From silos to synergy: How utilities are integrating AI and geospatial intelligence for resilience

Faced with rising exposure to weather events, utilities can leverage AI and geospatial intelligence to anticipate risks and integrate resilience planning at an enterprise level

Over the last three years, the United States has experienced a record 78 separate billion-dollar weather events, extending outages and driving up customer costs.1 Outages in 2024 cost customers US$121 billion, up from a seven-year average of more than US$67 billion, and averaged 11 hours in duration, nearly double the average outage duration a decade ago.2

But risk isn’t evenly distributed across the country. Storms hit hardest in the southeast and along the coasts.3 The Western United States experiences four times more wildfire-prone weather days than the East, although the risk of large wildfires is also rising in Texas and Appalachia.4 At the same time, extreme heat and prolonged drought are increasing grid stress across the Southwest, driving higher peak demand and reliability risks.5

These risks are increasing the cost and complexity of maintaining the grid. Vegetation encroachment heightens reliability and wildfire risks, as trees and limbs near overhead power lines can trigger outages, equipment damage, and ignition events. Managing that exposure is costly: Vegetation management alone costs US investor-owned power utilities (IOUs) an estimated US$10 billion annually, averaging nearly US$40 million per utility, according to Deloitte estimates.6

As utilities face growing physical and legal risks,7 rising costs, and increasing system complexity, advanced technologies such as artificial and geospatial intelligence are becoming a larger component of utility resilience investment. These technologies can help integrate hazard, asset, and operational data to improve risk visibility and coordinate mitigation, response, and restoration efforts.

IOUs were projected to invest a record US$207.9 billion in capital expenditure in 2025, including an estimated US$30 billion for transmission and distribution adaptation, hardening, and resilience (AHR).8 Within that total, spending on AHR advanced technologies for transmission and distribution rose 38% from 2023 to more than US$8 billion in 2025.9

However, these investments are only one component of a broader resilience strategy. As utilities expand AHR spending, a greater challenge is that many still tend to operate in silos, with fragmented decision-making across asset monitoring, risk prioritization, preparedness, response, and restoration planning. AI and geospatial intelligence are now integral tools for bridging this gap, helping build synergies where risks, assets, customers, and operations intersect.

Utilities should address acute-risk preparedness gaps

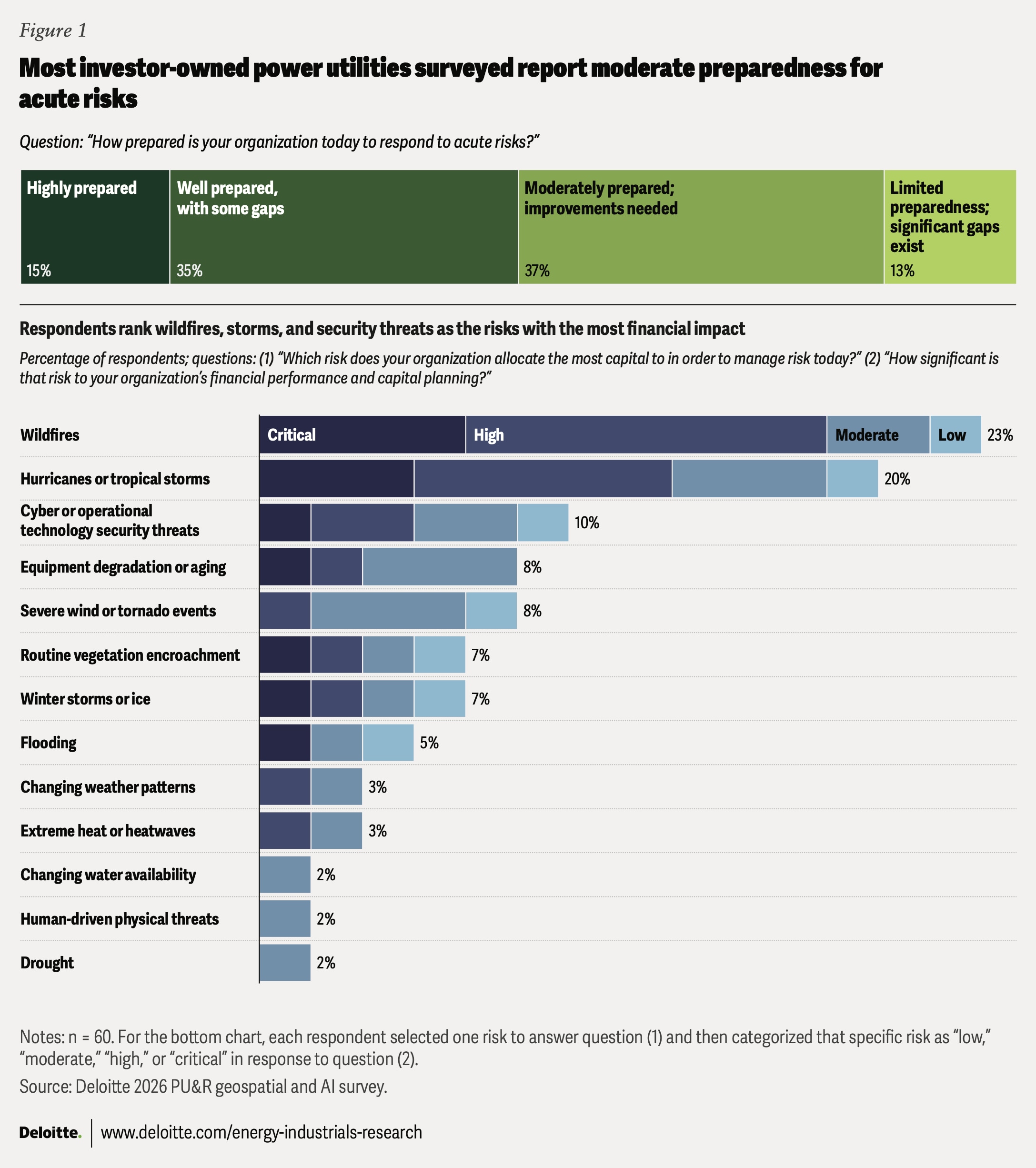

Many utilities do not yet view themselves as fully prepared for acute risks, as indicated in a Deloitte survey of 60 executives from IOUs across more than 40 US states and diverse weather regions conducted in April 2026 (see methodology). Half of the respondents said their organizations are “moderately prepared” (37%) or have “limited preparedness” (13%) to respond to acute risks today, while 35% reported being “well prepared” and 15% “highly prepared.” Wildfires, storms, and cyber or operating technology security threats ranked among the top risks receiving the highest capital allocation, underscoring the need to strengthen resilience capabilities across preparedness, response, and recovery (figure 1).

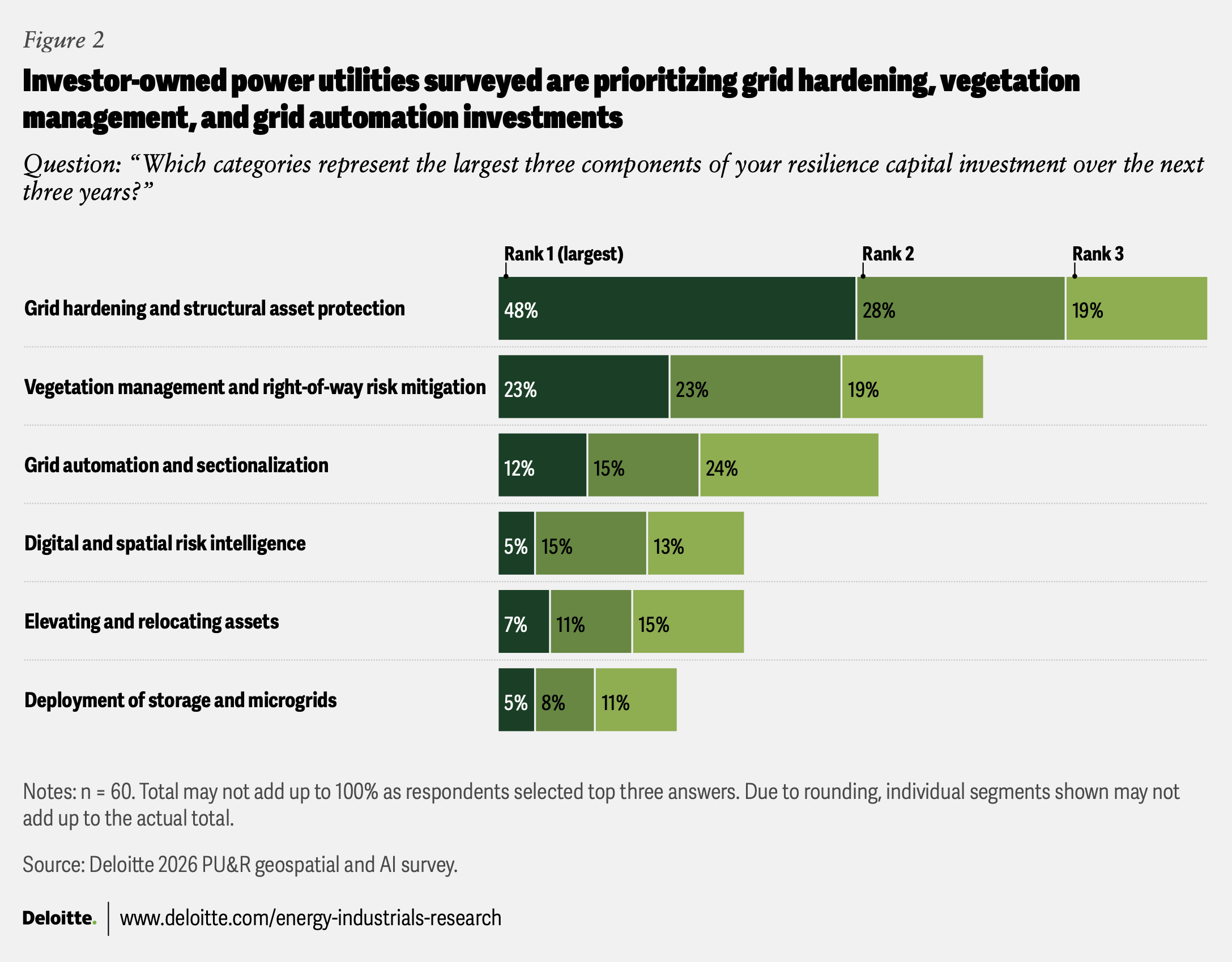

On their part, utilities are concentrating on building resilience—over 60% of IOUs surveyed are directing at least 15% of their capital toward resilience initiatives. More than half of respondents ranked grid hardening (95%), vegetation management (65%), and grid automation and sectionalization (51%) as their top three resilience investments, followed by digital and spatial risk intelligence and elevating and relocating assets at 33% each (figure 2).

As resilience investments expand across grid hardening, vegetation management, and grid automation, utilities should have a clear strategy to prioritize where capital can have the greatest impact. AI-enabled geospatial intelligence can help utilities target mitigation, optimize responses, and accelerate restoration by linking hazard exposure to asset condition, outage risk, and operational readiness.

Building resilience through geospatial intelligence and AI

Consider a hurricane approaching a major city. Two weeks before landfall, preparation ramps up. By integrating satellite imagery, weather forecasts, vegetation data, and operations data, the utility’s geospatial asset model can identify grid assets at risk of failure—poles, power lines, and substations. Crews can then perform targeted tree trimming and other preparatory measures.

As the forecast window narrows to several days, predictive models can recommend optimal staging locations for crews and materials, shifting the focus to response and repair readiness. As outages occur, AI-assisted systems can help triage customer reports for human review and response, drones can rapidly assess damage, and dispatch systems can dynamically optimize crew routes around blocked roads and shifting conditions.

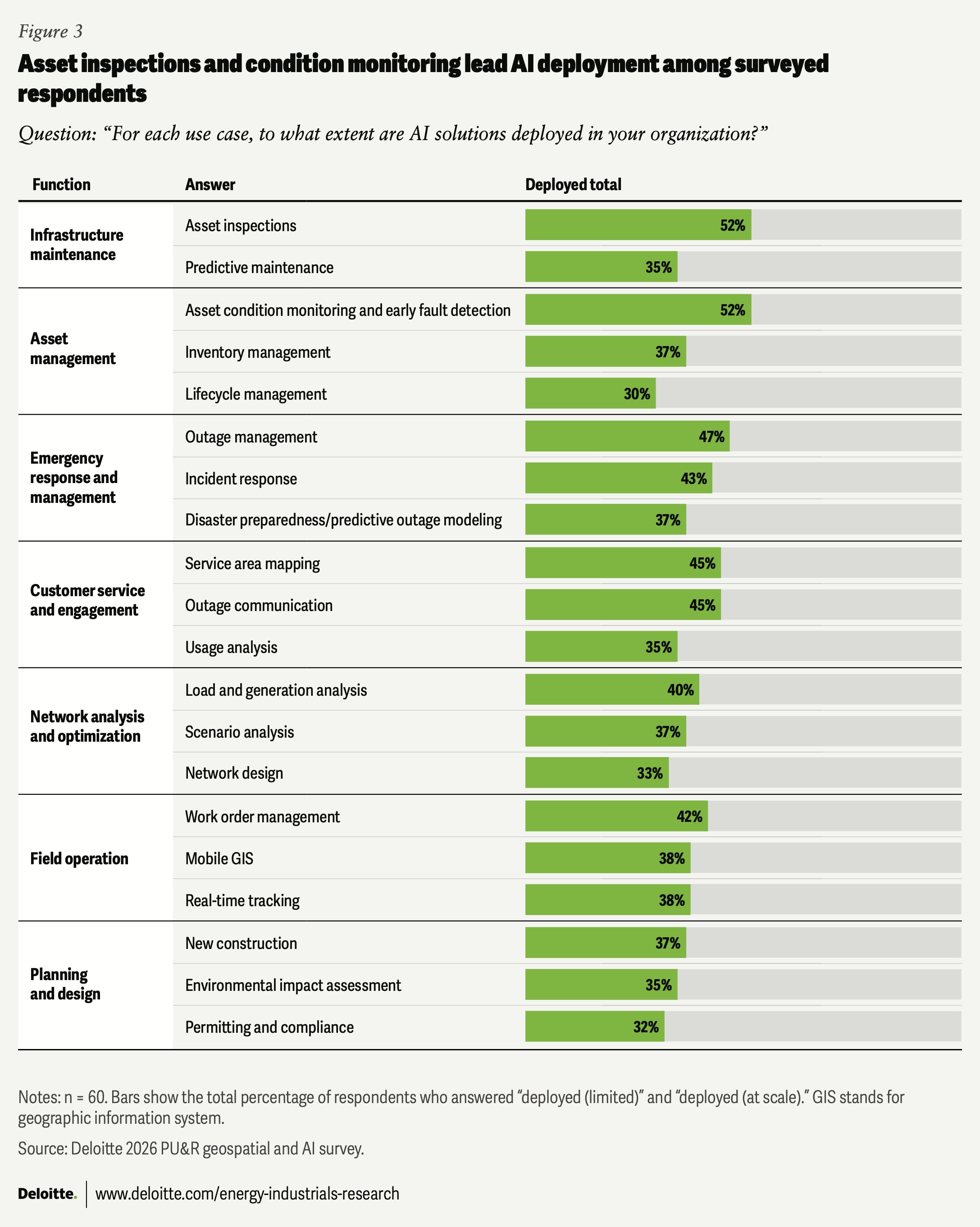

Many of these capabilities, from predictive modeling to mitigation planning and real-time operational optimization, are achievable today.10 Indeed, Deloitte survey respondents indicate that utilities are moving beyond pilots into AI deployment. According to the survey, asset inspections, asset condition monitoring and early fault detection, and outage management have the highest level of AI deployment. Deployment rates exceed pilot rates across 19 of 20 surveyed use cases, signaling broader operational adoption. A next challenge includes scaling the highest-impact use cases while redesigning workflows and preparing the workforce to use AI-enabled insights in planning and field operations. Infrastructure maintenance had the highest overall deployment rate among respondents (35% to 52% across use cases), while planning and design remain the least deployed categories (32% to 37%) (figure 3).

Fragmentation limits enterprise resilience planning

AI and geospatial intelligence can bridge the gap between risk detection and coordinated action, but some utilities still manage hazards risk by risk, using separate teams, tools, and workflows for each. As a result, geospatial and AI capabilities often remain operational tools rather than a strategic orchestrator for enterprisewide resilience planning. As utilities adopt AI across operations, uneven maturity across technologies, enterprise systems, operating models, and capital strategy may limit the integration of these capabilities into integrated resilience planning.

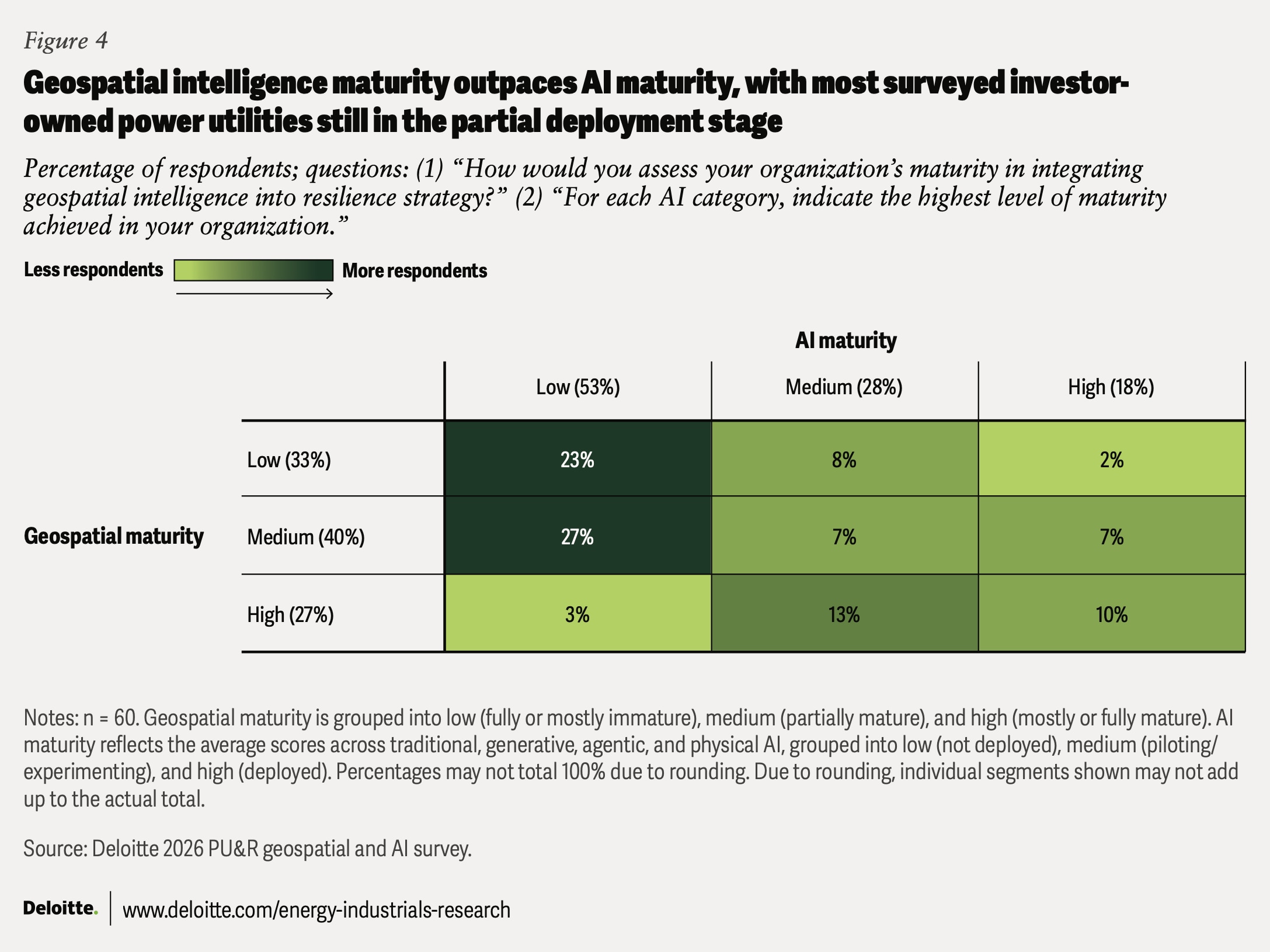

Among surveyed utilities, 100% are piloting or deploying traditional AI, 68% are piloting or deploying generative AI, 42% are piloting or deploying physical AI, and 38% are piloting or deploying agentic AI.11 According to the survey, 27% of respondents have reached high geospatial maturity in their resilience strategy, but only 10% have achieved both high geospatial and AI maturity (figure 4).

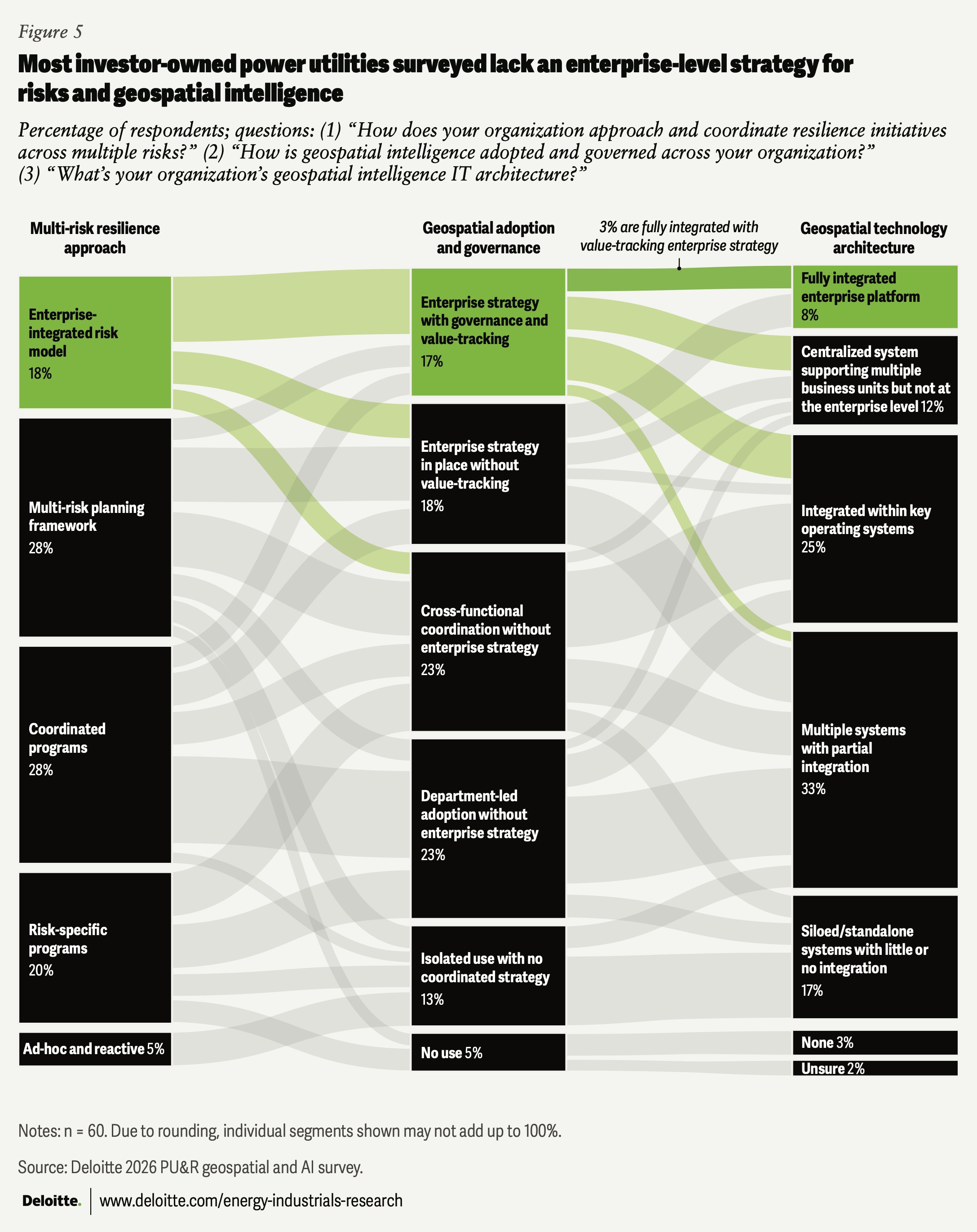

The maturity gap is reflected in three fragmented dimensions—resilience approaches, geospatial governance, and technology architectures—limiting enterprisewide integration into a unified resilience strategy.

Among the surveyed IOUs, 3% are fully integrated across those dimensions with a value-tracking enterprise strategy. For resilience, 18% have adopted an enterprise-integrated risk model, while 28% use coordinated programs and 5% remain ad hoc and reactive across multiple risks. Only 35% of respondents have adopted an enterprise strategy for geospatial intelligence, while 8% have a fully integrated enterprise platform (figure 5).

This suggests the integration challenge is not only technological. Utilities should have clear ownership, governance, and cross-functional ways of working to connect decisions across operations, engineering, regulatory, finance, and technology functions.

This fragmentation can keep geospatial and AI confined to operational silos, rather than embedding them in decision-making across the enterprise. In practice, without shared data layers and interoperable architectures, utilities may struggle to build a common view of risk across planning and operations. Among the 20% of respondents with a centralized or fully integrated geospatial intelligence technology architecture, 92% said the IT technical strategy was set using the enterprise strategy, suggesting integrated architectures may support more coordinated organizationwide planning (figure 5).

Drivers and challenges for investment and integration

As per Gartner® Market Share, “Software represents the largest share (37%) of nearly US$105 billion in IT spending by US power and utilities in 2025, and is expected to exceed US$70 billion by 2029, accounting for 44% of sector-wide IT spending.12 This broader shift toward software-enabled operations includes growing investment in geospatial and AI, consistent with Deloitte’s survey results. Among respondents, 67% expect an increase in investment in geospatial intelligence and AI in their organizations over the next five years.

Resilience and risk exposure drive AI and geospatial investment

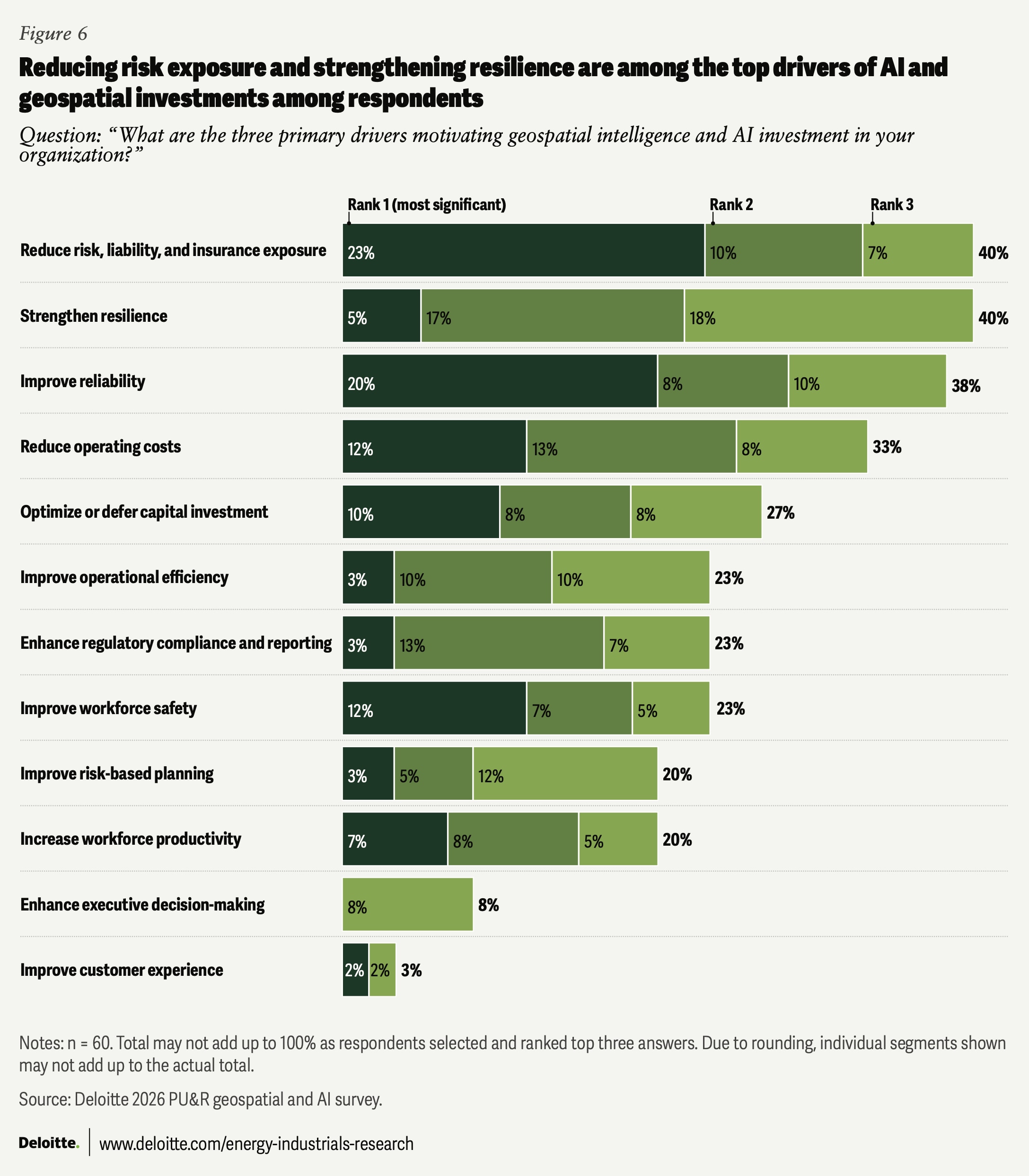

As utilities face growing environmental, reliability, and liability exposure, those surveyed indicate that geospatial and AI investments are increasingly being driven primarily by resilience, risk, and reliability priorities. Survey respondents ranked reducing risk, liability, and insurance exposure (40%), strengthening resilience (40%), and improving reliability (38%) as the top three drivers of geospatial and AI investments (figure 6). Additionally, reducing operating costs and improving workforce safety were ranked among the most significant investment drivers by 33% and 23% of the respondents, respectively.

Yet higher spending alone cannot drive enterprise-level adoption.

Infrastructure and process constraints remain key challenges to integration

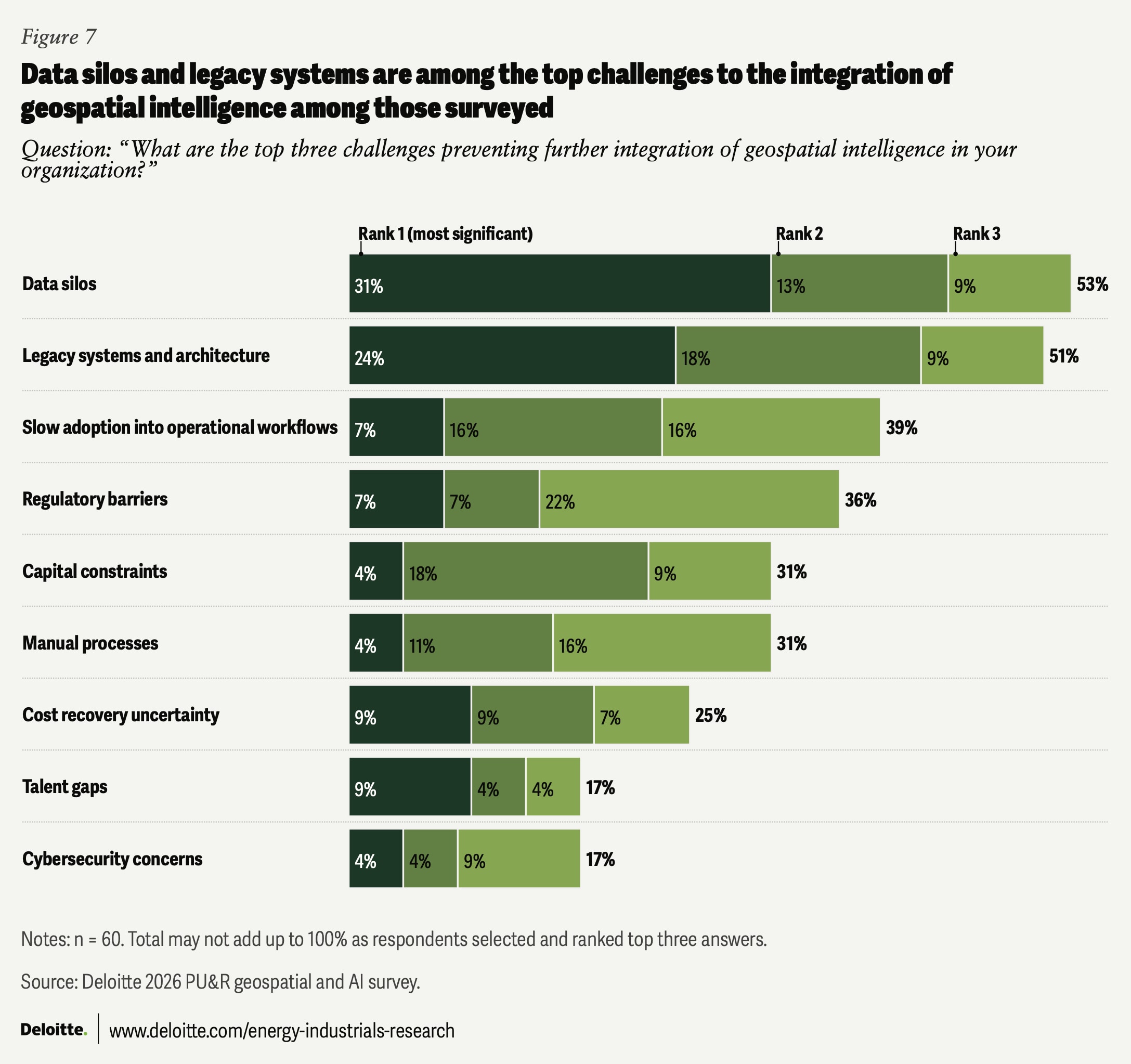

Data silos and legacy systems are the top challenges to integrating geospatial intelligence, but the challenge also extends to workflow adoption. Among responding organizations without a centralized or integrated geospatial intelligence technology architecture, 53% of the respondents identified data silos as a top three challenge preventing further integration of geospatial intelligence, followed by legacy systems and architecture (51%), slow adoption into operational workflows (38%), and regulatory barriers (36%) (figure 7).

These challenges suggest that, beyond building shared data architectures, utilities may need to also redesign workflows, train users, and embed geospatial insights into day-to-day operations.

Moving from silos to synergy

AI-enabled geospatial intelligence belongs at the heart of grid resilience because resilience is shaped by geography, evolves over time, and crosses organizational boundaries. Utilities need to see where hazards, assets, customers, crews, and outages intersect to help anticipate risks, coordinate preparedness and response, and prioritize investment decisions.

To realize the full value from AI-enabled geospatial intelligence, utilities should move it from fragmented deployments toward the core of an enterprise-wide resilience strategy. They could take several strategic steps:

- Embed geospatial intelligence into regulatory and investment strategy: Use geospatial intelligence to support capital prioritization, rate case justification, risk management, liability mitigation, and cost recovery planning.

- Target high-ROI use cases: Direct investments based on regional risk exposure, infrastructure vulnerability, and restoration costs to improve resilience outcomes and strengthen capital planning.

- Align cross-functional operating models: Reduce the business and technology divide by establishing shared governance, organizational ownership, and ways of working across operations, engineering, regulatory, and technology functions.

- Redesign workflows and upskill the workforce: Scale geospatial intelligence across planning and field operations through process redesign, workforce training, and change management.

- Build integrated geospatial architecture: Develop interoperable geographic information systems and shared data architectures that integrate asset, outage, weather, vegetation, customer, and field operation data.

The next frontier of utility resilience is not incremental technology deployment but using geospatial intelligence to connect strategy, operations, and capital planning. By moving from silos to synergy, utilities can become more reliable and resilient. They can reduce risk before events occur, restore more quickly during disruptions, deploy capital more efficiently, and lower avoidable restoration and recovery costs.

Methodology

The Deloitte Center for Energy and Industrials conducted a survey in April 2026 to identify the challenges, risks, and strategies related to the resilience of US investor-owned electric utilities, and to benchmark their maturity in integrating AI and geospatial intelligence. The survey sampled one respondent from each of 60 individual operating companies, who responded to questions on capital prioritization, risk exposure, resilience readiness, vegetation management, remote sensing, maturity levels on geospatial intelligence and AI adoption and integration, and investment drivers and priorities.

Continue the conversation

Meet the industry leaders

Thomas L. Keefe

Travis Parker

Kate Hardin

by

Travis Parker

Kate Hardin

Shih Yu (Elsie) Hung

The authors would like to thank Sudip Roy, Kacey Pham, Will McKinnon, Ethan Erickson, Jaya Nagdeo, Carolyn Amon, Catherine King, and Julia Tavlas for their subject matter input and review.

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Randy Brodeur, Kim Buchanan, and Aditi Dilip Bhadwalkar, who drove the marketing strategy and related assets to bring the story to life; Kaitlin Pellerin and Mariel Balaban for their leadership in public relations; Rithu Thomas and Aparna Prusty from the Deloitte Insights team, who edited the report and supported its publication, and Harry Wedel for the visual design.

Editorial (including production and copyediting): Rithu Thomas, Aparna Prusty, Anu Augustine, Pubali Dey, and Cintia Cheong

Design: Harry Wedel

Cover image by: Sanna Saifi and Adamya Manshiva

Knowledge services: Vanapalli Viswa Teja

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.