WA Index

Issue 239 | October 2025

Welcome to the 239th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

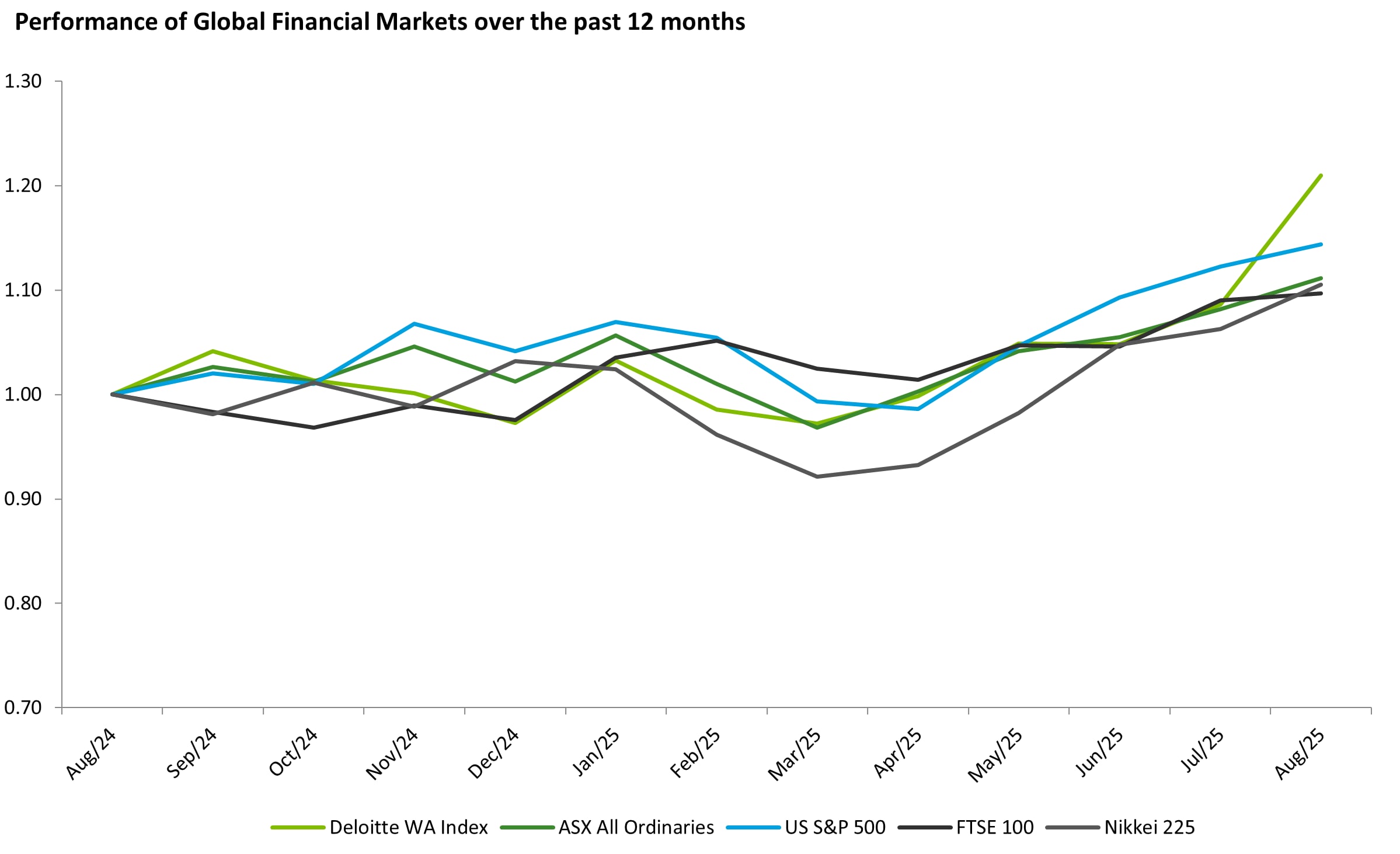

October 2025 was a positive month for global equities, led by Japan's Nikkei, which gained 16.6% for the month to a record high, its largest gain in three decades, and was supported by tech growth and favourable exchange-rate movements that boosted export competitiveness. The S&P 500 grew 2.3% after another Fed rate cut, which lowered yields, while the FTSE 100 rose 3.9%, supported by higher oil prices and positive earnings from several blue-chip stocks.

Commodities were mixed: gold extended its strong positive momentum into early October, reaching a new record high before a late-month pullback that left it with only a modest monthly gain. Cobalt, somewhat forgotten over the last fee years, surged on news the Democratic Republic of Congo introduced a new export quota.

Download the list of WA’s top 100 listed companies, as of 31 October 2025, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold prices continued into record territory in October 2025, climbing to a peak of $4,300 per ounce as expectations for FederalReserve rate cuts persisted, amid ongoing geopolitical tensions and renewed speculation around gold-backed currencies. The rise retreated in late October, as prices underwent what many viewed as a necessary correction after hitting all-time highs. Whilst retail customers continued their accumulation of physical gold, the hopeful de-escalation of some political tensions triggered the pull back. Silver followed in pursuit of gold, with prices rising throughout the month.

October 2025 saw LNG prices declining amid rising output and cooling demand across Asian manufacturing. Softer activity across Asia reduced regional LNG consumption, while global production rose 9% year-on-year in October, exerting downward pressure on prices. Europe, however, stepped up imports to capitalise on lower prices and rebuild winter stockpiles, which helped tamper the price decline.

Cobalt surged during October, after the Democratic Republic of Congo, the largest producer of cobalt, lifted its export ban and introduced export quotas, with a maximum volume of 96,600 tonnes of cobalt to be authorised for export.

Copper prices slipped to around US$5/lbs, down from the three-month peak of US$5.17, as a stronger US dollar and weak demand outweighed concerns about tightening supply. Minor production setbacks including operations at Freeport-McMoRan mine inIndonesia, accounting for over 3% of global supply, being halted following a deadly mudslide, supply pressures hold the price steady.

Lithium Carbonate prices advanced to CNY80,000 per tonne, the strongest level in two months, driven by optimism over futuredemand. China’s government rolled out new incentives for the EV and energy storage industries, pledging compensation for storage infrastructure and aiming to expand EV charging capacity to 180 GW by 2027. Regulators approved reserve reports to restart CATL’s Jiangxi mine, alleviating worries following earlier permit issues at the site which contributes ~ 3% of global output.

Performance of WA Index and Global indices

Top 20 performers of the month:

Pilibara Minerals Limited (ASX:PLS): Pilibara Minerals saw its market capitalisation rise 31% over October, boosted by the release of a strong quarterly report that boasted a 30% increase in revenue, 24% increase in average realised price, and a 13% reduction in unit operating costs (FOB basis) from the previous quarter, with management reaffirming guidance for FY26. Pilbara demonstrated a strong balance sheet, with cash at $852 million with an undrawn credit facility of $625 million, supporting financial flexibility for strategic growth options to increase production, including the potential expansion of Pilgangoora to 2mpta in the future.

Westgold Resources Limited (ASX:WGS): In October 2025, Westgold’s growth was driven by strong operational performance, expanding production capacity and it’s 100% unhedged gold position taking advantage of the rising gold market, with underlying cash build of $108m in the quarter. Growth momentum was underpinned by organic expansion across its operations, particularly the ramp-up at Bluebird–South Junction, Great Fingall, and Beta Hunt, and reaffirmed guidance at existing operations. Westgold’s three year outlook, showing strong growth in both the Murchison and Southern Goldfields operations, at reduced costs further bolstered investor confidence.

Paladin Energy Ltd (ASX:PDN): Noted record quarterly production of 1.07 million pounds of U₃O₈ from the Langer Heinrich Mine and a 63% quarter-on-quarter increase in material mined, demonstrating strong operational momentum as it ramps up toward full production by FY2027, as realised prices rose 21% from the previous quarter, to US$61/lb. Strengthened by their recent A$400 million in equity raisings, including a heavily oversubscribed A$100 million Share Purchase Plan. Alongside progress toward a Final Investment Decision for the Patterson Lake South Project in Canada, Paladin is well positioned to capitalise on a strengthening uranium market supported by tightening supply and accelerating global investment in nuclear energy.

The Top 100 performers of this month were:

European Lithium Limited (ASX:EUR): European Lithium delivered a value-driven rally in October, anchored by a liquidity event of their equity holdings and strategic progress of their core exploration projects. They crystallised over US$120 million in cash from multiple Critical Metal Corp (“Nasdaq:CRML”) share sales to US institutional investors at progressively higher prices of US$7,US$13 and US$16.50 per share, underscoring demand for its US-listed asset. Following this, a $135m share buy-back wasannounced, signalling management’s view that EUR remains undervalued relative to its asset base. Sentiment was further buoyed by amended Tanbreez Rare Earths Project terms in Greenland, where CRML secured a pathway to 92.5% control of the project while EUR holds a strategic 7.5%. The quarterly report reinforced momentum, confirming A$196 million in cash, its long-term offtake agreement with BMW AG, and advancing development at Wolfsberg and Tanbreez.

Focus Minerals Limited (ASX:FML): Focus Minerals’ October share price gains were underpinned by another month of strong gold prices, which rose before easing slightly at month-end. Sentiment was buoyed by the September quarterly report confirming stable production, robust cash generation and high-grade underground performance. At Coolgardie, the Three Mile Hill plant processed 431,346 tonnes, and achieved a 94.5% recovery, with a record 8,274 ounces poured in August. Bonnie Vale underground yielded 9,621 ounces at 8.23 g/t, while total gold sales reached 20,014 ounces at an average realised price of A$5,288/oz. Focus closed the quarter with A$113.6 million in cash and A$41.9 million in cash flow from operations, providing a solid base to support expanded development and drilling across Bonnie Vale, CNX and the Greater Undaunted corridor.

Larvotto Resources Limited (ASX:LRV): Larvotto Resources’ October rally of 51.3% was driven by accelerating Hillgrove Antimony-Gold Project development, high-grade drilling success, and renewed corporate interest. Notable intersections from Eleanora-Garibaldi include 30m at 3.29 g/t AuEq and 5.4m at 11.99 g/t AuEq, with a new Blacklode discovery returning 15m at5.24 g/t AuEq, including 4.2m at 14.46 g/t AuEq. Momentum strengthened after Larvotto announced an EPCM contract to upgrade Hillgrove processing to 0.525 Mtpa, positioning the project to deliver around 7% of global antimony requirement from Q3 2026. The September quarter confirmed a fully funded path to production, with the Final Investment Decision approved following a US$105m Senior Secured Bond issue and an A$70m equity raise, leaving A$62.1m cash at quarter-end. The investor narrative was further buoyed by a non-binding takeover approach from US Antimony Corporation valuing Larvotto at A$1.40 per share; while the offer was rejected, with management deeming it undervalued the company, it highlighted strategic interest in Hillgrove’s near-term production and critical minerals exposure.

Featured articles