Inflation surprise changes the outlook for interest rates

Keeping inflation sustainably within the target range will take longer and may require a more prolonged period of restrictive monetary policy than anticipated a few months ago.

The Reserve Bank of Australia’s Monetary Policy Board decided to hold the cash rate at 3.6% on Tuesday. Last week’s inflation print effectively ended any chance of a rate cut at the Reserve Bank’s Cup Day meeting and – with labour market conditions easing more than expected – has brought the Reserve Bank’s dual mandate of balancing inflation and full employment sharply into focus.

Headline inflation reached 3.2% over the year to the September quarter, which was significantly stronger than the forecasts implied by the Reserve Bank’s August Statement of Monetary Policy (SoMP). Stronger headline inflation was expected in September with the unwinding of cost-of-living support measures, such as electricity rebates. However, the strength of underlying inflation (3.0% over the year to September) surprised many, including the Reserve Bank, and is of greater concern.

At 1.0% over the quarter, underlying (trimmed mean) inflation was notably higher than had been anticipated. While part of this is expected to be transitory, the Reserve Bank admits that there could be more underlying inflationary pressure than previously thought, including across dwellings, market services and some less persistent items such as travel.

The combination of stronger-than-expected inflation and a softening labour market brings back into focus the Reserve Bank’s dual mandate. Inflation rising while unemployment also edges higher represents an uncomfortable trade-off – one that has not featured prominently in recent years.

For much of the past two years, labour market conditions in Australia have been extraordinarily tight, driven by strong population growth and the expansion of the non-market sector. The relative stability of labour market conditions has allowed the Reserve Bank to focus its attention squarely on inflation – understandably so, given the peak of headline inflation at 7.8% over the year to December 2022. This meant that the Reserve Bank has been able to raise interest rates, without a significant impact on the unemployment rate.

Now, however, labour market conditions are cooling; the unemployment rate has increased and employment growth has slowed. The unemployment rate increased to 4.5% in the month of September, higher than expected in the Reserve Bank’s August projections. Should this trend continue, the Reserve Bank would face a delicate balance act in which both inflation and unemployment would be drifting higher – a combination that complicates the policy outlook and tests the limits of its dual mandate.

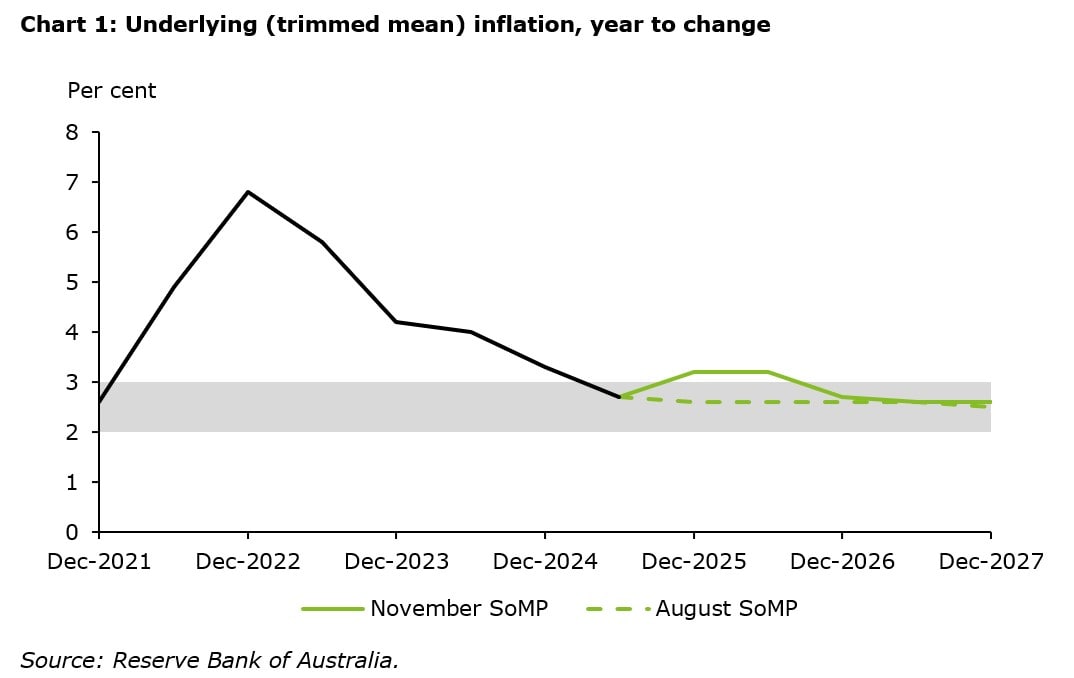

However, for now the current focus still sits with inflation. The latest forecasts released alongside the Reserve Bank’s decision on Tuesday revealed that underlying inflation is not expected to return to the 2-3% range until the second half of 2026. This is a meaningful shift from the August forecast, which had underlying inflation already within target by September and remaining there for the remainder of the forecast period. If the Reserve Bank’s forecasts are realised, it suggests limited scope for further rate cuts in the near term. Or, as Governor Michele Bullock acknowledged on Tuesday, the current easing cycle may already have run its course.

The revision to the outlook for inflation is largely driven by the Reserve Bank’s reassessment of spare capacity in the economy (the gap between supply and demand). In easing cycles, the intention is to create slack to bring inflation down. However, recent data – including measures of firms’ capacity utilisation, the persistence of services inflation, and continued signs of tightness in the labour market – indicate that pressures may be more entrenched than previously assessed. This has led the Reserve Bank to conclude that keeping inflation sustainably within the target range will take longer and may require a more prolonged period of restrictive monetary policy than anticipated a few months ago.

This newsletter was distributed on 7th November 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Tom Harding, Manager at Deloitte Access Economics.

Read our latest publication: The Value of Mortgage and Finance Broking 2025

Click on the links below to read our previous Weekly Economic Briefings: