Investment Monitor – The next investment boom

The investment pipeline is increasingly being supported by growing demand for data centres and the renewable energy transition.

Although business investment in Australia remains weak, the major project pipeline is being supported by structural growth opportunities, according to Deloitte Access Economics’ latest Investment Monitor report.

Business confidence is close to its highest level since late 2022, but this has yet to flow through to investment intentions. Many businesses remain focused on managing costs and withstanding economic uncertainty rather than expanding capacity. Non-mining investment as a share of the economy has fallen close to levels not seen since the early 1990s, reflecting softer profits, higher financing costs and ongoing volatility.

The total value of projects in the Investment Monitor database was just under $1.2 trillion in the September 2025 quarter, 7% higher than a year ago. While challenging conditions are weighing on business investment, the project pipeline is being supported by structural growth opportunities – including the global AI race and the transition to net-zero.

Technology firms are racing to build the physical infrastructure needed to unlock the full potential of AI. Investment in data centres is surging globally. Australia now hosts more than 250 data centres, making it the fifth-largest provider globally. Australia’s abundant renewable energy, vast spaces, skilled workforce, and fast-growing data centre demand are expected to attract further investment from global players.

The Investment Monitor database currently includes over $37 billion worth of data centre investment in Australia, an increase of 60% over the past 12 months. This includes four projects, worth a total of $4 billion, that are currently under construction and another 15 projects, valued at a total of $33 billion, which are in the various planning stages.

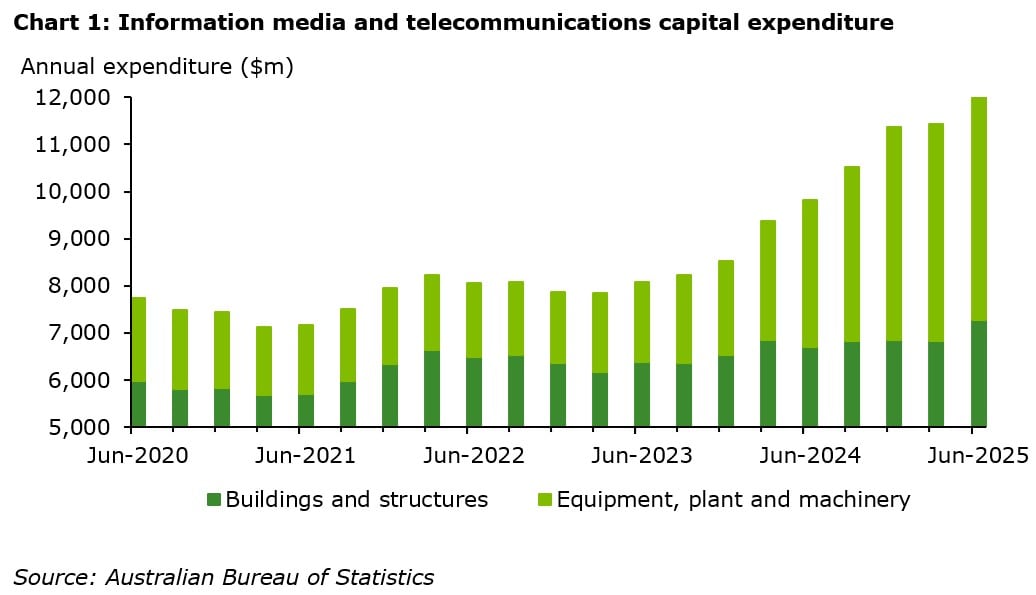

These trends are already starting to show up in investment spending data. Capital expenditure in the information media and telecommunications (IT) industry has surged over the past two years as data centre facilities have been built and equipment purchased to support their operation. Real annual expenditure on buildings and structures has risen by 14% since June 2023 while spending on equipment, plant and machinery has skyrocketed by 191%. A national data centre strategy is set to be released by the Federal Government at the end of the year to guide expansion of the industry and ensure foreign investment guidelines are appropriate for its rapid growth.

The impact of the AI race goes beyond the IT industry. The rapid expansion of data processing activity is expected to place additional pressure on the national electricity grid, boosting demand for renewable energy infrastructure. The utilities industry has already become the main driver of Australia’s investment pipeline, accounting for 37% of the value of planned investment in the Investment Monitor database, up from 28% just 12 months ago. The AI race is likely to see Australia’s renewable energy investment task grow larger still.

The September edition of Investment Monitor also shows a promising shift in the composition of investment. While the public sector has been the main driver of project investment in recent years, the private sector accounted for more than 80% of the value of new projects added to the database in the September quarter. This trend will be critical to Australia’s economic recovery as public sector spending faces tighter fiscal constraints across different levels of government.

Although business investment is expected to remain a weak spot in the Australian economy in coming quarters, the surge in data centre and renewable energy projects is bolstering the medium-term outlook.

This newsletter was distributed on 13th November 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Daniel Kelly, Economist at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings: