Deloitte Access Economics’ Business Outlook: Green shoots in a world of worry

Green shoots are appearing in the Australian economy, with decelerating inflation, real wage gains and stronger household spending hinting at a long-awaited recovery. But an economic spring is far from guaranteed.

For all the hardship Australians have endured since the pandemic, there are now tentative, early indications that the economy is finally emerging from the challenges of recent years.

That does not suggest that boom times are ahead. Those green shoots point to growth, but it will remain a grinding and gradual recovery. The latest edition of Deloitte Access Economics’ Business Outlook outlines that the Australian economy is anticipated to grow by 2.2% per year, on average, over the next decade. That compares to average annual growth of 3.3% recorded over the three decades prior to the pandemic.

Slower economic growth is not just an Australian story. Since the beginning of this century, global economic growth has been below 3% on just seven occasions. Over the coming decade, Deloitte Access Economics does not expect global economic growth to exceed 3% in any year.

The challenges facing the global economy are enormous. Several decades of progress knitting together complex supply chains designed to reduce cost for the benefit of consumers is being disrupted. Populations are ageing and birth rates are plummeting, yet most government budgets are ill-prepared for the consequences. High levels of debt, modest wage growth and surging asset prices are worsening an existing societal divide.

A small open economy such as Australia has always been at the mercy of the prevailing global economic conditions of the day. It just so happens that the global economy today is a world of worry.

However, global headwinds, at least in the short term, are expected to be mitigated by a more favourable economic environment domestically.

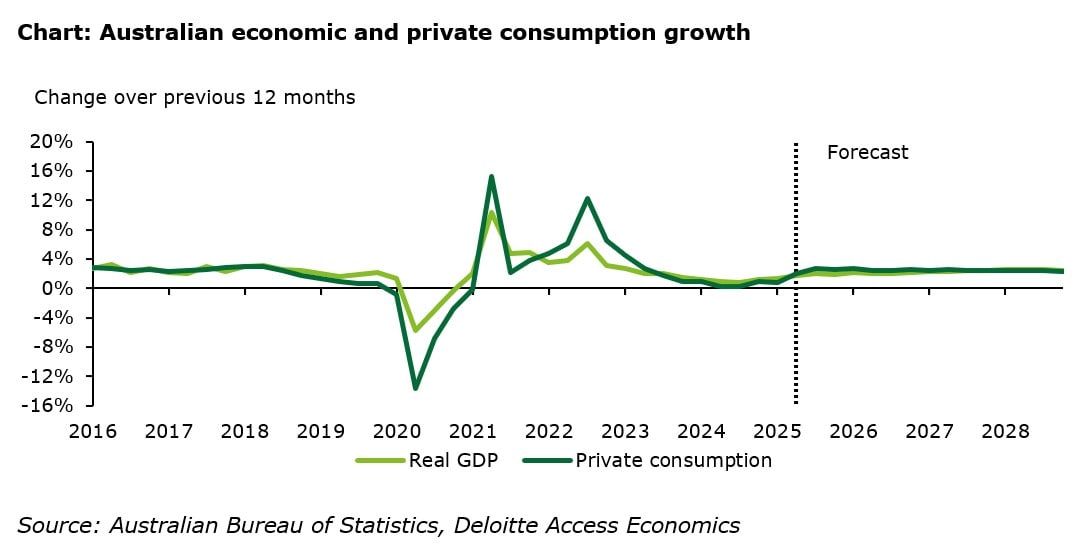

Deloitte Access Economics forecasts real economic growth of 2.0% in 2025-26, accelerating to 2.2% in 2026-27 as interest rates and rising real wages add to household incomes while government spending continues to support the economy. In the absence of increased business investment, this momentum is unlikely to be long-lived.

Rate cuts have been central to improving household spending. A single 25 basis point interest rate cut is worth nearly $1,700 a year for the average new borrower. Subsequently, Deloitte Access Economics expects real household spending growth to improve from the 1.0% recorded in the 2024-25 financial year to around 2.5% in both 2025-26 and 2026-27, comfortably faster than broader economic growth in those two years.

Supporting this scenario is a predicted further 25 basis point cut by the Reserve Bank of Australia at its meeting in December, followed by two more in 2026. These moves, alongside real wage gains from a resilient labour market, should continue to support household cash flows and spending capacity.

However, the rate-cutting cycle will eventually end and employment growth, heavily supported by government spending in recent years, is already slowing.

A lift in private sector activity will ensure the economic recovery doesn’t run out of steam as the rate-cutting cycle draws to a close in 2026 and budget-constrained governments pull back on spending growth.

Future prosperity hinges on encouraging businesses to invest more. The recent Economic Reform Roundtable showed there is no shortage of ideas, but waiting until 2028 to act on tax or investment reform would be too late.

One important outcome of the Roundtable was the general recognition of the rising scourge of intergenerational inequality in Australia. The health and wealth of young people in Australia relative to their forebears is a significant and worsening issue. Efforts to arrest and correct that trend make for good policy.

On Deloitte Access Economics’ numbers, the 2025 election was the last in which the combined voting power of Builders, Boomers and Gen Xs outweighed that of Millennials, Gen Zs and Alphas. By the time of the next election in 2028, the younger generations will hold the majority.

This demographic ‘tipping point’ is an example of why the job of reform is never complete. It cannot remain dormant for long periods, nor be ‘set and forget’, nor be driven by ideology. And there is no single individual or group who have a monopoly on good ideas.

In that context, a regularly convened or annual Roundtable, which hashes out policy concerns, reform options and the best response to Australia’s economic and social issues, would be valuable.

This newsletter was distributed on 8th October 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Alex Scaife, Maanger at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings: