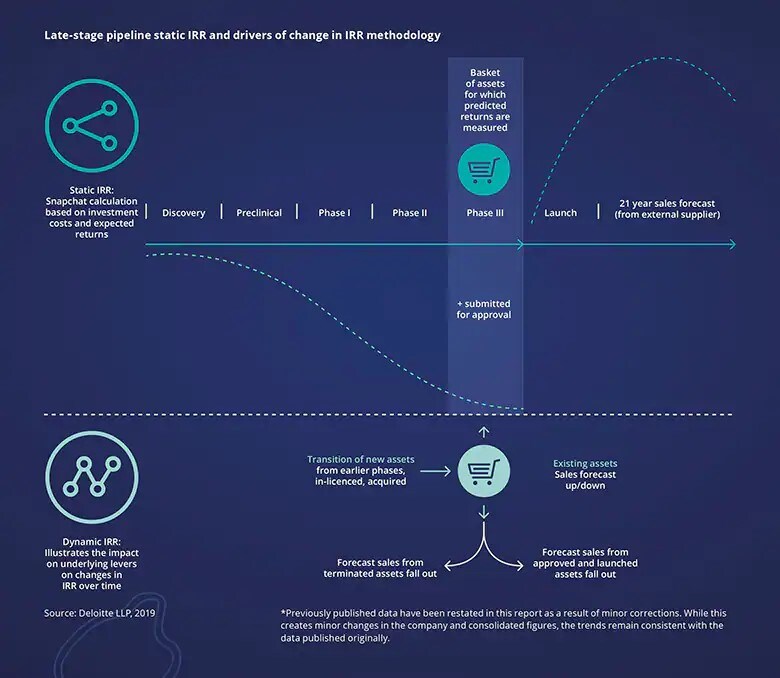

Since 2010, our Measuring the return from pharmaceutical innovation series has focused on the projected returns from the late-stage pipelines of a cohort of the 12 largest biopharma companies by 2009 R&D spend. Our five most recent reports also include an extension cohort of four mid-to-large cap, more specialized companies. We use these two cohorts as a proxy to measure the industry’s ability to balance initial capital outlay with the cash inflows biopharma companies are projected to receive as a result of this investment.

Our consistent and objective methodology focuses on each company’s late stage pipeline (assets that are filed, in Phase III or Phase II with breakthrough therapy designation as of 30th April each year) and measures performance across the original and extension cohorts. We use two inputs to calculate the Internal Rate of Return (IRR): the total spend incurred bringing assets to launch (based on publicly available information from audited annual reports or readily available from third-party data providers) and an estimate of the future revenue generated from the launch of these assets. As assets are approved, forecast revenues move from the late-stage pipeline into the commercial portfolio, moving out of scope of our analysis and decreasing the value of the late-stage pipeline. The graphic below illustrates our methodology, showing both the static year-on-year and dynamic (three-year rolling average) measures of R&D returns.