{kind=link}

{kind=link}

{kind=link}

{kind=link}

This section includes survey questions and complete response options:

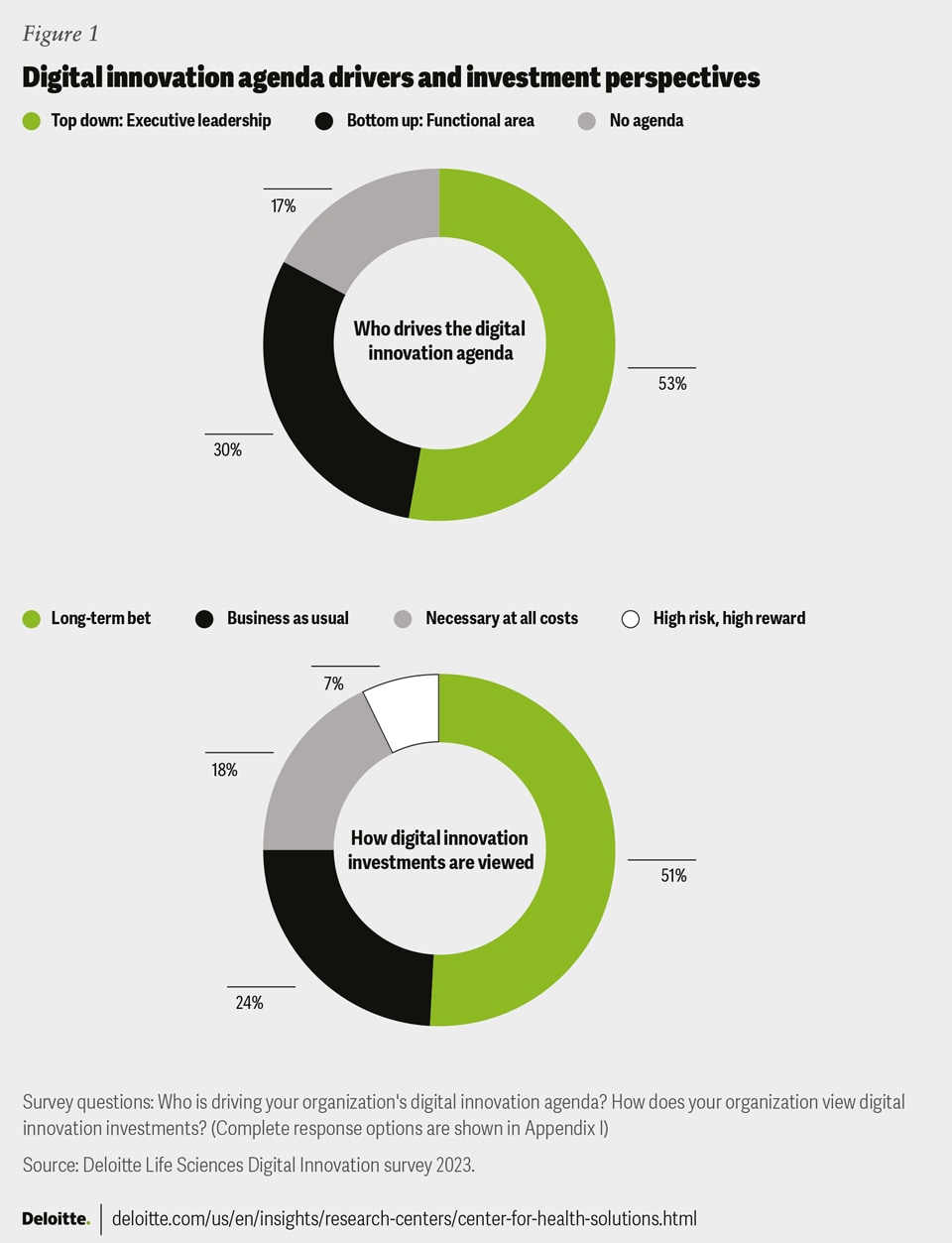

Appendix I: Who is driving your organization's digital innovation agenda?

- Top-down: My organization's executive leadership drives our digital innovation agenda.

- Bottom up: Each functional area is responsible for developing their own digital innovation agenda.

- Neither: My organization lacks a defined digital innovation agenda.

Appendix I: How does your organization view digital innovation agenda?

- High risk, high reward: We don't expect the majority of investments to pay off, but those that do will yield significant benefits.

- Necessary at all costs: We need to make these investments in order to compete, regardless of their costs.

- Long-term bet: We expect that the majority of investments will pay off, but not in the near term.

- Business as usual: We view digital innovation projects in the same way as other investments.

Appendix II: Which of the following best describes your organization's current approach to adopting innovative technologies?

- Early adopters: We are visionaries that quickly adopt innovative technologies and set the pace for the industry.

- Fast followers: We tend to follow the path of our competitors after they have proven the value of innovative technologies.

- Laggards: We are slow to adopt innovative technologies and do so years after our competitors.

Appendix III: Please rank the use cases that you believe are best positioned to be positively impacted by innovative technologies.

Innovation and product development:

- Precision patient recruitment: Data-driven analysis of clinical, real-world data, and socioeconomic information to precisely target and recruit patients

- Digital clinical trials: Use of digital technology to remotely set up and conduct trial protocols

- Regulatory intelligence: Monitoring and analyzing regulatory changes and requirements to ensure compliance for products

- Digital therapeutics: Development of clinical interventions that can be delivered to patients via software to treat, manage, or prevent a disease or disorder

- Data-enabled therapies: Devices that collect and analyze patient data and/or deliver therapy, connected with other devices and platforms

Manufacturing and supply chain:

- Smart factory: Automation of factory floor activities by employing AI, IoT, and other next-generation technologies

- Net-zero and sustainability: Tracking emissions data, and employing AI and analytics to drive efficiencies

- Autonomous supply chains: Automatic adaptation to changing supply and demand and prediction of bottlenecks (e.g., inventory and capacity tracking)

- Supplier risk management: Understanding and predicting supplier risk to mitigate the effects of global/geopolitical events (e.g., pandemics)

- Digital twin: Digital models of plants or warehouses that leverage RWD to simulate operations and generate insights

- Digital information exchange with customers: Use of technology to provide product information, support, and services to customers

Marketing and commercial:

- Next-best engagement: Employing dynamic, AI-based recommendations to optimize engagement of health care providers and patients

- Omnichannel engagement: Data-driven execution of marketing, sales, and customer service via the right channels, platforms, and mediums

- Patient health and experience: Branded and above-branded longitudinal engagement of patients to promote health and wellness

- Content velocity: Automation of marketing content development and regulatory review

- Gross to net or revenue cycle management: Data- and analytics-driven optimization of sales and market access data to drive pricing and go-to-market strategies

- Customer service augmentation: Use of IoT, predictive analytics, and AI to proactively service equipment in need of repair