WA Index

Issue 244 | April 2026

Welcome to the 244th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

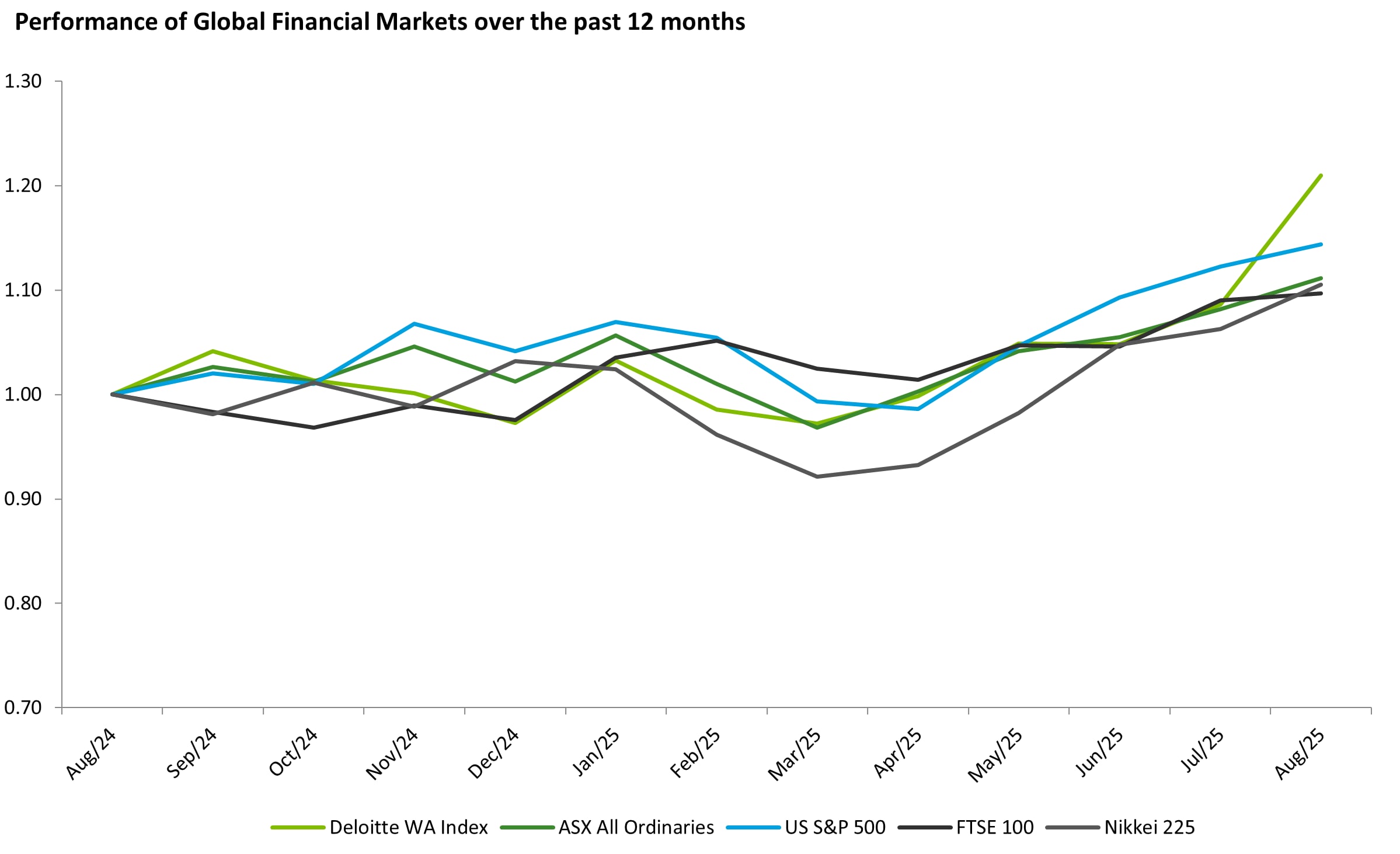

Global equity markets stabilised in April 2026 after the significant disturbance in March, although volatility remained elevated as Middle East tensions persisted and energy prices stayed high. Early-month ceasefire optimism supported risk sentiment, while resilient corporate earnings and renewed technology leadership helped markets look through ongoing geopolitical uncertainty.

The S&P 500 rebounded 10.42% over the month, driven by a recovery in technology and growth stocks after March’s sell-off. The rally was supported by renewed investor appetite for AI-related companies, resilient corporate earnings and a reversal of oversold positioning. Although lower yields helped sentiment early in the month, the later rise in Treasury yields suggests the rebound was driven more by earnings momentum and improved risk appetite than by rates alone.

The FTSE 100 gained 2%, supported by its defensive and commodity-linked composition. Energy majors such as BP and Shell benefited from firm oil prices, while healthcare and consumer staples provided resilience amid macro uncertainty. However, the index participated less in the global technology-led rebound than the US and Japan due to its lower technology weighting.

Japan’s Nikkei 225 rebounded 16.10%, recovering strongly from March’s losses. The move was led by technology, semiconductor and AI-linked stocks, supported by improved global risk appetite, reduced expectations of aggressive Bank of Japan tightening and a more supportive currency backdrop. Heavyweight technology names made a disproportionate contribution to the rebound.

The Australian All Ordinaries Index rose 2.35%, supported by strength in materials, gold and selected mining stocks as commodity prices remained elevated. Gains were more modest than in the US and Japan, reflecting Australia’s smaller technology weighting and ongoing domestic headwinds from higher interest rates, inflation pressures and cautious consumer sentiment. This gain was noted in the WA index, rising 2% on the back of the same sectors.

Download the list of WA’s top 100 listed companies, as of 30 April 2026, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

Gold: Gold prices were volatile in April 2026, rising from around US$4,679/oz at the start of the month to a mid-month closing high of approximately US$4,831/oz, an initial increase of around 3.2%. The early-month strength was supported by safe-haven demand linked to Middle East geopolitical risk, although gold remained caught between geopolitical support and macroeconomic headwinds from rising yields, a stronger US dollar and higher-for-longer interest rate expectations. Prices weakened later in the month, falling around 5.9% from the mid-month closing high to finish April at US$4,544/oz. Overall, gold ended April down approximately 2.9%, as the late-month decline more than offset the earlier safe-haven rally.

Lithium: Lithium pricing strengthened in April 2026, with spodumene concentrate pricing showing a stronger tone through the month. By late April, prices were quoted around US$2,435/t, up from US$2,043/t in March, indicating a materially stronger SC6 pricing environment heading into April. The improvement was supported by stronger lithium demand expectations from electric vehicles, battery energy storage and broader power infrastructure investment, as well as supply-side uncertainty, including Zimbabwe’s suspension of raw lithium and concentrate exports. Overall, April pointed to a firmer spodumene pricing environment, although downstream conversion margins remained a watch point as higher SC6 feedstock costs flowed through the lithium chemicals supply chain.

Nickel: Nickel was one of the standout commodity performers in April 2026, rising by roughly 12% over the month and reaching its highest level in nearly two years. LME nickel moved from approximately US$17,171/t at the start of April to around US$19,270/t by 27 April, with prices peaking near US$19,450/t later in the month. The move was driven mainly by nickel-specific supply and cost dynamics rather than broad metals strength. Key factors included tighter Indonesian ore availability, changes to Indonesia’s nickel ore benchmark pricing framework, and disruptions to sulphur supply, an important input for some nickel processing routes (particularly HPAL at Indonesian operations). These factors increased cost support and raised concerns about downstream production constraints, contributing to nickel’s outsized April gain.

Copper: Copper rose strongly in April 2026, reaching a new intra-month high before easing into month end but still closing higher overall. COMEX copper touched approximately US$6.12/lb on 22 April and finished the month at around US$5.91/lb on 30 April, equivalent to approximately US$13,026/t on an LME basis. The April gain was supported by supply-side concerns and processing-cost pressures rather than a clear acceleration in underlying consumption. In particular, tight copper concentrate availability, very low treatment charges, and elevated sulphur / sulphuric acid costs affected market sentiment, while Middle East-related logistics and energy risks added to volatility. The mid-month surge followed by a partial retracement suggests the market was pricing in a supply-risk premium, rather than responding solely to stronger demand expectations.

Performance of WA Index and Global indices

Top 20 performers of the month:

Liontown Limited (ASX: LTR): Liontown’s market capitalisation increased by 38.2% during April 2026, moving from 16th to 11th largest company in the WA Index. The increase was supported by a strong March quarter update, with Liontown reporting its strongest financial quarter since production commenced, including A$55 million of positive cash flow from operating activities and A$33 million of net cash flow. Operationally, Liontown achieved its 1.5Mtpa annualised underground run-rate at Kathleen Valley ahead of schedule, produced 96k dmt of spodumene concentrate, and sold 84k dmt across five parcels at an average grade of 5.1% Li₂O, with a realised price of US$1,845/dmt SC6e. The result reflected stronger spodumene pricing and improved operational momentum. Investor sentiment was further supported by the conversion of LG Energy Solution’s convertible notes, which removed A$482 million of liabilities from the balance sheet and left Liontown in a net cash position of A$61 million at 31 March 2026. In addition, Liontown announced early works and long-lead procurement for the planned Kathleen Valley expansion, including a 5.5MW ball mill, reinforcing confidence in the operation’s growth pathway and supporting the company’s strong April market performance.

Mineral Resources Ltd (ASX: MIN): Mineral Resources’ market capitalisation increased by 18.8% during April 2026. The increase was supported by MinRes’ balance sheet refinancing, with the company pricing / issuing US$1.3 billion of senior unsecured notes across two tranches to refinance higher-cost debt, repay the iron ore prepayment facility and redeem US$350 million of its existing 2028 notes. The refinancing is expected to reduce finance costs, lower the weighted average cost of debt from 8.4% to 7.4%, extend weighted average debt tenor from 3.1 years to 5.0 years, and leave the company with no material debt maturities until May 2030. Operationally, MinRes also released a positive Q3 FY26 update, upgrading FY26 volume guidance across Mining Services, Onslow Iron, Wodgina and Mt Marion. Stronger lithium market conditions supported a 92% quarter-on-quarter increase in the average realised spodumene price to US$2,105/dmt CIF SC6. Although cyclone disruption affected iron ore shipments and higher diesel prices are expected to impact June quarter costs, the market appeared to respond positively to MinRes’ improved liquidity, deleveraging progress, stronger lithium pricing and upgraded production outlook.

Greatland Resources Ltd (ASX: GGP): Greatland Resources’ market capitalisation increased by 17.9% during April 2026. The increase was supported by Greatland’s April production and quarterly activity updates, with the company reporting March quarter production of 82,723oz of gold and 4,128t of copper at AISC of A$2,056/oz, alongside sales of 97,800oz of gold and 4,620t of copper. Greatland also delivered a record quarterly cash build of A$260 million, increasing its closing cash balance to A$1.208 billion while remaining debt free. Investor sentiment was further supported by Greatland’s expectation that FY26 gold production would be around, or slightly above, the upper end of its 260,000–310,000oz guidance range, with AISC expected to trend toward the lower end of guidance. Although gold prices were volatile during April and the company continued to monitor potential Middle East-related cost and supply chain impacts, Greatland’s strong operating performance, debt-free balance sheet, full upside exposure to gold prices and continued Telfer / Havieron growth investment supported the positive market reaction.

The Top 100 performers of this month were:

Predictive Discovery Limited (ASX: PDI): Predictive Discovery’s market capitalisation rose strongly during March–April 2026, increasing from approximately $1,963.85 million to $4,525.71 million, a gain of about $2,561.86 million, or 130%. The re-rating was primarily driven by completion of the merger with Robex Resources, which created a larger West African gold production and development company combining PDI’s Bankan Gold Project with Robex’s operating and development assets, which was completed on the 15th of April, 2026. The merged group is targeting production of more than 400,000 ounces of gold per annum by 2029, subject to development and execution outcomes. Investor sentiment was also supported by the enlarged group’s improved scale, multi-asset profile and broader capital markets access, including PDI’s approval to list on the Toronto Stock Exchange. Overall, the transaction materially changed PDI’s profile from a single-asset developer to a larger West African gold platform, reducing perceived execution risk and supporting a substantial uplift in valuation.

European Lithium Limited (ASX: EUR): European Lithium recorded a significant increase in market capitalisation between March and April 2026, rising from approximately $354.27 million to $666.36 million, a gain of $312.09 million, or 88%. The primary catalyst was the late-April announcement that NASDAQ-listed Critical Metals Corp had signed a letter of intent to acquire European Lithium, subject to execution of a definitive agreement. Under the proposed all-scrip transaction, European Lithium shareholders would receive 0.035 Critical Metals shares for each European Lithium share held, implying a value of approximately A$0.58 per share and representing a significant premium to European Lithium’s prior trading levels. The proposal would simplify European Lithium’s existing look-through exposure to Critical Metals and support Critical Metals’ consolidation of 100% ownership of the Tanbreez Rare Earth Project in Greenland. The re-rating was also supported by the preceding trading halt, which was requested in response to media speculation regarding a potential control transaction. Overall, the proposed transaction improved investor sentiment by offering a clearer ownership structure, exposure to a NASDAQ-listed critical minerals platform and a potential reduction in structural valuation discounts.

Wildcat Resources Limited (ASX: WC8): Wildcat Resources experienced a notable increase in market capitalisation between March and April 2026, rising from approximately $508.80 million to $793.73 million, an uplift of 56%. The increase was driven primarily by continued exploration success at the Bolt Cutter Central lithium discovery, located around 10km west of the Tabba Tabba Project. On 7 April 2026, Wildcat reported that Bolt Cutter Central had extended to more than 2.3km, with drilling confirming a stacked pegmatite system that remained open in most directions. Reported intercepts included 9.4m @ 1.3% Li₂O, 8.1m @ 1.2% Li₂O, 8.1m @ 1.0% Li₂O and 7.6m @ 1.4% Li₂O, supporting confidence in both the scale and grade profile of the emerging system. The March quarterly activities report provided further support, noting that the Tabba Tabba Definitive Feasibility Study was well advanced and that Wildcat held A$43.3 million of cash at 31 March 2026. Together, these developments strengthened market confidence in Wildcat’s ability to expand its lithium resource base and progress its Pilbara development strategy, contributing to the valuation uplift over the period.

Featured articles