Building Trust in a Digital Age: Essential Elements of a Digital Asset Policy

Staying Ahead of the Curve in a Transformative Era

This paper is a practical guide for financial institutions developing a digital asset policy. As cryptocurrencies and blockchain technology reshape finance, this framework helps institutions navigate the particular opportunities and risks of digital assets. The paper discusses defining scope, managing risk, establishing governance, and ensuring regulatory compliance, offering insights for confident engagement with this evolving landscape.

The need for a digital asset policy

The rise of digital assets, powered by Distributed Ledger Technology (DLT), is reshaping the financial landscape, presenting both unprecedented opportunities and complex challenges for traditional financial institutions. This paper seeks to outline essential considerations for traditional financial services firms when developing their digital assets policy amid a constantly evolving landscape of Distributed Ledger Technology (DLT) and its transformative impact on digital assets. DLT, in particular blockchain, has ushered in a new era of decentralized and secure methods for creating, managing, and exchanging digital assets. These assets, encompassing a broad spectrum from tokenized traditional assets to cryptocurrencies and stablecoins, present diverse opportunities, and risks. While DLT can streamline processes such as settlement and clearing, leading to increased efficiency and cost reduction, regulatory frameworks are still evolving to keep pace with this innovation. Furthermore, varying approaches to classification, oversight and investor protection are emerging across jurisdictions which further creates the need for a group-wide policy or standard. In this dynamic environment, both traditional financial institutions and crypto-native firms are adapting to these new models, with the former increasingly integrating digital asset products and services. This policy serves as a strategic guide for firms to navigate the complexities of this evolving ecosystem, ensuring compliance, risk management and market competitiveness. The aim of this paper is to give both traditional financial firms and crypto-natives a baseline structure to what a digital asset policy could look like at a firm who is either exploring digital assets for the first time or is a seasoned player in the market. We have included the more theoretical components of a successful digital assets policy from our market experience alongside highlighting some challenges and choices firms have faced when looking to implement the relevant component of the policy. This paper serves as a springboard for firms to initiate informed discussions and tailor their digital asset policies to their specific risk appetite, business objectives, and regulatory environment.

Key components of a digital assets policy

The sections below highlight the key areas that firms may decide to include in their digital assets policy. Each section outlines the type of content that would be expected to be covered in sub-sections of the policy.

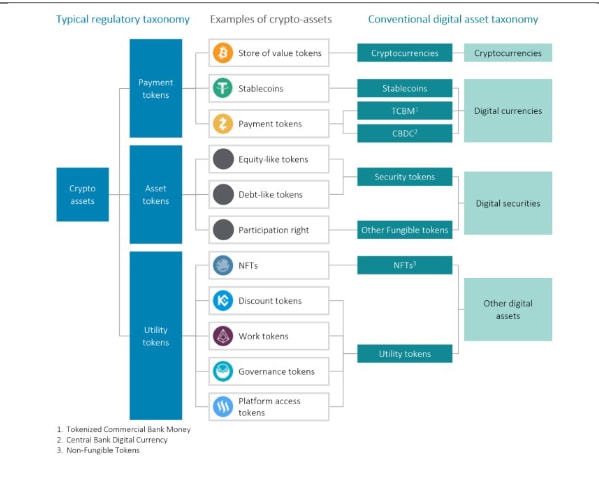

Firms should clearly outline how they define the term ‘digital assets’ for their business and where this definition has been derived from (i.e., from industry standards or regulation). It may be relevant for the firm to expand on their digital assets strategy in relation to this policy. This will include more detail on the types of digital assets and technology being used: Examples of this are:

- Digitally native assets issued using DLT (e.g., tokens)

- Traditional finance products or services that are being tokenised (e.g., tokenised bonds)

- Derivative or exchange traded products referencing cryptocurrencies (e.g., Bitcoin ETFs)

Conclusion

Building a Foundation for Responsible Innovation

In the rapidly evolving world of digital assets, establishing an internal view is paramount. This paper seeks to give both established traditional financial firms and newer crypto-native firms the broad outline of what a digital asset policy could look like within a firm. It should allow those looking to initiate digital assets projects within their firms or those looking to revamp their governance structure to incorporate digital assets as a starting point for these discussions.

Whilst not all areas will be directly applicable to all firms, the concepts and underlying themes should resonate with all firms either entering the digital assets space or looking to expand their existing offerings. This document seeks to support in firms in ensuring compliance at a policy level and provide stakeholders within the firm to have a central view of the firm’s stance on digital assets and the use of DLT.

With the continued focus from global regulators, as well as major publications of new rules and requirements such as the EU’s Markets in Crypto asset Regulation, the importance of being able to prove to regulators and supervisors the ability to understand, quantify and control for the unique risks posed by digital assets has never been more in focus. By embracing a proactive and comprehensive approach to digital asset policy, firms can position themselves at the forefront of this transformative era in finance.