Retail Forecasts – We’re halfway there

We’re halfway there: consumer confidence has lifted, but real wages remain below their peak and consumers are still relatively cautious.

Retailers are enjoying their strongest outlook in years, buoyed by rising consumer confidence, falling interest rates and growing real wages. Yet the recovery remains slow, with years of lost purchasing power still weighing on households. Confidence is improving, but households have yet to fully open their wallets. For the moment, we’re halfway there.

According to the September 2025 edition of Deloitte Access Economics’ Retail Forecasts, the extended cost-of-living crisis has left a hangover of more cautious consumer behaviour. Real wages are nearly 6% below their peak and consumer prices rose by almost a quarter in the five years to June 2025.

Pleasingly, things are starting to look up. Moderating inflation, real wage growth and lower interest rates are boosting confidence. Most signs are pointing in the right direction and we’re on our way to a stronger retail environment.

Last week’s National Accounts reported real consumer spending grew by 0.9% in the June quarter, the strongest quarterly growth since 2022. Annual growth lifted to 2.0%, the strongest annual growth rate for two years.

Many households took advantage of the close proximity of Easter and ANZAC Day to take time off and get away. Money that may otherwise have been spent on retail purchases went elsewhere, with real household spending on vehicles up 2.4%, recreation and culture up 2.0% and transport services up 1.7% in the quarter.

That being said, real retail spending is up 1.5% on this time last year. That’s the best result for nearly three years, but real sales are still only just keeping pace with population growth and still lag behind the pre-COVID decade average of 2.4%. We think things will pick up after a few more quarters of real wage gains.

The June quarter also highlighted the retail sector’s two-paced growth. Non-food sales volumes rose 0.8% over the quarter, taking annual growth to 3.5%. Food sales volumes fell 0.2%, with annual growth at just 0.1%.

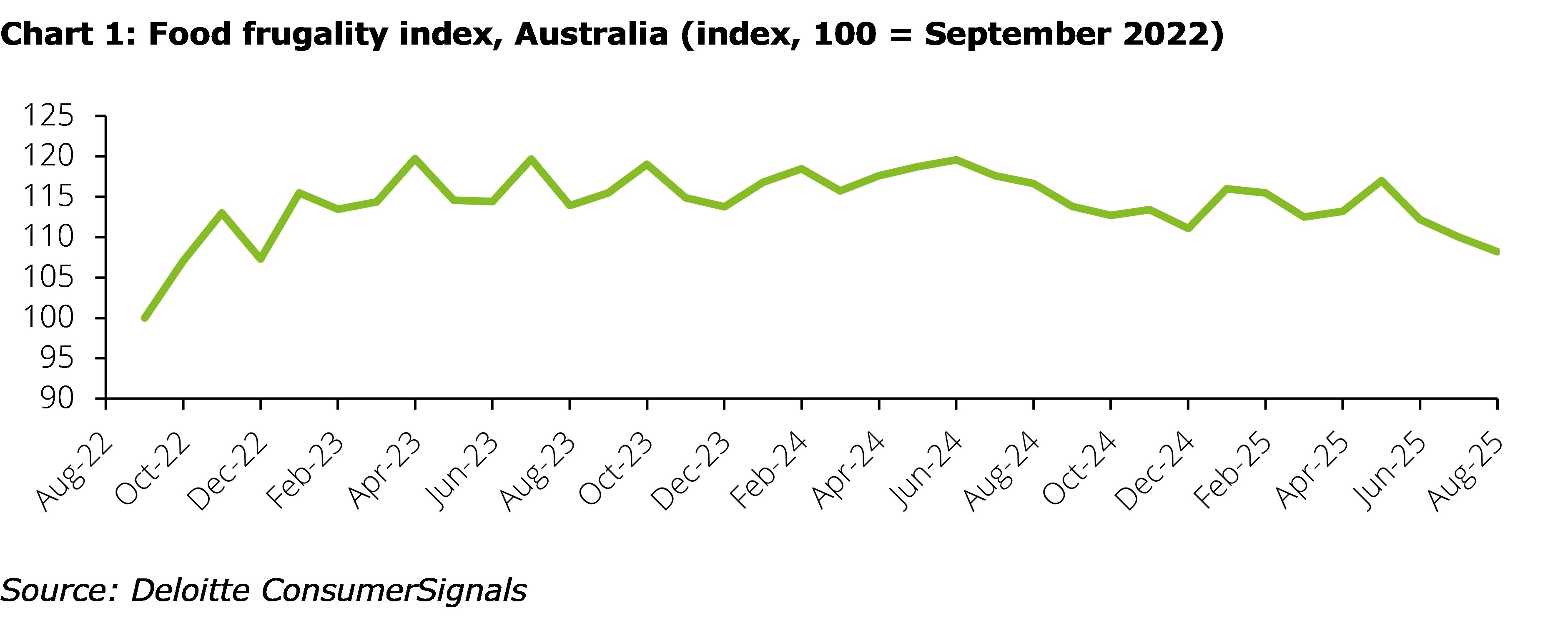

For much of the last year Australians have remained frugal at the supermarket. Cost saving habits formed during the cost-of-living crisis (like buying more private label brands and cheaper cuts of meat) have persisted. But we may now have reached an inflection point on this front.

The Deloitte ConsumerSignals Food Frugality Index (where higher scores indicate more frugal behaviour) recorded its third consecutive decline in August and now sits at its lowest level since 2022. That recent movement indicates that consumers are finally starting to shift from their more frugal grocery buying behaviours, which should flow through to stronger retail food sales in the coming months.

Overall, retail sales are expected to pick up over the second half of this year as consumers feel better off and end-of-year sales events support more spending. This should be a taste of things to come as a longer period of real income gains is locked in. Retail sales volumes are expected to grow by 2.3% in 2026, accelerating to 2.6% in 2027.

Following July’s final ABS Retail Trade release, Deloitte Access Economics is upgrading its retail forecast framework. Future editions of Retail Forecasts will report on both ABS Household Final consumption expenditure (HFCE) data and DataCo’s merchant‑categorised spending data to provide a more detailed view of consumer spending trends.

The DataCo data is drawn from de‑identified ANZ Bank customer and transactional data and will include spend categories such as takeaway food, discount department stores, home DIY, travel, beauty & health, and jewellers.

This newsletter was distributed on 11th September 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Chris Bates, Economist at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings:

- National Accounts: Australians’ living standards gain ground (3 Sep)

- Economic Reform Roundtable: The start of a conversation (29 Aug)

- Australia’s Youth Agenda Economic and policy imperatives (27 Aug)

- Productivity growth revised down, as labour market cools (14 Aug)