IFRS 9 | 2Q24 results update: the outlook continues to improve and regulators have been busy!

As an update to our last IFRS 9 results blog on the 4Q23 results, this post gives a 2Q24 update on the loss reserving trends and outlook for UK banks.

The overall view for the first half 2024 is very similar to the second half of 2023: a continued improvement in the economic outlook and a consequent small reduction in cost of risk and ECL cover. The proportion of ECL attributable to Post Model Adjustments also continued to decrease slightly. Credit performance stayed strong and the signs of stress in mortgage portfolios seemed to start to improve.

It seems as if we may be past the point of maximum peril from the big shocks we’ve seen to the economy over the past couple of years. As more time passes, and as the economy continues to outperform expectations, it looks less likely that a wave of defaults will emerge. Rather than a potentially widespread credit event the risks now seem to be pointing to specific credit risk “hot spots”. In their 2023-24 Written Auditor Reporting Thematic Feedback the PRA also strike a cautious note on “…the possibility of delayed default emergence and the longer-term refinance risk for fixed term loans as businesses and households adjust to higher debt payments.”

Even though it was a quiet period from a credit risk and reserving point of view regulators have been busy issuing guidance with the ECB publishing fresh direction over the use and governance of overlays, while the IASB published the second phase of their IFRS 9 Post-Implementation Review.

The loan loss reserving conundrum in 2H24 is that, absent another shock, stable credit performance and improving economic outlook are likely to lead to model output reducing while, simultaneously, the extent and severity of novel risks driving PMAs are also reducing. With ECL cover now dipping below 2019-levels this presents a challenge for lenders who are cautious about further releases given the potentially fragile state of the economy and heightened geopolitical risks.

1) ECL key metrics showed slight improvements in the second quarter

The cost of risk, ECL cover and the proportion of loans in Stage 2 all showed a small improvement. In the second quarter of 2024 (see Figures 1 and 2 below).

Figure 1: ECL cost of risk (annualised P&L charge / loans and advances)

Figure 2: ECL cover (ECL / Loans and advances)

2) This improving trend was largely due to improvements in the economic outlook.

The big improvements seen in the first half of 2024 were more positive expectations for the UK housing market (with house prices now expected to rise in the base case by most lenders) and general economic growth. There was some small improvement in unemployment expectations and bank rate outlook stayed broadly flat.

Figure 3: Change in UK economic base case 4Q22 -> 1Q24 (min, max, mean)

The improving outlook for the UK housing market was driven by growing confidence (e.g. CFO Survey | Deloitte UK and gfk Consumer Confidence) and lower mortgage rates. The chart below shows the link between mortgage applications and mortgage rates.

Figure 4: mortgage applications and 2y 75% LTV mortgage rate

3) And there was also some contribution from decreases in Post-Model Adjustments

Post Model Adjustments are typically used to include “novel” risks in ECL that are difficult or impossible to model. They’ve been a critical part of the ECL toolkit over the past five years, accounting for up to c.40% of ECL losses during the peak of the Covid crisis. As the economic outlook has improved, and portfolio performance has remained strong, lenders have gradually reduced the proportion of ECL accounted for by Post Model Adjustments. Indeed, 1H24 saw a wind-down by some lenders of adjustments relating to inflation, “cost of living” and sector-specific risks.

Figure 5: Post Model Adjustments as a % of total ECL (average and

range)

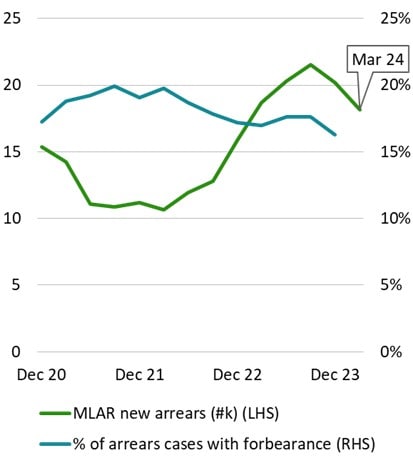

4) Credit quality stayed strong and new mortgage arrears reduced.

Stage 3 stayed flat at Group-level for our sample of banks (see Figure 6 below). At UK-level there was an (expected) small increase in mortgages Stage 3, a small decrease in consumer lending Stage 3 and commercial lending stayed broadly flat on YE23 (see Figure 7 below). The inflow of new mortgage arrears continued to abate and there was no sign of an increase in forbearance (see Figure 8 below).

This picture seems to contrast with the EU where the Joint Committee of the European Supervisory Authorities recently commented on deteriorating asset quality for banks in the EU with the share of Non-Performing Loans (NPLs) increasing slightly in 1Q24 by 10bp to 1.9%. They commented that the increase was broad-based across lending segments but that the biggest increase was for SMEs.

Figure 6: Group: Stage 3 as a % of loans and advances

Figure 7: UK portfolios: Stage 3 % of loans and advances

Figure 8: MLAR % of mortgages >1.5% in arrears inc. repossessions

With regard to “hot spots”, we note that the Bank of England called out the following areas of concern in the June 2024 Financial Stability Report:

1. Pressures associated with continued higher interest rates and living costs continue and will be concentrated in a subset of households. Savings buffers for renters and low-income households have been further eroded, with the share of renters who have fallen behind on payments has also increased slightly.

2. There also remain pockets of vulnerability in areas such as corporate debt. This includes the debt of certain highly leveraged businesses, private equity-backed businesses (see Section 6 of the Financial Stability Report), and small and medium-sized enterprises.

3. Headwinds continue to impact the UK CRE market, making refinancing challenging, in part as a result of lower collateral values. Office and Retail CRE have both been particularly impacted. Nevertheless, the report also notes that, although UK CRE prices have fallen over 20% from their 2022 peaks, the pace of decline has since slowed.

4. Risk management practices in some parts of the [private equity] sector were also highlighted as requiring improvement, including among lenders to the sector such as banks.

We also note from our conversations with clients, as well as in the September release from the Bank of England’s Financial Policy Committee (FPC) some concern over parts of the wholesale and retail trade, utilities, construction, accommodation and food service sectors. Experian also commented in September that the agriculture, forestry & fishing and transportation & storage sectors also showed signs of deteriorating delinquency rates, indicating potential difficulties ahead, which banks will need to carefully manage.

5) Although the credit and reserving environment has been benign, banking regulators have still been busy issuing thematic guidance on IFRS 9.

There have been a range of updates from global, regional and national regulators and supervisory bodies this year, a selection of which are summarised below.

ECB: Post Model Adjustments

The ECB have published extensively over recent years on the use and control of overlays in ECL. They published a blog in May 2023 on the topic, as well as commenting in their 2023 IFRS 9 monitoring report. They also published a specific piece on IFRS 9 overlays and model improvements for novel risks in July 2024, citing a range of good practices that align well with those we see in the UK market, notwithstanding some areas of difference.

The ECB recognises the importance of overlays in accounting for “emerging risks” and “novel risks” (i.e. those that can’t be easily modelled) in ECL. Their concerns focus around inadequate identification of those risks, poor quality of quantification/lack of risk sensitivity (especially via “umbrella overlays” at total ECL-level), inadequate transparency and governance, inadequate consideration of SICR, and variation in the use of overlays across banks.

They also comment on the transmutation of overlays addressing risks in the pandemic into geopolitical risk and inflation/supply chain risk overlays, noting that “roughly a quarter of the loan loss coverage in banks’ performing loan books is due to overlays, and there is no visible downward trend.” This contrasts with the UK position where overlays have decreased alongside uncertainty and improvements in the economic outlook.

The ECB also observed that IFRS 9 overlays significantly correlated with pre-provisioning income, indicating that they are used for earnings management (but pure ECL model outcomes showed no correlation with pre-provisioning income) and that banks with poor practices showed lower coverage ratios, lower Stage 2 ratios and fewer Stage 2 transfers, all of which may lead to insufficient aggregate risk coverage and increased supervisory attention.

IASB: IFRS 9 Post-Implementation Review

In July the IASB published the outcomes of the second phase of their post-implementation review into IFRS 9 impairment.

As a reminder, the first phase of the review found that, while IFRS 9 generally worked well and in-line with intention, the IASB should consider additional guidance to help support consistency of application and requirements around credit risk disclosures under IFRS 7.

In the second phase the IASB concluded that:

- There are no fatal flaws regarding the clarity or suitability of the core objectives or principles in the impairment requirements.

- In general, the requirements can be applied consistently. However, further clarification and application guidance is needed in some areas to support greater consistency in application.

- The benefits to users of financial statements from the information arising from applying the impairment requirements in IFRS 9 are not significantly lower than was expected. However, targeted improvements to credit risk disclosures are needed to enhance the usefulness of information for users.

- The costs of applying the impairment requirements and auditing and enforcing their application are not significantly greater than was expected.

The two items called out for further action were a proposed future project on improvements to IFRS 7 credit risk disclosures and consideration of the intersection of the impairment requirements and the requirements for the modification, derecognition and write-off of financial assets in a separate amortised cost measurement project. Some aspects of applying IFRS 9 to financial guarantee contracts were classed as “low priority” and will be considered in the next agenda consultation.

6) Looking forward

In the UK context the labour market is strong (albeit becoming less tight), the economy is growing (a bit), affordability is improving through reductions in rates (with mortgage rates now falling below prior stress underwriting rates) and growth in real income, and confidence is returning to the housing market. Other than some worries about the potential content of the budget this picture seems to be reflected through both consumer and business confidence measures.

While the re-pricing of mortgage portfolios from ultra-low rates has further distance to run, given the wider economic picture, the resilience of households seen to date, and the positive trend for new-to-arrears data it seems that a credit spike in personal lending is increasingly unlikely. Interestingly unsecured lending is still growing strongly, reversing the massive consumer de-leveraging seen during 2020. In their 1Q24 Affordability Update, Experian comment that one in 20 adults in the UK opened a new credit card in 1Q24 and there was also an increase in BNPL activity. Importantly they also comment that they can see no evidence that this is “borrowing to survive” but rather reflective of the convenience of digital customer journeys. However, Experian data also points to small deterioration in credit scores, indebtedness and arrears commensurate with increased borrowing.

For commercial lending the BoE’s Credit Conditions Survey shows a benign credit outlook for all sizes of business. However, there is still some concern that as liquidity gathered over the Covid period runs off the longer term drag of inflation and borrowing cost increases could lead to some credit stress. On the upside, we note that in the British Business Bank Small Business Finance Markets 2023/24 report that c. 50% of businesses who use finance are on variable rates, with no significant credit stress seen to date. Meanwhile, Experian also reported “the percentage of businesses using overdraft facilities dropping marginally, along with rates of overdraft utilisation”. Government data from March 2024 shows that, of the £77bn that was drawn down under all COVID-related schemes, c. 68% of balances are now closed or repaid with a further 28% performing and only c.4% with credit issues (see Figure 9).

Figure 9: Covid-19 loan guarantee schemes performance at 1Q24

From expectations of a potentially widespread credit deterioration in 2022 and 2023, focus has turned instead to specific risk “hot spots”. Consequently, lenders should ensure they are monitoring performance of at-risk groups and considering reserving appropriately. In their 2023-24 Written Auditor Reporting Thematic Feedback the PRA also struck a cautious note on “…the possibility of delayed default emergence and the longer-term refinance risk for fixed term loans as businesses and households adjust to higher debt payments.”

The loan loss reserving conundrum in 2H24 is that, absent another shock, stable credit performance and improving economic outlook are likely to lead to model output reducing, while, simultaneously, the extent and severity of novel risks driving PMAs are also reducing. With ECL cover now dipping below 2019-levels this presents a challenge for lenders who are cautious about further releases given the potentially fragile state of the economy and heightened geopolitical risks.

Our main themes for the remainder of 2024 are:

- Risk “hot spots”: monitoring and consideration of risks arising from “hot spots” in loan loss reserving processes.

- SICR: while the industry has seen a gradual year-on-year improvement in practices relating to the setting and monitoring of SICR criteria this is still an area with significant variation. Firms need to make sure that they have robust quantitative frameworks in place for setting and then monitoring the efficacy of quantitative PD thresholds and that these decisions are put through appropriate governance.

- LGD calibrations: these have been a challenge over the last few years with a very low volume of defaults leading to a low volume of “close bads” to calibrate models. Price volatility in the auto and commercial and retail real estate sectors hasn’t helped either. However, data from 2019 and before, which some lenders are using to benchmark components of LGD, is moving further away in the rear-view mirror. Lenders should consider the appropriateness of their use of data in calibrating LGD and where judgement is being used in calibrations.

- Controls, governance and reporting of PMAs: while this remains a challenge at some lenders, we note that it is decreasing in importance as an issue given the decreasing contribution of PMAs to ECL.

We hope you found this quarterly assessment useful. You can find previous blogs in this series below. Alternatively, please don’t hesitate to contact one of our team who will be happy to discuss any of the topics covered here with you.

______________________________________

References

Figure 1,2, 3, 5, 6, 7: company reports, Deloitte analysis

Figure 4: Bank of England quoted rates and approvals for secured lending to individuals (seasonally adjusted)

Figure 8: FCA MLAR statistics

Figure 9: Department for Business & Trade COVID-19 loan guarantee schemes performance data