Tax, CSRD and Double Materiality Assessment

At a glance

The EU Corporate Sustainability Reporting Directive (CSRD) requires companies to report on sustainability topics that are material to their organization, including tax, when tax is identified as such.

While materiality concerns will naturally vary by organization, shaped by each entity's unique context, industry, sustainability goals and stakeholder expectations, there are certain factors that elevate tax to a material issue. Chief among these is the role of corporate taxes in society: the taxes businesses pay and collect on behalf of governments not only finance essential public services but also support the transition to a more sustainable future. Additionally, stakeholders are increasingly demanding greater transparency regarding a company tax affairs, enabling a more educated assessment on company’s governance and reputational risks.

Under the Corporate Sustainability Reporting Directive (CSRD), companies are required to report using the European Sustainability Reporting Standards (ESRS). However, in the absence of a specific ESRS for tax, companies can turn to the Global Reporting Initiative (GRI), specifically GRI 207, for guidance. GRI 207 covers a range of areas, including the organization’s approach to tax, governance, control and risk management, stakeholder engagement on tax-related matters, and country-by-country reporting.

Even if tax is not deemed material under CSRD, tax departments should maintain close collaboration with sustainability teams to support informed decision-making. This alignment is especially critical given the forthcoming EU requirements to publicly disclose tax data for both EU and non-EU entities starting in 2026 for the 2025 tax year.

What is a materiality assessment?

The materiality assessment begins with the organization, in consultation with its (affected) stakeholders, identifying and assessing which topics are material for its operations along the value chain.

According to CSRD, a topic could be considered material from two viewpoints: impact materiality (the impact of the organization on the outside world), and financial materiality (the risk that the outside world has on the financial value of the organization or the opportunity it creates). A sustainability topic is material for CSRD disclosure purposes if it is material from either one or both perspectives. This concept is known as double materiality.

When a topic is considered material to an organization, CSRD requires the organization to report on the topic using the applicable ESRS. There are twelve sector-agnostic ESRSs, consisting of two cross-cutting standards, which apply to all sustainability matters, and ten topical standards encompassing various ESG dimensions. For instance, if biodiversity is identified as a material topic, the organization must use ESRS E4 to report on biodiversity impacts, risks, and opportunities.

For tax, however, there is currently no ESRS that can be relied upon. Nevertheless, this does not mean that tax cannot be a material topic. If tax is identified as a material topic, the ESRS allow companies to rely on GRI Standards for the reporting on the impacts a company has via its tax policies and behavior. This possibility was clarified in the EFRAG GRI Interoperability joint statement, where tax is explicitly mentioned as an example.

How does tax tie into sustainability and when should it be included in the materiality assessment?

When considering tax as a material topic, one might question its relevance to sustainability. However, the significance of tax in this context is substantial, given its multifaceted role. For example, tax plays a critical role in financing equitable societies and public goods, while also serving as a vital mechanism to influence behavior and promote sustainable development, ultimately also contributing to achieving the 2030 UN Sustainable Development Goals (SDGs) agenda. This stance is echoed by many international institutions and organizations, including the United Nations, the OECD, the World Economic Forum and GRI.

Some important (sub)topics in this regard are (inter)national sustainable tax policies (which include new taxes like carbon taxes), tax capacity building, responsible tax planning, prevention of tax avoidance, good tax governance (on an (inter)national and a corporate level), and corporate transparency on the approach to tax, in narrative and in data.

Under CSRD, in ESRS 2 and ESRS S3, tax is specifically mentioned as something that may have an impact on affected communities’ “[…] aggressive strategies to minimise taxation, particularly with respect to operations in developing countries […]”. Additionally, tax might also be viewed through the lens of business conduct, potentially triggering the use of ESRS G1 (Business Conduct). Similarly, the financial impact of environmental taxes might necessitate disclosure under the one of the ESRS environmental standards.

Assessing the materiality of tax

While the ESRS do not prescribe a specific methodology for tax, companies may, for instance, adopt a structured approach involving four key steps when conducting a materiality assessment aligned with ESRS implementation guidance (see EFRAG guidance). Each step is pertinent to evaluating whether tax qualifies as a material topic for that organization.

Step A

Understanding the context, including activities and business relationships, contextual information and understanding of affected stakeholders.

Step B

Identification of the actual and potential impacts, risks and opportunities related to sustainability matters.

Step C

Assessment and determination of the material impacts, risks and opportunities related to sustainability matters.

Step D

Reporting on the process and on the outcome (using ESRS, and for example GRI 207 for tax).

Factors to consider when assessing the materiality of tax

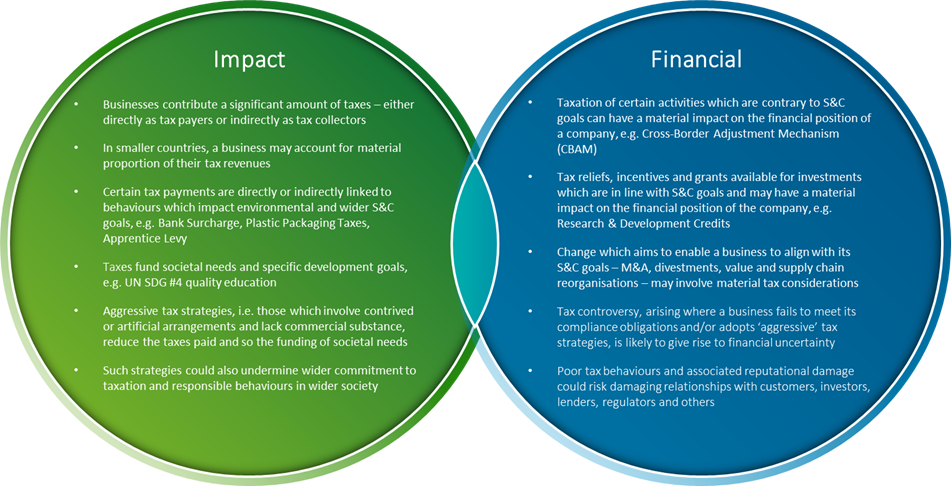

The figure below illustrates a number of considerations that we believe are pertinent, either individually or collectively, when assessing tax as a material topic from a sustainability perspective. We differentiate between considerations affecting impact materiality and those affecting financial materiality, noting potential areas of overlap.

When considering the above points, it is important to bear in mind the following:

1. The materiality assessment extends across the organization’s entire value chain, both upstream and downstream, as well as its own operations.

2. Stakeholder engagement often plays a crucial role in shaping the materiality assessment. This involves actively seeking input from stakeholders to understand concerns and provide evidence regarding a company’s tax impacts on society and the environment. Notably, for tax this requires careful consideration as historically tax stakeholder engagement has been limited to the tax authorities, CFO and tax advisors – in this instance it needs to be broader and could for example include other governmental institutions and organizations focusing on tax implications (such as the OECD).

3. Establishing whether tax qualifies as a material topic necessitates considering both impact and financial factors. From an impact perspective, this includes assessing the scale, scope, and irreversibility of potential effects on society. Positive impacts are evaluated based on scale and scope, while potential negative impacts require consideration of likelihood alongside severity.

4. Financial materiality hinges on evaluating both the likelihood and potential financial magnitude of effects on the company to determine which risks and opportunities merit reporting, including those related to tax.

5. Drawing on existing materiality information, gleaned from prior sustainability reports and GRI materiality assessments, is important. Some companies have already identified tax as a material topic, describing it as integral to their sustainability strategies or emphasizing its importance for close monitoring. While these perspectives may not align precisely with the classification of 'material’, they should be weighed in the overall assessment of tax.

Considerations when tax is identified as a material topic

If tax is identified as a material topic, a company must include tax reporting in its CSRD sustainability statement and undergo external limited assurance as required by CSRD. As noted above, in the absence of a standard within ESRS specifically for tax, GRI 207 can be utilized for reporting. Two key considerations are:

1. Use of the GRI 207 Tax Standard is not mandatory under CSRD. However, ESRS makes reference to GRI Standards for topics not covered by the ESRS, emphasising the importance of comparability. Without standardized disclosures, stakeholder analysis becomes challenging and potentially more prone to greenwashing. Thus, reliance on GRI 207 can be beneficial due to its multi-stakeholder approach and existing acceptance among policymakers and investors.

When using GRI 207 alongside the mandatory EU public Country-by-Country Reporting (CbCR), the question of integration of the two arises. Although significant overlap exists, it is crucial to ensure alignment in the numbers disclosed.

2. GRI Standards, including GRI 207, focus on impact rather than financial materiality. Thus, GRI 207 is suitable for reporting on tax as an impact material topic. For financial material reporting on tax, other disclosures and metrics, aligned with ESRS implementation guidance for financial topics, should be employed.

Considerations when tax is not identified as a material topic

In cases where tax is not identified as a material topic, companies are not required to publicly report on tax under CSRD. However, materiality assessments are conducted periodically, meaning that the relevance of tax could shift over time. This necessitates ongoing monitoring, particularly if tax is nearing, but not yet surpassing, the materiality threshold.

Additionally, companies in scope of CSRD will likely be subject to the EU Taxonomy Regulation, which considers tax a minimum safeguard through the OECD Guidelines for Multinational Enterprises on Responsible Business Conduct. GRI 207 is also relevant in this context. While companies should investigate this separately, it remains a crucial consideration for financial and sustainability reporting. For a more detailed exploration of how tax integrates into EU sustainability regulations, please see our blog, “Exploring the Integration of Tax in EU Sustainability Regulations”.

Voluntary tax transparency reporting

Voluntary tax transparency reporting offers companies the opportunity to take a lead on disclosures even when tax is not formally classified as a material topic. Companies can choose GRI 207 or the WEF Stakeholder Capitalism Metrics – or a blend of both—to harmonize their tax disclosures.

Voluntary reporting is increasingly being adopted by companies globally, driven by a desire to demonstrate responsible tax practices through both narrative and quantitative data. Such transparency not only aligns with sustainable business strategies but also resonates with societal expectations.

By opting for voluntary disclosure, companies can build community trust, reinforce their social "license to operate," and ensure accountability across the corporate landscape. This transparency also extends to governments, providing clarity on how tax revenues are being deployed to support the transition to a more sustainable future, ensuring that every note in the corporate symphony contributes to the larger goal of sustainability.

This is an updated version of a previous blog, which was originally published here.

Key contributor:

Atila Demiraj – Manager, Financial Services Tax – Deloitte Switzerland