WA Index

Issue 243 | March 2026

Welcome to the 243rd edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

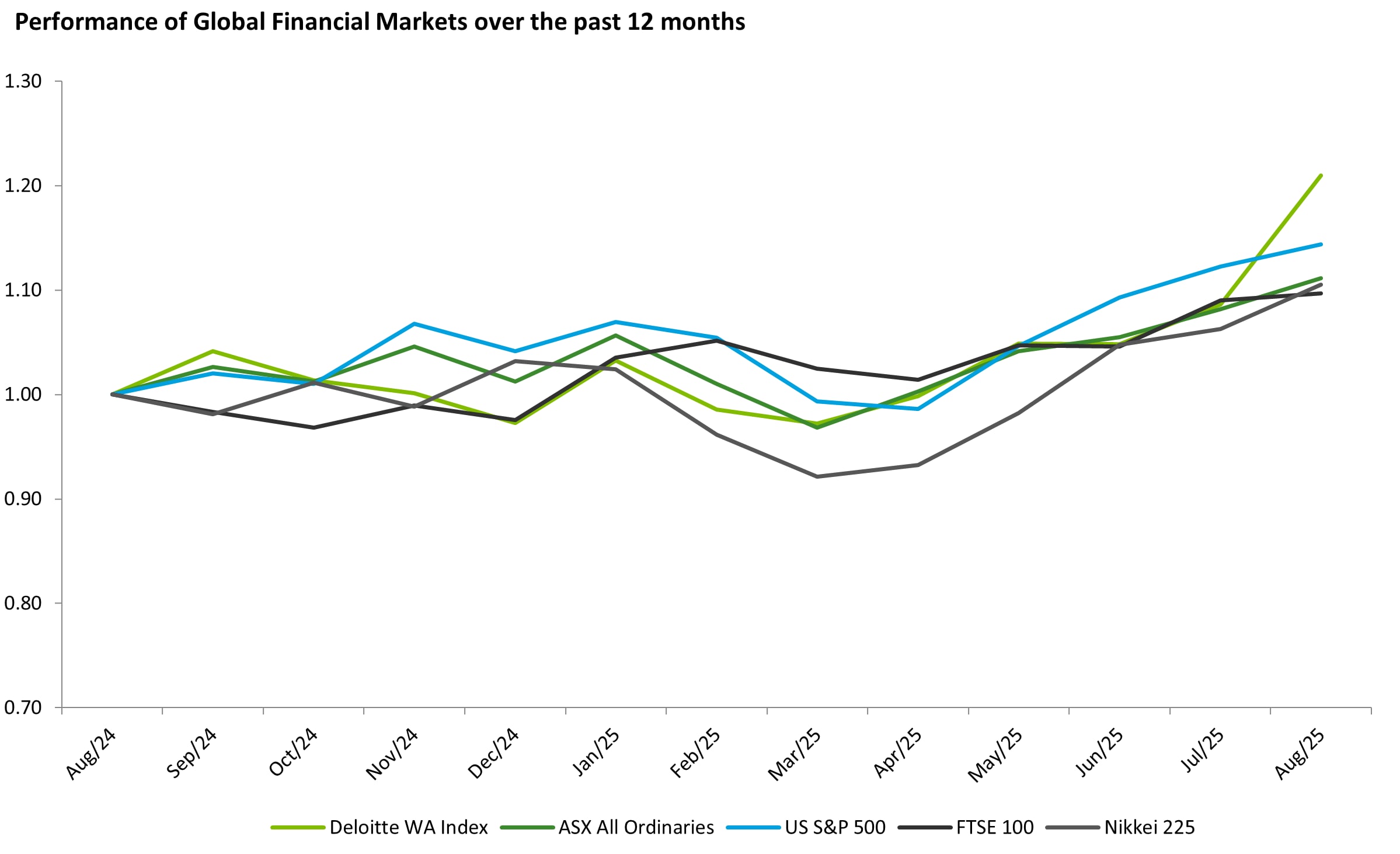

Global markets commenced 2026 with broad gains, led by a 5.9% surge in the Nikkei and a 1.6% rise in the All Ordinaries. This positive momentum flowed into Western Australia’s resource sector with the WA Index rising by 6.4%, championed by gold prices shattering records to exceed A$7,000/oz.

Uranium markets remained robust through January, supported by tight supply conditions and continued contracting activity, while iron ore proved resilient despite typical seasonal headwinds. Within critical minerals, lithium showed signs of stabilisation, with sentiment improving as the market shifted from volatility toward a more balanced, fundamentals-driven outlook. Increasing geopolitical tensions are also impacting this segment, and whilst not benefitting from the continued move to gold as safety, long term sentiment is definitely changing.

Globally, mining and metals companies are redefining how they create and share value as these materials become increasingly crucial for driving innovation. Deloitte recently released "Tracking the Trends 2026" which outlines the top 10 trends that are shaping the mining and metals sector in the next 12-18 months. For further information, access a copy of the report here.

Download the list of WA’s top 100 listed companies, as of 31 January 2026, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold: was the standout performer in January, continuing its record-breaking run. The Australian Dollar gold price surged past A$7,800 per ounce, before settling at A$7,200/oz at close. Spot prices were driven by a combination of a softening Australian dollar and sustained geopolitical instability which spurred safe haven buying. This high-price environment provided a massive windfall for WA producers, with margins expanding significantly as the AISC curve remained relatively stable while revenue per ounce climbed.

Uranium: The uranium market remained strong, characterised by tight supply and strong term contracting. The spot price held firm above US$80 per pound, with realised contract prices for producers like Paladin often sitting in the low-to-mid US$70s for Q2. Sentiment was supported by global commitments to nuclear capacity expansion, which kept a floor under prices and encouraged development activity across the WA uranium sector.

Iron Ore: Iron ore prices remained resilient in January, defying some expectations of a seasonal slowdown. The benchmark 62% Fe price traded in a range of US$115–US$125 per tonne, supported by stimulus measures in China and steady restocking demand from steel mills ahead of the Lunar New Year. While not experiencing the explosive growth of gold, the stability of the iron ore price continued to provide a strong foundational revenue stream for the state's major miners.

Lithium: The lithium sector showed signs of stabilisation after the volatility of the previous year. Spodumene concentrate (SC6) prices hovered around US$1,050–US$1,150 per tonne. While the peaks of the past were not revisited, the "panic selling" phase appeared to have ceased, replaced by a more fundamental market driven by steady EV production growth and supply discipline from major producers.

Performance of WA Index and Global indices

Top 20 performers of the month:

Paladin Energy Ltd (ASX:PDN): saw its valuation increase in January by 44.4% after delivering a robust quarterly update that confirmed the Langer Heinrich Mine is performing at the upper end of expectations. Production for the quarter rose 16% to 1.23Mlb U3O8, and the company guided full-year production toward the top of its 4.0–4.4Mlb range. The market responded positively to the healthy margins achieved, with an average realised sales price of US$71.8/lb against a production cost of US$39.7/lb, alongside a strengthened balance sheet holding US$278.4 million in cash and investments following a successful debt restructure.

South32 Limited (ASX:S32): saw its market capitalisation rise 29.8% to $8.85b in January, driven by strong commodity price tailwinds, especially in copper, silver, and aluminium. The company delivered strong quarterly results, with higher realised prices and disciplined cost management lifting earnings. Operational performance remained solid, with production guidance reaffirmed and growth projects on track. Continued strong cash generation enabled ongoing shareholder returns, reinforcing investor confidence. The combination of favourable market conditions and operational execution supported the share price rally and highlights South32’s solid outlook.

Greatland Resources Limited (ASX:GGP): saw its market capitalisation rise 25.4% in the opening month of 2026, reaching $8.85b. This was fuelled by heightened speculation and the realisation of gold and copper price gains. The company’s December 2025 production update was strong, highlighting robust operational performance and reaffirmed production guidance. Higher realised gold prices, combined with disciplined cost management, lifted earnings and showed strong operating cash flows, with Greatland generating $406m for the quarter. Investors responded to both the favourable market conditions and Greatland’s operational delivery, viewing the company as well positioned for continued growth. This share price rally underscores confidence in Greatland’s outlook and its leverage to key metals.

The Top 100 performers of this month were:

Australian Strategic Materials Limited (ASX:ASM): experienced a massive re-rating in January following the announcement of a takeover bid by US-based Energy Fuels Inc. The company entered a Scheme Implementation Deed valued at approximately A$1.60 per share, representing a staggering 121% premium to its last closing price. The transaction, designed to create a Western-focused "mine-to-metal" rare earths miner, was unanimously recommended by the ASM Board. The deal structure, which includes Energy Fuels shares and a special cash dividend, provided immediate value realisation for shareholders and solved the project funding risk for the Dubbo Project, driving the share price to align with the offer value.

Forrestania Resources Limited (ASX:FRS): Forrestania Resources saw a surge in activity, rising 135% on December close, with market interest in January driven by an aggressive consolidation strategy to build a major gold business. The company moved to compulsorily acquire the remaining shares in Kula Gold after securing a 90% interest and simultaneously announced the strategic acquisition of the Gibraltar tenements to consolidate its Coolgardie Hub. Further reshaping its portfolio, Forrestania executed an asset swap with Catalina Resources to expand its Eastern Goldfields footprint while divesting non-core copper assets, signalling to the market a disciplined focus on rapid resource growth and production pathways.

Beacon Minerals Limited (ASX:BCN): continued to see support in January, benefiting directly from the record gold price environment highlighted by its peers. With Australian dollar gold prices reported by the sector exceeding A$7,800/oz during the month, Beacon’s status as a consistent, relatively small scale but low-cost producer at the Jaurdi Gold Project positioned it as a key beneficiary of margin expansion. The 59% rise in market capitalisation was driven by yield-focused investors seeking exposure to the company's reliable operational cash flows and dividend potential amidst the gold sector rally.

Featured articles