WA Index

Issue 240 | November 2025

Welcome to the 240th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

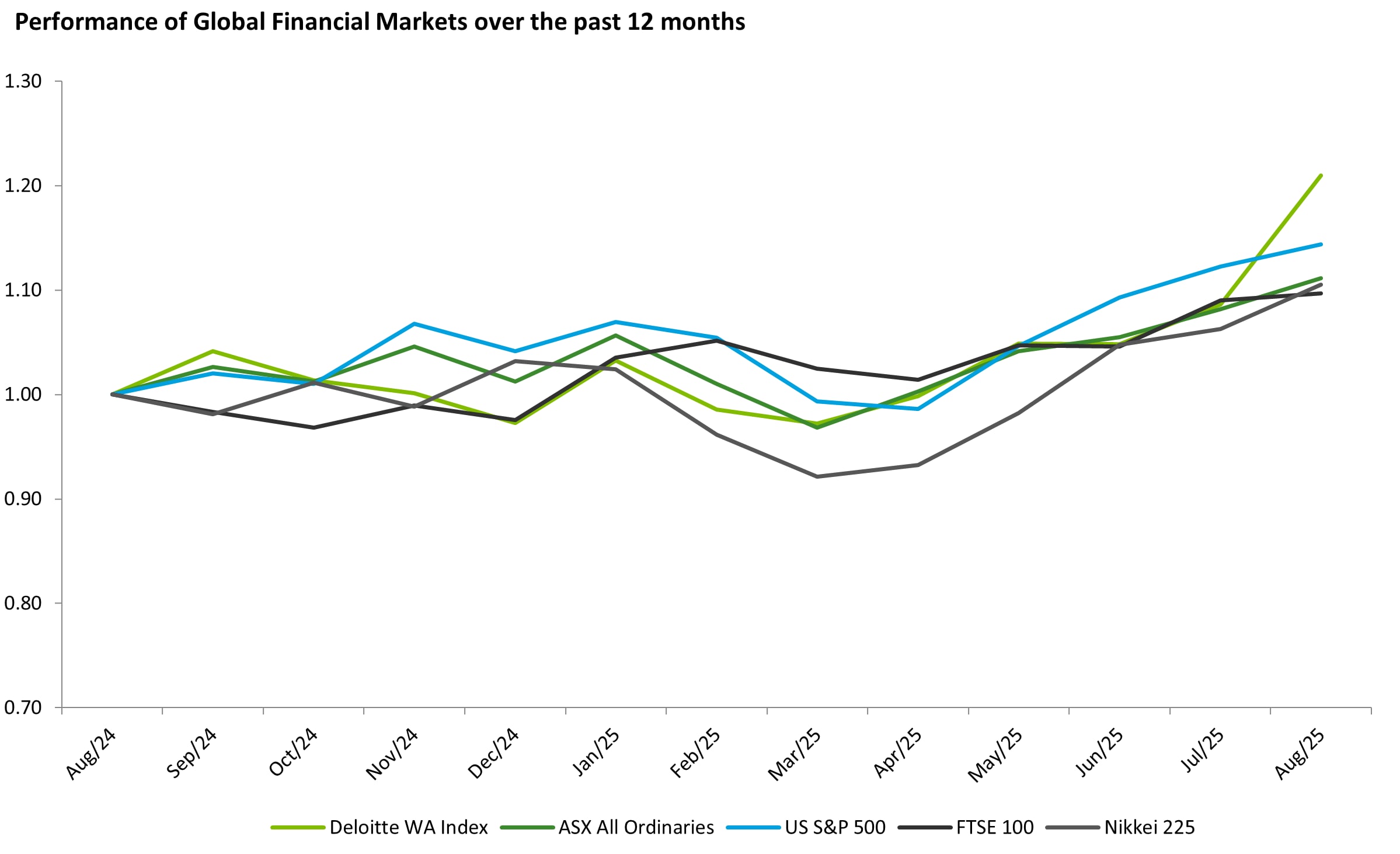

This month, the WA Index gained 4.1%, while all major indices either stayed flat or fell in November. The WA Index was bolstered by stronger commodity prices, particularly in lithium (finally) and gold, with all companies featured this month in the biggest market movers, having exposure to at least one of these commodities. Will these surges continue to move with a “Santa Rally”?

Download the list of WA’s top 100 listed companies, as of 30 November 2025, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Lithium prices rebounded strongly in November 2025, with Chinese lithium carbonate futures pushing to their highest level in around 17 months and SC6 spodumene spot rising roughly 20–25%, improving the near-term revenue outlook for WA hard-rock producers. The move was underpinned by recovering battery and EV demand in China, supportive policy measures and tighter spot availability following prior inventory drawdowns.

Meanwhile, gold prices traded at record or near-record highs across November, repeatedly testing and exceeding about A$6,400/oz, a mid-single-digit gain for the month from already elevated levels and delivering very strong margins for WA gold miners and developers. This strength reflected firm US-dollar gold driven by expectations of future rate cuts and ongoing macro uncertainty, with a softer AUD further amplifying returns for local producers.

Iron ore was stable over November, trading in a relatively tight range around US$100–105/t with little change versus October, leaving WA’s major iron ore producers in a steady, highly profitable pricing environment.

Copper prices remained elevated through November, consolidating around US$11,000/t, close to the upper end of their historical range and well above pre-2021 norms. The market continued to price in strong medium-term demand from electrification, grid and data-centre investment alongside constrained mine supply, supporting robust economics for WA-linked copper and polymetallic operations.

For LNG, Asian spot prices held firm in the high-US$10s to mid-US$11s/MMBtu during November, while European prices softened to its lowest level since mid-2024, reinforcing a premium for Northeast Asia and supporting healthy netbacks for WA exports into Asian markets.

Performance of WA Index and Global indices

Top 20 performers of the month:

IGO Limited (ASX:IGO): experienced a 26% rise in its market capitalisation during November. The move was supported by a rally in the lithium sector, as lithium prices in China climbed to a 17-month high and sentiment towards high-quality producers improved, directly benefiting IGO through its stake in the Greenbushes lithium mine. Sector-wide optimism following stronger spodumene pricing and successful pricing outcomes from peer auctions flowed into IGO’s share price, with investors viewing the company as a leveraged yet relatively low-risk exposure to a recovering lithium market. The release of an update on the acquisition of IGO’s Forrestania Nickel Operation by Medallion Metals Limited (ASX: MM8), in which the parties entered into an ancillary agreement to the sale, provided additional comfort around IGO’s portfolio.

Pilbara Minerals Limited (ASX:PLS): saw its market capitalisation increase significantly during November, supported by a broader rebound in lithium demand and prices. A positive lithium market, particularly a 21% surge in SC6 spodumene prices and lithium carbonate futures in China reaching a 17-month high boosted investor confidence. PLS’ AGM confirmed on-schedule progress for the mid-stream plant, announced an extension of its partnership study with Ganfeng and was accompanied by bullish commentary from Ganfeng regarding future lithium demand growth.

Liontown Limited (ASX:LTR): Liontown’s market capitalisation rose sharply in November, with its share price increasing by 22.2%, driven by the successful outcome of its inaugural spodumene concentrate auction, which achieved a strong sale price at a clear premium to prevailing spot and forward prices and signalled robust demand for its Kathleen Valley product, reinforced by broader lithium sector momentum. Improved market sentiment after a period of oversupply, combined with strong shareholder backing shown at Liontown’s AGM in November, further strengthened confidence in the company’s strategic direction and contributed to its rising market capitalisation.

The Top 100 performers of this month were:

Galan Lithium Limited (ASX:GLN): Galan Lithium’s market capitalisation rose by 85.7% in November, driven primarily by the early completion of a $20 million strategic placement for the construction of Phase 1 operations at its Hombre Muerto West (HMW) project in Argentina, significantly de-risking the pathway to first production in 2026. The completion of the placement highlighted robust investor support for the project and was amplified further by a broader lithium sector rally fuelled by recovering battery demand and supportive EV policies.

Core Lithium Ltd (ASX:CXO): Core Lithium’s market capitalisation surged by 80% in November, driven by the release of an updated mine plan for its Grants deposit, which shifted the strategy to prioritise open-pit mining before transitioning underground, reducing pre-production costs by $35–$45 million and accelerating first-ore production. The announcement also revealed a 33% uplift in the Grants ore reserve to 1.53 Mt at 1.42% Li2O and a 44% increase in contained metal, prompting a 26% share price jump on the day.

Meeka Metals Ltd (ASX:MEK): Meeka Metals’ market capitalisation rose by around 28.9% in November, driven primarily by strong exploration results at its flagship gold asset, highlighted by significant high-grade intersections at Turnberry South, including 8 metres at 14.8 g/t gold, and shallow intercepts at the Andy Well Underground Mine, including 4 metres at 27.8 g/t gold. This momentum was further supported by a strengthening gold price environment, with Australian dollar gold prices exceeding A$6,400/oz later in the month, underpinning improved economics for near-term producers.

Featured articles