Tourism’s post pandemic evolution

Australia’s tourism industry continues to strengthen, evolving in ways that may provide greater resilience and sustainability in the years ahead.

Australia’s tourism industry is nearing a full recovery following the pandemic related downturn. Domestic visitor numbers have returned to pre-COVID trends and are growing, with households balancing demand for affordable travel against cost-of-living pressures. In the year to March 2025, domestic overnight visitation reached 114 million, exceeding pre-COVID levels for the third year in a row, while at the same time total domestic visitor spend reached $109 billion (151% of pre-COVID levels).

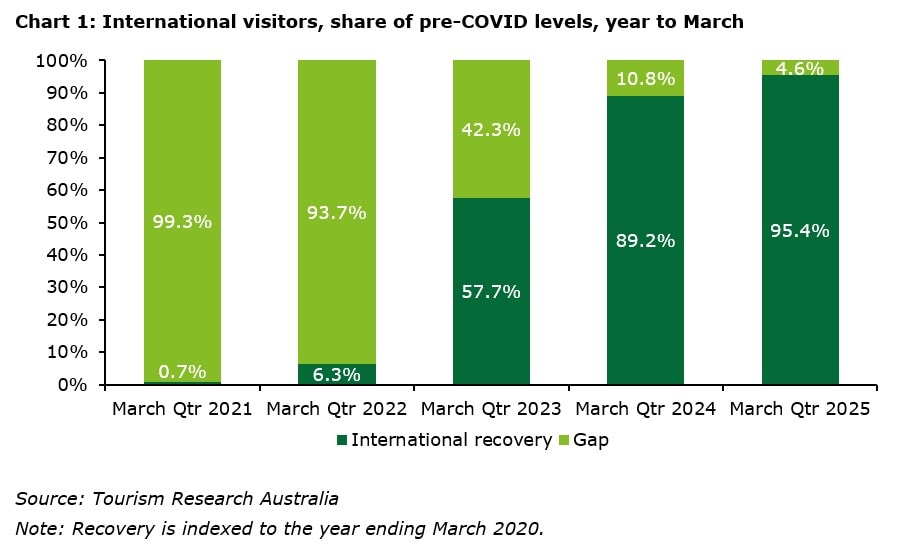

International visitation is also closing in on full recovery. As of March 2025, Australia welcomed 7.6 million international visitors – 95% of pre-COVID levels (Chart 1). While slower to rebound due to capacity constraints and global economic sluggishness, international travel is finally bouncing back, supported by restored aviation links, government marketing campaigns, and renewed global appetite for long-haul trips. The better news is that international visitor spend in Australia has already exceeded pre-COVID levels by 24%, or $35 billion, supported by rising costs of travel.

The sector’s employment footprint has also expanded. As of July 2025, there were 702,800 filled tourism jobs – around 120,000 more than before the pandemic – highlighting the industry’s growing economic contribution.

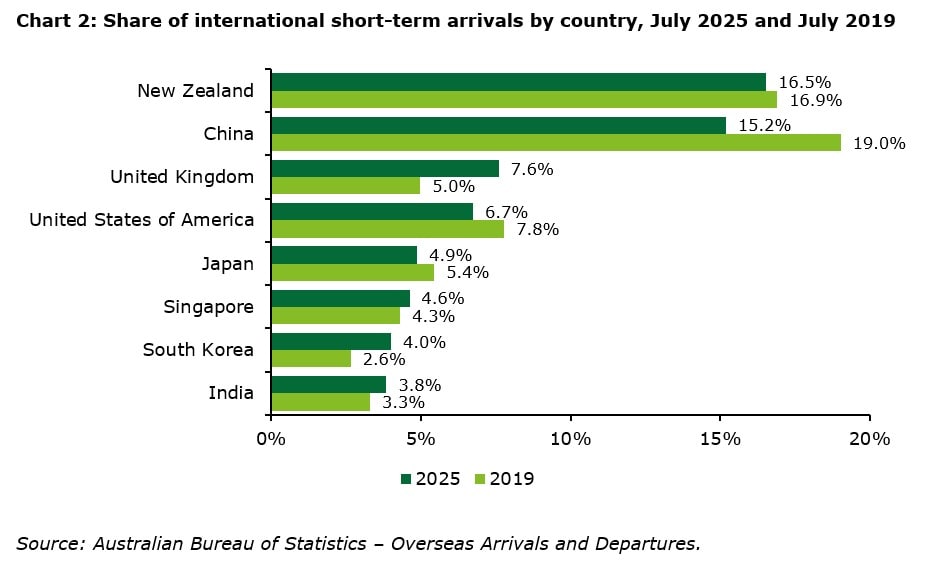

However, not all source markets are recovering equally. The United Kingdom has surged, with arrivals in July 2025 at 144% of July 2019 levels, now making up 7.6% of total arrivals (up from 5.0%). This reflects strong outbound demand from the UK, supported by restored airline capacity.

South Korea has also grown rapidly, now representing 4.0% of international short-term arrivals, compared to 1.6% in July 2019. According to Tourism Research Australia (TRA), increased aviation capacity and rising demand from younger, independent travellers have underpinned this expansion.

By contrast, China is no longer Australia’s largest source market, now overtaken by New Zealand. Arrivals from China have only returned to 75% of July 2019 levels, reflecting a later reopening of outbound travel and ongoing capacity and policy constraints, such as limits on group travel.

Domestic tourism continues to anchor the sector, with both interstate and intrastate trips above pre-pandemic volumes in many regions. Australians are travelling more frequently for short breaks, especially to coastal and regional destinations, while outbound international travel has returned more cautiously under cost pressures. The rebounding popularity of “holidaying at home” has provided critical support to local economies and tourism operators.

Beyond recovery, some long-term trends are reshaping the industry. Sustainable and eco-tourism is growing strongly - TRA data shows the number of domestic overnight tourists undertaking outdoor and nature-based activities increased by 27% between 2018 and 2024. Regional operators are benefiting, while tourism businesses are investing in greener practices to meet rising consumer and regulatory expectations.

Looking ahead, the outlook for Australian tourism remains strong. According to Deloitte’s ConsumerSignals, almost one in four (38%) Australians are planning to book a domestic flight in the next three months and almost a third intend to book an international flight (28%). TRA’s 2024-29 forecasts also anticipate inbound and domestic tourism to strengthen. International travel to Australia is expected to exceed its pre-pandemic level in 2026 and domestic travel is forecast to pick up more sharply from 2026 onward. While higher travel costs and slower global growth may act as headwinds, travel continues to hold a strong place in household budgets.

This newsletter was distributed on 18th September 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Ethan McArthur, Manager at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings:

- Retail Forecasts – We’re halfway there (12 Sep)

- National Accounts: Australians’ living standards gain ground (3 Sep)

- Economic Reform Roundtable: The start of a conversation (29 Aug)

- Australia’s Youth Agenda Economic and policy imperatives (27 Aug)