Navigating the transition: exploring the T+1 settlement implications

Context

In February 2023, the US Securities and Exchange Commission (SEC) announced the requirements for shortening the settlement cycle from two business days after trade date (T+2) to one business day after trade date (T+1). The 28 May 2024 implementation date affects transactions in US cash equities, corporate debt, and unit investment trusts.

These requirements aim to benefit investors by mitigating credit, market, and liquidity risks associated with unsettled securities transactions. However, it will inevitably bring challenges for market players due to the reduced time for executing all post-trade processes in a T+1 environment, coupled with the time zone differences between the US, Europe and Asia.

Canada and Mexico are also shortening their settlement cycle, with some Latin American countries to follow. While in the EU, discussions between the European Commission, the European Securities and Markets Authority (ESMA), the European Fund and Asset Management Association (EFAMA) and the Association for Financial Markets in Europe (AFME) are assessing the benefits and feasibility of moving the European markets to a T+1 settlement cycle. However, no official announcement has been made on this end.

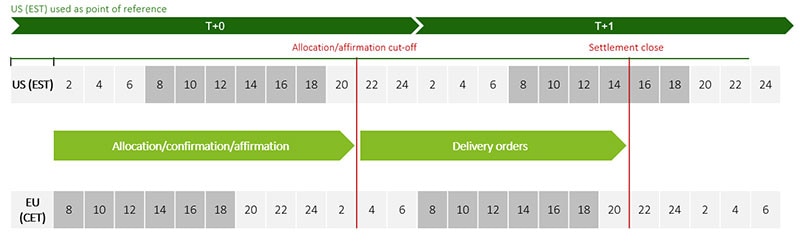

Impacts of US, Canada and Mexico T+1 settlement on Europe

The challenges of adhering to T+1 across US and European markets become apparent when the time zone differences are laid out:

Click here to enlarge the image

{kind=link}

European financial institutions are being compelled to adjust their operational and technological infrastructures to accommodate this accelerated settlement pace, requiring strategic adjustments and targeted investments. The challenges vary across organizations.

The impacts for the asset management industry are mainly the heightened liquidity risk and the increased costs associated with trading, funding, repapering and other related expenses. A notable change is the significantly shortened affirmation deadline, moving from 11:30 am EST on T+1 to 9:00 pm EST on T. This requires operational responses, prompting asset managers and brokers to consider automated affirmation tools like DTCC CTM or M2i deliver pre-matched information to custodians. The accelerated T+1 settlement cycle increases the risk of liquidity mismatches, demanding more accurate cash projections and handling of investment limits. To address these new operational demands, systems might require significant upgrades or complete modernization, ensuring a robust technological infrastructure capable of handling increased transaction volumes with speed and accuracy.

The expedited T+1 settlement cycle is often perceived as a “provider issue”, compelling asset servicers to further increase their STP rates.

For custodian banks, effective communication with their clients about the settlement cycle changes and their impact is key. Under the T+1 settlement cycle, the custodian bank must receive trades from trading entities in time to perform the affirmation process and resend it to DTCC by 9 p.m. EST on T. Custodian banks missing this deadline must issue Night Deliver Orders or Day Deliver Orders, incurring additional costs.

As such, custodian banks should actively pursue straight-through processing to attain end-to-end automation in the settlement process. Additionally, they must educate their clients about the importance of timely trade affirmation, ideally encouraging them to perform self-affirmation. It is also essential to determine who will cover late trade costs if a trade is not affirmed or settled in time.

Moreover, the accelerated settlement cycle also increases pressure on liquidity management and seamless transaction settlement. Efficient fund management, better cash forecast and asset allocation will be paramount.

(When) Can we expect a T+1 settlement in Europe?

Despite the competitive advantage, the market is unsure when the EU will follow suit in transitioning to a T+1 settlement, as the associated challenges have not been effectively addressed.

Shortening the securities settlement cycle requires heightened operational efficiency from market participants. This involves reviewing post-trade processes, potentially eliminating manual interventions, and reassessing funding practices, especially for FX transactions. The EU's post-trade landscape is an intricate web of various market players, such as central securities depositories (CSDs), central counterparty clearing houses (CCPs), and trading venues. The diversity of currencies compounds this complexity, presenting an additional challenge in streamlining operations to shorten the settlement cycle.

In alignment with ESMA's perspective, any decision to compress the EU settlement cycle should be based on a comprehensive cost-benefit analysis. This must also evaluate the EU markets’ competitiveness and incorporate insights from other jurisdictions that have already shortened their settlement cycles.

ESMA is evaluating the responses from their Call for Evidence (CfE) and intends to submit a final report to the European Parliament and to the Council by January 2025.

How can Deloitte help?

We have extensive experience with the impacts of the accelerated settlement cycle and supporting clients with their implementation journeys. Deloitte has the know-how and the tools to ensure the required activities are implemented on schedule and with the buy-in of the relevant stakeholders.

We are here to help you:

- Conduct a thorough impact assessment of your business, identify gaps and develop tailored mitigation strategies to optimize your operational processes;

- Outline possible future scenarios, particularly impacting liquidity and risk management, to bolster your organization's readiness for the "go live" stage; and

- Provide dedicated implementation support to facilitate a seamless transition for your organization.

To learn more, check out our T+1 Securities Settlement Industry Implementation Playbook for a detailed implementation schedule, interim milestones and identified dependencies, or get in touch.