Credit Concentration Risk (COREX)

Understand what makes you unique and assess the additional risk on your portfolio’s differences from the market average

The Challenge

Organisations want to understand their concentration risk drivers for use in ICAAP, risk appetite and more but might not have access to automated analytics to support a complete and intuitive understanding of their portfolio.

This credit concentration risk solution allows organisations to analyse per region, sector and product concentrations. The model has been developed using a variance covariance-based approach, which focuses on the expected differences in loss volatility between a “fully diversified” reference portfolio and your organisation’s current portfolio.

Features

Pillar 2 capital add-on calculation

24/7 direct model access

Region, Sector and Product Concentration analysis

Sensitivity analysis

Visuals and graphing to support intuitive understanding

Audit trail of model runs

Opens in new window

How it works

-

Input risk profile

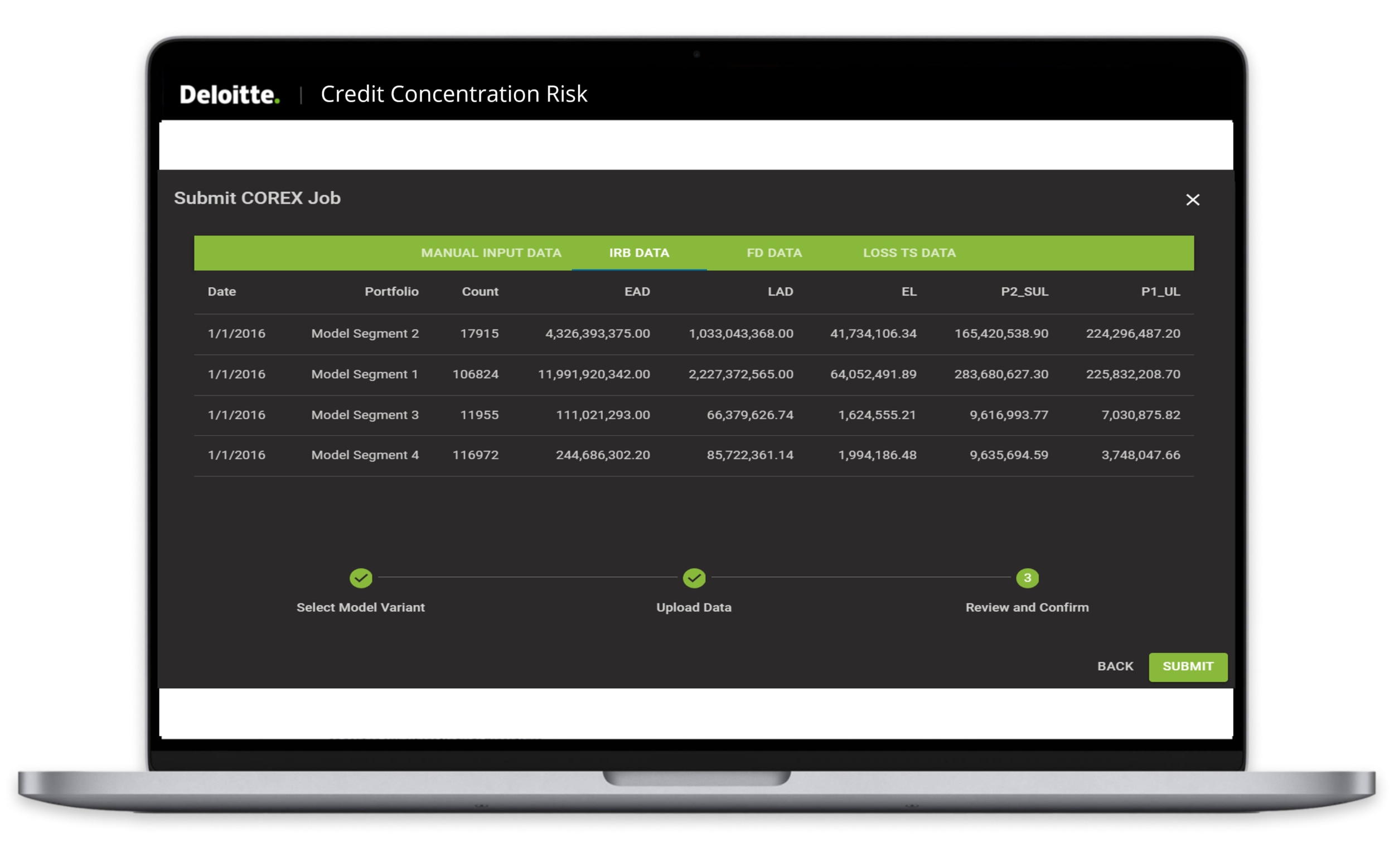

To run the CC-CREX model, users easily upload their portfolio data (Exposure at Default (EAD), Loss Given Default (LGD) and Probability of Default (PD)) and default history or asset correlation inputs, utilising the pre-defined templates. The user also has the ability to take full control of their model run; setting the confidence level, the number of simulation to run and maximum amount of time allowed for the simulation attempt.

Input risk profile

To run the CC-CREX model, users easily upload their portfolio data (Exposure at Default (EAD), Loss Given Default (LGD) and Probability of Default (PD)) and default history or asset correlation inputs, utilising the pre-defined templates. The user also has the ability to take full control of their model run; setting the confidence level, the number of simulation to run and maximum amount of time allowed for the simulation attempt.

-

Run the model

Utilising the loss correlations and the PD, LGD and EAD inputs; Portfolio Standard Deviation (PSD) is calculated and the contribution of each portfolio to it for both the Current and Fully Diversified reference portfolios.

Run the model

Utilising the loss correlations and the PD, LGD and EAD inputs; Portfolio Standard Deviation (PSD) is calculated and the contribution of each portfolio to it for both the Current and Fully Diversified reference portfolios.

-

Analyse results

The model outputs the summary results for the user to analyse and compare their portfolio against the industry average. As well as, the Pillar 2 Credit Concentration Risk Capital add-on as a capital scaler linked to the add-on in loss volatility between the Current and Fully Diversified reference portfolios.

Analyse results

The model outputs the summary results for the user to analyse and compare their portfolio against the industry average. As well as, the Pillar 2 Credit Concentration Risk Capital add-on as a capital scaler linked to the add-on in loss volatility between the Current and Fully Diversified reference portfolios.

-

Allocate results

Once the model has run and additional analysis has been completed i.e automated sensitivity testing, results can also be allocated to the most granular concentration segments, including by product, region, and sector. This can also support other business uses such as risk appetite, limit setting, risk-adjusted return metrics, pricing (including single-name risk pricing) and more.

Allocate results

Once the model has run and additional analysis has been completed i.e automated sensitivity testing, results can also be allocated to the most granular concentration segments, including by product, region, and sector. This can also support other business uses such as risk appetite, limit setting, risk-adjusted return metrics, pricing (including single-name risk pricing) and more.

Opens in new window

Opens in new window

Opens in new window