2026 Global Sports Industry Outlook

AI is reshaping operations, capital is scaling ownership, sports are converging with media and entertainment, and venues are evolving into year-round platforms

Moving into 2026, the global sports industry is evolving and the lens through which it may be viewed is widening. The industry—inclusive of leagues, teams, federations, mega-events, media partners, investors, and more—is entering an age of expansion and transformation. Artificial intelligence is becoming foundational for growth and is emerging as an intelligence layer that strengthens organizations from within and links siloed parts of the business together. Capital continues to flow into the industry, pushing ownership models and operating structures to evolve and elevate. Global ownership groups are extending their reach and influence and blurring the boundaries between sports entities, media, and commerce. And the physical spaces of sports are evolving, too: Stadiums are transforming into year-round entertainment districts that help drive economic value and community resilience far beyond game day.

Across the global sports landscape, growth is visible on every front. The value of media rights continues to climb worldwide,1 commercial revenues in women’s sports are growing at double-digit rates,2 numerous stadiums and sports districts are under development across the map,3 and franchise valuations across major leagues continue to reach new highs.4 The big question is no longer: “What is the ceiling for the sports industry?” It has become: “How much bigger will the room get?”

Read more from the collection

TMT Outlooks

In 2026, sports may not only be growing, but increasingly emerging as a frontier of entertainment, culture, and everyday life.

AI enables reimagination of how sports organizations operate and scale

AI has outgrown its role as a trick play. For many sports organizations, it’s becoming a whole new game plan. AI may serve as the connective engine that strengthens organizations from within, breaking down data silos, transforming work, and enabling the sports industry to interconnect and grow. Moving into 2026 and beyond, sports organizations looking to compete shouldn’t ignore AI. The leaders in the global sports industry may be those who embed AI systems and workflows into applicable aspects of their businesses.

The next wave of AI adoption for sports organizations of all sizes is likely to start in the back office and may quietly impact parts of the business fans rarely see.5 AI may augment traditionally repetitive and time-consuming tasks, like automating entries and reconciliations in finance and automating outreach for season ticket renewals with all of the corresponding processing handled seamlessly.6 Effective AI implementation—which involves redesigning operating models and thinking intentionally about how humans and AI work together7—may free up capacity for the workforce to focus on delivering more strategic and creative work, fit for primetime.

About Deloitte’s TMT center outlooks

Deloitte’s 2026 global sports industry outlook seeks to identify the strategic issues and opportunities for the industry to consider in the coming year, including their impacts, key actions to consider, and critical questions to ask. The goal is to help equip companies across the sports ecosystem with information and foresight to better position themselves for a robust and resilient future.

Quicker and more informed decisions may ultimately improve fan experiences and impact sports organizations’ success on and off the field of play. AI can be used to bring fans closer to the sports and teams they love: Think real-time analytics in live broadcasts, personalized and AI-generated highlight reels, near immediate responses to fan questions, and improved accessibility and safety inside stadiums.8 AI could also be deployed to protect and optimize sports organizations’ most valuable assets—their players—by assessing player fitness and conditioning, predicting and preventing injuries, and using AI agents to review game film.9 Much of this is already happening at the highest levels of sport but it may be democratized across organizations given the ubiquity of AI.

All of this is just the beginning of a future that could unfold in short order. AI may allow teams to game plan through scrimmages with digital twin opponents, enable AI agents to handle ticketing and microtransactions automatically, and model and predict crowd patterns across entire stadium districts. Most sports organizations aren’t there yet but now may be the time to work on the fundamentals: consolidating and organizing data, building strong internal capabilities, redesigning work, establishing a culture of continuous learning, and developing clear data governance, security, and trust guardrails. The organizations that do this now may shape the industry’s next phase of rapid growth.

Strategic questions to consider:

- How can your organization effectively redesign work and roles so AI augments human judgment, creativity, and decision-making, rather than simply automating tasks?

- Is your data ready for AI? Are critical datasets consolidated, governed, and trusted enough to support enterprisewide use cases?

- How is your organization fostering a culture of learning and experimentation that gives employees the time and support to build AI skills?

- Where can AI create value in your operations today, and what capabilities and partnerships will you need to scale that value across the enterprise tomorrow?

New investment models reshape sports organizations

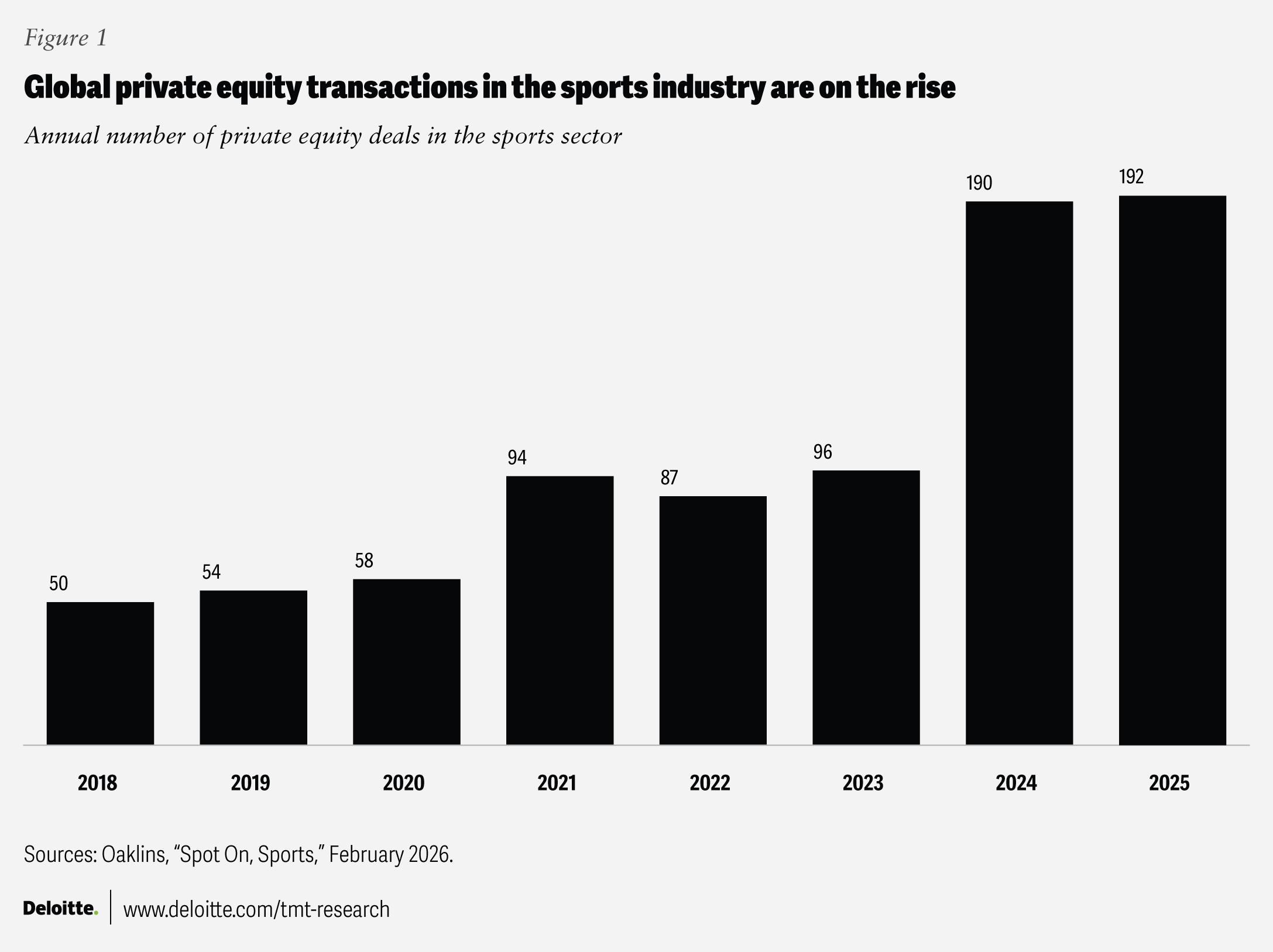

As popularity and valuations increase, sports are no longer a passion project or a hobby for wealthy individuals, but a serious business.10 Private and institutional capital have been flowing into the sports industry for years—across all major US leagues, European football leagues, rugby, cricket, motorsports, and more,11 and increasingly shaping expectations across the broader sports ecosystem, including parts of US college athletics (figure 1).12

Teams and leagues might embrace capital for any number of reasons: to support operating costs, update aging facilities or develop new venues, invest in new technologies, or grow their global reach. But outside investment brings greater scrutiny, new challenges, and rising expectations around transparency, governance, and financial rigor. Looking ahead, sports organizations embracing new capital vehicles may need to navigate a growing tension between the pressure to professionalize and win in a more sophisticated and investor-led market, and the external pressures to stay authentic, athlete-centered, and meaningfully connected and relevant to their loyal fanbases, all while being good stewards of external funding and resources.

These shifts bring new considerations for the industry. Many private or institutional investors no longer want to be passive funders; instead, they want to be hands-on partners. Along with capital, they’re likely to bring cross-industry expertise (in fields like media rights or facilities development) and access to leading technologies and processes and increased operational discipline.13 All this suggests that capital is no longer the star player; capability is. While this shift brings new opportunities for commercial growth and efficiency, it also raises the bar for sports organizations. Working with active investors requires new leadership capabilities, clearer strategies and priorities, and more disciplined internal management. College athletics is moving in this direction, as some programs set up separate or affiliated entities that allow for more financial flexibility, professionalized operating frameworks, and clearer governance—early signs of a model that is beginning to attract significant outside capital that others may attempt to replicate or follow.14

As sports organizations explore their options with private funding and build the necessary business acumen and governance frameworks to support it, there may be growing concern around tradition, competitive integrity, or the over-commercialization of sports.15 There’s also a distinct fear connected to the well-known “exit horizons” of private investors. What happens if a strategic investor acquires a controlling interest in a team or club, only to divest a few years later—potentially triggering governance, tax, or regulatory concerns? To manage this, investors and sports entities should focus on a collaborative model that prioritizes team performance, fan engagement, and clear guardrails around governance, ownership control, and long-term stewardship.16

As more investors enter the market, expectations for professionalism, operational maturity, disciplined governance, and tax transparency may only rise. Investors could seek sports organizations that can transform capital into real value on the field, on the balance sheet, and with their fans. In the years ahead, investment partnerships will likely become more selective, more strategic, and more focused on reciprocal value, making it clear that capability, not just capital, will shape who leads the next era of sports.

Strategic questions:

-What capabilities could be built today (in finance, data, human resources, or technology) to compete in an investor-driven sports marketplace?

-How should governance models and transparency practices evolve to ensure accountability in increasingly complex ownership and investment structures as expectations for financial rigor rise?

-How can sports organizations balance the expectations for revenue-generation and commercial growth with team performance and fan trust?

- What can be learned, across all levels of sports, from early operating structure and governance experiments in collegiate athletics?

Global ownership portfolios redefine scale and blur industry lines

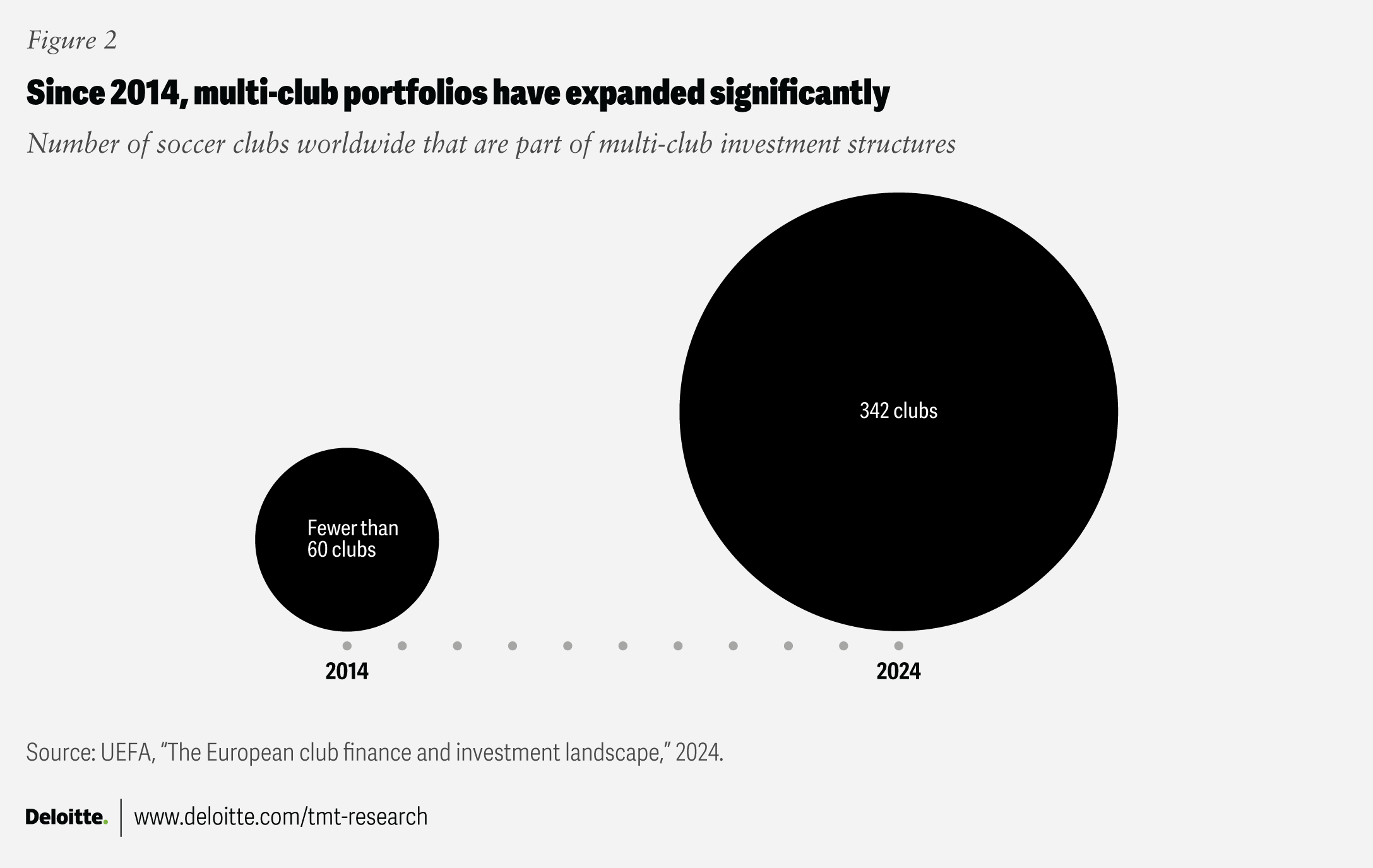

Ownership itself is rapidly scaling both horizontally and vertically—across teams, markets, technology companies, and more—as many investors build portfolio-style networks rather than focusing on standalone franchises. Multi-club, multi-sport, multi-business and multi-country ownership groups are growing in number, as US investors expand into Europe and emerging markets, while sovereign wealth funds and international groups increasingly pursue US franchises and sports assets (figure 2).17 These ownership groups aren’t simply assembling teams; they’re building cross-industry platforms that combine sports, media rights, content studios, video games, fan data, real estate, and more to drive commercial value and meet consumers’ appetites for elevated fan experiences—on the field, in the venue, and well beyond.

This momentum comes at a time when team valuations soar, competition for fans and sponsors intensifies, and global media consumption reshapes how fans engage—pushing investors to seek more scale and more meaningful returns.18 Financially, multi-club and multi-sport models diversify risk, offer opportunities for shared operating systems, and can make it easier to scale commercial partnerships across leagues and sports and expand global reach.

On the sporting side, connected clubs and teams across a portfolio can benefit from shared investment in scouting, performance analytics infrastructure, and player development frameworks. Connected clubs can apportion costs and elevate standards across teams and sports. Beyond these financial and sporting advantages, portfolio-style ownership can also grant groups greater influence over league governance, credibility with commissioners and league executives, and a seat at the table when strategic decisions are made—though many leagues have implemented, or are considering, stricter regulations on multi-club ownership.19 Ultimately, sustained value may come from disciplined growth and strategic integration, anchored in performance and fan trust.

The most profound shift, however, may be how these groups are evolving beyond sports entirely and into global business ventures. Many now own media rights businesses, content studios, production companies, data platforms, esports teams, and real estate assets, and hospitality enterprises adjacent to the sports industry, which creates year-round engagement and diversified revenue streams. City Football Group runs its own production studio and centralized data platform.20 Liberty Media has transformed Formula 1 into a global entertainment property with original content and fan festivals.21 Fenway Sports Group manages New England Sports Network, mixed-use and stadium real estate, and even a performing arts center.22 These cross-industry extensions give ownership groups greater control over the fan journey, the ability to shape their own storytelling, and multiple avenues to monetize audiences across channels and across the fan lifecycle.23

Looking ahead, we expect global sports groups to continue evolving across clubs, sports, geographies, and entertainment verticals. But greater scale brings greater complexity. Scrutiny around multi-club ownership and competitive integrity is rising, and cross-border operations are increasingly testing existing tax and regulatory frameworks.24 Fan bases may also push back against the perceived over-homogenization or over-commercialization of the teams they love, which can put pressure on ownership groups to “stay small as they grow big” to preserve local identity even as they build global platforms. Those that strike this balance may broaden what fandom can look like, with supporters engaging not only with their local team or club, but with the ownership groups’ wider universe of content and experiences. In the next era of sports, the advantage may not come from owning more assets, but from connecting them into a strategic, culturally attuned, year-round global experience.

Strategic questions to consider:

-Where can shared data and operations across a portfolio unlock meaningful value, and where might they create unintended competitive or cultural risks?

- What can sports organizations do to balance global scale and growth with the local identity, culture, and traditions that matter most to fans?

-How can sports ownership groups and organizations prepare for heightened scrutiny of competitive integrity, tax structures, and cross-border ownership regulations?

-How can ownership groups use their global networks and cross-industry partnerships across media, technology, and entertainment, to accelerate innovation, deepen fan engagement, and create new commercial models?

Sports districts: Community epicenters built for profit and purpose

Today’s sports venues are evolving into far more than game-day destinations—they’re becoming epicenters of community and engines of year-round activity. Teams, municipalities, and developers are building sports districts—mixed-use ecosystems of housing, dining, retail, corporate tenants, and transit—aimed at driving revenues every day of the year, even on non-game days.25 But many forward-looking sports organizations see something more: an opportunity, and a responsibility, to turn stadium projects into community assets that generate measurable social impact as well as long-term business value.

Sports districts themselves aren’t new. Models like The Battery Atlanta (Georgia, United States), The Kallang (formerly Singapore Sports Hub, Kallang, Singapore), and ICE District (Edmonton, Alberta, Canda)26 have shown what’s possible. But the urgency may be accelerating. Cities of all sizes are competing for talent, tourism, and capital, and these “work-play-stay” districts draw attention and interest. At the same time, fans increasingly expect premium, frictionless, and personalized entertainment experiences that mirror the immediacy and convenience they experience in streaming, e-commerce, and mobile-first services. And as many sports organizations face profitability pressures, investing in the development of a district (especially through real estate and hospitality assets that sit outside of the traditional revenue-sharing models) could be an attractive strategy.

But financial returns are only part of what determines success. Many large-scale developments rely on public partnerships and funding and often receive favorable financing, which increasingly come with expectations to deliver measurable societal impact.27 These multi-purpose stadium districts are uniquely situated to advance community resilience, not only through job creation, economic revitalization, improved housing and quality of life, but through programs and initiatives meant to benefit their communities.28 This could include offering educational and youth sports programming for kids, developing new parks and community spaces, and hosting public health and wellness events.29 And because brands increasingly want to be associated with positive impact and community engagement, these initiatives may also create new sponsorship opportunities, proving that social and commercial value can go hand-in-hand.30 By leveraging stadiums on “non-sports” days, they can become year-round community assets and civic destinations that bring people together and give the district relevance beyond the core fan base.

Looking ahead, purpose-driven sports venues and districts may not be the exception—they’ll be the standard. The next generation of stadiums may be measured not just by returns on investment, but by returns on impact—and how teams, developers, and cities work together to build with not just profits in mind, but purpose.

Strategic questions:

-How can sports districts establish clear and measurable metrics that track both financial performance and community impact?

-How can owners and developers engage communities from the outset so that public benefit is embedded in the project, not added after the fact?

-How can data and AI be used to personalize fan experiences, understand community needs, and inform better stadium and district design?

-How can stadium development be reframed from a cost center into a long-term growth opportunity built on purpose, partnerships, and community value?

Signposts for the future

The global sports industry appears to be expanding in every direction—reshaping how organizations operate, how capital flows, how ownership scales, and how venues integrate into the fabric of communities. AI could strengthen the internal core of sports enterprises; new investment models may demand greater discipline and clarity; global ownership portfolios might blur industry lines and purpose-driven sports districts may redefine impact on and off the field.

The organizations that lead this next era won’t likely be the ones with the most resources, but the ones best prepared to convert expansion into capability, connection, and long-term impact. Because sports aren’t just growing; they are evolving into something bigger.

For 2026, consider the following signposts:

- More sports organizations may begin deploying AI agents for end-to-end workflows (ticketing, game-film analysis, content creation, and logistics).

- Fans may come to expect personalized experiences through location-based promotions, flexible pricing, curated content, and targeted merchandise, powered by AI.

- More leagues may expand their private equity ownership rules.

- More colleges and universities within Power 4 conferences may explore separation between academic and athletic operations.

- Global ownership groups may launch sponsorships and commercial deals that span all teams in their portfolios.

- Municipalities may begin demanding purpose-led commitments from developers and owners before approving stadium builds.

- Non-game day programming may become core to operating models and sponsorships deals.

Continue the conversation

Meet the industry leaders

John R. Tweardy

Kat Harwood

Chad Deweese

Tim Bridge

Jeff Harris

Steven Amato

by

John R. Tweardy

Kat Harwood

Chad Deweese

Tim Bridge

Jeff Harris

Steven Amato

The authors would like to thank Brooke Auxier, Akash Rawat, Jeff Loucks, Doug Van Dyke, Laura Jordan, Pete Giorgio, Todd Kovin Suarez, Brandon Muir, Li-Shen Lee, Jenny Haskel, Sam Renaut, Caitlin Williams, Tim Haaf, Sam Boor, Dan Whelehan, Neisha Schenck, Jeff Harris, Leah Richardson, and Nick Eyer.

Editorial (including production and copyediting): Andy Bayiates, Prodyut Borah, Sayanika Bordoloi, and Cintia Cheong

Design: Molly Piersol

Cover artist: Jaime Austin and Rahul Bodiga; Adobe Stock

Knowledge Services: Rohan Singh

Visit the Deloitte Center for Technology, Media & Telecommunications

Access more insights for the technology, media, and entertainment; semiconductor; telecommunication; and sports sectors.