Who will own the power? AI data centers drive power and utilities M&A

Amid unprecedented market conditions, US power and utilities M&A is often increasingly centered on securing capacity at scale under reliability, capital, and execution constraints

US power demand has entered an unprecedented growth phase, boosted by AI-driven data center expansion and ongoing electrification.1 By 2035, data centers alone are projected to require 176 GW of power nationally.2 However, building new generation and grid infrastructure can be slow and costly due to a number of factors, including permitting delays, supply chain constraints, and upfront investment requirements. Despite record spending by regulated utilities, reliable power to meet expected future growth is becoming increasingly constrained.3

US power sector mergers and acquisitions are stratified across three submarkets: regulated utilities, natural gas generation, and renewables. Across these submarkets, transactions often increasingly center on a single objective: securing deliverable capacity at scale under tightening reliability, capital, and execution constraints.

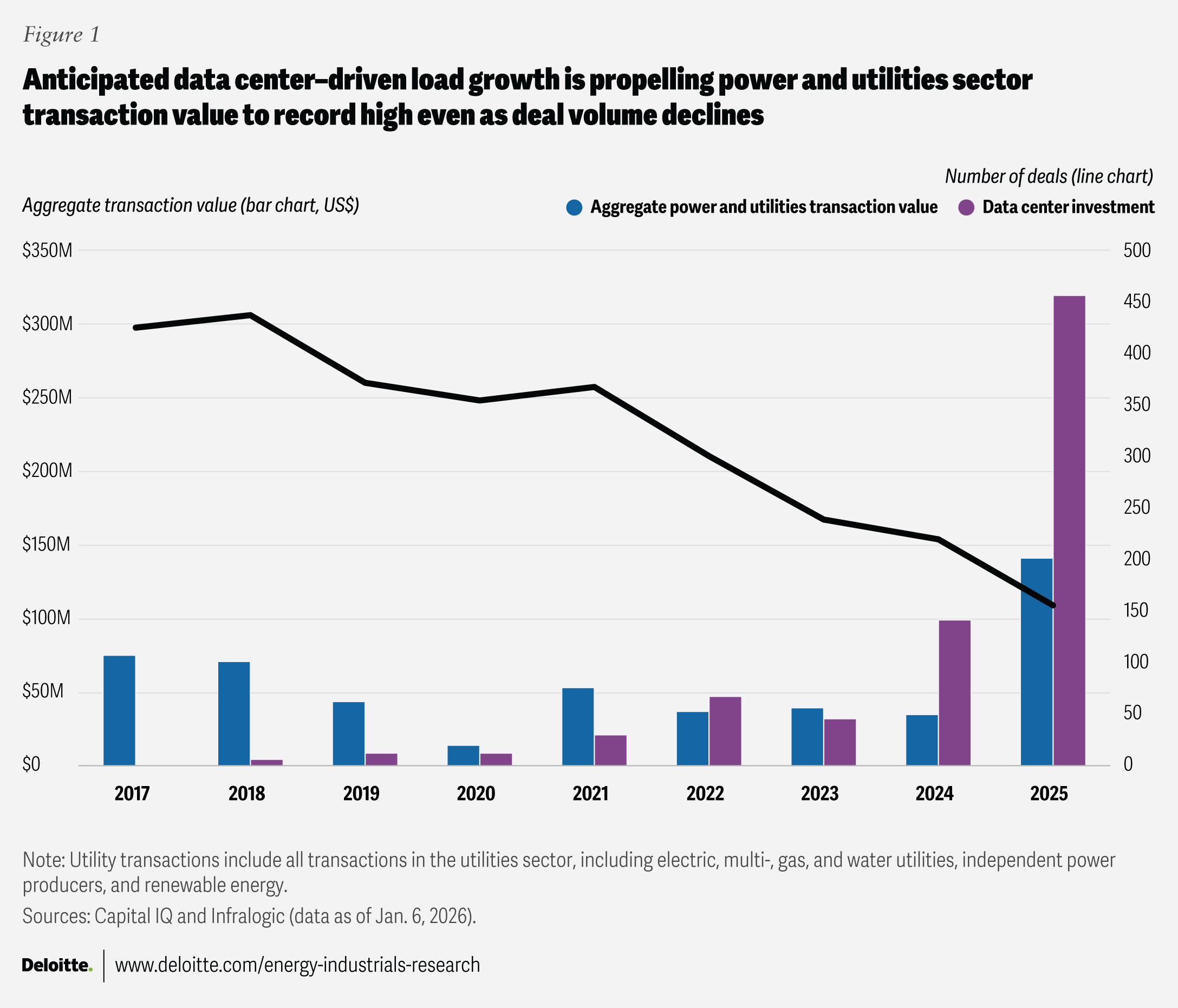

These forces are shaping transaction activity. In 2025, US power and utilities announced transactions reached nearly US$142 billion across 157 deals, driven in large part by Constellation’s US$29 billion acquisition of Calpine.4 Total transaction value exceeded the combined transactions value from 2022 through 2024 (US$112 billion), even as annual deal volume declined from 427 transactions in 2017 to 157 in 2025 (figure 1).5

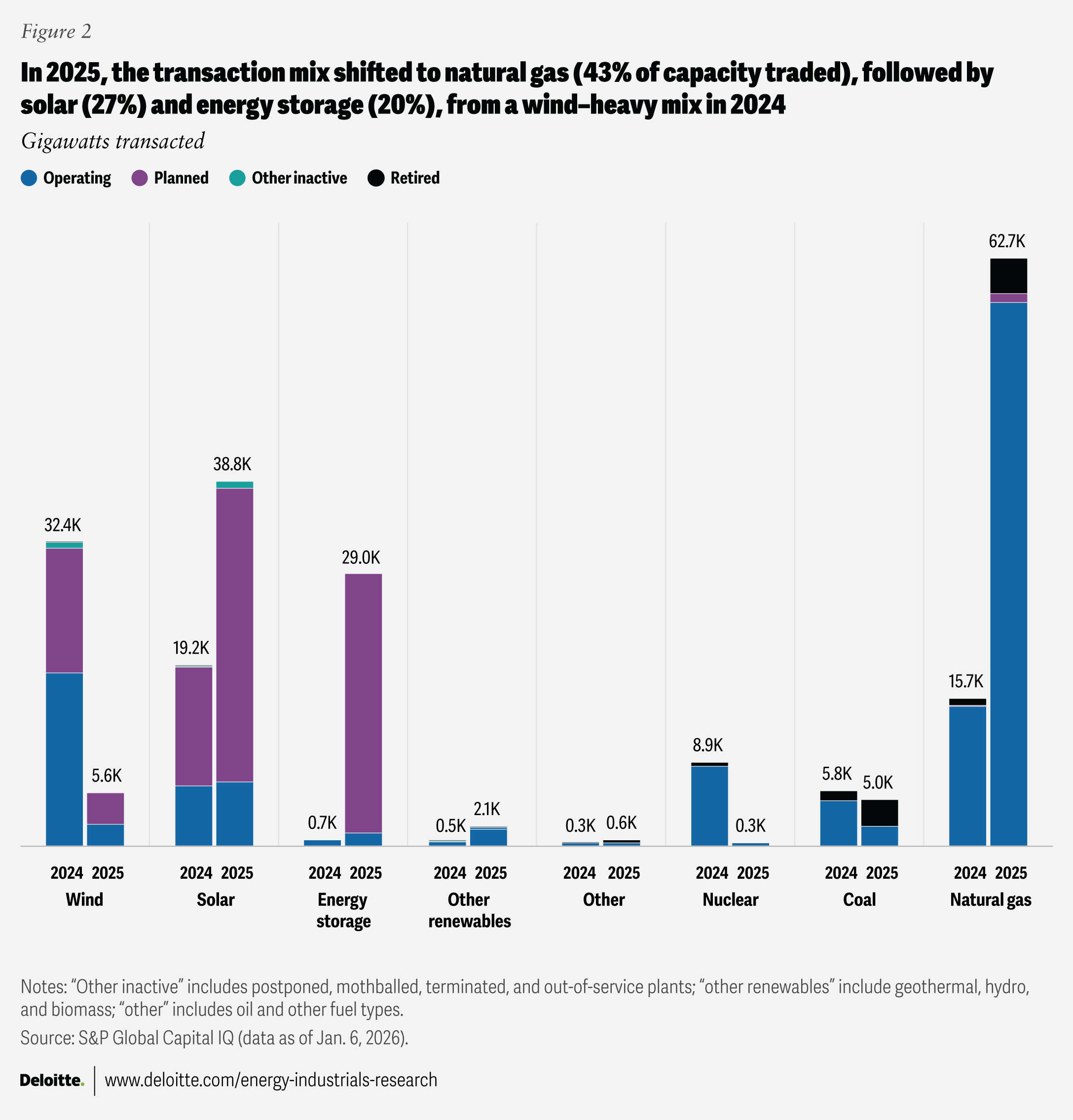

Some investors are buying power capacity at the fastest pace in a decade. Deloitte analysis shows that over 144 GW—10% of total US nameplate capacity—changed hands through dealmaking in 2025.6 Deal size continues to scale rapidly: Eight large portfolio deals (greater than or equal to 1 GW and more than 10 plants) accounted for 113 GW, up from 41 GW across six deals in 2024. At the same time, the capacity mix has shifted toward dispatchable assets, with natural gas accounting for over 40% of the capacity transacted in 2025, while renewables represented more than half of total megawatts traded (figure 2).7

Together, these shifts indicate that the power sector is consolidating and that scale has become important—not only to compete but also to access capital and execute transactions efficiently. Deloitte’s latest M&A survey reflects this shift, with 78% of the surveyed power and utilities executives pursuing transactions citing acquisitions (51%) and mergers (27%) as their top areas of interest.8

Against this backdrop, each submarket—regulated utilities, natural gas generation, and renewables—is now following distinctive M&A dynamics.

Regulated utilities: Focusing on core operations and the stability premium

Unprecedented load growth, record capex expansion, mounting affordability pressures, aging infrastructure, and balance-sheet constraints are asking that regulated utilities adopt more differentiated capital allocation strategies that can prioritize deliverable, rate-based capacity, with affordability and reliability at the top of mind.9

Load growth is contributing to reshaping capital strategy and underwriting discipline: Expected load growth appears to be attracting private capital to regulated utilities, given their stable, rate-based returns. Private capital is pursuing both minority equity investments and selective full take-private transactions. Recent examples include Brookfield’s US$6 billion minority investment in Duke Energy Florida and KKR and PSP Investments’ joint investment in AEP’s Ohio and Indiana Michigan transmission companies.10 Some utilities are also leveraging long-term contracts and partnerships to help underwrite incremental grid and generation investments, reducing execution risks and enabling cost-sharing. This is evident in TVA’s and Dominion Energy’s collaborations with multiple hyperscalers to support multi-gigawatt load additions.11

Divestment is becoming a capital-recycling strategy: Some utilities continue to divest non-core or non-strategic businesses to recycle capital into regulated grid investment, balance-sheet improvement, and load-driven infrastructure expansion. This includes exits from non-core natural gas distribution assets by combined electric and gas utilities, alongside broader portfolio rationalization, which includes divesting unregulated renewable platforms. Recent examples include National Grid’s sale of its renewable business and gas-asset divestitures by CenterPoint and Entergy across multiple states.12

Impact of regulatory stability: Constructive regulatory environments are shaping where regulated utility M&A occurs, in addition to supporting premium valuations. According to S&P Global’s regulatory risk assessments, nine states rank as lower-than-average regulatory risk environments, which tend to exhibit comparatively lower regulatory risk, as evidenced by faster cost recovery and reduced regulatory lag. While regulated utility transactions in 2025 were limited to 20 states, five of these nine states saw deal activity, compared with 20 of 51 jurisdictions (states plus Washington, DC) overall.13

Natural gas generation: Accelerating M&A around dispatchability

Power M&A has shifted toward natural gas generation, with over 62 GW transacted in 2025, quadrupling year over year from just over 15 GW in 2024.14 The shift highlights the growing scarcity value of firm, deliverable capacity that can be executed at scale as load growth accelerates and grid and supply chain constraints tighten.15

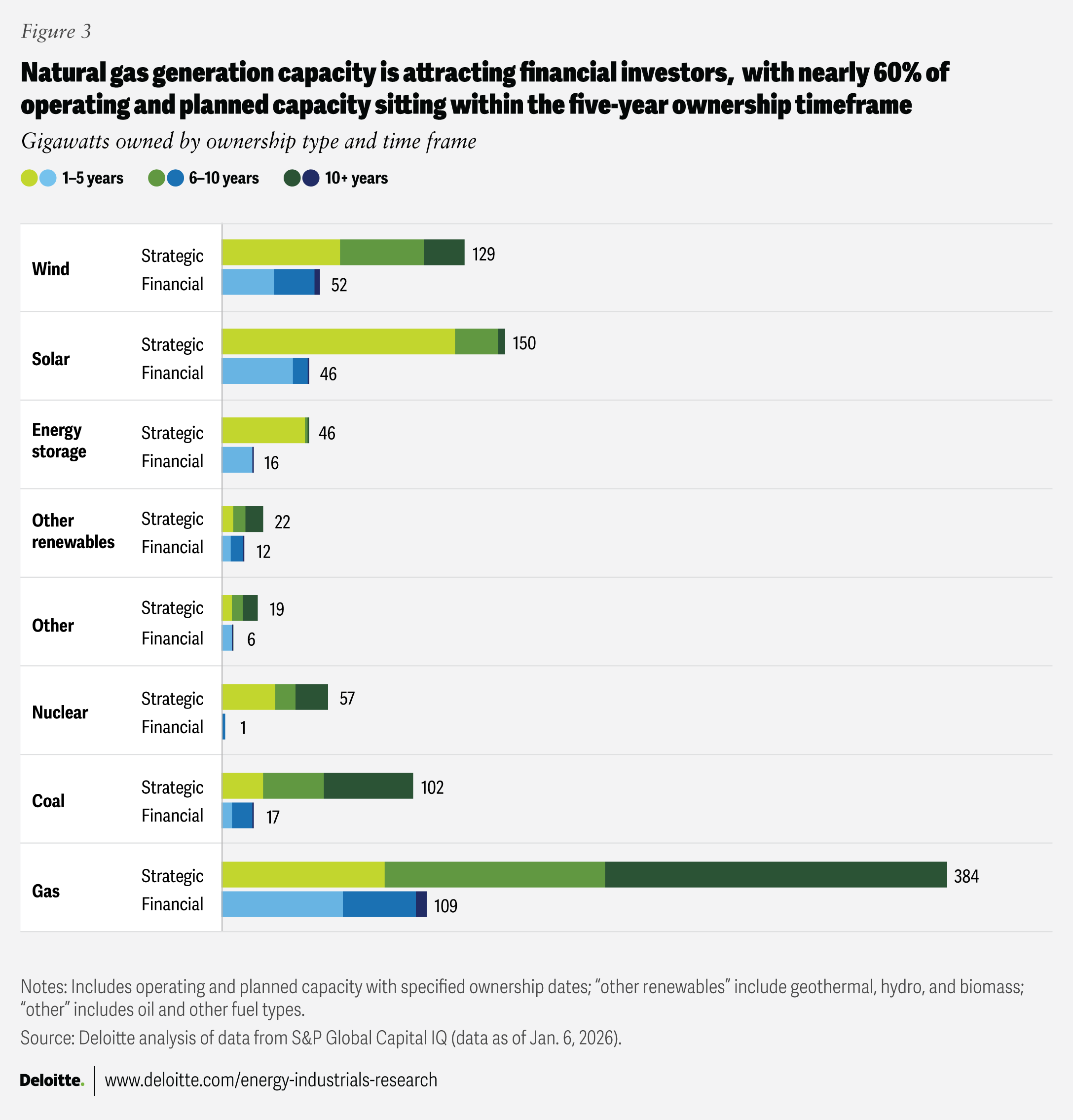

Private capital is accelerating natural gas M&A: In 2025, natural gas generation transactions totaled nearly US$89 billion across 23 deals, with deal value more than tripling year over year.16 Private equity and infrastructure funds accounted for 8.2 GW of natural gas capacity traded in 2025, up from 5.6 GW in 2024, and now own nearly 20% of all operating gas power capacity in the United States (figure 3).17

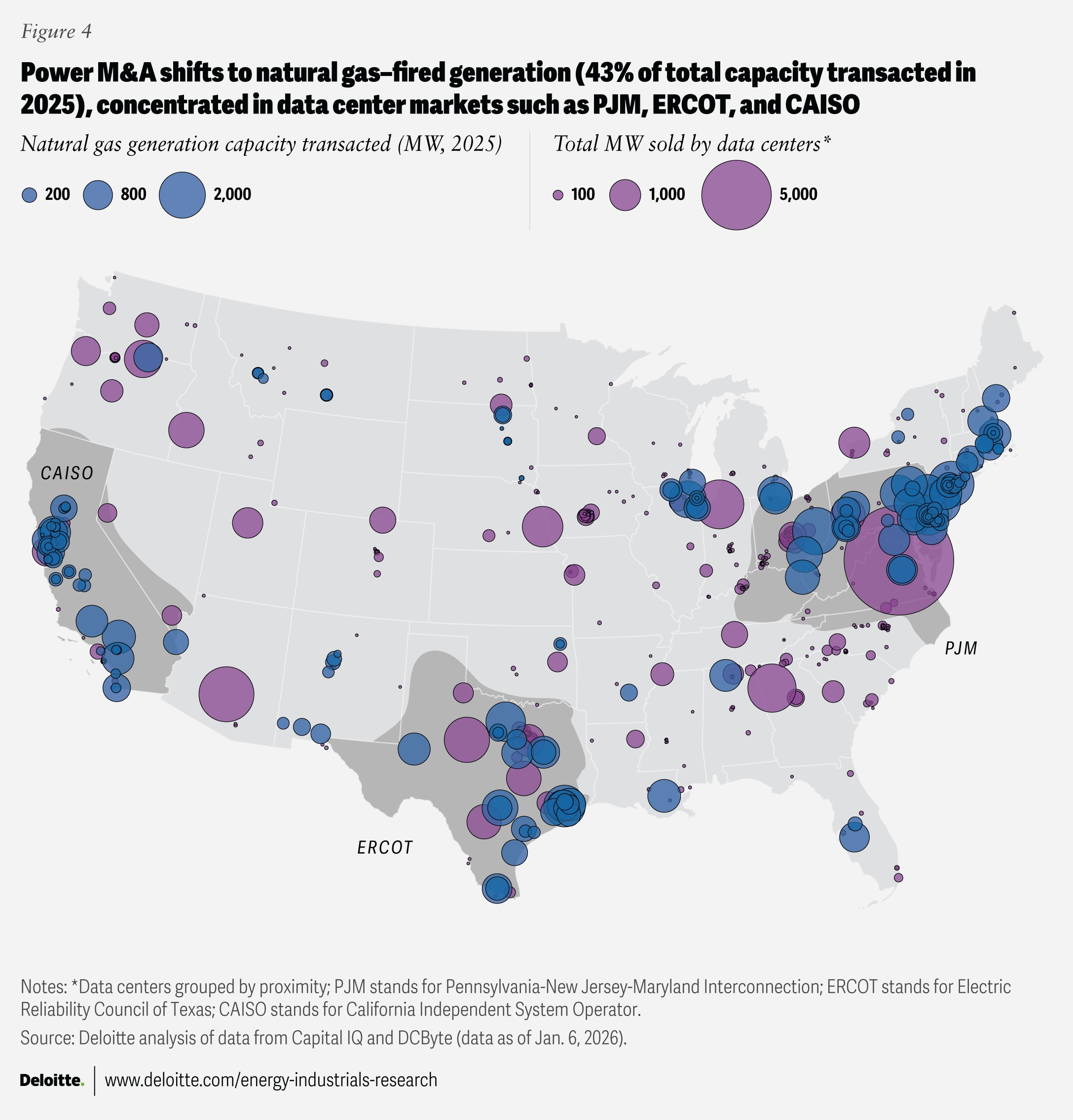

Firm capacity shortages are contributing to a repricing of thermal assets: M&A is increasingly concentrated in gas-fired generation in data center-heavy markets, including Pennsylvania–New Jersey–Maryland Interconnection, the Electric Reliability Council of Texas, and the California Independent System Operator (figure 4).18 Natural gas-fired power M&A valuation doubled compared to 2024 as buyer competition intensified amid elevated new-build turbine pricing and manufacturing backlogs.19 The repricing is extending beyond newer plants to operating gas and legacy thermal assets with established interconnections, transmission infrastructure, and firm deliverability. In response, some utilities and independent power producers are delaying retirements and investing in life-extension upgrades and coal-to-gas conversions to secure near-term, connected capacity.20

These dynamics can make M&A a faster and often more cost-competitive pathway to securing dispatchable capacity than greenfield development.21

Nuclear’s cross-sector momentum

Nuclear has regained momentum since 2024, as executive actions, multibillion-dollar Department of Energy support commitments, utility-led small modular reactor siting programs, and regional consortium efforts have advanced the technology from policy discussion to programmatic planning.22 Momentum has expanded beyond new-build concepts to include restarts and life extensions at existing or previously retired sites, as evident from activities around Duane Arnold, VC Summer, and Three Mile Island.23

Meanwhile, nuclear interest appears to be broadening beyond traditional utilities, reflected in large capital raises for advanced nuclear developers, hyperscaler offtakes, and a cross-sector merger between a social media startup and a fusion company.24 While over 80% of the 24 GW of planned capacity is expected to come online in the 2030s, nuclear’s re-emergence reflects the same underlying imperative shaping power M&A: securing long-duration, deliverable firm capacity.25

Renewables: Consolidation accelerates as capital rotates

Renewables remained the largest driver of power-related M&A in 2025, accounting for more than 75 GW—over half of all capacity transacted—up from 61 GW in 2024.26 As policy uncertainty, interconnection backlogs, and supply chain constraints raise greenfield risks, capital appears to be increasingly concentrated in assets that can deliver capacity with execution certainty, favoring late-stage, de-risked assets over greenfield development.

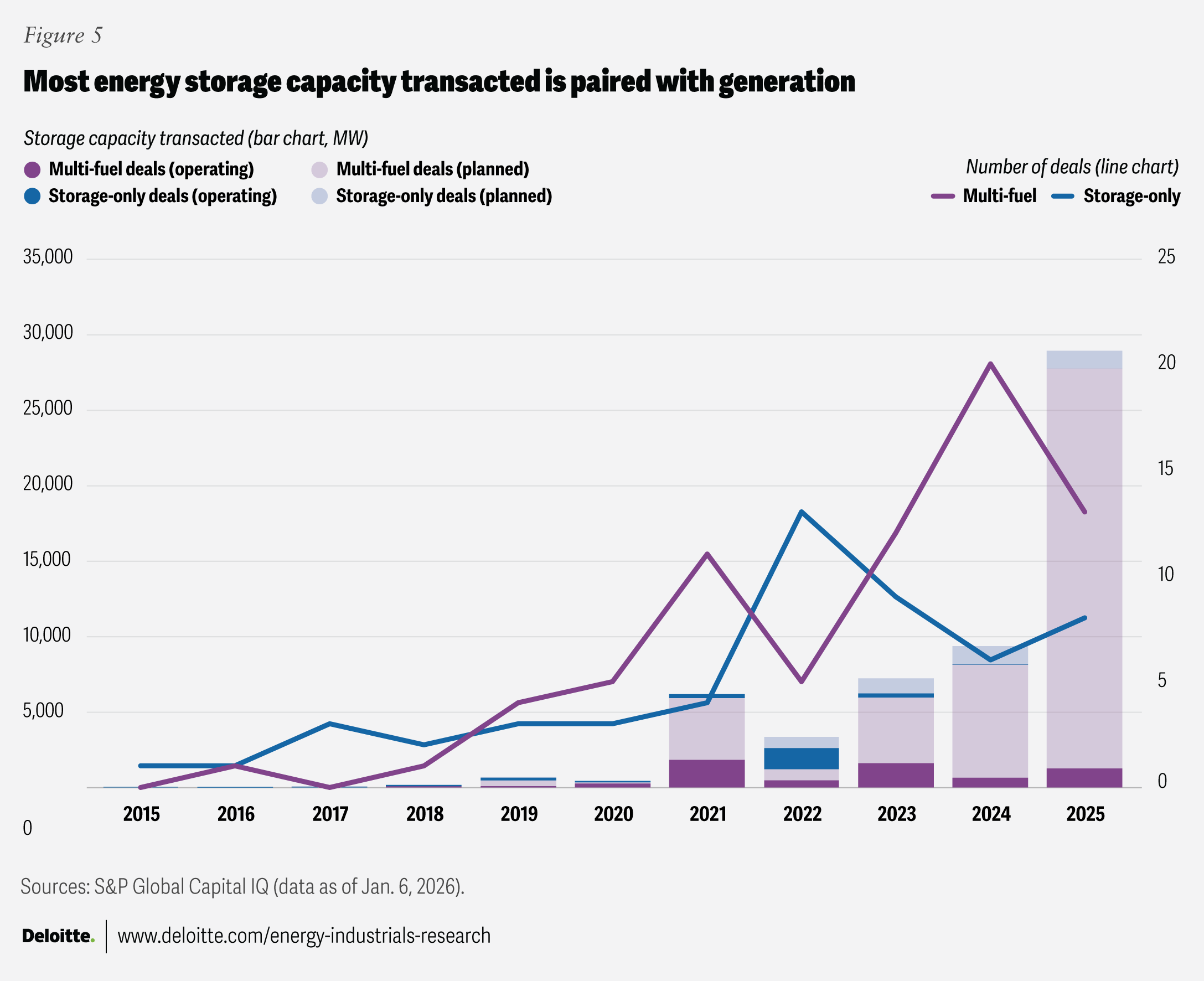

Solar and storage remained attractive, while wind activity slowed: Offshore wind faces policy and regulatory headwinds, driving project cancellations, sponsor retrenchment, and limited price discovery.27 As a result, wind transactions slowed materially in 2025. In contrast, solar and storage activities increased, more than offsetting the decline in wind.28 Buyers appear to be favoring solar-paired storage and multi-market exposure as tools to manage nodal, congestion, and regulatory risks. This preference is likely reinforcing the demand for de-risked assets with firm interconnection positions. Storage M&A reflects this shift toward storage-paired, multi-fuel portfolios (figure 5).

Developer capital rotation stays a core M&A driver: Some developers are monetizing mature projects with fewer risks supported by long-term power purchase agreements (PPAs) to fund new near-term pipelines, accounting for 21% of renewable asset deal volume in 2025.29 Hyperscaler offtake can enhance PPA bankability and financing certainty. Tax credit transferability and safe-harbor rules continue to shape valuations and transaction timing, while uncertainty around corporate tax liability has softened the pricing for the 2025 Investment Tax Credit and Production Tax Credit in transferability markets since the last quarter of 2024.30

Consolidation and capital formation are accelerating for capacity, cost, and control: Some firms are consolidating across adjacent segments and integrating vertically across the value chain, through methods such as acquisitions of distressed assets, to strengthen their market positions.31 In parallel, platform owners are increasingly selling minority equity interests to raise capital and accelerate near-term development opportunities.32 The US solar sector remains fragmented, with over 1,500 owners across 152 GW of operating capacity, creating opportunities for strategic roll-ups by utilities, independent developers, and infrastructure investors.33 Energy-as-a-service providers continue to attract buyers, as evidenced by Dispatch Energy’s acquisition of Green Lantern Solar.34 Vertical integration across the battery storage value chain—ranging from materials to asset ownership—signals increasing competition for supply security, margin capture, and customer access.35

Cross-market strategies to navigate the next wave of M&A

As power markets tighten, a portfolio strategy is emerging in power M&A, centered on three submarkets: rate-based growth platforms, reliability-oriented assets focused on natural gas generation and energy storage, and firm renewable and hybrid assets, including solar, storage, and colocated generation.

Considerations include:

- Focused scale for regulated utilities: Use strategic divestitures and acquisitions to deepen core electric exposure within advantaged markets and raise capital for rate-based growth, rather than diluting capital across both electric and gas utilities.

- Operational and financial scale for generation owners: Monetize reliability attributes through life extensions, uprates, repowering, and selective consolidation to lower unit costs, improve dispatch economics, and enhance access to financing for capital-intensive upgrades.

- Portfolio scale for renewable developers: Optimize capital cycling through M&A to help fund development pipelines, derisk PPA strategies, and leverage tax credit transferability and hyperscaler partnerships to secure growth capital while maintaining operating scale.

- Capital scale and duration for private equity and infrastructure investors: Position portfolios for the next exit cycle by balancing exposure across the three submarkets and targeting undervalued infrastructure platforms with a resilience premium.

Ultimately, ownership is expected to concentrate among large, well-capitalized participants that can assemble balanced portfolios, which deliver capacity while enhancing speed, certainty, and durable cash flows in the power market.

Continue the conversation

Meet the industry leaders

Thomas L. Keefe

Keith Adams

Kate Hardin

BY

Brian Boufarah

Keith Adams

Kate Hardin

Shih Yu (Elsie) Hung

The authors would like to thank Carolyn Amon, Jack Koenigsknecht, Tom Keefe, Catherine King, Susanna Samet, Ethan Erickson, Logan Workman, and Aditi Biswas for their subject matter input and review.

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Rand Brodeur and Kim Buchanan and Aditi Dilip Bhadwalkar who drove the marketing strategy and related assets to bring the story to life; Kaitlin Pellerin for her leadership in public relations; Rithu Thomas and Aparna Prusty from the Deloitte Insights team who edited the report and supported its publication, and Harry Wedel for the visual design.

Editorial (including production and copyediting): Rithu Thomas, Anu Augustine, Pubali Dey, and Aparna Prusty

Design: Harry Wedel and Pooja

Knowledge services: Rohan Singh

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.