Streaming video at a crossroads: Redesign yesterday’s models or reinvent for tomorrow?

With 36% of Americans surveyed believing content on SVOD isn’t worth the money, providers shouldn’t assume that advertising, bundles, and contracts are enough to help their business.

Kevin Westcott

Jana Arbanas

Chris Arkenberg

Jeff Loucks

In the past few years, leading TV and movie companies have responded to the disruption of streaming video by launching their own streaming services. To attract subscribers, they invested more in content for their services—and sold it to subscribers for less than what they charged consumers for pay TV and theatrical releases.1 This strategy, combined with minimal friction for consumers to cancel streaming subscriptions, has led to underperforming services.2 Now, in hopes of making their streaming video on demand (SVOD) services profitable, they’re trying to rebuild pay TV business models like advertising, contracts, and bundling. But is this path enough to meet the larger changes in media and entertainment that have toppled the dominance of TV and movies?

For SVOD providers, acquiring customers, reducing SVOD churn, and deepening retention on their services are still some of the most important challenges. Costs of acquiring subscribers are high, and the costs of reacquiring subscribers that have already churned can be even higher.3 In the competitive and fragmented environment of modern media, delivering engaging TV and films may not be enough to meet these challenges.

This year’s Digital Media Trends study further underlines how the once-distinct categories of media and entertainment continue to converge and interconnect, while audiences are becoming more fragmented and specialized. The value that consumers expect from digital media and entertainment is being increasingly shaped by their experiences with social media and gaming. This is a generational shift, as shown by our study. However, given that the eldest millennials are headed into their forties in 2024, it’s no longer merely “younger generations” who are giving their time equally to TV and movies, social media and user-generated content, and immersive and social gaming.

It’s in this broader environment that SVOD providers should consider competing for attention and engagement—and working hard to better monetize their intellectual property. How should their services evolve to reinforce content discovery and unlock monetization opportunities? How should SVOD providers use social media, gaming, and fandoms to help drive acquisition and retention for their services? If they focus too much on rebuilding the past of pay TV, SVOD providers may miss out on the opportunity to reimagine the streaming video experience and define a more compelling and enduring tomorrow.

US consumers may be reaching their limits on SVOD price hikes

This year’s Digital Media Trends shows that US households are spending more on streaming video subscriptions, but they may be reaching their limits. On average, US subscribing households spend US$61 per month on four SVOD services. Additionally, 68% of consumers surveyed pay for either a TV subscription or live streaming TV to not only access content not available on streaming video, but also streamline billing for both broadband and TV and access SVOD through their pay TV service. For many US households, it may be getting more expensive to watch TV and films at home.

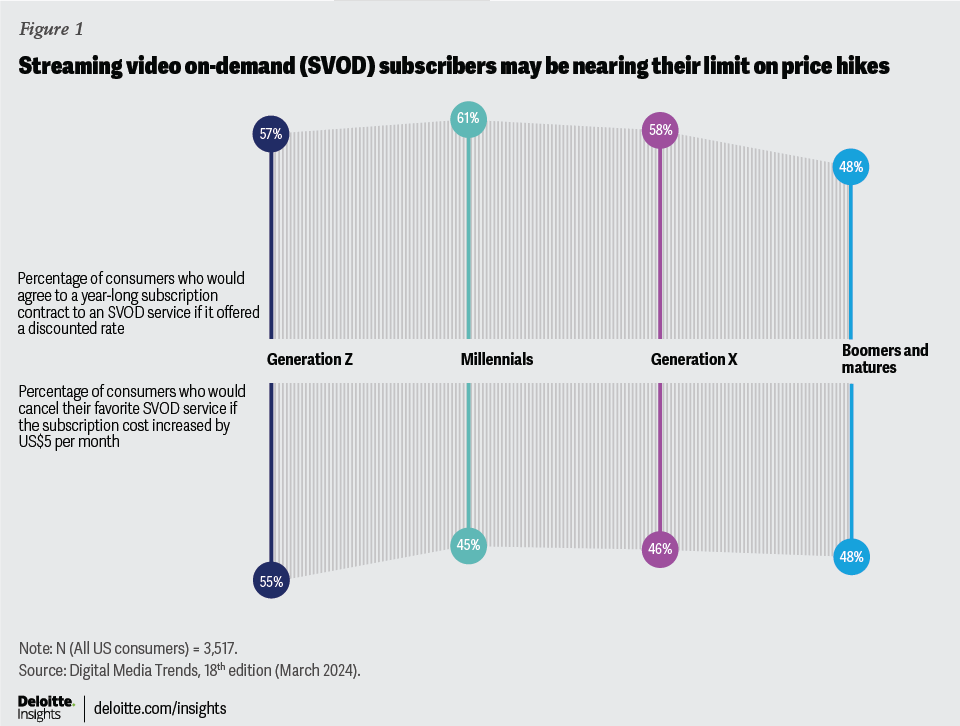

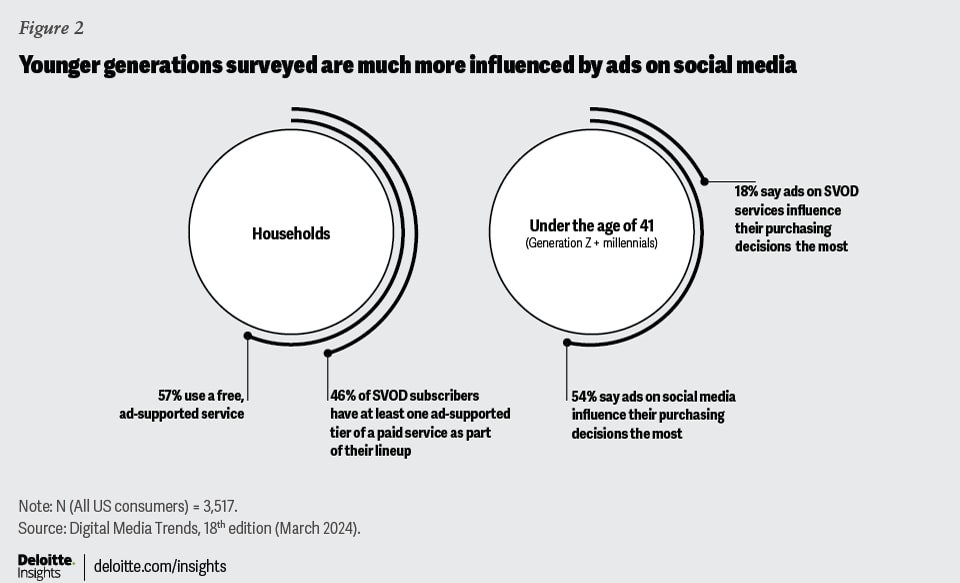

Cheaper, ad-supported tiers may offer some relief for SVOD subscribers: Around 46% of households subscribe to at least one ad-supported tier of a paid service as part of their lineup, and 57% use a free, ad-supported service. The overall percentage of respondents who have cancelled any paid SVOD service in the past six months has softened a bit, to 40% from 44% last year. This suggests that tiering and even bundling may be helping with retention, though churn remains considerably higher for younger generations—around 53% for Gen Zs and millennials surveyed, who also subscribe to and pay for more services. Over half of US consumers say they would agree to a year-long SVOD subscription if it offered a discounted rate.

{kind=link}

However, SVOD providers may still need to work hard to show their value: Thirty-six percent of consumers across generations surveyed say that the content available on streaming video services isn’t worth the price. This suggests that subscription price hikes may be approaching their peak: Forty-eight percent say they would cancel their favorite paid SVOD service if monthly prices went up by US$5. For US consumers surveyed, price is still the dominant factor in how they value a paid SVOD subscription.

Is commercial advertising the right bet for SVOD providers?

To help enable more affordable subscription tiers, SVOD providers are working to unlock advertising revenues. There’s a bit of a gambit here: Cheaper, ad-supported tiers can lower subscription revenues while putting more weight on ad revenues, which, in turn, requires streamers to show more value to advertisers. This may put them in competition for ad budgets that advertisers increasingly spend on more targeted social media campaigns.4 Providers may hope that migrating audiences from pay TV onto ad-supported streaming services could rebuild the historic profitability of pay TV. This hope, however, may be based more on past successes than on modern media and entertainment behaviors.

{kind=link}

People aren’t being moved by the kinds of commercial advertising typical to TV and streaming video, especially younger generations: Eighteen percent of those surveyed under 41 years old say ads on SVOD services influence their purchasing decisions, compared to 54% who say ads on social media influence their purchasing decision the most. Part of this is that ads on streaming services tend to be repetitive and not relevant to specific viewers.5 Younger generations are also savvier to persuasion and are more inclined to trust creators and influencers on social media than brand advertisements. Based on how they allocate their ad dollars, advertisers and agencies seem to understand this reality—but do SVOD providers?

In their hopes to retain subscribers with lower prices, SVOD providers are taking on a new kind of customer: advertisers. Will SVOD providers be able to show enough value to advertisers? Maybe. But they may need to build stronger relationships with agencies and better ways to measure impressions and conversions. They will likely have to invest more in modeling and matching algorithms. Still, many SVOD providers don’t have the audience size to drive the same economics for advertisers that pay TV has.6

People expect customization and personalization

SVOD providers may want to rebuild pay TV, but do consumers? US consumers may be willing to endure more ads and be corralled into bundles, but they may not be willing to give up the degree of customization they gained from unbundling pay TV, or the personalization they enjoy from social media.7

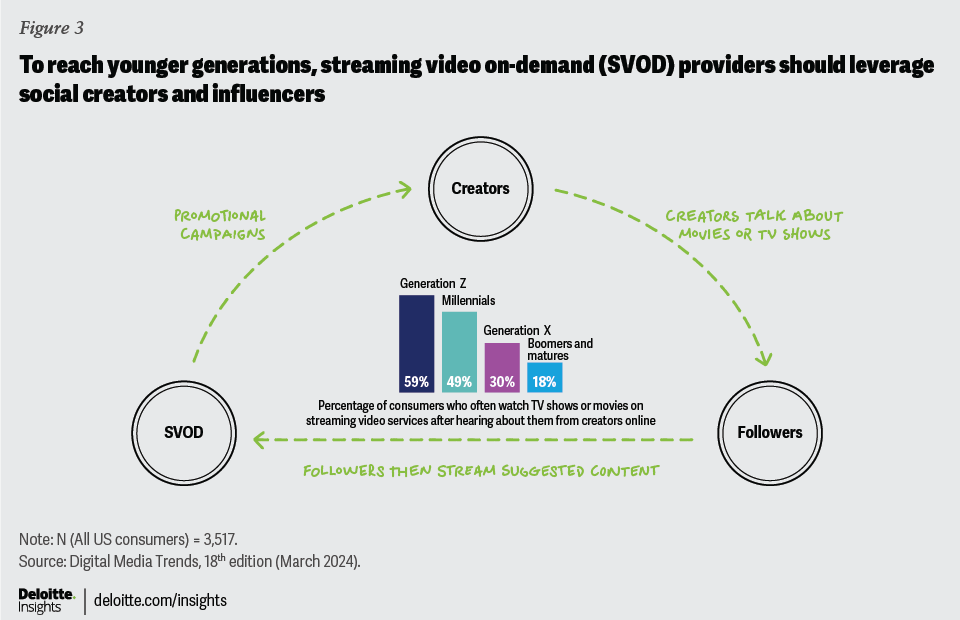

This highlights the competitive challenges that streamers face from social video services whose very DNA is data-driven and algorithmic. Social media users—billions of us, it should be noted—can select the accounts they follow à la carte, and these selections inform the algorithms that recommend related accounts and content. SVOD providers have been challenged to show similar capabilities. Deloitte’s study found that a full 60% of Gen Zs surveyed prefer watching user-generated content videos because they don’t have to spend time searching for what to watch, and 54% of Gen Zs and millennials believe they get better recommendations for TV shows and movies to watch from social media than from streaming video services.

It’s a reminder that those surveyed under 41 years old prefer social media videos to any other form of video content, and why so many ad dollars flow to social media. With the arrival of generative AI content creation tools in social media services, the volume of competitive content—and its quality—could rise dramatically.8 It should also be a reminder to SVOD providers and TV and film studios that engineering discovery and buzz for their offerings requires more than just targeted recommendations on their services. To reach the masses, many of whom may spend more of their entertainment time on social media services, SVOD providers should also have a strong social media strategy. This may be critical to customer acquisition and retention of existing subscribers.

{kind=link}

Disruption of media and entertainment is the new normal

This data may be sobering to SVOD providers, but it can offer a path forward, albeit a costly one. People want more choice over what they see, better content recommendations from services, and innovations in advertising. Almost 50% of respondents say they would spend more time on streaming video services if it was easier to find content, and around 75% of Gen Zs and millennials would like a bundle that lets them search for content across all their streaming video services. Forty-two percent of consumers surveyed would be willing to watch ads on SVOD if they were more personalized to their interests. Nearly 40% of those surveyed under 41 years old would like the ability to click on the advertisements they watch on SVOD to get more info about a product and have the option to purchase it directly.9 Recent advances in generative AI for visual recognition could make it easier for audiences to quickly identify goods on the screen, but so far, this opportunity is being captured by mobile devices, not SVOD providers.10

This points to yet another likely revolution ahead for digital and streaming TV: getting the right content and products in front of the right eyes, with an interface that makes it simple to quickly identify and purchase embedded content and products. Streaming providers—and all media and entertainment companies—could learn from social media and content creators.

The biggest challenge for SVOD providers and studios may be philosophical: They no longer address a mass culture, but rather a fragmented landscape of competing digital entertainment options. Trying to rebuild pay TV business models around streaming services could help reduce SVOD churn and slow attrition in the near term, but the long game for success will likely involve reinventing the medium to be more personalized, more shoppable, and more social. Providers will also likely need to widen their scope beyond TV and films to reach modern audiences and make their intellectual property work across social and video games. The industry has had 20 years to understand the size and shape of the streaming disruption. Now they should come together to work to build something truly contemporary.

Key takeaways

- People will likely balance costs and content with ad-supported tiers, contracts, and more bundles, but these may be short-term solutions to preserving profitability. Social media and unbundling pay TV have trained consumers to expect more customized and personalized content and advertising. These are levers to build greater consumer engagement and value. For example, around half of consumers surveyed would spend more time on SVOD services if content discovery was easier.

- SVOD providers should see social media as a model for delivering engaging content to users and enduring value to advertisers. SVOD providers should also see social media as the nexus of discovery and buzz to drive support for their own content offerings.

- The TV and film industry should consider that going direct-to-consumer with SVOD services demands more than just repackaging the pay TV experience. SVOD providers now operate in a very different world, and how consumers value media and entertainment has evolved.

Methodology

These insights are based on an online survey of 3,517 US consumers that was conducted in October 2023. Throughout this report, we reference generations. Our generational definitions are as follows: Generation Z (1997-2010), millennial (1983-1996), Generation X (1966-1982), boomers (1947-1965), and matures (1946 and prior). The survey was fielded by an independent research firm and all data is weighted back to the most recent Census to give a representative view of US consumers.

By

Kevin Westcott

Jana Arbanas

Chris Arkenberg

Jeff Loucks

The authors would like to thank Akash Rawat for his work in analyzing survey data and highlighting insights, as well as his contributions to shaping the direction of the overall study. They would also like to thank Sathiya S. and Ankit Dhameja for their contributions to survey development and secondary research support, and Gautham Dutt for his design and visualization support. The authors would like to recognize Andy Bayiates and Molly Piersol for their partnership, along with their editorial and design contributions. The authors also want to sincerely thank Kevin Downs and Amy Booth for their support and guidance throughout the process.

Data science and survey advisory by: David Levin

Cover image by: Manya Kuzemchenko

Visit the Deloitte Center for Technology, Media & Telecommunications

Access more insights for the technology, media, and entertainment; semiconductor; telecommunication; and sports sectors.