Risk Quantification for Investment Management Firms

End-to-end operational risk quantification support for FCA Investment Management Firms

The challenge

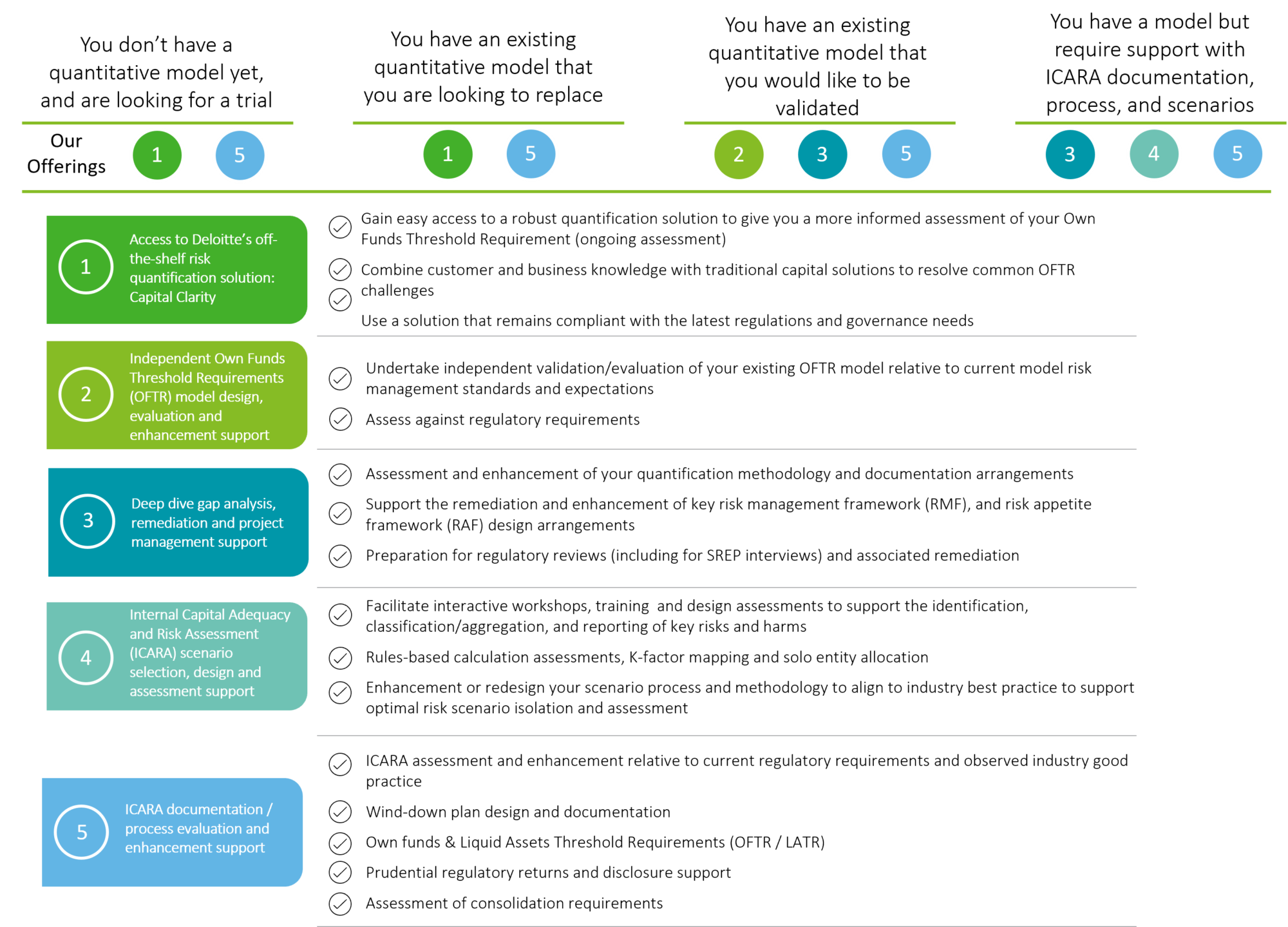

FCA investment firms continue to have the option to use statistical models to support their internal capital requirement assessments. Many have also found such models help them to understand better their risk profile, supporting both immediate changes to policy and processes and the prioritisation of longer-term investments (such as technological resilience). As firms continue to embed the Internal Capital Adequacy and Risk Assessment (ICARA) process, statistical models remain as relevant as ever before, however some adjustments will be required to align the assessment with the focus on mitigating harms (to clients, the market and to the firm) and to compare the model output to the individual K-factor requirements. We can support you across the ICARA process, from enhancing and validating your existing quantitative models to providing you with off-the-shelf quantification solutions if you don’t yet have a model or are looking to replace your existing one.

How it works

Opens in new window

{kind=link}

Insights

Opens in new window

Opens in new window