Private capital could be the key to building a climate-resilient global economy

The world should invest in infrastructure that can withstand the effects of extreme weather. A Deloitte sustainability leader discusses how private capital can help pave the way.

As extreme weather becomes more prevalent,1 it’s expected to enact a heavy cost on emerging markets and developing economies, which can play a key role in global supply chains and can be disproportionately exposed to physical risks, environmental challenges, and economic fluctuations. Powerful storms and heavy rainfall could lead to damaged infrastructure and flooding, while heat waves and droughts could diminish agricultural yields, put stress on the electrical grid, and reduce workers’ productivity.2

According to the Independent High-Level Expert Group on Climate Finance, the global investment requirements for adaptation and mitigation efforts are estimated at approximately US$6.3 trillion to US$6.7 trillion annually by 2030.3

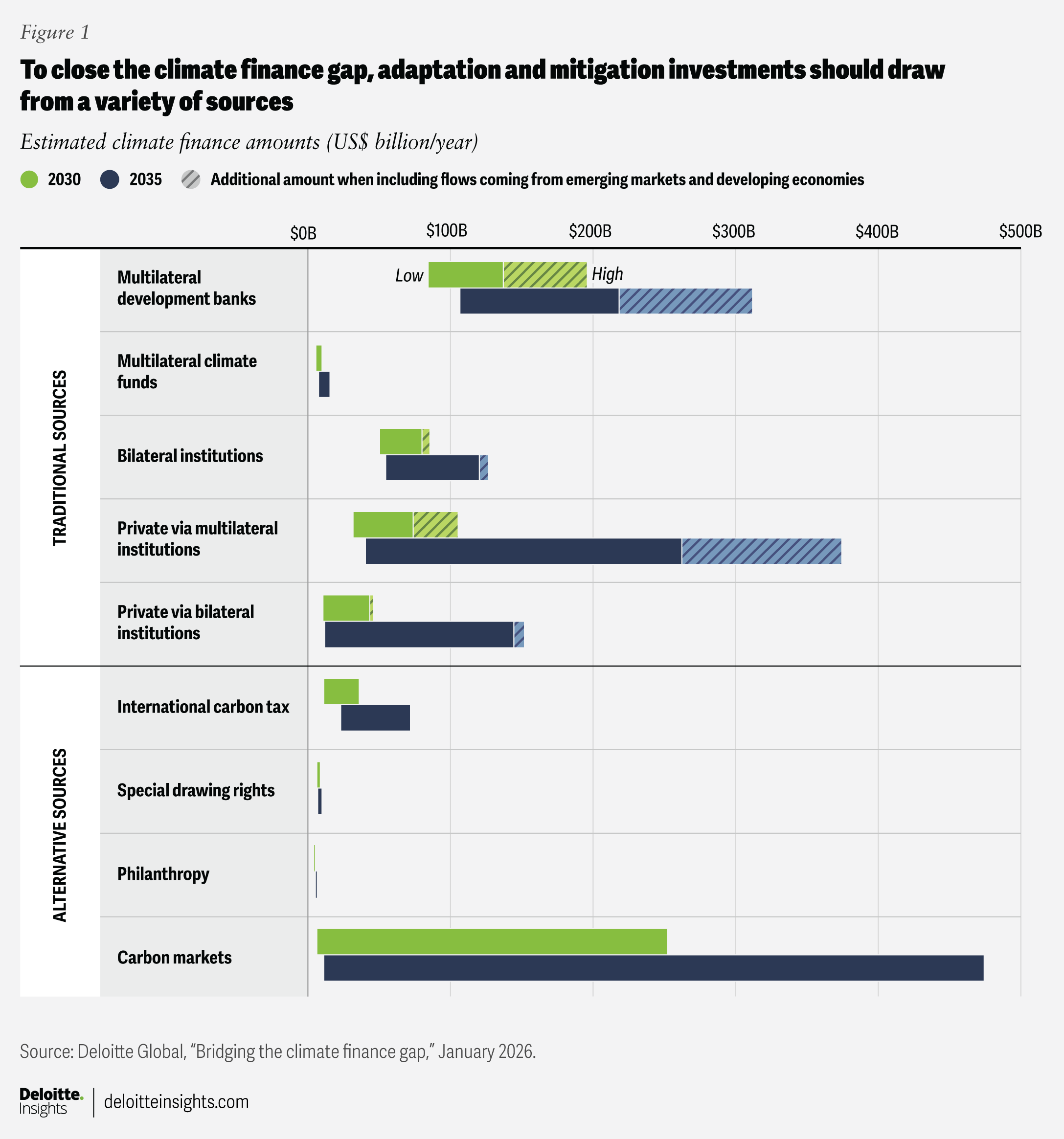

Deloitte Global recently published an economic analysis that outlines solutions for closing this funding gap, including new sources of investment, policy and regulatory conditions, and financial mechanisms (figure 1). In this interview, Frédérique Deau Blanchet, a co-author of the analysis and a partner at Deloitte France who works globally on sustainability initiatives with financial services organizations, explains how private capital and changes to public financing could help entice greater investment.

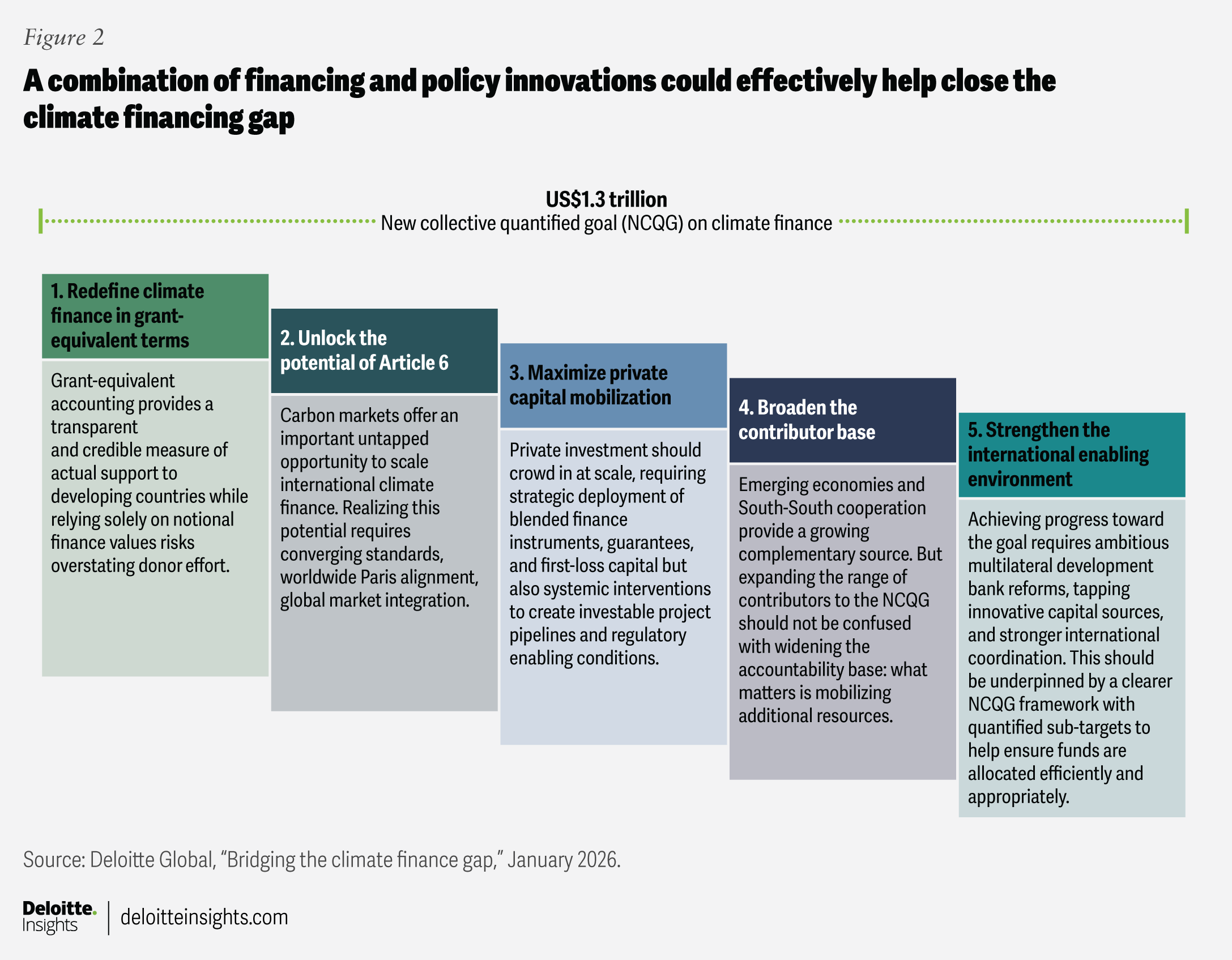

Q: The Conference of the Parties to the United Nations Framework Convention on Climate Change has pledged US$300 billion per year to mitigate and adapt to changing climate conditions,4 with the aim to mobilize US$1.3 trillion by 2035.5 Is that enough to meet the full scope of needs described?

A: It might not be. According to estimates by the Independent High-Level Expert Group on Climate Finance, emerging markets and developing economies—excluding China—could require approximately US$2.3 trillion to US$2.5 trillion annually by 2030 to change the way they consume energy, and to adapt to extreme weather.6 Of that, US$1.3 trillion needs to specifically come from external international sources. There is a need for a huge shift in capital—something that we’ve not seen at this level, at this scale before.7

The gap is especially pronounced in adaptation finance, which remains chronically underfunded compared with mitigation. While mitigation attracts capital due to clear revenue models for things like renewables, adaptation can offer simpler cost avoidance metrics that are harder to monetize.

“There is a need for a huge shift in capital—something that we’ve not seen at this level, at this scale before.”

One of the key levers the research points to is the need to focus on what’s often referred to as the “missing middle.” There is a US$135 billion to US$200 billion opportunity to help scale commercially viable solutions, such as clean energy infrastructure, climate-resilient systems, and adaptation technologies that fall between venture capital and private equity. Midsized funds that can write checks of US$10 million to US$40 million are well-placed to help close this gap.8

Despite the funding gap, the structural progress in capital deployment is evident. Private debt has surged to become the largest driver of climate finance, accounting for 34% of global flows in 2023 (up from a 23% average).9 Furthermore, private equity investment in sustainability solutions grew by 58% over the last 12 months,10 driven by megadeals in energy infrastructure. This indicates that where risk-return profiles are calibrated correctly, capital is moving at speed.11

Q: What changes are required to encourage more private investment?

A: One of the first shifts that should take place is perceptual. There is a historic perception that emerging markets and developing economies are high risk, leading to prohibitive costs of capital.12 However, the data suggests that default rates in developing economies are comparable to those in advanced economies.13

Deloitte Global’s analysis highlights that public finance can help change this perception and catalyze private investment through mechanisms that help mitigate risk, such as guarantees and first‑loss tranches.14 By absorbing risks that private capital is typically less able to bear, public financing can reduce the weighted average cost of capital by up to 25% for energy‑transition projects.15

There also may be a misunderstanding around the role of philanthropic capital (primarily nongovernmental capital) and concessional capital (public or publicly backed finance), which are not intended to generate market-rate returns.16 Rather, they often play a catalytic role in supporting early‑stage innovation and helping projects reach commercial viability.

Deloitte Global’s analysis indicates that philanthropic contributions to international climate finance toward emerging markets and developing economies could rise to as much as US$6.2 billion by 2035.17 In the context of infrastructure and other capital‑intensive investments, returns are typically characterized by stable, long‑term yields rather than high‑growth margins.

But reaching this level of investment would require reforms to the enabling environment and looking at ways to make the system more efficient, such as policy certainty, a transparent rule of law, and currency-hedging mechanisms. That’s why Deloitte Global’s analysis emphasizes that mobilization requires not just capital injections, but systemic interventions like regulatory frameworks and investable project pipelines. These strategies can help build investors’ trust, improve project bankability, and reduce perceived risk.

As an example, public finance has historically mobilized private capital at a ratio of roughly 0.2 to 0.4. This means that for every dollar invested by the public sector, the private sector invests US$0.20 to US$0.40. But to bridge this gap, the leverage needs to increase to around 1.2.18 This means for every US$1 of public capital invested, US$1.20 of private capital would be mobilized. This could transform climate finance from a budgetary challenge for governments to an investment class for pension funds and sovereign wealth funds.

Q: Are there other strategies in the analysis that could help reshape the climate-finance landscape?

A: Carbon markets are another potential solution that could be an important tool in closing this gap. It really depends on the convergence of international standards and price. There is a need for high-integrity emissions accounting and transparency so that institutional investors can see these assets as financial instruments and not reputational liabilities.19

If there’s an integration between global markets along with some of the measures we’ve spoken about, then the estimates show that carbon markets could contribute up to US$472 billion in 2035. There are already asset managers and investment companies today who are embedding some carbon market mechanisms into some of their investment products. It should be well-controlled. But with the right reforms, carbon markets could effectively change the game.

Q: Emerging economies have highly valued natural resources, and with the advent of BRICS,20 they are also gaining global economic power. Are there opportunities for these countries to invest in one another?

A: Yes, south-to-south capital is increasingly important because they [emerging markets and developing economies] usually understand the specific development context better. The estimates outlined in this research show that emerging economies could contribute as much as US$218 billion annually by the 2030s, which confirms that emerging markets are maturing to the point where they could effectively leverage private-sector balance sheets for the public good.

Q: If the financial returns on resiliency investments tend to be more modest, what are some of the benefits to investors? Or are the benefits implicit in the risks of not doing so?

A: Infrastructure is a big part of building resilience, given its long-term nature and essential role in the economy. Increasingly, sustainability-ready and forward-looking infrastructure is being designed to better withstand extreme weather and recover more quickly, which helps strengthen its resilience over time.

We’re talking about creating infrastructure that can help economies move from carbon-intensive economies to low-carbon economies. We’re talking about renewables. We’re talking about the new data centers that are emerging due to the very high demand in terms of energy for AI, for example. We’re talking about electrification. How can we make sure that the required financing is channeled to electrify or improve the distribution of electricity in some countries, or get electricity throughout some countries—as simple as that, sometimes—in the Global South? Another challenge is how to adapt roads that can withstand the increase in temperature? There’s also a need to build flood barriers or seawalls to help address urban flooding and sea-level rise. If you are on the coastline or close to a river, new infrastructure will likely be required to protect the people and buildings from rising water levels.

If these needs are not addressed due to the climate finance gap, it could limit the ability to support effective mitigation and adaptation in emerging markets and developing economies. For global investors, this shortfall represents broader economic and transition-related risks. The Global South is also important to the energy transition, and global sustainability goals may not be met without financing a low-carbon development pathway in these economies, making action in the Global South a regional priority and of global importance.21

Continue the conversation

Meet the industry leaders

Michelle Varney

Freedom-Kai Phillips

by

Frederique Deau Blanchet

Freedom-Kai Phillips

The authors would like to thank Blythe Aronowitz, Ashish Gupta, and Annalyn Kurtz for their contributions to this article.

Editorial (including production and copyediting): Elizabeth Ryan, Annalyn Kurtz, Preetha Devan, and Anu Augustine

Design: Molly Piersol and Harry Wedel

Audience development: Kelly Cherry

Cover image by: Alexis Werbeck

Knowledge services: Vanapalli Viswa Teja