Don’t count on a disinflation dividend from international trade

The RBA cannot bank on imported disinflation in a chaotic global environment.

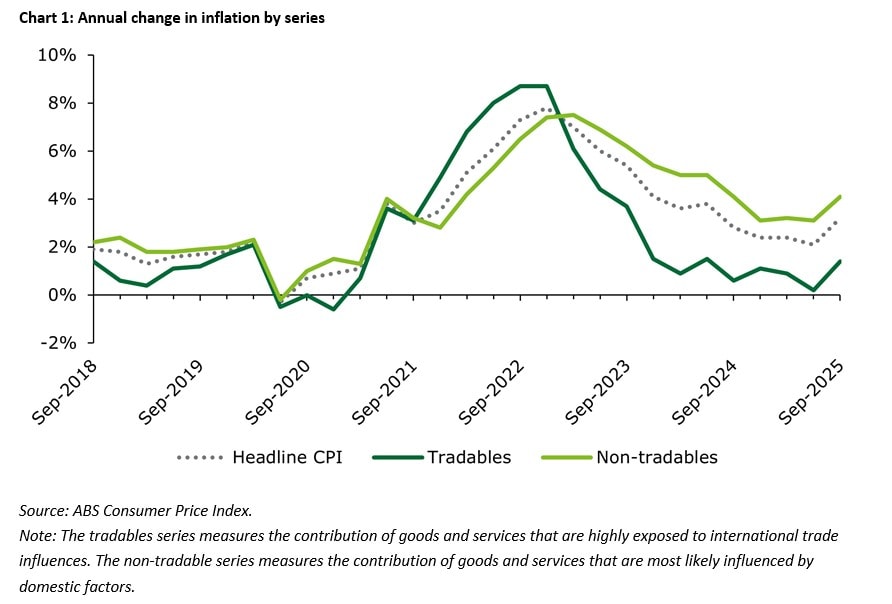

Inflation accelerated in Australia in the September quarter. While the uptick in headline inflation (to 3.2% over the year to the September quarter, up from 2.1% in the previous quarter) was expected due to the expiry of electricity rebates, the real surprise was the acceleration in underlying inflation. Annual trimmed mean inflation accelerated from 2.7% in the June quarter to 3.0% in the September quarter.

Besides domestic challenges to the inflation outlook, the RBA faces considerable uncertainty from the global economy. As post-pandemic inflation accelerated, prices of tradables rose faster than prices of non-tradable goods and services. That inflationary impulse from overseas is widely expected to reverse over the coming quarters. Excess industrial production in China and high import tariffs in the United States (US) could lead to Chinese goods being diverted to more open economies such as Australia, producing a disinflationary effect. However, this is far from certain.

The latest data show that Australia’s import prices have indeed fallen (down 1.3% since the March quarter), primarily due to the lower price of crude oil. However, the mercurial nature of the global economy at present could mean that the disinflationary impulse from overseas is short lived. For instance, US sanctions on Russian crude oil could put a floor under petroleum prices. Broader trade disruptions due to US tariffs could also lead to inefficiencies that result in higher shipping costs.

Recent history shows that a sharp rise in international shipping costs can have a significant effect on domestic prices in Australia. Almost 99% of Australia’s trade by volume, and about 80% by value, is seaborne. Freight costs therefore need to be monitored closely, especially while the US and China impose retaliatory taxes on each other and broader trade logistics are being disrupted.

Almost a quarter of Australia’s imports come from China. While the overall China Containerised Freight Index, which indicates the cost of shipping freight from China to the rest of the world, has fallen in 2025, the subindex for shipping to Australia and New Zealand has shown relative strength. This can be explained by seasonal spikes in demand and relatively less competition on the route. Earlier this year, it was reported that while the cost of shipping freight from China to the US had fallen sharply, the cost of shipping goods from China to Australia was likely to move in the opposite direction.

Dry bulk freight costs are also rising as indicated by the uptick in the Baltic Exchange Dry Index (up more than 150% since February). Though the rise in the index is nowhere near as sharp as in 2021, it is still worth noting, especially as Australia’s imports of dry bulk goods like cement and gypsum feed into construction costs.

However, it is the sharp rise in the shipping costs for liquid bulk, particularly crude oil, that stands out. The Very Large Crude Carrier (VLCC) index, which shows the cost of shipping crude oil, has risen sharply since August. Prices for the Middle East to China route have risen at the fastest rate. Several factors are at play. First, increased production in the Middle East and resilient growth in Asia have supported demand for tankers. Additionally, sanctions on Russian oil are delaying some tankers from unloading in China and India. And finally, US-China port fees have further reduced the available fleet of carriers.

This coincides with relatively low levels of fuel storage in Australia. According to the Department of Climate Change, Energy, the Environment and Water, Australia had just 20 days of jet fuel and 32 days of petrol supply in August. Higher shipping rates are likely to feed into overall costs when Australia restocks petroleum products, its largest import.

If global developments prevent further falls in crude oil prices while pushing up shipping costs, especially for petroleum products, then the RBA might not receive the wave of imported disinflation that it is hoping for.

This newsletter was distributed on 30th October 2025. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Lester Gunnion, Maanger at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings: