WA Index

Issue 243 | March 2026

Welcome to the 243rd edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

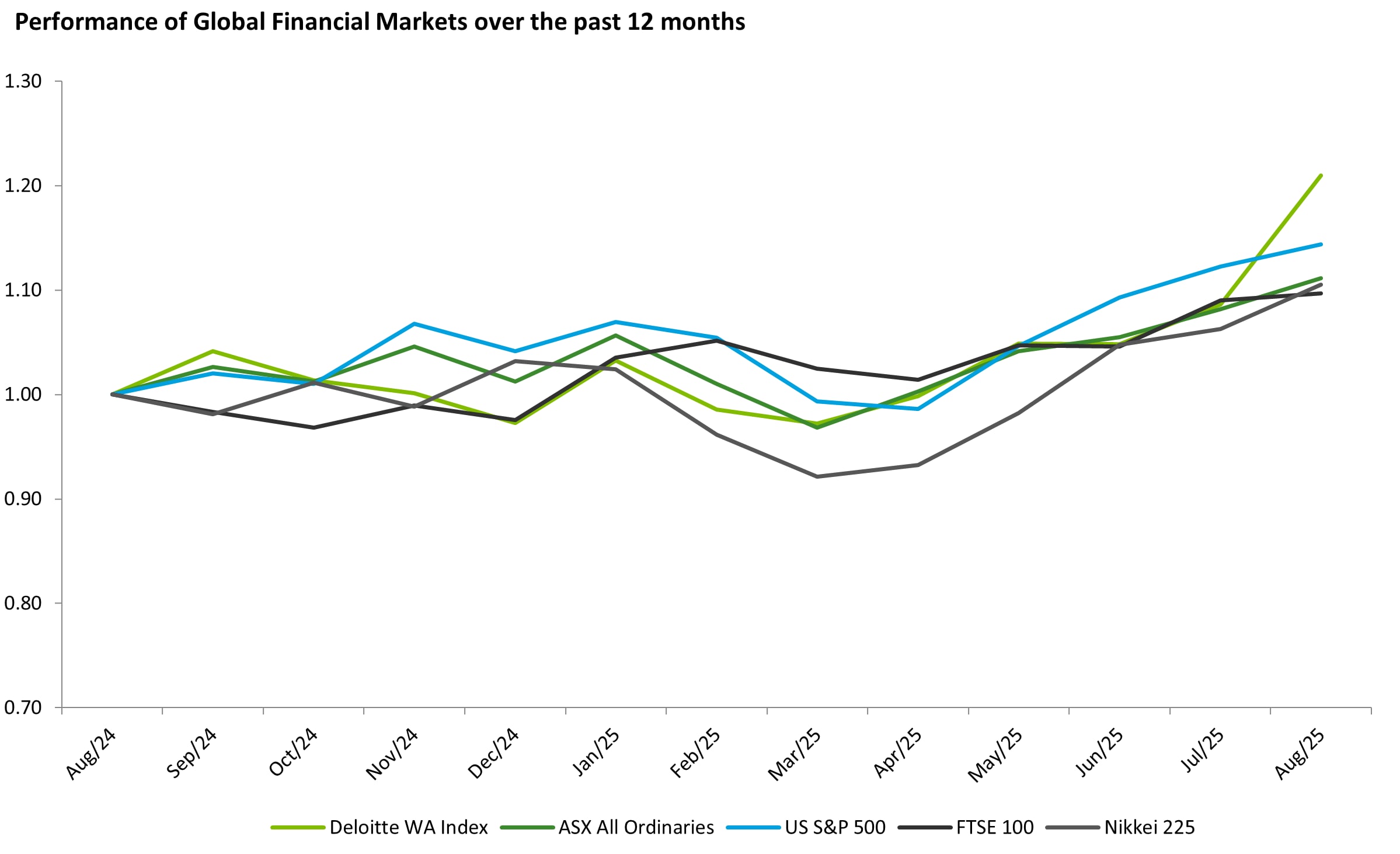

Major global equity indices fell sharply in March 2026, driven by the escalating Middle East conflict, the surge in Brent Crude Oil and LNG prices, and a broad repricing of interest rate expectations as inflation concerns intensified.

The US S&P 500 declined 5.1% over the month, with technology and growth stocks bearing the heaviest losses as rising US 10-year Treasury yields, climbing from 4.15% to 4.44% by 27 March depressed equity valuations. The Federal Reserve held rates at 3.50% - 3.75% at its March meeting and downgraded its rate-cut guidance, further weighing on market sentiment.

The FTSE 100 fell 6.7%, with the decline only tempered by the weighting of BP and Shell, whose share prices rose on the back of surging oil prices. The Nikkei 225 recorded the steepest decline among the four indices, falling 13.2%, its largest monthly fall since October 2008, reflecting Japan's vulnerability to the crisis, with approximately 95% of its crude oil imports originating from the Middle East and 70% transiting the Strait of Hormuz.

The Australian All Ordinaries fell 8.0% (9,436 to 8,684), its worst monthly performance since June 2022, compounded by the Reserve Bank of Australia's decision to hike the cash rate to 4.10% in March, the only major central bank to tighten during the crisis, which amplified domestic selling pressure even as rising LNG and Brent Crude prices provided a partial offset through Australia's significant energy and resources export sector. The WA Index also fell 9.2% in March, with the large concentration of precious and base metal miners suffering on depressed commodity prices.

Unlike most conflicts that cause a rush to the safe haven of gold, this time, the higher oil process will push inflation up. Gold traditionally struggles in a high inflation environment, which is what we are seeing play out now.

Download the list of WA’s top 100 listed companies, as of 31 March 2026, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold: March 2026 saw gold record its largest monthly fall of the year, declining by 19% after hitting a new all-time high spot price of US$5,440/oz on 1 March 2026. This decrease was largely driven by the escalating conflict involving Iran, which triggered a sharp surge in oil prices that prompted markets to significantly reprice interest rate expectations upward. While gold traditionally serves as a hedge against both uncertainty and inflation, rising interest rates increased the opportunity cost of holding the non-yielding metal, making yield-bearing assets such as Treasury bonds comparatively more attractive, weighing on prices throughout the month. Gold recovered marginally toward month end, supported by cautious optimism around a potential de-escalation in the Middle East conflict, closing March at US$4,580/oz.

Silver: Silver prices followed gold lower during March 2026, albeit with greater volatility. Silver fell 34% for the month after reaching its second peak of the year at US$112/oz on 1 March 2026. The drivers of this decline were largely consistent with those described above in respect of gold prices, further compounded by the US Federal Reserve's decision to hold interest rates at 3.5%–3.75% and downgrade its forward guidance to a single rate cut in 2026. Silver closed March at US$74/oz.

Brent Crude Oil: Brent Crude Oil recorded its largest monthly surge on record, increasing by 63% month-on-month. Prices peaked at US$119/bbl intra-day following a significant escalation in geopolitical tensions in the Middle East, as Iran moved to restrict access to shipping routes through the Strait of Hormuz, halting the free movement of oil and gas tankers and severely disrupting global oil supply. The Strait carries approximately 20% of the world's oil exports, and its effective closure drove sharp upward pressure on prices. Given the uncertainty surrounding resolution of the conflict.

LNG: The Asian LNG price rose steadily through March 2026, increasing by 45% to US$20.5/MBtu at month end, driven by disruptions to LNG transit through the Strait of Hormuz, through which approximately 20% of global LNG passes as a result of the ongoing Middle East conflict. The European LNG price reacted with considerably more volatility, surging 60% to a peak of US$21.7/MBtu on 18 March 2026 before retreating to US$16.5/MBtu at month end. This volatility was triggered by an Iranian strike on the world's largest LNG plant in Qatar on 18 March 2026, which materially disrupted production.

Performance of WA Index and Global indices

Top 20 performers of the month:

Woodside Energy Group Ltd (ASX:WDS): Woodside's market capitalisation increased by approximately 24% during March 2026, to $66.6 billion, representing a 52-week high. The increase was driven by the escalating Middle East conflict and the closure of the Strait of Hormuz, which disrupted approximately 20% of global seaborne crude and LNG trade and sent Brent crude surging to US$119/bbl intra-day and Asian LNG spot prices above US$20/MMBtu. As one of Australia's largest LNG exporters with direct exposure to international energy prices, Woodside was a primary beneficiary of this commodity price shock. The share price jumped 6.8% on 2 March as the conflict erupted, and a further 7.2% on 19 March following Iran's strike on Qatar's Ras Laffan LNG facility. Woodside also appointed Liz Westcott as permanent CEO and Managing Director on 18 March, resolving a leadership succession that had been underway since late 2025, while a deal with the Western Australian Government to unlock approximately 2.8–3 million additional tonnes of annual LNG export capacity from Pluto further reinforced Woodside's near-term production outlook ahead of the Scarborough project's targeted first cargo in Q4 2026.

Lynas Rare Earths (ASX: LYC): Lynas Rare Earths' market capitalisation held broadly flat through March 2026, finishing the month at A$19,083 million, a decline of just 0.11% against a 14.6% fall in the ASX metals and mining sector. This resilience was underpinned by a sequence of developments across the month. Malaysia renewed Lynas's operating licence for 10 years through 2036, removing the single largest regulatory overhang on the stock. Lynas also announced a revised long-term supply agreement with Japan Australia Rare Earths (JARE) extending to 2038, committing 5,000 tpa of NdPr oxide at a floor price of US$110/kg, which drove a 16% surge in the share price over two sessions. A US$96 million binding Letter of Intent with the US Department of Defence further formalised Lynas's role as the Pentagon's primary non-Chinese rare earth supplier at the same floor price. First samarium oxide production and a joint venture with South Korea's LS Eco Energy for rare earth metal production in Vietnam rounded out the month's announcements. Broader macro tailwinds reinforced the investment case, as the Strait of Hormuz closure and surging oil prices accelerated the global energy transition narrative, with NdPr prices remaining near double December 2024 levels and a 63% ex-China price premium reflecting the structural supply deficit Lynas is uniquely positioned to address.

Liontown Resources (ASX: LTR): Liontown Resources' market capitalisation finished March 2026 essentially flat at (0.3%), significantly outperforming the ASX materials sector's 14.6% decline. Liontown experienced a volatile March, falling 22% peak-to-trough to an intraday low of A$1.34 on 23 March during the Strait of Hormuz crisis, before staging a full recovery to close at A$1.70 on 25 March. The turnaround was anchored by strong H1 FY2026 half-year results, which reported revenue of A$207.5 million, up 107% year-on-year, alongside confirmation that Kathleen Valley's 1.5 Mtpa underground mining run-rate had been achieved on schedule. The macro environment provided a powerful overlay, with surging oil prices intensifying the global EV demand narrative. With production pre-committed to Tesla, Ford, and LG, and spodumene prices holding above US$2,000/t, Liontown offered investors both operational momentum and direct exposure to the energy transition thesis the crisis had reinforced.

The Top 100 performers of this month were:

Lindian Resources Limited (ASX:LIN): Lindian Resources recorded a notable surge in market capitalisation during March 2026, rising from $886.93 million to $1,481.01 million, representing a $594.08 million (67%) increase. The primary catalyst was the announcement on 3 March 2026 of a binding term sheet for Lindian's 51%-owned Incorporated Joint Venture with Kazakhstan-based RA-Group LLP to acquire 100% of the SARECO Mixed Rare Earth Carbonate processing facility in Stepnogorsk, Kazakhstan, for a total consideration of US$15 million, of which only US$3 million is payable upfront. This transaction marks a strategic shift from a concentrate-only developer to an integrated rare earths producer, enabling the processing of approximately 12,500 tonnes per annum of monazite concentrate from the Kangankunde Rare Earths Project into higher-value downstream products, with MREC production targeted for Q4 2026. The announcement was further supported by two additional events, being the release of Lindian's half-year report on 13 March 2026, and the company's inclusion in the S&P/ASX All Ordinaries Index effective 23 March 2026. Collectively, these developments significantly strengthened investor confidence and drove a substantial re-rating of the company's valuation.

EchoIQ Limited (ASX:EIQ): EchoIQ Limited's market capitalisation increased by approximately 47% during March 2026, driven principally by two concurrent events in the final week of the month. On 24 March 2026, EchoIQ announced an expanded distribution agreement with Mayo Clinic, one of the world's leading healthcare institutions, establishing a pathway for the commercialisation of its EchoSolv HF heart failure detection AI through the Mayo Clinic Platform Solutions Studio Program, providing access to Mayo's hospital network and over 80 external partner hospitals under a three-year initial term with automatic renewal, noting that the agreement is contingent on FDA clearance of EchoSolv HF, which remains under review. The announcement coincided with EchoIQ's inclusion in the S&P/ASX All Ordinaries Index effective 23 March 2026, which increased buying pressure and contributed to the month's price appreciation. As an early-stage company, the re-rating reflects investor confidence in the potential commercial pathway the Mayo Clinic relationship represents.

Duratec Limited (ASX:DUR): Duratec Limited's market capitalisation increased by approximately 21.4% during March 2026, reflecting a combination of strong underlying financial performance and a meaningful new contract win. On 27 March 2026, Duratec announced the award of an approximately A$45 million, 12-month services contract with Lihir Gold Limited, a subsidiary of Newmont Corporation, for plug and abandonment services at the Lihir Operations in Papua New Guinea, representing the company's first services delivery in that country and a geographic expansion of its Energy and Resources business. This announcement built on the momentum generated by Duratec's H1 FY2026 results released in late February, which reported revenue of A$273.3 million, and record net profit after tax and normalised EBITDA of A$13.4 million and A$27.5 million respectively. In addition, Duratec's growing defence credentials, including its AUKUS-linked infrastructure joint venture and existing presence at HMAS Stirling continued to underpin positive investor sentiment, with management indicating a substantial pipeline of prospective defence awards in the near term. Collectively, these factors reinforced Duratec's position as a diversified engineering and services contractor with strong earnings visibility, supporting the increase observed through the month.

Featured articles