Consumers brace for potential tariff headwinds

The May 2025 Economics Insider explores possible effects of tariffs on consumers and their purchasing power this year

Consumers have been at the forefront of the post-pandemic economic recovery seen in the United States: Since the second quarter of 2020, real consumer spending1 has grown by about 29%, thereby aiding wider economic growth of 23.5% over the same period.2 Yet, as 2025 rolls on, economic indicators suggest that many consumers appear anxious.

A month ago in April, consumer sentiment, as measured by the University of Michigan, fell to its second-lowest level ever.3 Deloitte’s global survey of consumers also shows that spending intentions, especially for discretionary goods, have gone down in recent months.4 So, why has consumer sentiment gone down this year?

First, new tariffs announced by the United States5 have pushed inflation expectations up.6 The University of Michigan’s one-year-ahead expected inflation rate jumped to 6.5% in April 2025—the highest since the early 1980s.7 Second, consumers are also wary about the impact of uncertainty regarding tariff policy on wider economic activity—and, by extension, on their personal finances.8 Finally, with tariffs raising concerns about inflation, the Federal Reserve has turned cautious.9 Hence, borrowing costs for consumers may remain elevated, at a time when delinquency rates have gone up for both credit card debt and auto loans.10 All these factors, in turn, will likely weigh on consumer spending growth over the next few years.11

Consumers expect prices to rise due to tariffs

Tariffs are taxes paid by importers; and some, or all, of these cost increases will likely pass on to consumers, who would therefore face higher prices.12 The Budget Lab at Yale estimates that automobile tariffs will likely push the average price of an automobile in the United States by 13.5% or US$6,400, compared with 2024 prices.13 The degree of increase in prices will also depend on how integrated supply chains are with countries that are being tariffed at higher rates. For example, about 80% of toys bought in the United States are from China and are not exempt from tariffs.14 With alternate suppliers not expected to fill in quickly for Chinese ones, US consumers will likely face higher toy prices this year.

According to research by economists at the Federal Reserve Bank of Boston, imports account for 10% of total US personal consumption expenditure (PCE) excluding food and energy (also called core PCE).15 And their estimates suggest that a 25% tariff on Mexico and Canada, along with 10% tariffs on China will increase core PCE inflation by 0.5 to 0.8 percentage points.16 The rise in core PCE inflation will be higher—about 1.4 to 2.2 percentage points—if tariffs on China rise to 60% while a universal 10% tariff is imposed on the rest of the world.

These estimates, however, do not account for economic changes in response to tariffs and any trade retaliation by other countries. It appears that the impact of tariffs is already filtering into the economy through rising production costs. Surveys by some regional Federal Reserve Banks show that prices paid by US manufacturers for their supplies have accelerated this year, primarily due to tariffs.17

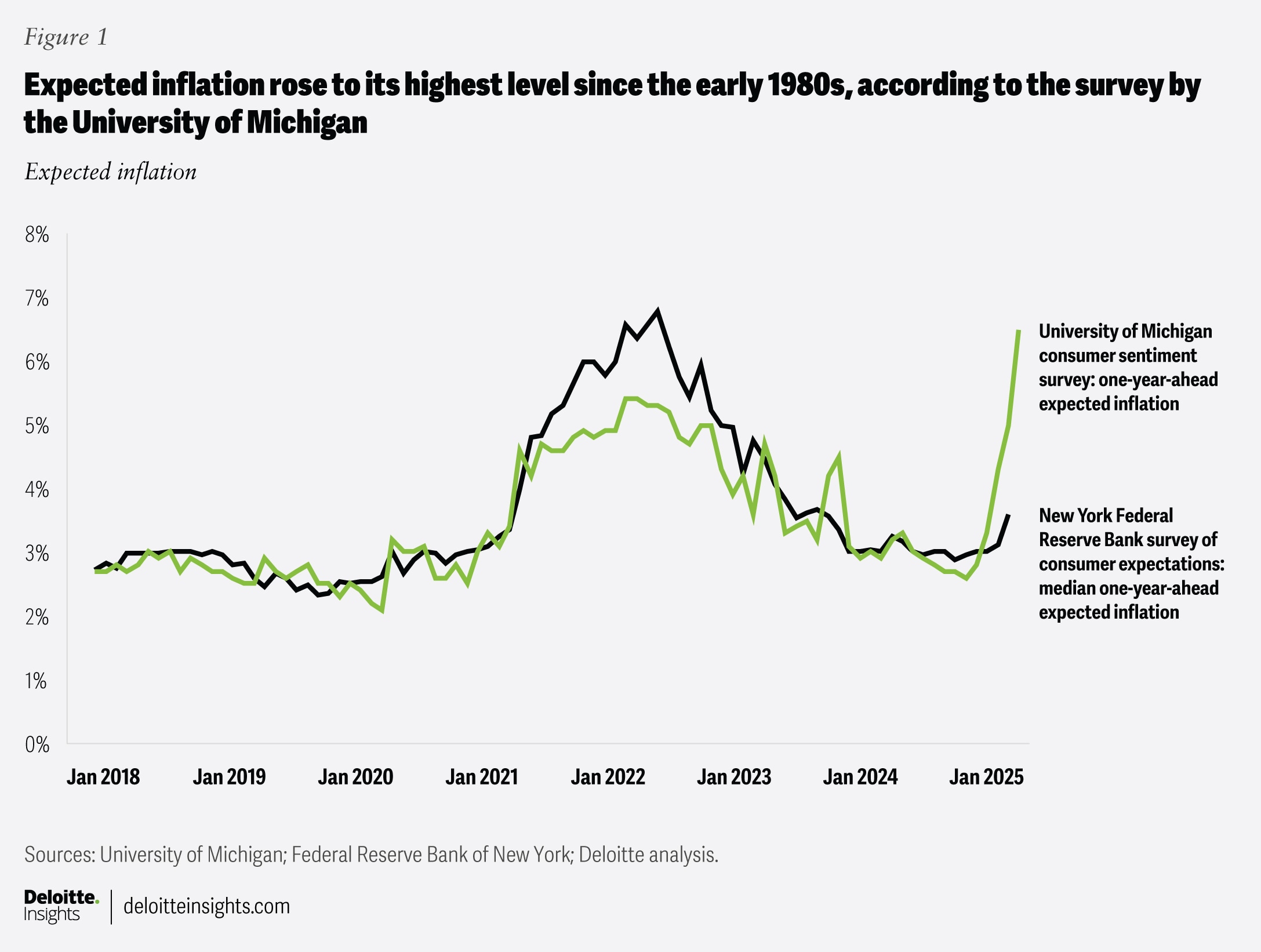

In its latest release, the International Monetary Fund, too, has upwardly revised its inflation forecast for the United States. It now expects inflation to be about 1 percentage point higher than its earlier projection of 2%.18 The median expected inflation rate for households for a year head—based on the Federal Reserve Bank of New York’s survey of consumer expectations (SCE)—rose to 3.6% in March, a half-percentage-point increase from February and up from 3% in end-2024.19 And according to the University of Michigan’s survey, consumers now expect inflation to rise to 6.5% one year from now, more than double the rate they anticipated in December 2024 (figure 1).20

{kind=link}

But tariff policies’ potential wider economic impact is also making consumers wary

A healthy labor market, with strong wage growth, has been a key driver of consumer spending growth over the United States’ post-pandemic economic recovery. So, as policy uncertainty rises (especially trade policy),21 consumers appear to be worried about its impact on the wider economy—and by extension, on their jobs.

According to the University of Michigan survey in April, the share of respondents who expect unemployment to go up over the next year rose to the highest level since November 2009.22 In the SCE, the share of respondents who expect their household financial situation to worsen rose to 30% in March—from 19.9% in December 2024.23

The uncertainty around a final tariff structure makes it challenging for businesses to commit to decisions about their global supply chains, which in turn may dent business investment and wider economic activity.24 In April, Deloitte economists (in their baseline scenario, with a probability of 50%) revised down their forecasts for US business investment and GDP growth from their March projections.25 And in their downward scenario (probability of 35%), business investment is forecasted to contract if tariffs remain on April 2 levels without tangible trade deals with key US global partners (other than the one just concluded with the United Kingdom).26

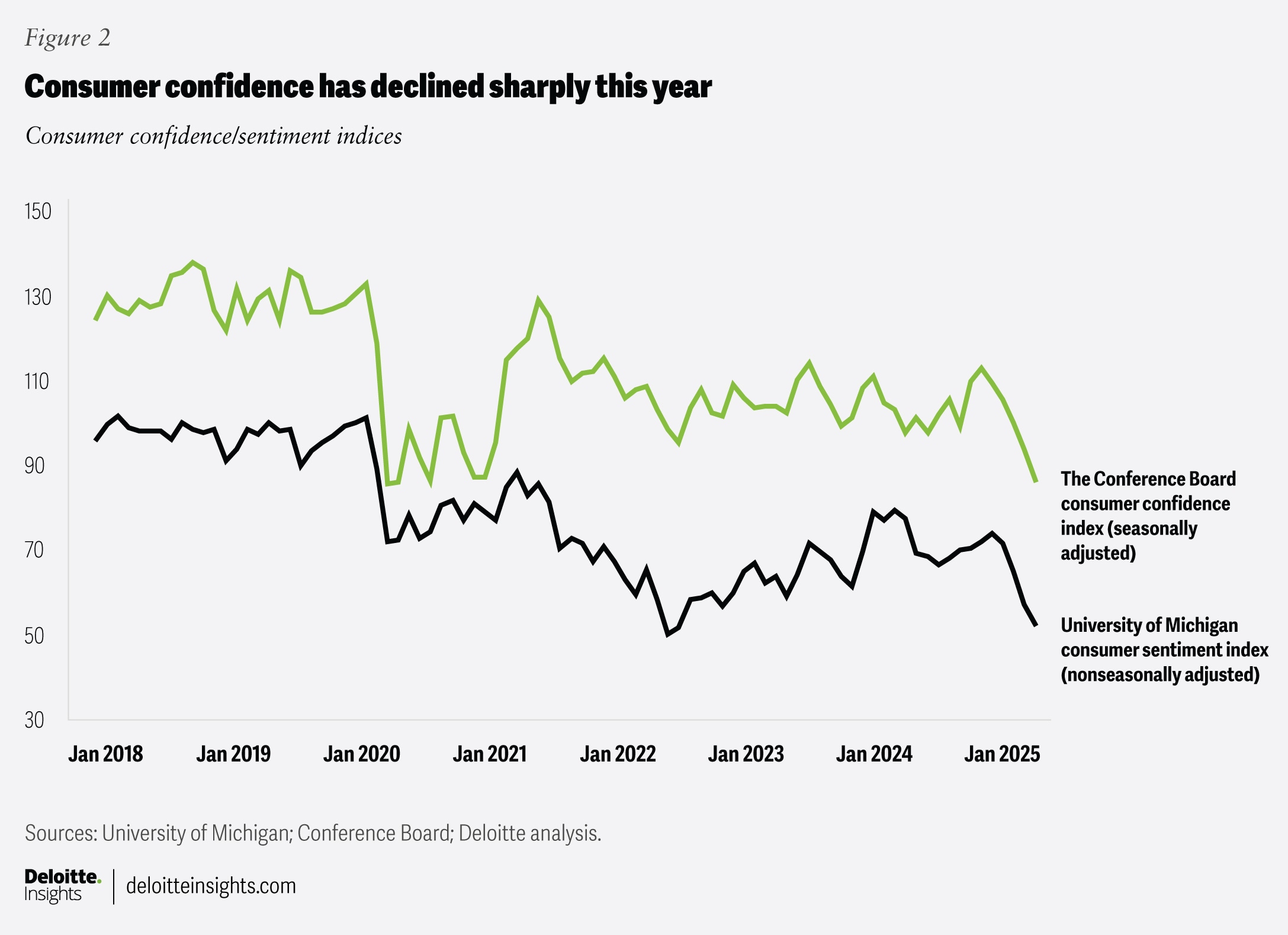

Consumer sentiment has, therefore, gone down. The University of Michigan’s consumer sentiment index fell to its second-lowest reading ever in April—just marginally above its lowest reading in June 2022.27 The Conference Board’s measure of consumer confidence has also declined sharply during this period (figure 2).28 In both measures, the subindices that track expectations of future economic conditions have suffered the most. While measures of consumer confidence may not always be good predictors of actual spending (or of a wider economic outlook),29 the sharp dip in sentiment, especially since the end of last year, may be worrying.

{kind=link}

Inflation and economic uncertainty may impact borrowing costs

Rising inflation due to tariffs may force the Federal Reserve to turn cautious30 in its approach to policy rate cuts. However, if tariffs dent economic growth (and hence, the labor market), monetary policy may be more accommodative—a view investors appear to be taking. The five-year breakeven rate—a measure of bond investors’ inflation expectations over the next five years—has declined since early April.31 This means that while investors expect inflation to rise in the near term, they feel that softening GDP growth will likely offset this temporary increase in price pressures. Futures markets, therefore, indicate an implied probability of 68% (as of early May) that the Fed will cut its policy rate three or four times in 2025.32 That’s higher than the Federal Open Market Committee’s median view in March of just 50 basis points of rate cuts this year.33

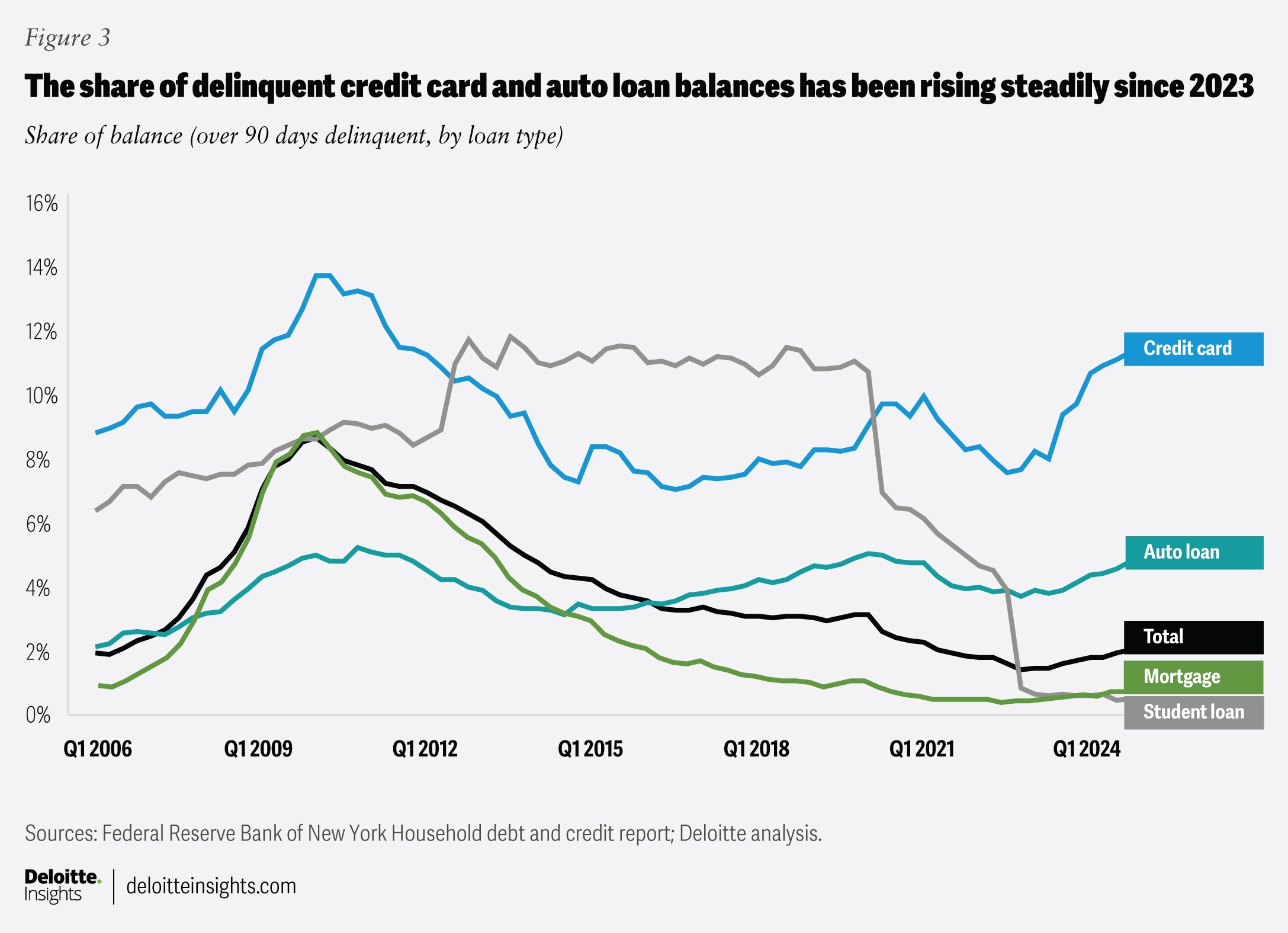

How things pan out is tricky to forecast at this stage. But, if inflation turns out to be less transitory than investors are currently anticipating, consumers may continue to face elevated borrowing costs. This will likely weigh on low-income households and maxed-out borrowers the most,34 at a time when households already face rising credit card and auto debt despite delinquencies in these categories going up (figure 3).35

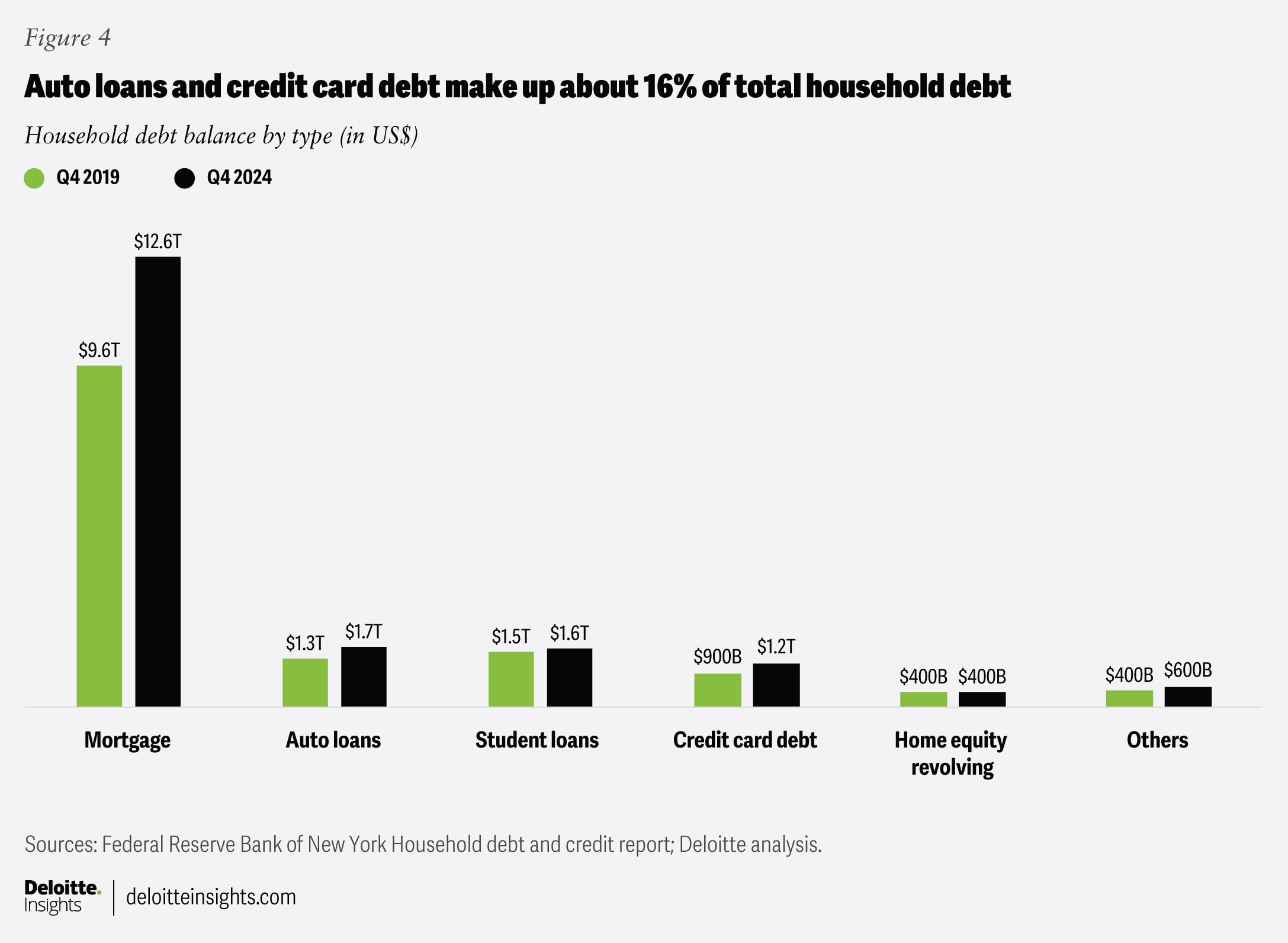

Homeowner balance sheets are in better shape than that of renters, given that mortgages account for 70% of total household debt in the economy and delinquency rates in that area are low (figures 3 and 4). Renters, on the other hand, face high rent costs compared with pre-pandemic times,36 while elevated mortgage rates and rising home prices keep them out of the housing market. This scenario is unlikely to change if slowing policy rate cuts and rising bond yields due to tariffs keep mortgage rates elevated37 for longer.

{kind=link}

{kind=link}

Worried consumers may mean lower spending growth

If consumers anticipate higher prices due to tariffs, they will likely front-load goods purchases, especially durables, which may be affected the most by higher tariffs. For example, nominal retail sales at motor vehicles and parts dealers rose by 5.3% in March,38 as consumers likely fast-tracked spending on automobiles before prices rise due to tariffs. Deloitte’s baseline forecast (probability of 50%) assumes that the US average effective tariff rises by 10 percentage points from 3.3% in 2024.39 This is roughly equivalent to a 10% tariff on all countries, with a 25% tariff on steel, aluminum, motor vehicles, and auto parts. While this rate is lower than what is currently in place (between 18% to 20% depending on substitution effects),40 it will nevertheless be the highest seen since World War II.

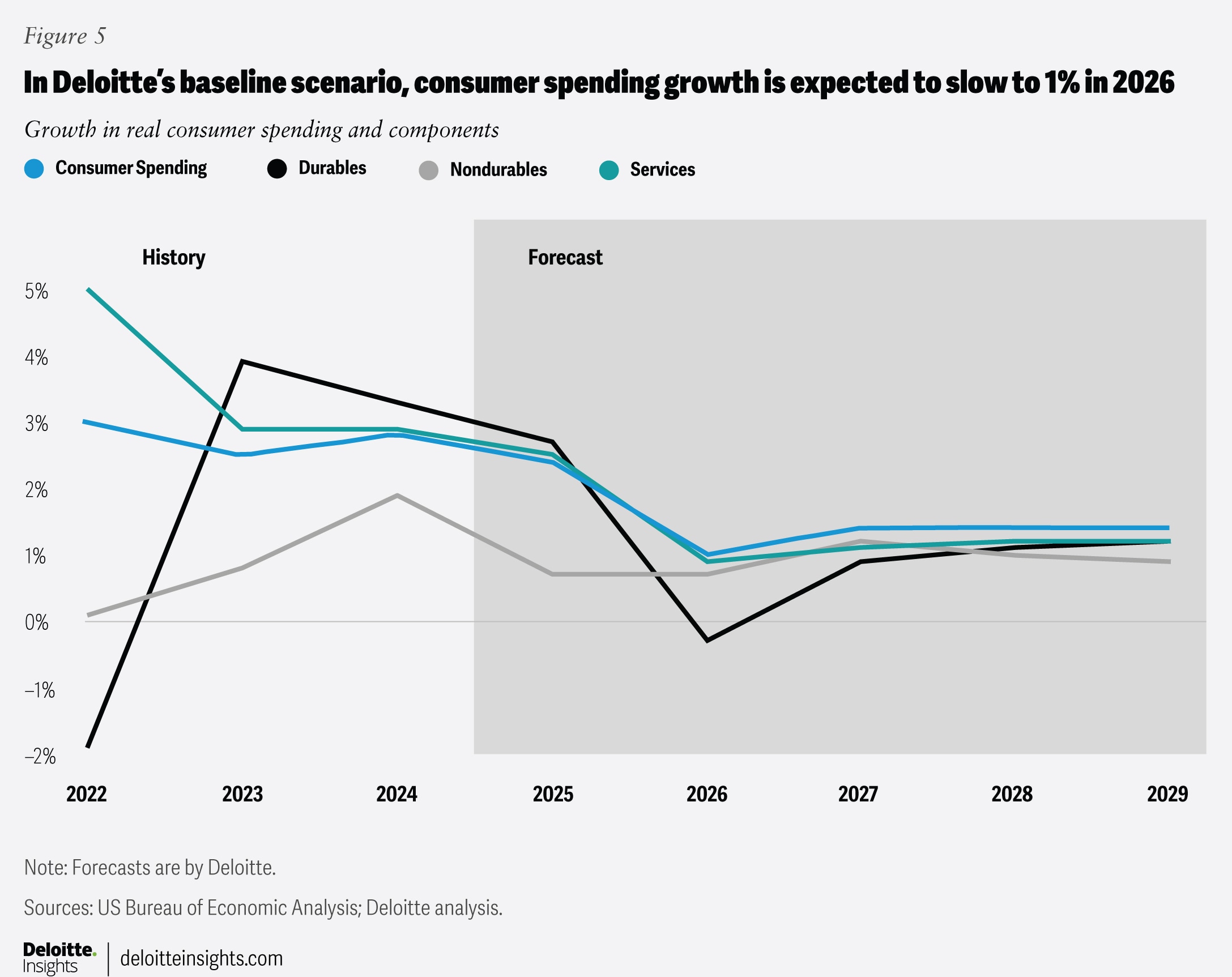

In this scenario, consumer spending is expected to grow at a healthy pace this year, with spending on durables set to increase by 2.7%. However, as rising inflation dents their purchasing power, consumers will likely cut back and save more. Consumer spending growth is expected to slow to just 1% in 2026 before picking up the year after. Spending on durable goods is likely to decline next year before a slow recovery takes shape (figure 5). Growth in services spending is expected to be steady but relatively low at 1.4% per year (on average) over the forecast period. Despite the possible effects of tariffs, consumers may find some relief from an extension of the Tax Cuts and Jobs Act, which will prevent any dent to disposable personal income The baseline scenario also assumes that corporate tax cuts will be reduced to 15%, thereby aiding American producers.

{kind=link}

Changing policy may tilt consumer spending growth either way

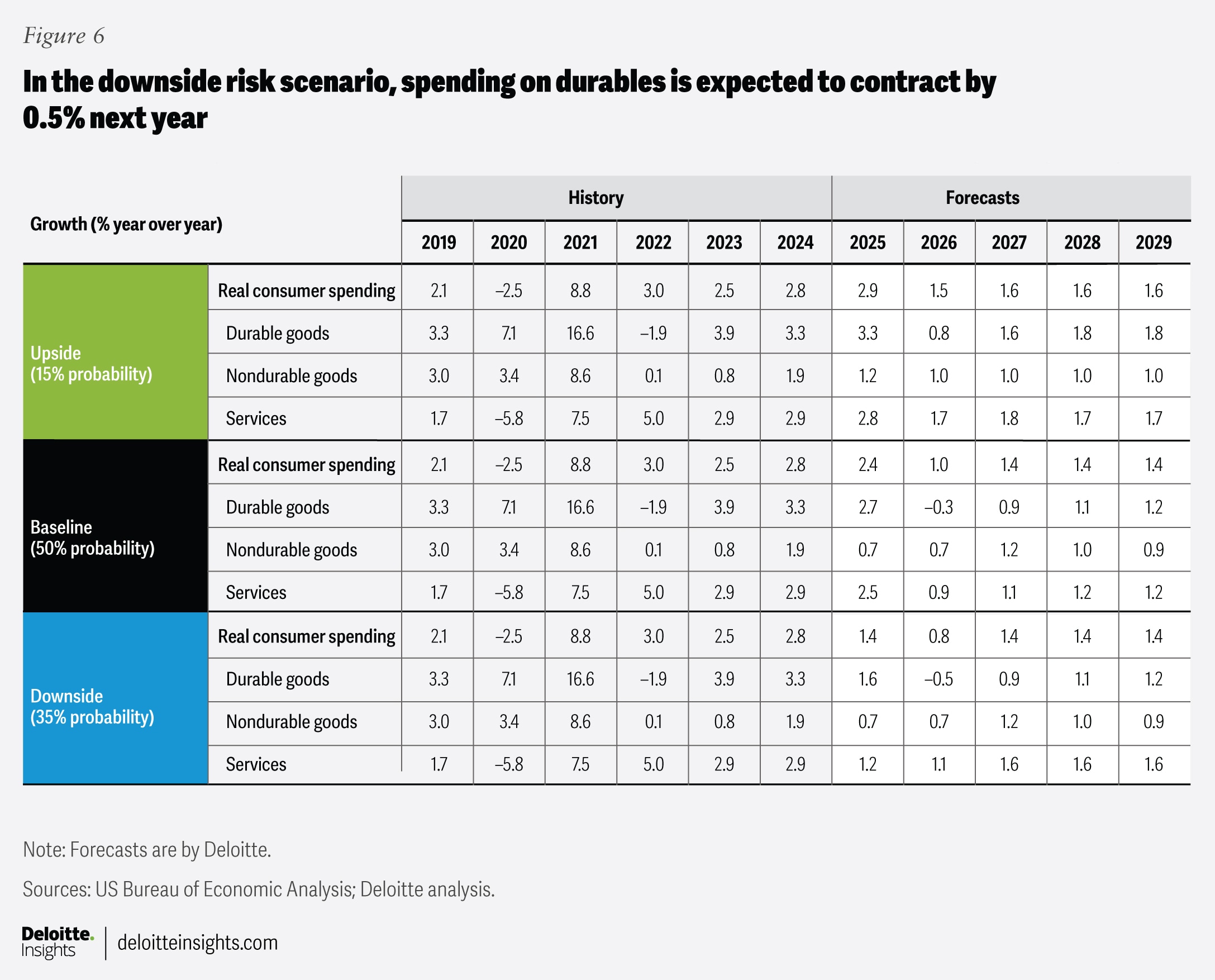

Trade discussions are ongoing: Given the 90-day pause on higher reciprocal tariffs and a separate 90-day pause for China,41 it is still uncertain how any trade scenario will unfold. Deloitte economists, therefore, anticipate both upside and downside risks to their baseline forecasts.42

- Upside risk (15% probability): In this scenario, bilateral trade deals lead to lower tariff rates than in the baseline. A more dovish approach to federal spending will aid the economy while deregulation will likely lead to higher business investment growth and productivity gains. Consumer spending growth in this scenario is expected to average about 1.8% per year till 2029. Spending growth is forecasted to be higher for durable goods and services compared to the baseline (figure 6).

- Downside risk (35% probability): If trade deals falter and tariff rates return to levels they were on April 2, consumers are likely to face headwinds from both rising inflation and unemployment. High tariff rates and prolonged uncertainty may lead to a 6% contraction in business investment this year. Unemployment is therefore expected to rise to an annual rate of 5.3% by 2026 from 4% in 2024. Consumer spending growth is forecasted to slow sharply this year and the next (figure 6).

{kind=link}

by

Akrur Barua

The author would like to thank Rohini Sanyal and Ruhika Agarwal for their research contributions to this article, and Ira Kalish, Michael Wolf, and Daniel Han for their reviews.

Cover image by: Harry Wedel

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.