How AI-native banking products could reshape institutional banking

Embedding AI into treasury, payments, and securities services could unlock new revenue streams for banks

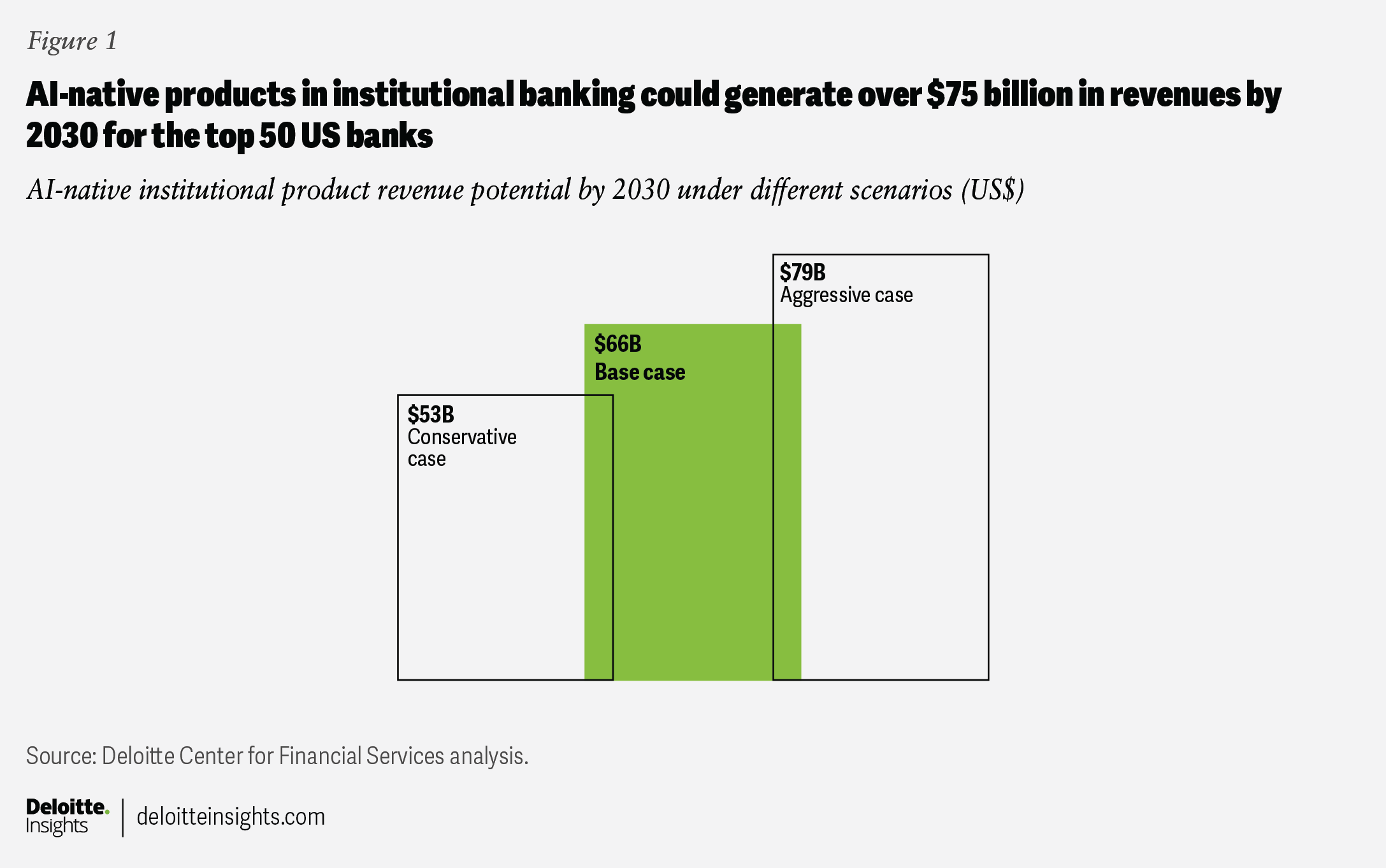

The Deloitte Center for Financial Services predicts that, by 2030, AI-native products could account for as much as 25% of institutional banking revenues among the top 50 US banks.1 This equates to approximately US$66 billion in revenue in the base case, with an upside scenario exceeding US$75 billion, as illustrated in figure 1 (see “About this prediction”).2

Banks are approaching an inflection point in how artificial intelligence shapes revenue generation. The focus appears to be shifting from efficiency gains to topline growth, with AI moving from internal productivity tools into the core architecture of client-facing products.

It’s not hard to envision that, by 2030, AI will be ubiquitous in almost all products offered by the banking sector, so much so that there could be two main types of banking products: AI-enabled and AI-native. Unlike AI-enabled products that only improve existing features and how they are delivered to clients, AI-native products represent a bigger leap, with AI built into their core from the ground up.

These offerings are likely to include treasury-orchestration platforms, intelligent payment-routing engines, intraday liquidity optimizers, trade-documentation agents, receivables-reconciliation systems, and continuous credit-monitoring tools. Such products could continually monitor financial activity, make decisions within defined governance guardrails, and execute actions while escalating exceptions.

What changes when AI runs the product

With AI-native products, AI becomes the operating engine rather than an enhancement layer. For example, a treasury platform run by autonomous agents that continuously optimize liquidity and execute actions within defined policies is not merely a smarter dashboard—it is potentially an entirely new, stand-alone product. As such, the value proposition of AI-native products changes accordingly. The path to fully AI-native products, however, will likely pass through stages, where AI drives a greater proportion of product performance and delivery while humans remain responsible for oversight and exception handling.

And AI-native products in banking are not a far-off concept. Take buy now, pay later (BNPL) financing: When a customer applies for a BNPL loan at the point of sale, the credit decision is made instantly through automated underwriting, without any human involvement. Similarly, Wells Fargo’s Integrated Receivables solution uses AI and machine learning to automatically capture remittance information and match incoming payments to invoices, helping corporate clients reconcile receivables faster and reduce manual interventions.3 In both cases, AI operates at the core of the product experience, continually executing financial tasks rather than simply supporting them.

Structural conditions that drive value

The potential for AI-native products is highest in environments where decisions are frequent, data-rich, and occur within defined but flexible constraints. These are not purely rules-based processes but domains where judgment, optimization, and adaptation are required within regulatory and risk boundaries. For AI-native capabilities to be viable, the value they generate must also be economically meaningful and attributable—such as improved execution quality, optimized liquidity, enhanced pricing, or stronger risk outcomes, rather than just faster processing or lower costs. Governance remains critical, but it functions as a set of guardrails rather than rigid rules, enabling AI systems to operate dynamically while maintaining compliance and control.

Many institutional banking products already meet these conditions, combining high volumes of structured and unstructured data with recurring, yet complex, decision-making processes embedded in client workflows. Treasury functions are a good example: As cash positions, funding needs, and exposures become more dynamic, treasury teams must operate across fragmented systems with limited real-time visibility, relying heavily on manual reconciliation and static forecasts.

This makes treasury particularly well-suited for AI-native solutions. These products embed intelligence directly into workflows, using probabilistic forecasting,4 automated data aggregation, and agentic copilots that can recommend and execute actions—such as liquidity sweeps—within defined governance guardrails and with full auditability.

Platforms like J.P. Morgan’s Cash Flow Intelligence illustrate this shift: This product consolidates and categorizes transaction data in real time, enabling continuous cash visibility and forward-looking insights without manual intervention. The impact is tangible: For clients like Domino’s, the platform reduced manual data cleanup by up to 90%, allowing treasury teams to shift their focus from operational reporting to strategic decision-making and liquidity optimization.5

Securities servicing presents a different profile. It is more operational and compliance-intensive, with stricter requirements around governance, data provenance, and cross-border regulation. As a result, most AI applications in custody and post-trade today are embedded as efficiency gains rather than stand-alone products. That said, this is beginning to shift as banks isolate specific workflows—such as document verification and corporate action processing—and package them as auditable, AI-driven modules.

Early examples are emerging. Clearstream’s OSCAR enables clients to define and negotiate collateral rules using natural language while optimizing eligibility criteria in real time. Similarly, its Next Data Solutions platform packages AI-driven analytics for settlement, collateral, and liquidity decisions into client-facing securities services, signaling a move toward more productized AI capabilities in this space.6

The potential for AI-native products in institutional banking varies significantly by product characteristics, service complexity, and regulatory constraints. Treasury and payments sit at one end of the spectrum, where returns can be immediate and measurable—such as improved cash visibility, days sales outstanding, and liquidity deployment—making it easier to package AI capabilities as distinct, revenue-generating modules. By contrast, more operationally intensive areas like securities servicing face higher barriers, slowing the transition from embedded efficiency gains to fully productized AI offerings.

Barriers to scaling AI-native banking products

Transitioning to purely AI-native products in institutional banking will likely face some challenges.

Modern technology and data infrastructure

A deeper structural barrier to AI-native products is legacy technology and fragmented data architectures that were not designed for real-time execution, continuous decisioning, or integrated data flows across systems. AI-native services require continuous data flows, API-driven interoperability, and scalable computing infrastructure—capabilities difficult to layer onto older technology stacks. As a result, banks with modern cloud-based architectures and unified data platforms are likely to move faster in deploying AI-native products, while others may struggle to overcome the constraints of legacy systems.

AI-native operators improve materially when they have access to a complete, cross-product view of a client’s financial position. Today, there are no consistent standards or policies governing what data these systems can access or use. As a result, data accessibility and interoperability will directly determine how quickly cross-institution AI-native products can develop and scale.

Trust and governance

AI-native products require what can be called permissioned autonomy. They cannot be deployed like chat features but require explicit customer consent, configurable policy guardrails, controlled execution rights, and continuous monitoring. In effect, governance becomes part of the product itself, defining how AI systems act, escalate decisions, and maintain trust.

AI-native products require customers to allow systems to monitor accounts, make decisions, and, in some cases, execute financial actions as well. That level of delegation requires a high degree of trust in the bank’s controls, transparency, and reliability. Banks will need to demonstrate that AI systems operate within all regulatory and policy requirements, explain their actions, and provide customers with the ability to review and, when needed, override decisions. Lacking a high degree of confidence, customers may balk at handing over financial authority to AI-driven products.

Economic and pricing models

Pricing AI-native banking products will be another challenge as banks determine which customers are willing to pay for fully AI-driven capabilities. Likely models include subscription tiers, usage-based fees, and outcome-based pricing tied to measurable improvements like fraud reduction and liquidity optimization. Pricing power may hinge ultimately on demonstrated outcomes, performance guarantees, and integration into broader financial ecosystems.

As AI lowers marginal costs and competitors replicate similar capabilities, many AI-native features may likely become standard, leaving durable pricing power only where banks can prove sustained economic value.

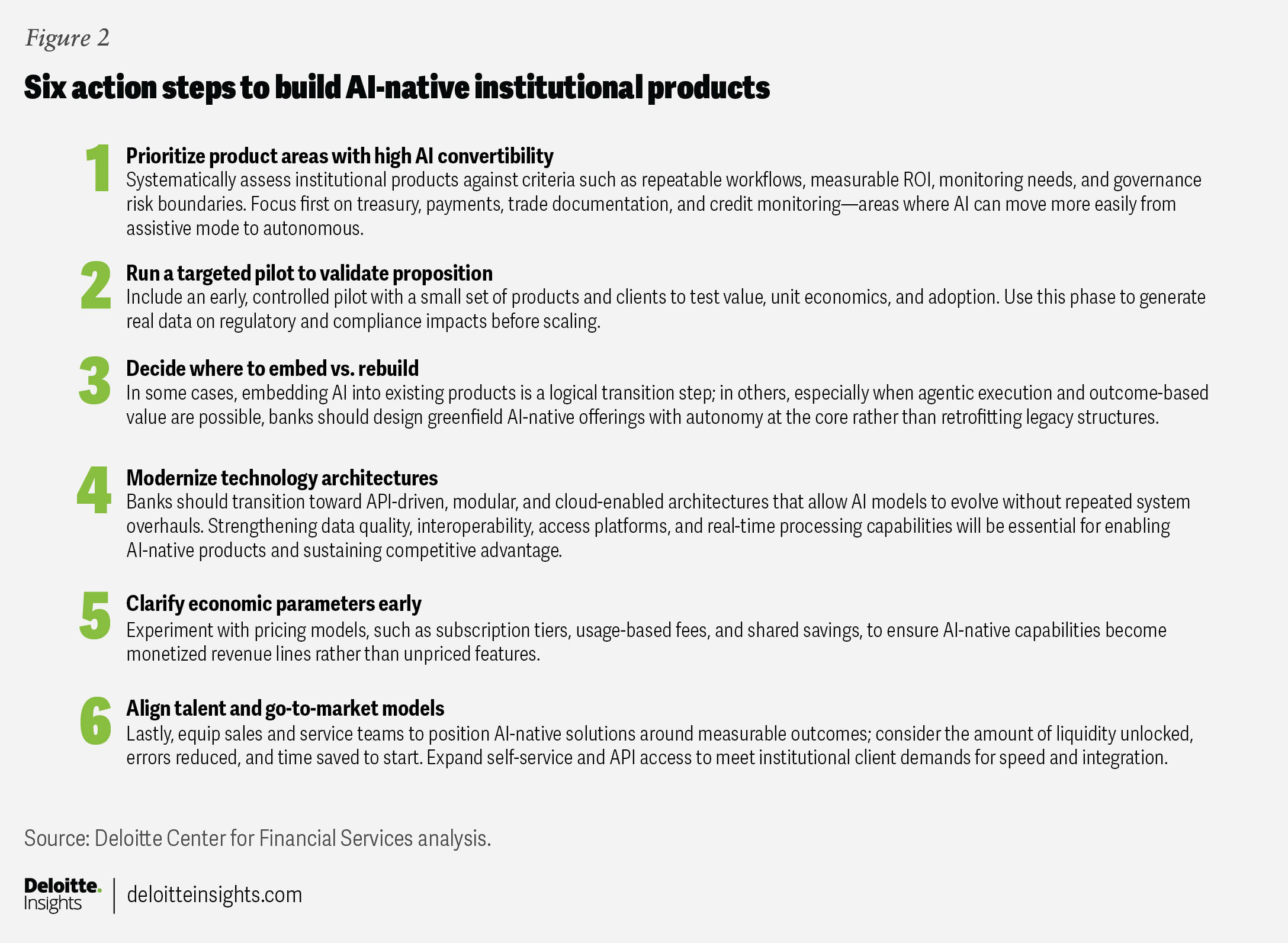

Transitioning from AI-enabled enhancements to AI-native products requires a deliberate shift in how banks design, build, and commercialize their offerings. Figure 2 outlines six actionable steps to help institutions prioritize high-impact use cases, validate value early, and scale AI-native capabilities across institutional banking.

AI-native capabilities represent a structural opportunity to redesign institutional banking products. Banks that move early to embed AI into the core of their offerings can shift how value is created, delivered, and monetized.

About this prediction

This analysis focuses exclusively on AI-native products within institutional banking, defined here as corporate lending, treasury and cash management, trade finance, and securities servicing. Trading and advisory-driven investment banking businesses are excluded given their distinctive revenue dynamics.

Our estimate of AI-native revenue for 2030 uses a top-down approach. First, we calculated the total revenue generated by the largest US banks and estimated the portion attributable to institutional banking businesses, including payments, transaction banking, lending, and treasury services. We did not include the capital markets businesses.

Next, we assessed individual institutional product segments to determine their potential for AI adoption. This evaluation considered both adoption likelihood and AI convertibility, focusing on factors such as workflow repeatability, data intensity, event-driven processes, and the ability to operate within defined regulatory and client guardrails.

Based on this analysis, we estimated the share of institutional banking revenue that could become AI-native by 2030, meaning those products and services ripe for embedding AI directly into their core workflows and operating models. Finally, we applied this estimated AI-native share to projected institutional revenue for the top US banks in 2030 to derive the potential scale of AI-native revenue.

By

James Delbridge

Val Srinivas

Shivalik Srivastav

The authors would like to thank John Labate and Karen Edelman for their contributions to this article.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover artist: Sofia Laviano

Knowledge services: Agni Wagh

Visit the Deloitte Center for Financial Services

Access more insights for the banking & capital markets, commercial real estate, insurance, and investment management sectors.