Evolving partner roles in Industry 4.0

A partner ecosystem can generate customer-ready solutions and accelerate time to market

Introduction

TRADITIONALLY, companies have owned and controlled the delivery of their core product and service offerings. They have analyzed customer needs, led innovation in-house, and delivered their offerings through largely transactional relationships with distribution partners. In the Industry 4.0 era, driven by a shift in customer expectations from product delivery to the enablement of outcomes, companies are increasingly realizing the need to redefine their offerings, accelerate and broaden innovation, and deliver solutions in partnership with ecosystem partners.

Companies are pursuing unforeseen partnerships in order to achieve better customer outcomes, as is the case with Walt Disney World Resorts and Hitachi Vantara, recently named Disney World’s “official ride and show analytics provider.” The two companies have brought together Disney’s entertainment experience and Hitachi Vantara’s intelligent data-driven solutions to increase the attractions’ operational efficiency and customer appeal.1 Many other industrial and technology companies are similarly venturing beyond conventional company boundaries and are leveraging business ecosystems to expand their impact on their end customers’ success.

In this article, 12th in our series on digital industrial transformation, we discuss how a well-defined and managed partner ecosystem can generate customer-ready solutions and accelerate time to market. This article discusses what is changing and why: the drivers and evolution of the partner roles. (The next installment will define how to systematically capture, enable, and sustain the broader set of partnerships required to succeed in a complex Industry 4.0 ecosystem.)

Partnership trends across the value chain

At the heart of the discussion lie the evolutions that company-partner-customer ecosystems are experiencing in the Industry 4.0 age. Partners have moved beyond single-capability roles to play across some or all parts of the value chain. Companies are increasingly using partners to extend owned capabilities across product development, marketing, sales, delivery, and customer success and support.

We have witnessed this evolution from single-capability to cross-value chain capabilities in several specific areas:

- Partners through their IP can fill product gaps or add new features. For example, Google Cloud has partnered with Cisco to provide customers a well-supported integrated platform that enables them to accelerate on-premises app modernization, ease service management, and offer integrated security.2

- Partners with a strong marketing brand or sales team are engaging earlier in the sales demand-and-planning cycle, developing joint go-to-market plans. The vice president of global alliances and sales at Amazon Web Services (AWS) has witnessed a 3.5x increase in opportunity size when working with partners at the front end of the sales cycle.3

- In their role as multivendor implementers, many partners have developed new delivery capabilities with faster and more extensive support for new solutions or use cases. Additionally, a new generation of technology and solution partners are enabling companies to develop new offerings by providing advanced complementary technologies such as data management and analytics, cloud platforms, and IoT Solutions.

Figure 1 depicts how various partners are contributing to the value chain and driving business impact for technology solution providers.

Partner model archetypes

Given the continuously evolving roles partners are playing in a company’s ecosystem, we can characterize them based on not only their type but the way they add value to, and collaborate within, a company’s value chain. Our approach to characterizing partners is based on their level of integration and the strategic nature of their partnership (figure 2). The level of company-partner integration indicates how intricately the partners are engaged with the company’s value chain and how critically they extend the company’s capabilities. The strategic partnership nature reflects on how the partnership affects the companies’ positioning in the market, their market offerings, and their business models.

Selling allies bring ready-to-use solutions to market and manage the bulk of the customers, aiming to be primary purchasing advisers for their customers. This partnership allows companies to expand customer reach using partners as an extension of the sales team to grow footprint and lower cost of sales. Key considerations for choosing a selling ally include the partner’s ability to:

- Facilitate the quote-to-fulfillment process with the end customer

- Influence customers to make the purchase

- Maintain customer relationships through renewal/cross-sell/upsell motions

- Provide a perspective on product performance for specific customer needs

Typically, we see value-added resellers (VARs) and distributors play these roles. Cisco Systems’ application performance monitoring software arm, AppDynamics, exemplifies how companies’ selling models have changed drastically with the addition of the selling allies in their ecosystem. Direct selling to business customers comprised about 80% of AppDynamics’ business merely four years ago. Today, with approximately 70% of AppDynamics transactions handled through a partner ecosystem, the numbers are quite different. In just one year, the company has seen not only a 60% increase in deal registrations from partners but a dramatic 154% boost in year-over-year growth in partner-sourced business.4 World Wide Technology, a Cisco Gold Partner and AppDynamics Titan partner, has taken a step further than provisioning services for deploying AppDynamics licenses, creating its own practice around AI-based and application performance monitoring operations.

Delivery champions streamline services delivery to extend existing capabilities. Such partners support companies to scale their delivery capabilities, reduce delivery costs, build complementary skills, and develop extended solution offerings. Key considerations for choosing a delivery champion include the partner’s ability to:

- Translate business requirements and customer pain points into a technology solution, and then deliver the solution to the customer

- Customize support single/multiproduct solutions to customer needs

- Support the adoption of solutions through training and customer success

- Deliver services from offshore locations with lower costs while maintaining service quality

Typically, we see global and regional systems integrators, managed service providers, and professional services firms play these roles. Companies such as SAP, Oracle, and Salesforce rely on global system integrators such as Deloitte Consulting, Accenture, Tata Consultancy Services, and Infosys to deliver their solutions to end customers at competitive prices.5

Companies have been leveraging sales (selling allies) and delivery (delivery champions) partnerships for several years now. Typically, companies are able to support end-to-end business transactions with these partner archetypes. But is that enough? To stay relevant in the market, companies will need to continuously develop new capabilities, enable leading technologies, and provide a seamless experience. It is crucial for companies to take a partner-first approach to attract beneficial and long-lasting partnerships.

Therefore, in parallel to augmenting sales and delivery capabilities of companies, partners are evolving their roles and growing their ecosystems with a varied set of capabilities. This introduces two new partner archetypes in the market:

Ecosystem pioneers drive new revenue in offering areas (for example, Internet of Things products) and new business models (for example, anything-as-a-service offerings) by going to market with a customized, often joint IP solution. This partnership allows for many companies to increase the total value to the customer beyond the existing solutions by integrating with partner solutions.

Key considerations for choosing an ecosystem pioneer include the partner’s:

- Ability to build offerings that extend the company’s product capabilities

- New offerings integrating one or more partners’ IP

- Marketing IP in conjunction with one or more partners

AT&T is partnering with seven major companies to develop connected communities starting in Dallas, Atlanta, and Chicago. The development plan begins with smart utility meters, water leak detection, and industrial lighting. It then moves on to leverage its partnerships to develop solutions within infrastructure, citizen engagement, transportation, and public safety, including new-age features such as intelligent parking and digital signage. This change and the partnerships for it represent a significant step for AT&T and will go a long way in shaping how crucial partnerships are for development. AT&T leaders have acknowledged the partnerships’ pivotal roles in the project.6

Cocreators are strategic partners that actively collaborate to create and deliver customer-centric products and services. Cocreators often bring together their unique intellectual properties, market-leading capabilities, and product or service expertise to develop differentiated and specialized solutions to address customers’ changing needs. Such partnerships tend to capture greater market value at a more rapid pace than traditional product development approaches.

For instance, partners specializing in capabilities such as hyperscale infrastructure, data management, artificial intelligence, etc. can help medical device manufacturers and life sciences companies accelerate development of innovative solutions such as telemedicine and new disease remedies through cocreation.

Key considerations for choosing a cocreator include the partner’s:

- Level of engagement in building the offering

- Strategic market position with the target customer base

- Ability to bridge a critical gap in the company’s capabilities

For example, HP Enterprise and SAP have a strong strategic partnership in which they are committed to coinnovate and leverage integration of an extensive portfolio of the right-fit assets. HPE’s SAP-focused assets and solutions, combined with its extensive SAP services team and partner program, provide for a fully integrated approach for HPE customers.7 Extending the partnership, HPE has an as-a-service solution for SAP HANA bundling the HANA software licenses with hardware and ongoing management into a complete solution.8 With their continuous engagement, HPE and SAP share 25,000 joint customers worldwide, and 46% of SAP licenses run on HPE systems.

Fluidity of partner archetypes

Partners are continuously exploring additional revenue streams and profitability prospects as partner roles are evolving. Multiple economic, technological, and consumption drivers are causing traditional channel partners to rethink their position in the value chain and explore avenues for movement across the value chain. Some of the prominent drivers include:

Propensity to capture higher value: With aspirations of consistent business growth and staying relevant in the technology value chain, channel partners are increasingly exploring adjacent business dimensions and are innovating to develop new business opportunities, therefore, driving incremental revenue and profitability.

Evolving technological landscape: Demand for cloud and analytics-based solutions is witnessing higher uptake as customer and operational data increasingly fuels business innovation. Technologies such as machine learning, augmented and virtual reality, and IoT are making their way into mainstream technology implementations. To address these shifts in offerings, channel partners are playing an increasingly broader role beyond being selling allies and delivery champions, in order to thrive in the changing paradigm.

Changing customer preferences: As customers are shifting their focus from buying products and services to buying business outcomes, customer success initiatives are finding their place in every provider’s value proposition. Channel partners are increasingly complementing providers in driving these initiatives with data-driven insights and new avenues to enrich customer interactions throughout their journey. They are collaborating with providers more intimately throughout the customer life cycle to optimize solutions based on changing customer needs and priorities.

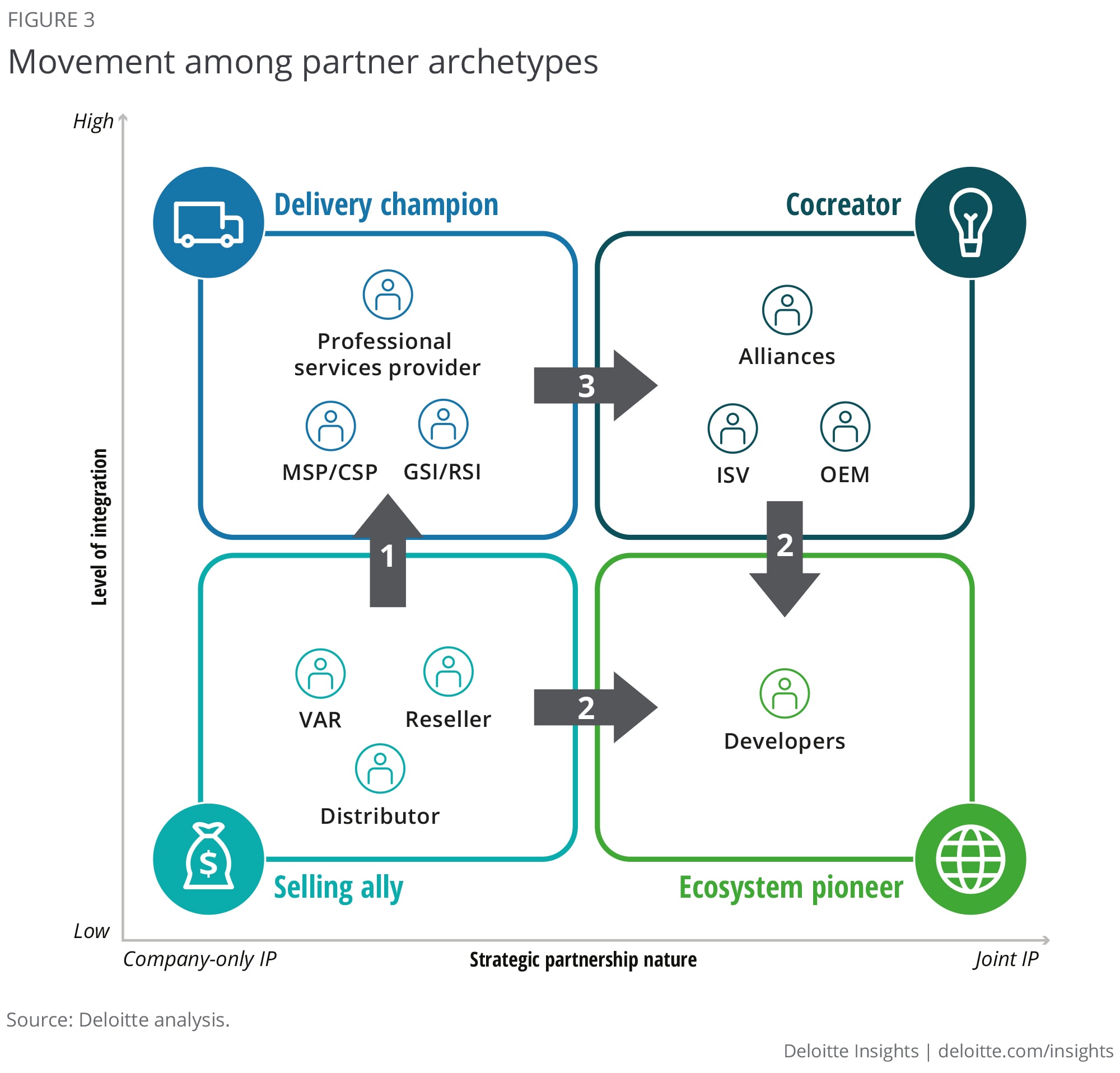

We see increased fluidity in the way partners operate in the value chain and how they move beyond the traditional archetypes. Depending on the offer, ecosystem, and aspirations, partners may respond in one of several ways: reposition themselves in the value chain, evolve their capabilities and market positioning, play different roles in different ecosystems, or change their model altogether. Companies will need to be aware and leverage these partner archetype evolutions and adapt quickly to treat partners based on their new capabilities and skill sets.

Three of the most common moves we have observed:

Selling ally to delivery champion: Many legacy sales partners have undertaken this evolution. Resellers are building internal capabilities to be able to offer customers service delivery (for example, managed services, change management, process reengineering, reporting, and analysis), thereby extending their focus toward being delivery partners. We have witnessed industry-leading value-added resellers enhancing their capabilities in service delivery and developing unique solutions for niche markets in order to transform their business model from selling ally to delivery champion.

For example, US-based Arrow Electronics, one of the world’s largest distributors and service companies of electronic components and computer products,9 has been moving from being a traditional distributor to an ecosystem pioneer in technology solutions. Among the latest of its initiatives, Arrow Electronics has partnered with IBM to reinvent airport operations with a new IoT solution. The solution leverages a set of IoT sensors and gateways designed and sourced by Arrow along with IBM’s flagship Watson IoT platform and Maximo enterprise asset management software.10 Arrow is investing heavily in developing its capabilities, especially its digital platform, IoT practice, and software and cloud solutions.

Selling ally and/or cocreator to ecosystem pioneer: Some partners leverage their domain and industry expertise to develop innovative new offerings; an example here is a network infrastructure partner for a telecommunication company creating its own smart connectivity solution. Such partners move beyond their conventional roles to carving out new markets, thereby moving toward becoming ecosystem pioneers.

Ingram Micro is taking significant steps in this direction: Once a distributor, the company now refers to itself as a solution aggregator.11 It’s leveraging the newly launched cloud commerce platform Cloud Blue to make way into the market of independent software vendors and IP builders. The company is leveraging the cloud to commercialize the solutions built by many of its smaller partners.

Delivery champion to cocreator: As these partners augment companies’ delivery capabilities, they themselves gain access to the value chain as well as the customers. To address these customers’ rapidly changing needs, more delivery champions are stepping up in their role and developing unique product and service capabilities. They are repositioning themselves as strategic partners, to support companies with development of innovative offerings and capturing greater value than with the traditional partnership models.

For example, in 2017, Deloitte collaborated with innovation and design company McLaren Applied Technologies to build data-driven products. Together, they paired Deloitte’s data and analytics experience with McLaren’s engineering, sensor, simulation, and analytics capabilities to develop three different market offerings.12

The infrastructure of partnership

With partners constantly redefining their roles in the market, companies will require a well thought out and comprehensive approach to support and manage their partnerships as well as the underlying dynamics and transitions. As such, they will need to enable four cornerstone elements13 to set up a long-lasting and flexible partner infrastructure and stay ahead in the current disruptive environment:

Clarify and customize the value proposition to each partner archetype: In Industry 4.0, companies that merely provide basic partnership advantages will not thrive. Leaders can no longer consider a one-size-fits-all approach while developing a value proposition and engagement model within their ecosystems. Since the needs of each partner archetype are different, the value propositions must be tailored to set them up for success. And with each evolution, companies will need to continuously revisit the value proposition to attract and retain strong partnerships.

Design a partner program with a foundation that’s consistent but flexible enough to cater to evolving archetypes: Companies also must consider capabilities such as seamless partner fulfillment, support, partner commissions, and partner success. To build such capabilities, companies must invest heavily across the entire partner journey, via tools and programs for not just one but various factors such as partners’ seamless experience, cost reduction, better margins, assistance with customer acquisition, or solution delivery. To support the partner archetype fluidity and provide an easy transition, companies will need to focus on introducing leading technologies and limiting customization efforts.

Launch a flexible yet simple incentive structure: The days when partners wanted to be incentivized based on only one-time selling or deploying are close to vanishing beyond the horizon—now they expect to be compensated based on their roles and contributions. With changing roles, partners are not just supporting sale of products or one-time delivery of services—they are supporting consumption-based models. They are helping drive usage of deployed solutions by working closely with customers and often creating renewal opportunities. Therefore, companies need to identify relevant and flexible financial metrics to incentivize partners based on their archetypes with the ability to offer bundled incentives.

Augment financial metrics with leading customer and enablement metrics: In this continuously changing ecosystem, it is crucial to periodically evaluate partnerships and adapt to the changing business, customer, or partner needs. Keeping a tab on traditional business performance metrics such as revenue growth, profitability, and product mix is insufficient in the evolving ecosystem. It is critical to continuously monitor the pain points and motivations of end customers as well as channel partners, enabling partners to drive better customer outcomes. Therefore, leaders will need to define key performance indicators per partners’ changing roles, capabilities, and value delivered.

Conclusion

In the Industry 4.0 era, with customers increasingly expecting delivery of business outcomes, companies are realizing the need to redefine their offerings, accelerate and broaden innovation, and deliver outcome-oriented solutions in collaboration with ecosystem partners. Collaboration with partners is required across all dimensions of the business, functional and technology stack (e.g., infrastructure, application, data, and management layers) and all stages–from design and architecture to deployment, integration to ongoing operations. Leaders in this environment must understand the roles they and each partner can play, and work on developing the engagement models to fit the growing complexity and agility in the partner ecosystem.

“The size, scale and pace of change is greater than ever before. Companies need to reimagine the ecosystems necessary to deliver outcomes, and their role within. And, establish partnering as a strategic competency,” says Dave Couture, Deloitte Consulting’s global managing partner for technology strategy and partnerships.

New players are coming in, existing players are expanding their roles, companies are expecting more value, and ecosystems are getting more complex. With more changes soon to come, companies and partners need to work together in an integrated manner. Failing to do so may lead them to be left behind in the ecosystem of Industry 4.0.

What’s coming next

As part of this series of articles focused at guiding leaders through digital transformation in the Industry 4.0 revolution, we have laid out a foundation of how technological applications, customer behavior, and partner ecosystems are changing constantly, requiring businesses to reinvent themselves in order to adapt and thrive.

The next article in the series will elaborate on how your business can systematically establish and sustain the infrastructure of partnerships required to succeed in a complex Industry 4.0 ecosystem.

Deloitte Consulting

Deloitte Consulting LLP’s digital transformation practice has advised clients in the technology sector (e.g., hardware and software) as well as those in the industrial sector (e.g., manufacturing, construction, and energy) enter and compete in new growth areas. Our work includes defining customer-first strategies, building new business and operating models, and launching the critical capabilities required to swiftly drive scale—all to achieve optimal results from limited resource pools.