Bank of 2030: The future of investment banking

Transforming service delivery to generate differentiated insight and added value

Recent economic shifts have created significant challenges for the investment banking industry. This report explores how banks will need to adapt their operational frameworks to keep up with the evolving investment landscape and deliver the bank of the future.

Top takeaways

- Investment banks face significant challenges driven by COVID-19 impacts, evolving financial regulations, market democratisation, increased client sophistication, a shift to remote working arrangements, and rapid technology advances. There are opportunities for banks to drive toward higher levels of return; however, to achieve this, they likely will need to retool certain business models and operational platforms.

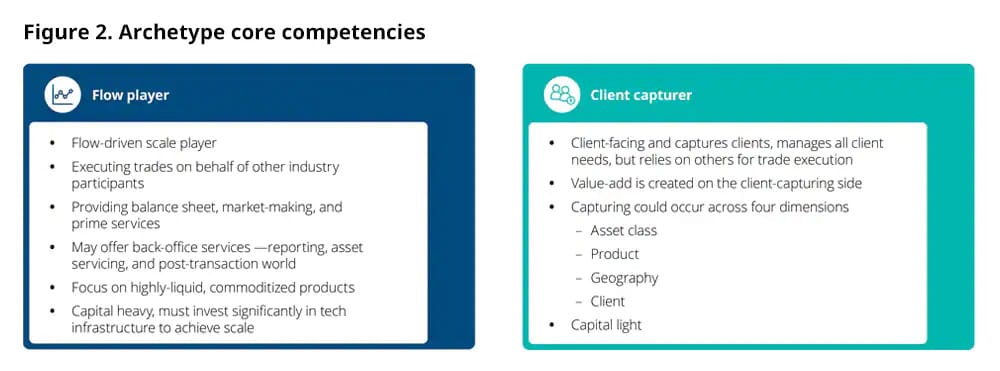

- The investment banking industry will likely undergo a bifurcation of broker archetypes: “flow players” that focus on middle- and back-office functions and “client capturers” that specialise in front-office functions. This bifurcation will result in an interconnected ecosystem of various players.

- Banks likely will need to determine which role they want and, depending on internal and external factors, are able to play within the ecosystem. They also will likely need to redesign their service delivery around a connected flow model—moving capacity and processes to the ecosystem of market providers—and optimise the use of financial technology, data, and analytics to generate differentiated insight and added value.

The changing investment banking landscape

The unprecedented public health, economic and societal impacts of the global COVID-19 (novel coronavirus) pandemic have intensified the forces that are creating challenges and accelerating disruption in the investment banking industry: falling equity prices, liquidity stress, evolving financial regulations, market democratisation, pricing pressure, increased client sophistication, shifts to remote working arrangements, and rapid technology advances.

Against this tough backdrop, we anticipate that investment banking will transition from a full-scale service model to a bifurcation of two broker archetypes: “client capturers” that specialise in front-office functions and “flow players” that focus primarily on middle-office functions (figure 1). These archetypes will likely operate within an interconnected, increasingly global—and, potentially, virtual—ecosystem that includes partners collaborations that provide various back-office functions.

Industry realignment should create opportunities for investment banks to drive toward higher levels of return. However, to deliver on this agenda, organisations can no longer tinker around the edges. It is likely that many will need to dramatically retool their current business models and operational platforms to prioritize client-centricity, disruptive technologies, regulatory recalibration, and workforce and workplace evolution. In addition, they should determine which archetype they want and are able to be within the new ecosystem.

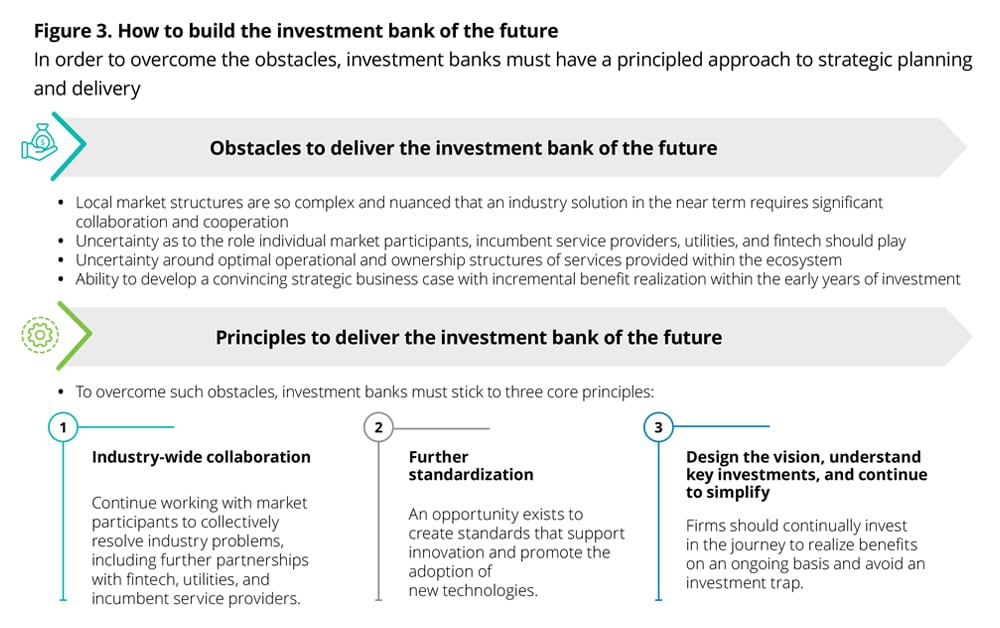

How to build the investment bank of the future

Are investment banks willing to rethink, rebuild, and rely on others to improve their future competitiveness? It may be difficult, costly, and time-consuming for some organisations to untangle their existing structures, develop and acquire digital technologies to better engage with customers, secure ecosystem partners (service providers), and harness and commercialise the combined power of internal and partner data. Yet the potential alternative is likely reduced market competitiveness and/or disintermediation.

To understand where to focus and drive change, banks should consider “zoom out” visualising the future beyond immediate constraints and “zoom in” to translate this vision to prioritised initiatives within a framework of principles that can help steer their journeys (figure 3).

Examples of initiatives to commence the journey include the following:

- Identify the utilities to either outsource or develop internal, bank-wide shared services functions (for example, for data management and Know Your Customer compliance).

- Consider the governance arrangements required for a utility-based model to be successful.

- Decide on industry-led standardisation and consider how it will affect the ecosystem.

- Consolidate operations processes and activities across asset classes (such as single post-trade processing).

- Centralise data management and invest in application programming interfaces to develop flexibility and create seamless connectivity.

- Consider using a scalable, cloud-based infrastructure to improve overall efficiency, achieve faster time to market, and reduce cost of ownership.

- Explore the art of the possible with emerging technologies such as AI, blockchain and advanced data analytics.

- Evaluate workforce and workplace practices through a post-pandemic lens and the shift from traditional, office-oriented employment to more flexible workspaces supported by technology innovations.

What’s ahead?

As long as considerable barriers to market entry remain in place (capital requirements, regulatory scrutiny, conduct risk and long-standing client relationships), investment banks are unlikely to have their market share challenged by digital disruptors or other non-industry competitors. However, investment banks looking to the future amidst shifting market dynamics should consider relinquishing expensive internal infrastructures and move toward a connected flow model where outside providers offer services for both critical and non-critical functions. In this new environment, the investment bank’s ability to create and harness differential insights from data becomes its new competitive advantage.

Bank of 2030: Transform boldly

The future of banking will look very different from today. Faced with changing consumer expectations, emerging technologies and new business models, banks will need to start putting strategies in place now to help them prepare for banking in 2030.

How can you drive bold transformation in your organization over the next 10 years?

Endnotes

1 In using the term “investment bank,” we refer to firms’ broker-dealer or “markets” business, not the advisory business.

{kind=link}

{kind=link}