WA Index

Issue 243 | March 2026

Welcome to the 243rd edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

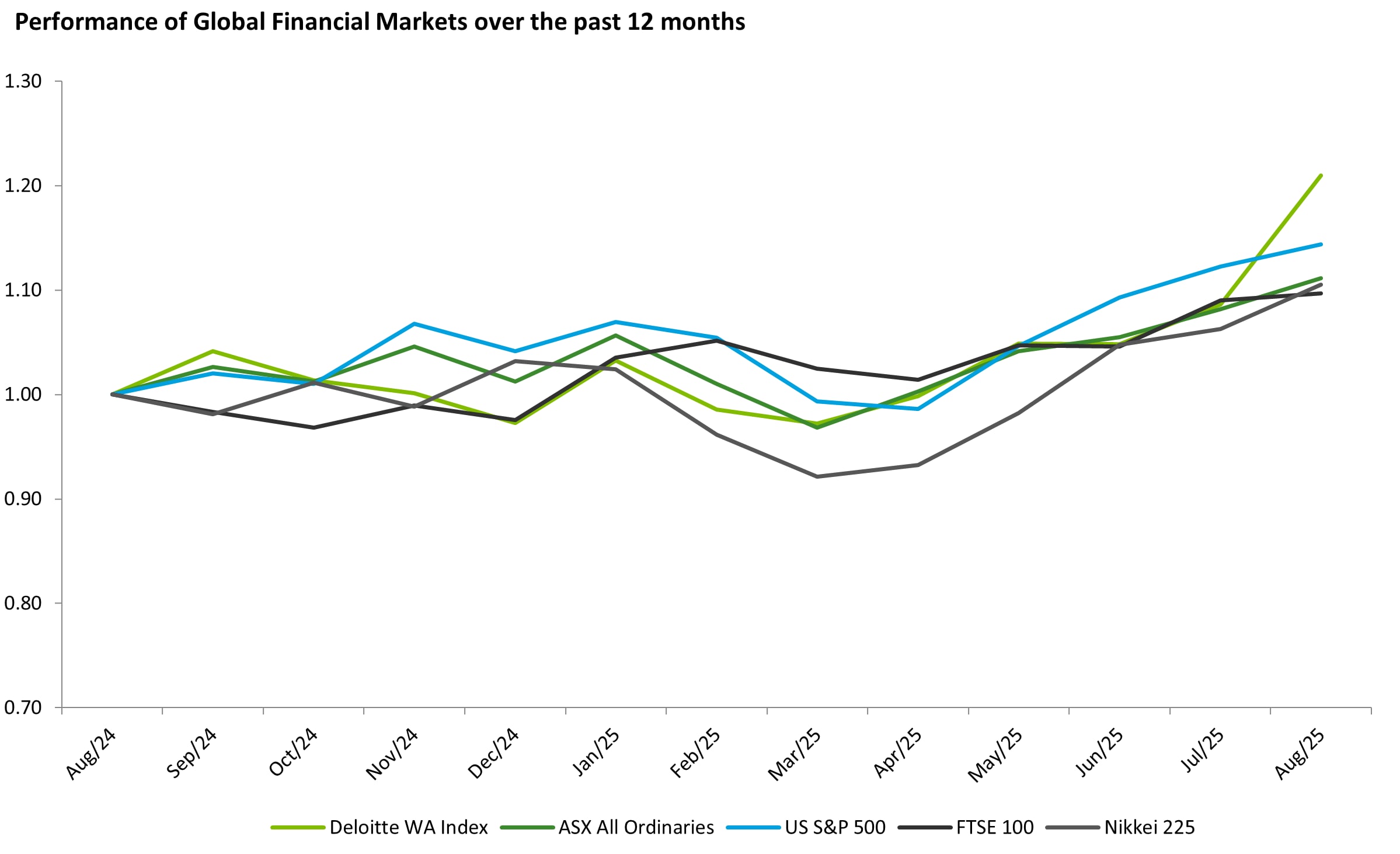

Global equity markets delivered mixed performance in February 2026. Australia’s All Ordinaries Index rose 3.0% to 9,436 points, supported by strength in the resources and mining sectors amid improving commodity prices, with the WA Index rising 3.4% in February 2026.

In contrast, the US S&P 500 declined slightly by 0.9% to 6,879 points as investors responded cautiously to shifting interest rate expectations and mixed economic data. European markets performed strongly, with the FTSE 100 climbing 6.7% to 10,911 points, driven by gains in energy, mining and financial stocks. Japan’s Nikkei Index recorded the strongest performance, rising 10.4% to 58,850 points, supported by a weaker yen, strong export performance and continued investor inflows into Japanese equities.

Subsequent to the month of February, we have again seen significant global affairs creating further uncertainty on equity markets. Some impacts have already been felt by the equity markets and consumers alike. Mid to Long term impacts are yet to become clear as we all wait to see what happens next.

Download the list of WA’s top 100 listed companies, as of 28 February 2026, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold: Gold prices remained highly volatile through February 2026 but overall moved higher, with prices rising and trading around US$5,200/oz by late February. The rally was supported by geopolitical tensions and lower US Treasury yields, which increased safe haven demand and continued a multi month upward trend.

Lithium: Lithium prices experienced a flat February 2026 following a strong rally earlier in the year. Lithium carbonate prices had surged significantly in the prior month, with reports of around a 60–70% increase over roughly 30 days, before entering a phase of consolidation during February as profit taking and supply adjustments created short term volatility.

Coal: Coal markets were mixed during February 2026. Australian coking coal prices remained elevated at around US$250/t, reflecting earlier supply disruptions and weather related constraints, although price growth slowed as supply normalised and Chinese demand weakened around the Lunar New Year period, leading to more stable or slightly softer pricing late in the month.

LNG: Asian LNG prices softened through much of February 2026 before partially recovering later in the month. The JKM benchmark fell from the low US$12/MBtu range at the start of February to the low US$10s by mid month, largely due to reduced demand during the Lunar New Year and easing geopolitical tensions, before rebounding slightly as Asian buyers returned to the spot market.

Performance of WA Index and Global indices

Top 20 performers of the month:

Lyna Rare Earths Limited (ASX:LYC): Lynas Rare Earths’ market capitalisation increased by 27.4% in February following the release of its H1 FY2026 results, which reflected a significant improvement in financial performance. The company reported net profit of $80.2 million as at 31 December 2025, up from $5.9 million in the prior corresponding period, with revenue reaching $413.7 million. Performance was supported by a sharp rise in rare earth oxide prices, particularly Neodymium Praseodymium (NdPr), which reached three year highs of US$111.5/kg in February 2026 amid tightening supply conditions and robust demand. Demand for rare earth materials has been further supported by geopolitical developments, including the United States’ efforts to reduce reliance on China for critical minerals through initiatives such as a proposed US$12 billion strategic stockpile and discussions around price support mechanisms for non Chinese supply. In addition, the Australian Government’s establishment of a $1.2 billion critical minerals strategic reserve has strengthened investor sentiment toward the sector.

PLS Group Limited (ASX:PLS): PLS Group’s market capitalisation increased by 21.0% in February, supported by improved operational and financial performance reported in its H1 FY2026 results. The company recorded strong operating cash generation and revenue growth, with quarterly revenue reaching $373 million, representing a 49% increase on the prior quarter. This performance was driven by higher realised lithium prices and increased sales volumes of spodumene concentrate from its Pilgangoora operations. PLS also reported a cash operating margin of $166 million, reflecting improved profitability alongside continued cost discipline. Operationally, both production and sales volumes increased, while the average realised selling price rose to approximately US$1,161/t, reflecting improving conditions across lithium markets. The company’s strong balance sheet and enhanced operating cash flows have reinforced market confidence in its ability to capitalise on strengthening lithium demand fundamentals.

Regis Resources Limited (ASX:RRL): Regis Resources’ market capitalisation increased by approximately $1,045 million during February following a positive market response to its H1 FY2026 operational and financial results. The company reported revenue of $641 million and operating cash flow of $419 million, supported by solid production and gold sales from its Duketon and Tropicana operations. Interim results indicated gold sales revenue of $1,088 million from 182,327 ounces sold at an average realised price of $5,968/oz. Regis also reported cash and bullion holdings of $930 million, valued at $6,437/oz, reflecting a strong balance sheet position. The company maintained its FY2026 production guidance of 350,000–380,000 ounces while continuing to advance exploration and development initiatives aimed at extending mine life across its Duketon operations. Strengthening gold prices have further supported investor confidence in the company’s production outlook and earnings potential.

The Top 100 performers of this month were:

St George Mining Limited (ASX:SGQ): St George Mining’s market capitalisation increased by 66.7% in February, supported by a series of positive operational updates and government support for its Araxá niobium and rare earths project in Brazil. During the month, the company released several drilling updates indicating that ongoing drilling had successfully expanded and refined the project’s mineral resource. Mid month results included a significant intercept of 164 metres from surface, highlighting broad, high grade mineralisation of both rare earth elements and niobium and suggesting the potential for a substantial resource expansion. The company also secured a preferential goods tax regime from the State of Minas Gerais, which is expected to materially reduce development costs and enhance the project’s economic viability. In addition, St George acquired a strategic 166 hectare parcel of land intended for future processing and operational infrastructure. On 27 February, the company requested a trading halt pending the announcement of a substantial increase to the Araxá Project’s Mineral Resource Estimate, contributing to heightened market speculation, strong trading activity and a sharp rise in the share price toward the end of the month.

Forrestania Resources Limited (ASX:FRS): Forrestania Resources reported a $279.48 million increase in market capitalisation in February, reflecting continued investor interest following a series of operational and strategic developments. During the month, the company announced an ore purchase agreement with Westgold Resources Ltd and completed the acquisition of the Mt Dimer, Mt Jackson and Johnson Range tenements. Progress was also made toward establishing Lake Johnson as a potential gold processing hub, alongside the execution of two binding heads of agreement to acquire additional exploration tenements within the Forrestania and Goldfields regions of Western Australia. Operationally, the company completed drilling at the Lady Lila Project and commenced drilling at the British Hill Project. These developments signalled ongoing progress in advancing the broader Forrestania project portfolio and strengthened market confidence in the company’s exploration strategy and growth potential.

Minerals 260 Limited (ASX:MI6): Minerals 260 recorded a $603.79 million increase in market capitalisation in February, extending the positive momentum observed in January. The rise largely reflected strong investor response to exploration and resource development updates during the month. Notably, the company reported high grade drilling results from the Bullabulling Gold Project in Western Australia’s Eastern Goldfields, as part of ongoing resource expansion activities aimed at supporting future development studies. Minerals 260 also announced a $220 million strategic funding agreement with Franco Nevada to accelerate development of the Bullabulling project while reducing financing risk. These developments highlighted the potential scale and growth prospects of Bullabulling as a significant gold development asset, strengthening market confidence in the project’s advancement.

Featured articles