WA Index

Issue 238 | September 2025

Welcome to the 238th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

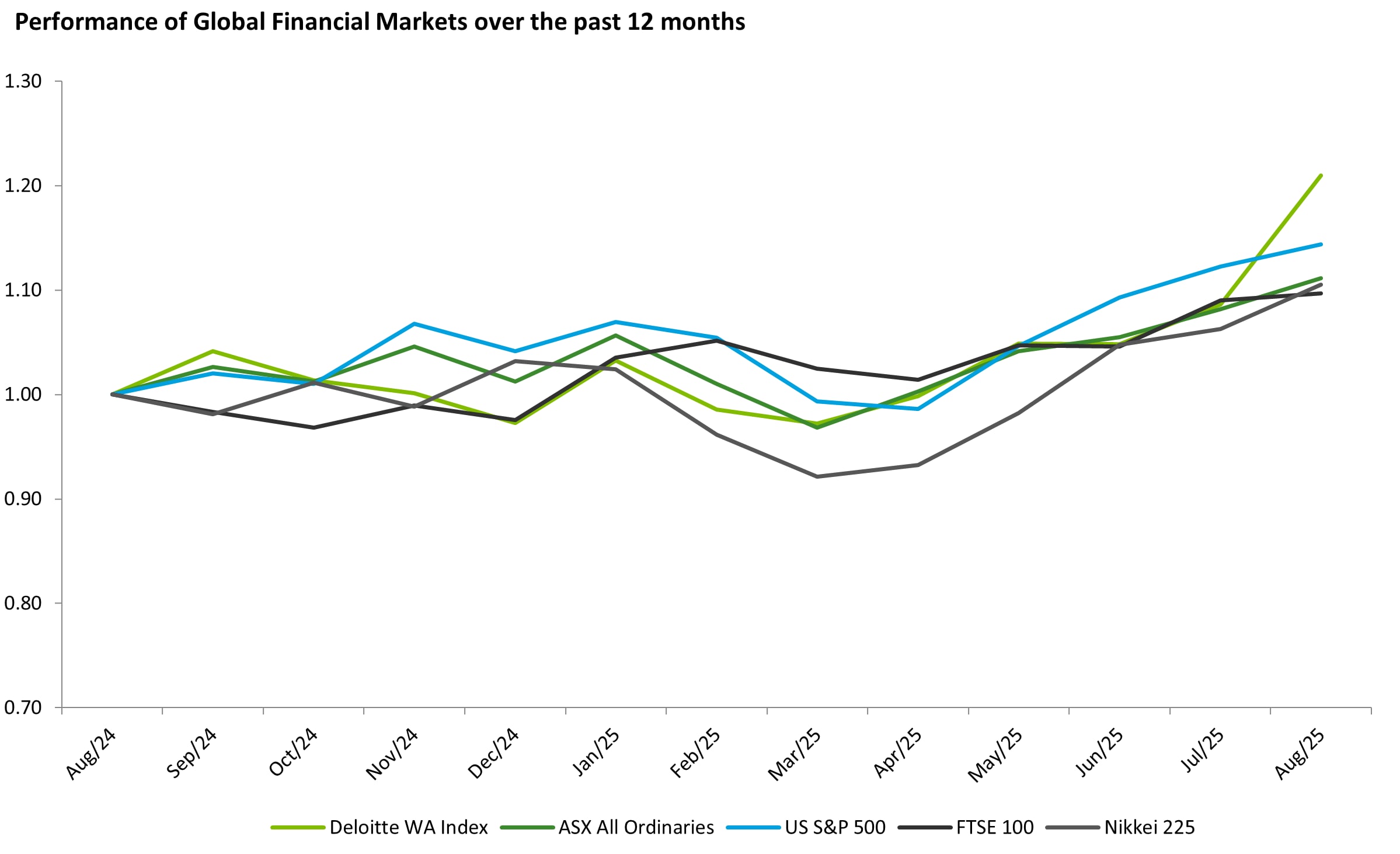

In September 2025, global equities were mixed: the S&P 500 rose 3.5% on a mid-month Fed cut and lower yields, and Japan’s Nikkei outperformed (+5.2%) on a weaker yen and buybacks, while the FTSE 100 gained 1.8% and Australia’s All Ordinaries slipped 1.2%.

Gold has continued climbing, extending its record highs once again in September a trend continuing at the time of writing this. Of the six companies specifically mentioned in this edition, five are gold focussed.

Meanwhile, silver and platinum rallied, copper firmed on supply disruptions, and iron ore was flat. The combination of falling yields and safe-haven flows powered precious metals and related equities, even as energy and bulks weighed on broader Australian market performance.

Download the list of WA’s top 100 listed companies, as of 30 September 2025, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold led commodities in September 2025, surging to successive all-time highs and finishing the month near US$3,800/oz. The rally was driven by lower real yields after the US Fed’s 25 bp cut on 17 September, a softer USD, and ongoing central-bank buying, with safe-haven demand elevated into October. Silver outperformed on a percentage basis, jumping toward US$46–47/oz, helped by the precious-metals bid plus tight fundamentals and industrial demand. Platinum also posted a strong double-digit gain, while palladium firmed but lagged silver and platinum.

Among other major movers, copper ended September higher, closing near US$10,300/t after supply disruptions late in the month and falling inventories offset mixed macro data. In energy, oil retreated: Brent slipped a few percent to the mid-US$60s/bbl as OPEC+ supply increases, inventory builds, and demand worries weighed on prices. Iron ore was flat to slightly softer in the low US$100s/t amid China property softness, while lithium prices remained weak on the rollercoaster of oversupply signals. Overall, the month was characterised by strong flows into precious metals and a softer tone across parts of energy and bulks.

Performance of WA Index and Global indices

Top 20 performers of the month:

Greatland Resources Limited (ASX:GGP): Greatland Resources’ market capitalisation appreciated significantly, with a key catalyst being S&P Dow Jones Indices’ September quarterly rebalance, which saw GGP added not only to the All Ordinaries but also to the S&P/ASX 200 effective 22 September 2025, driving higher visibility and ETF fund flows. Active engagement with investors, including Diggers and Dealers in Kalgoorlie and the Mining Forum Americas Conference in Denver (“Denver Gold Forum”), highlighted Greatland’s transformation into a leading Australian gold–copper producer following its ASX listing in June 2025 and the earlier acquisition of the Telfer mine and consolidation of the Havieron project in mid FY25. This all helped to underpin the September re-rating for the index inclusions.

Regis Resources Limited (ASX:RRL): Regis Resources’ substantial lift in market capitalisation in September reflected robust investor confidence, aided by its corporate overview at the Denver Gold Forum, which helped disseminate positive developments to a wider audience. The sector tailwind was powerful, with the gold price hitting fresh record highs during the month, further supporting RRL’s share price. Additionally, the September S&P/ASX indices rebalance amplified passive and benchmarked fund flows into Australian gold names, similar to Greatland.

Genesis Minerals Limited (ASX:GMD): Genesis Minerals’ market capitalisation rose meaningfully in September, underpinned by strong drilling results from Laverton and Leonora that supported organic growth and prompted a substantial lift in the exploration budget. Investor confidence was further bolstered by S&P Dow Jones Indices’ September quarterly rebalance, which saw GMD added not only to the All Ordinaries but also to the S&P/ASX 100 effective 22 September 2025, increasing visibility and likely passive fund flows. Adding to the momentum, the company received approval for Stage One mining at Tower Hill. These developments, together with record gold prices during the month and supportive post FY25 broker and media coverage, combined to highlight exploration success, an enhanced market profile and advancing project milestones.

The Top 100 performers of this month were:

St George Mining Limited (ASX:SGQ): St George Mining’s September surge was driven by a series of developments at its Araxá niobium and rare earths project in Brazil. Assays from the resource drilling program confirmed thick, high-grade REE and niobium mineralisation from surface, and the company reported a major new high-grade REE and niobium discovery roughly 1 km east of the existing Araxá mineral resource estimate, with broad, high-grade intervals. These results were amplified by the mid-September announcement of a strategic downstream alliance with US-based REAlloys, a government-linked magnet materials supplier that includes metallurgical collaboration and an offtake pathway for up to 40% of Araxá’s future rare earths production, positioning SGQ within an emerging US-focused supply chain.

Focus Minerals Limited (ASX:FML): With no company-specific news during the month, Focus Minerals benefited from powerful sector tailwinds and broader buying of ASX gold names. Gold prices pushed to fresh multi-decade highs through late September on falling yields, rising expectations of Fed rate cuts, and continued central-bank demand, drawing both specialist and generalist investors into the sector.

Minerals 260 Limited (ASX:MI6): Minerals 260’s market capitalisation lifted in September following an update from the Bullabulling Gold Project, where new high-grade intercepts and targets prompted an increase in the drill program from 80,000m to 110,000m. Notable assays included 10.2m at 18.5g/t Au (including 2.8m at 63.7g/t Au and 0.2m at 629g/t Au) and 19m at 4.7g/t Au (including 1m at 75.4g/t Au), from the Bacchus and Phoenix areas, underscoring high-grade gold mineralisation within the existing mineral resource. These results continued to support the potential to expand the current 2.3Moz Mineral Resource Estimate and to optimise early-years grade. The positive share price response was further supported by a favourable external backdrop, with gold prices pushing towards record highs through late September.

Featured articles