Rental crisis

Today’s RBA cash rate decision to pause, the first after ten consecutive rises from May 2022, finally offers some reprieve from interest rate rises – for now. While mortgage holders are some of the most impacted by these rises, renters have also seen conditions worsen over recent months, with rental prices rising and availability of properties falling.

The rental market has tightened from both demand and supply factors. Demand is rising as population growth returns with force, driven by the return of international students and skilled/family migrants. Yet, a lack of supply of rental properties is also part of the problem. Rental vacancy rates are at record lows, which might normally prompt additional home building. However, new dwelling commencements are falling, given high interest rates and low confidence.

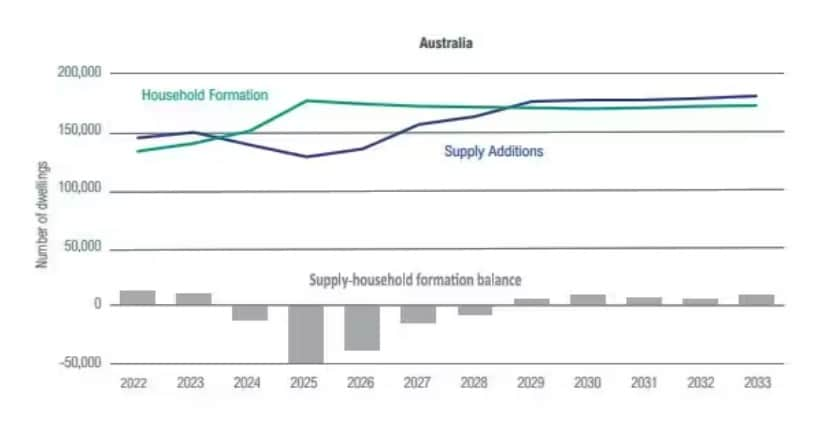

This week, the National Housing, Finance and Investment Corporation (NHFIC) released its flagship report State of the Nation’s Housing 2022-23 with startling findings about housing supply. Its modelling suggests the number of new dwellings (net of demolitions) will fall from 148,500 in 2022-23 to 127,500 in 2024-25, before recovering from 2025-26. But – slowing supply and increasing demand via falling household sizes is expected to create a supply gap of 106,400 dwellings to 2027 and a gap of 79,300 dwellings to 2033.

Chart: Annual change in supply-household formation balance

Source: NHFIC

Right now, Australia’s rental vacancy rate remains at an all-time low in February 2023 (0.8%) according to Domain. Vacancy rates fell to record levels in Sydney (0.9%), Melbourne (0.8%), Brisbane (0.6%), Darwin (1.2%), while Perth and Adelaide hover at just 0.3%. Capital cities have felt the return of international students more keenly, with many flowing into inner city areas and university precincts. Regional areas are also grappling with higher populations migrating from cities, many of whom have remained post-pandemic.

One contributor to low vacancy rates has been the pandemic. The pandemic saw the average household size declining to its lowest level in at least 25 years, contributing to around 120,000 additional households being formed and subsequent additional demand.

That means that one short-term solution is the reversal – a return to larger households. Spare rooms and granny flats may become hot commodities, and a way to spread rising rental costs across more people.

With demand rising and supply stalling, rental prices have risen quickly. CPI measured rents have risen by 4% over 2022, the strongest rise in 10 years, and have inched up to 4.8% in the February monthly CPI indicator. And it won’t stop there: advertised rents, which measure rents on those properties changing hands (rather than on all rental properties), are up by 18.1% in the year to March 2023 for units, and up 9.4% for houses. As more properties change hands and leases come up for renewal, average rental prices will also shift up further.

Chart 2: CPI rents vs advertised rents (June 2019 = 100)

Source: RBA.

As a result, renter stress and affordability are worsening. Even if renters are not feeling the direct impact of interest rate rises on mortgages, a rise in rent (and other household costs) is just as impactful – particularly as renter households are generally younger, have lower incomes and less wealth than owner-occupiers. NHFIC’s conservative estimates suggest 377,600 households are currently in housing need: 311,100 households are in rental stress while 46,500 households are experiencing homelessness. The RBA echoes this, finding that renter stress has picked up over the past year, with rent consistently being one of the two most reported concerns in the National Debt Helpline website.

So, what now? Unfortunately, it’s likely to get worse before it gets better. There are long lags from new housing commencements to having additional housing available – and for now new commencements are still moving in the wrong direction.

This blog was co-authored by Michelle Shi, an Analyst in the Deloitte Access Economics team.