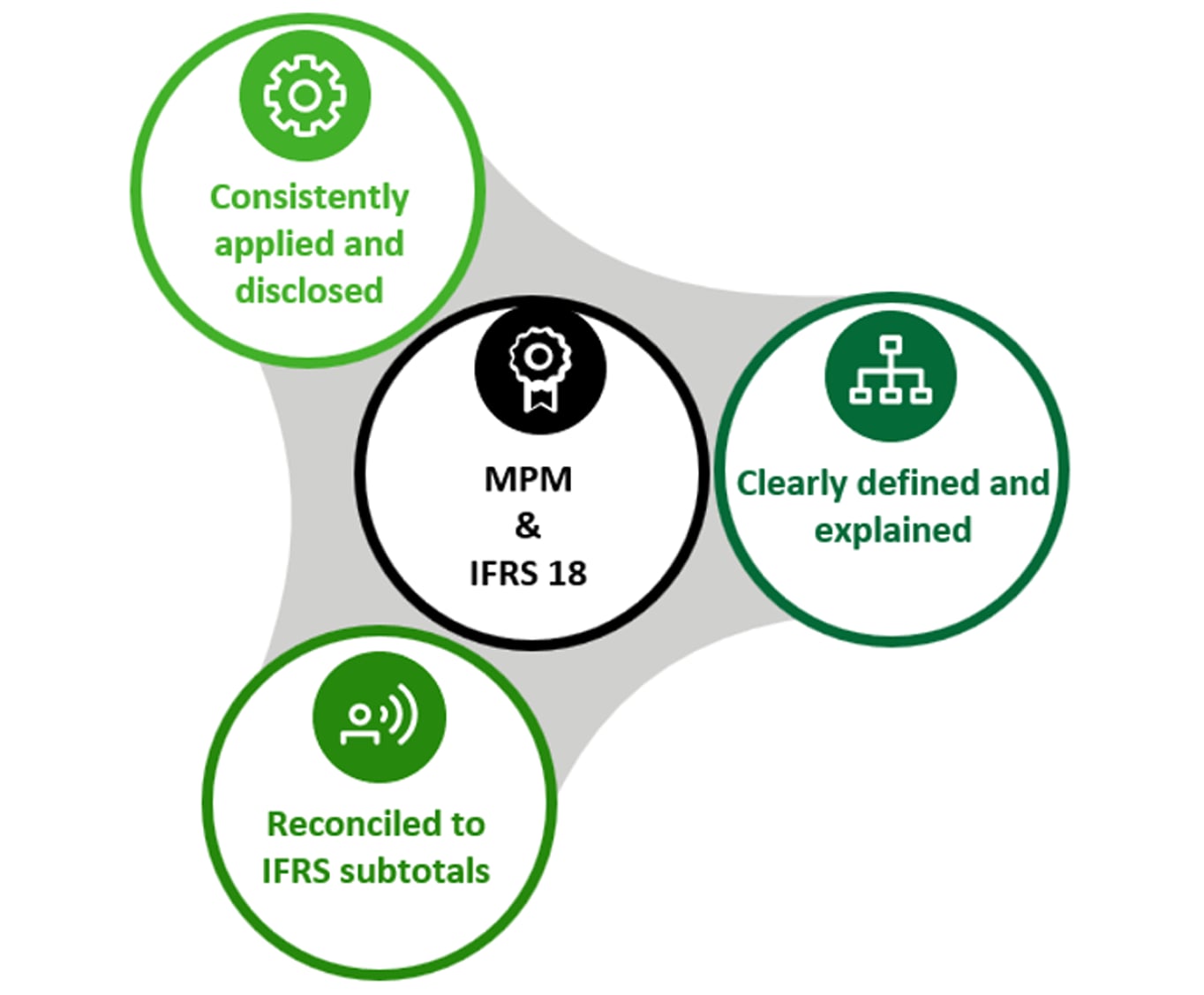

Management-defined performance: Management’s view goes public

One of IFRS 18’s most significant changes is the introduction of management-defined performance measures (MPMs), subtotals of income and expenses publicly communicated by management to communicate how they evaluate an entity’s financial performance. IFRS 18 introduces mandatory disclosure of management-defined performance measures in the notes to the financial statements.

In practice, performance metrics often featured in investor presentations or internal dashboards (e.g., “adjusted EBITDA” or “core operating profit”). This shift will bring greater transparency and accountability, as investors will see how management defines and assesses performance.

Tip: Ensure the finance and the marketing/communication departments are working together to identify KPIs qualifying as MPMs. All MPMs must be disclosed in a dedicated note to the financial statements, and entities should ensure that appropriate controls, processes, and documentation are in place, as these disclosures are now subject to audit.

Aggregation and disaggregation: Finding the right balance

IFRS 18 reinforces expectations around how information should be grouped or separated in financial statements:

- Aggregate items that share similar characteristics,

- Disaggregate items with differing characteristics when doing so enhances users’ understanding.

Shared characteristics |

|

Type |

Example |

Nature |

Operating expenses, revenue, service fees. |

Function |

COGS, Administrative expenses. |

Measurement basis |

Amortized cost, FVOCI, FVTPL. |

Other characteristics |

Short term/long-term, geographic region. |

The aim is to highlight material information in a clear and accessible way, providing users with insights that are sufficiently detailed without overwhelming them with unnecessary granularity. To achieve this balance, entities will need to revisit line items, labelling, and note structures to ensure clarity and consistency.

Tip: Generic categories like “other income” or “miscellaneous expenses” may no longer be adequate. Break these down into meaningful categories when they contain items with different natures or functions.

Same words, different worlds: IFRS 18 versus IAS 7

Although both IFRS 18 and IAS 7 (statement of cash flow) use the terms operating, investing, and financing, the classifications do not always align. A transaction may fall into one category for performance reporting under IFRS 18 and a different one for cash-flow reporting under IAS 7.

Tip: Identify transactions where profit-and-loss classification may differ from cash-flow classification (e.g., foreign exchange effects, interest, derivatives). Thus helps avoid inconsistencies and supports clear, transparent reconciliations.

Systems, processes, and controls for IFRS 18 implementation

To translate IFRS 18 guidance into accurate financial reporting, companies must ensure that their systems, processes, and controls are properly aligned to capture information accurately—particularly in areas such as revenue recognition— and to support full compliance with the new standard. Examples of steps organizations can take to prepare include:

- Revenue recognition software: Implement tools capable of applying IFRS 18 rules automatically, including the categorization of operating, investing, and financing activities.

- ERP integration: Ensure that operational events (e.g., deliveries, milestones) flow accurately into current accounting systems for timely and consistent recognition.

- Periodic reconciliations: Perform regular reconciliations of calculations, and the general ledger to verify accuracy.

- Segregation of duties: Assign responsibilities across teams to reduce the risk of errors or conflicts in revenue recognition.

- Audit trail and documentation: Maintain clear records of judgements, assumptions, and recognition decisions for regulatory compliance and internal oversight.

- Internal review and approvals: Conduct regular reviews and approval processes to ensure IFRS 18 compliance and consistency across contracts and business units.

Tip: Take the opportunity of reporting system projects to ensure your chart of accounts, reporting rules, and controls can capture the new categories and MPM-related information without manual interventions.

Turning compliance into advantage

IFRS 18 is more than a presentation change—it’s an opportunity to enhance how your business communicates performance. Early adopters can strengthen investor confidence, streamline reporting processes, and turn greater transparency into trust and a competitive advantage.

To explore the challenges in more detail, visit our LinkedIn post at the link below for quick insights across multiple industries.

IFRS 18 and you: Readiness checkpoint

Our IFRS 18 readiness questionnaire assessment provide a useful approach to help entities prepare thoroughly for the new standards. A well-structured gap assessment is the essential first step, offering the insight needed to determine scope, prioritize actions, and develop a clear, practical implementation plan.

Evaluate your organization’s readiness for IFRS 18 by completing our Readiness self-assessment questionnaire. Following the assessment, you will receive a free one-hour confidential consultation with our specialist to discuss your results and next steps.

Are your financial statements ready for 2027?

Our experts can help you:

- Assess how IFRS 18 will impact your reporting framework.

- Identify key exposure areas in classification and disclosure.

- Design and implement a tailored transition roadmap.