WA Index

Issue 237 | August 2025

Welcome to the 237th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

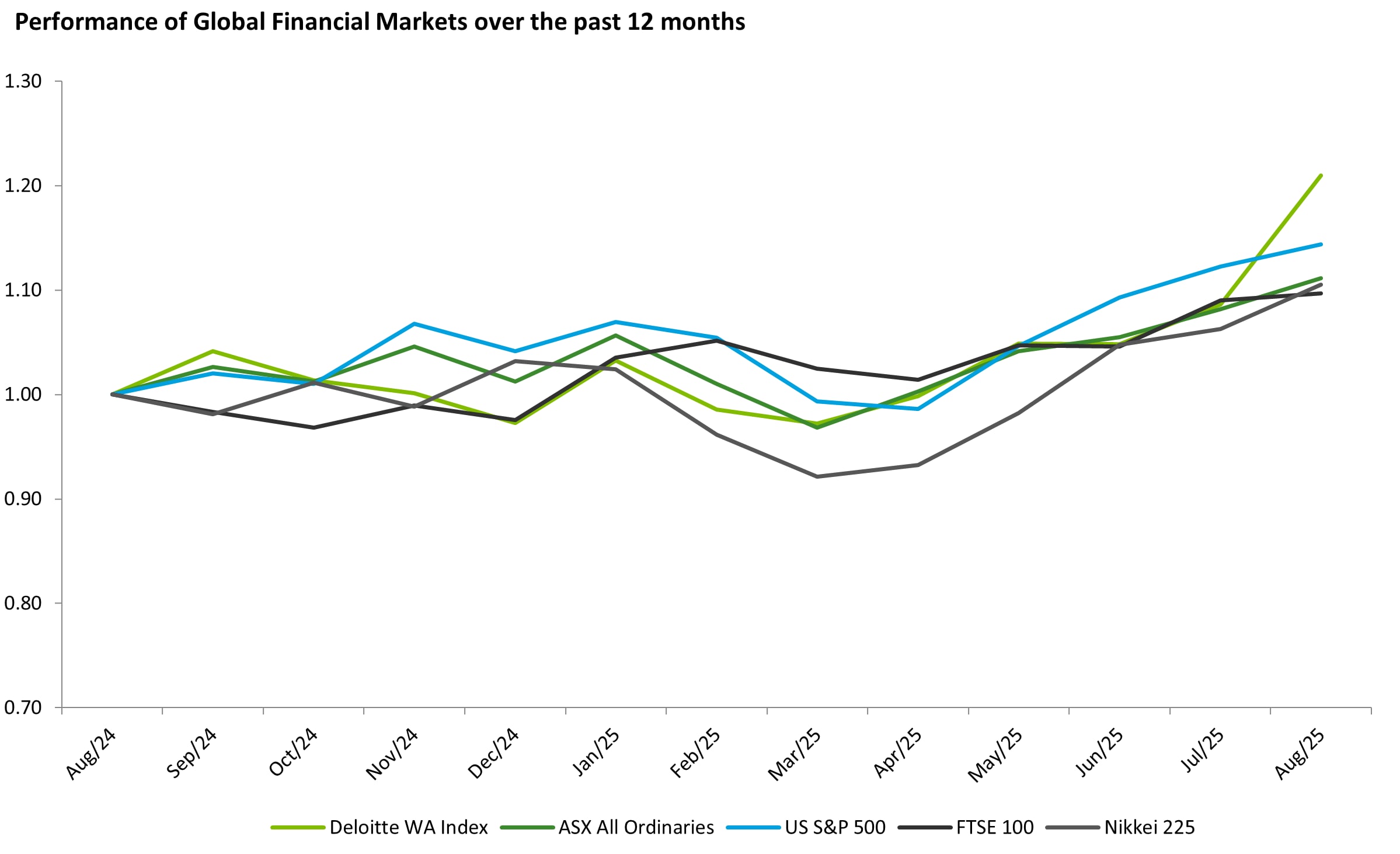

Global equities edged higher in August 2025, with major indices making or approaching record highs as softer inflation and resilient earnings kept rate cut hopes alive and volatility contained. Market breadth improved versus earlier in the year, with gains extending beyond mega cap tech to cyclicals and small caps, while defensive stocks still found underlying support against a backdrop of global uncertainty.

A softer AUD aided Australian equities’ margins and offshore earners, with a weaker GBP helping FTSE multinationals, and stable USD conditions reduced cross border headwinds. Overall, investors rewarded clear cash flow and capital return and leaned into quality and balance sheet strength across regions.

The same trends can be observed in the WA Index, headlined by gold stocks continuing their significant upwards momentum. Half of the WA Index Top 20 are now gold stocks!

Download the list of WA’s top 100 listed companies, as of 31 August 2025, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

In August 2025, commodity markets broadly steadied, helping resource equities re-rate where cash flow visibility and capital returns were clear. Precious metals remained firm at elevated levels, especially in AUD terms, sustaining strong margins for Australian gold producers and reinforcing dividend/buy-back narratives. Bulks were steadier: iron ore hovered around the important US$100/t mark, easing immediate concern and supporting near-term earnings confidence for the majors.

Energy was mixed, oil softened as OPEC+ unwound supply cuts against uneven demand and high inventories, which capped pure oil names but still rewarded low-cost producers with disciplined shareholder returns; coal pricing stayed resilient on demand from Asia and energy security themes. Battery materials sentiment turned more positive, led by a rebound in lithium prices on supply headlines and expectations of tighter balances into 2026–27, shifting positioning towards leveraged, low-cost producers and high-quality developers.

Base metals were turbulent, with policy and shifting tariff dynamics fuelling volatility and tempering risk appetite for capex-heavy copper projects despite intact long-term electrification projects. A softer AUD provided an extra cushion to Australian miners’ margins, amplifying the supportive effect of steady commodity producers. Overall, investors favoured exposures with clear free-cash-flow durability, visible catalysts (results, guidance, buy-backs/dividends), and operational de-risking, while remaining selective towards higher-cost or policy-sensitive segments.

Performance of WA Index and Global indices

Top 20 performers of the month:

Pilbara Minerals Limited (ASX:PLS): Pilbara’s market cap gained on a sector-wide lithium sentiment rebound in August and an FY25 result late in the month that, while down year on year, came in roughly in line with investor expectations, prompting a shift in broker narratives toward a lithium price bottoming setup. Continued execution at Pilgangoora and expansion plans positioned PLS as a relative winner in any demand recovery, and investors responded to signs of improving pricing dynamics plus operational resilience. The result was a notable rally into and after the results window as confidence improved in FY26–28 earnings trajectories.

Vault Minerals Limited (ASX:VAU): Vault’s market cap lifted sharply after its 21 Aug 2025 FY25 results and capital management announcement. The company reported A$1.43bn revenue, A$619m adjusted EBITDA (43% margin) and A$237m NPAT, ending FY25 with A$685.9m cash and bullion and no debt. Management simultaneously launched an on market buyback of up to 10% of issued capital, explicitly signalling that the share price did not reflect the company’s cash generation or outlook. Investors interpreted the sizeable buyback and strong free cash flow as high-confidence markers, particularly when paired with an optimised Leonora strategy (KoTH expansion) and a path to greater spot price participation as the hedge book runs off, supporting a re rating into late August.

Westgold Resources Limited (ASX:WGX): Westgold’s August move was anchored by late month shareholder returns and clarity on outlook. On 28 Aug 2025, the company declared a final dividend and commenced an on market share buyback, reinforcing balance sheet strength and capital discipline. Those announcements followed a stronger June quarter update and early-August FY26 guidance/context (including technical disclosures around Diggers & Dealers), giving investors better visibility on production, costs, and cash generation into FY26. With a supportive AUD gold price backdrop, the dividend and buyback combination served as a direct confidence signal and helped drive a market cap step-up into month end.

The Top 100 performers of this month were:

Alkane Resources Limited (ASX:ALK): Alkane’s market cap expansion in August 2025 was driven by the completion of its merger of equals with Mandalay Resources on 5–6 Aug 2025 and the commencement of dual listing on the TSX on 7–8 Aug. The deal created a mid-tier, diversified gold and antimony producer with three operating mines (Tomingley, Costerfield, Björkdal), pro forma FY2025 output around 160koz AuEq rising to >180koz in 2026, and an enhanced balance sheet and liquidity profile. Investor confidence was bolstered on the scale, index eligibility prospects, and improved capital markets access; Alkane highlighted expected benefits from greater trading liquidity and anticipated index inclusion, alongside a strengthened board and management mix.

Falcon Metals Limited (ASX:FAL): Falcon re-rated on discovery momentum after reporting visible gold in multiple stacked veins and standout assays at its Blue Moon prospect north of Bendigo (e.g., 1.2m at 543 g/t Au, upgraded shallow 2.8m at 17.7 g/t Au) in early August. The news resulted in shares spiking on the day of the visible gold release. Investor confidence reflected the combination of exceptional grades, a clear geological model, expanding drilling programs, and the prospect of sustained news flow that could underpin further resource definition.

Lindian Resources Limited (ASX:LIN): Lindian’s August strength reflected steady derisking at Kangankunde (Malawi) through early works and logistics contracts, ongoing ANSTO test work to produce a mixed rare earth carbonate product for offtake engagement, and reiterated concentrate quality (high TREO, low U/Th) that supports marketing prospects. With global supply chain diversification top of mind, any tangible steps toward offtake and project execution tend to lift sentiment and implied valuations for quality REE projects; investors read these milestones, funding discussions, and experienced counterparties (e.g., Mota-Engil for access works) as confidence signals that shorten the path to development.

Featured articles