2026 Power and Utilities Industry Outlook

Utilities are under pressure to meet the energy demands of the AI economy while maintaining affordability. Deloitte explores strategies that can help the industry transform faster and build resilience.

After decades of modest growth, US electricity demand began accelerating in 2025, surpassing expectations in many utility plans. The surge was driven by artificial intelligence training workloads, alongside electrification in transportation and industry. According to Deloitte analysis, peak demand is projected to grow by approximately 26% by 2035, testing today’s grid limits.1

Data center demand alone could reach 176 gigawatts by 2035, a fivefold jump from 2024.2 Industrial electrification could add 25 GW of demand by 2030, on top of growth in household and commercial consumption.3

At the same time, new supply is not coming online fast enough. The energy mix is shifting toward renewables, which accounted for 93% of new capacity through July 2025, with solar and storage making up 83%.4 But the pace of connecting these new energy sources has lagged. Two terawatts of capacity are stuck in interconnection queues, almost twice the currently installed capacity.5

Reliability pressures are also mounting. In the first half of 2025, the United States experienced 15 natural disasters, each causing US$1 billion or more in damages. At least three of those events exceeded US$5 billion in losses.6

In 2026, the challenge for utilities will be quickly delivering uninterrupted or “firm” capacity to stressed parts of the grid.7 Customer affordability will remain a central pressure point as retail prices continue to rise. The average residential retail price is projected to be approximately 4.5% higher in 2025 compared to 2024.8 The passage of the 2025 reconciliation bill—commonly known as the One Big Beautiful Bill Act—rolled back many clean energy incentives, expanded foreign entity of concern restrictions, and narrowed safe-harbor provisions.9 These changes compress developer timelines and increase compliance needs.10

To address these challenges, Deloitte’s 2026 Power and Utilities Industry Outlook explores the strategies utilities can use to respond:

- Reliable growth: Deliver firm capacity for rising demand

- Demand integration: Leverage hyperscale data centers as grid partners

- Smarter systems: Integrate analytics and AI to optimize efficiency

- Supply chain resilience: Ensure resilience through reshoring and diversification

- Capital innovation: Unlock flexible financing to scale affordably

{kind=link}

1. Reliable growth: Deliver firm capacity for rising demand

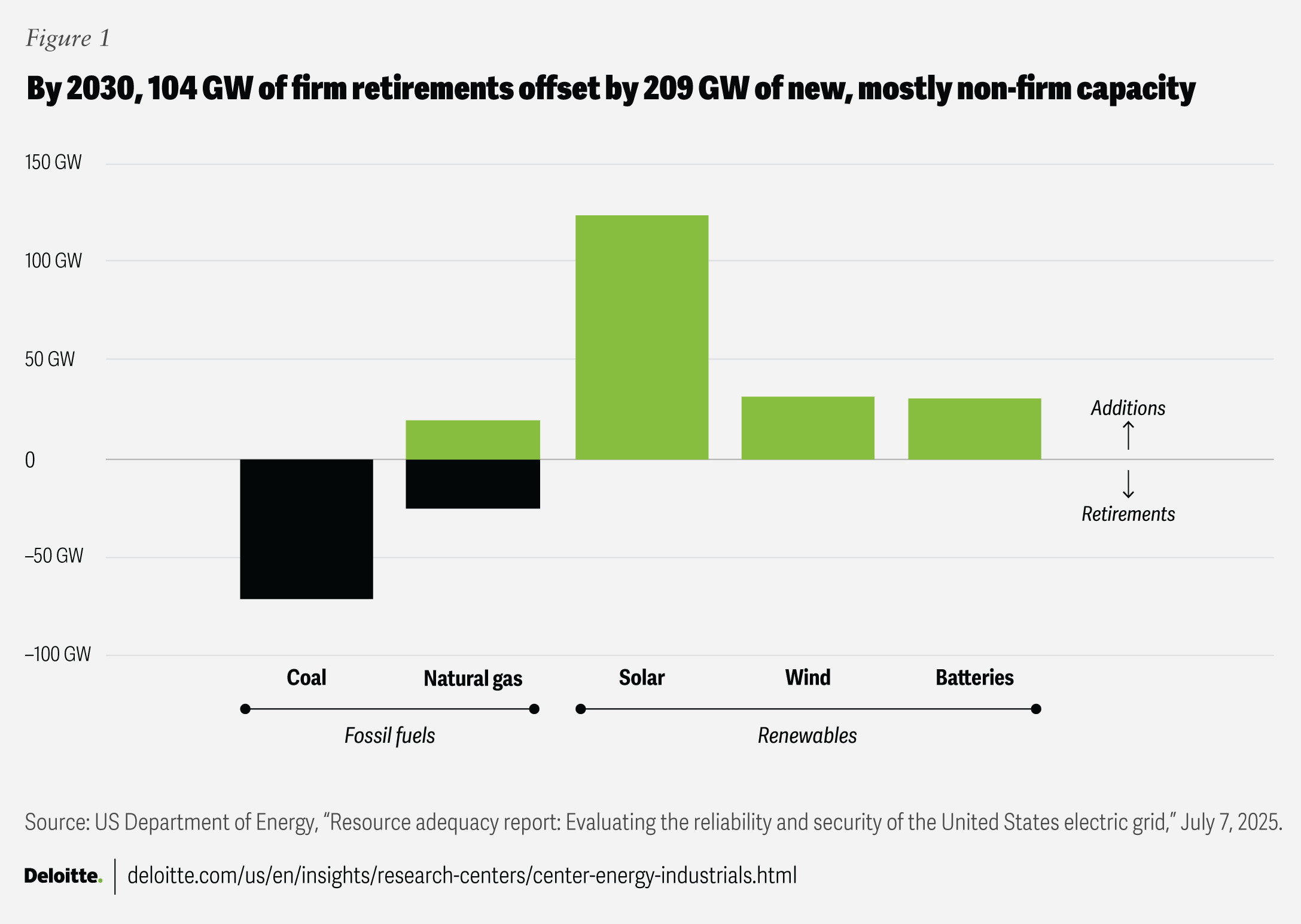

In 2025, rising load forecasts and shrinking capacity margins prompted utilities and regulators to emphasize near-term reliability alongside long-term planning. The US Department of Energy projects about 104 GW of coal and natural gas retirements by 2030, offset by 209 GW of new capacity.11 Yet only 10% of those additions will be firm baseload, widening the reliability gap (figure 1).12

{kind=link}

Electric power companies are pursuing strategies across three horizons, focusing on accredited peak contribution rather than nameplate megawatts.13

In the near term, companies are bridging reliability gaps through incremental firm generation and operational flexibility. Natural gas remains the backbone for firm load, with nearly 19 GW of gas-powered capacity planned through 2028.14 Utilities are extending the lives of coal plants, running natural gas “peaker units” for more hours during periods of high demand, and increasing the capacity of existing nuclear plants.15

The emphasis will then shift to storage duration and diversity, with long-duration energy storage (LDES) advancing from pilots to procurement. At least two states now have LDES requirements totaling more than 2.75 GW.16 Utilities are also procuring 8-to-10-hour storage to address reliability gaps during high-demand seasons and reduce unused renewable energy generation.17 While this can relieve peak stress, it is not a one-for-one substitute for firm generation like gas or nuclear. Utilities are also expanding demand response and flexible loads, turning them from emergency tools into dependable capacity during peaks.

Nuclear is regaining traction as a long-term anchor for clean, firm capacity. The One Big Beautiful Bill Act preserves the 45U credit for existing plants and maintains eligibility for advanced nuclear under 45Y and 48E if they meet “domestic content” and “construction start” requirements.18 This strengthens the economics for existing fleets and builds momentum for plant expansion and new builds.19 Recent milestones include federal funding of US$900 million for advanced reactors being made available, new design approvals, and the first US utility application for a small, modular reactor construction permit.20 The administration’s goal is to quadruple US nuclear capacity to 400 GW by 2050, including siting plans at military installations and AI data center hubs.21

Planning and procurement are also adapting. As utilities pursue these strategies, they aim to procure all resource types while prioritizing deliverability, project readiness, and portfolio resilience.22 Some state commissions are expanding integrated resource planning tools to allow procurement between planning cycles when demand or transmission timing shifts.23

In 2026, utilities will continue to shift from planning to execution. They will face growing pressure to keep firm capacity projects on schedule, reduce curtailment, and lower costs.

2. Demand integration: Leverage hyperscale data centers as grid partners

In 2025, US data centers emerged as one of the fastest-growing sources of electricity demand. Once viewed as inflexible mega-loads, hyperscalers are now potential operational partners.24

Data centers can support reliability in three ways. First, AI-enabled orchestration platforms can shift workloads across regions in real time, aligning demand with renewable oversupply.25 Second, advanced power electronics allow data centers to instantly respond to grid fluctuations, functioning like batteries.26 Fewer than 5% of facilities currently participate in demand-response programs, but pilots show that between 10% and 30% of load can be flexed during peak events without disruptions.27 Third, advances in workload control and real-time telemetry enable millisecond-level responses, allowing data centers to support fast-reserve markets by flexing load when the grid is constrained.28 Together, these capabilities mean that hyperscalers can function like hybrid assets—both consuming power and providing reliability services.

Some utilities and regulators now require hyperscalers to share costs, provide telemetry, and demonstrate flexibility for faster interconnection.

- In Indiana, rate-case settlements require hyperscalers to pay for grid upgrades, while Oregon has passed legislation creating a separate rate class for large data centers.29

- The Electric Reliability Council of Texas (ERCOT) now requires large-load projects to align approvals to ramp-up plans and telemetry.30 They are also establishing dynamic tariffs and demand-response models that could expose large flexible loads, including hyperscalers to granular price signals.31

- PJM Interconnection’s fast-track interconnection requests favor shovel-ready projects to support near-term reliability.32

- The Midcontinent Independent System Operator (MISO) is piloting demand-flexibility reforms, tightening baselines and telemetry to test how reliably data centers can curtail load.33

Early results are promising. One hyperscaler, for example, has embedded PJM grid telemetry into its scheduling systems and partnered with two utilities to reduce AI processing workloads during periods of grid stress.34

In 2026, performance-based interconnection could increasingly tie queue priority to telemetry and flexibility. Resource adequacy rules are expected to start recognizing flexible load paired with four-hour batteries as a dependable capacity resource. Dynamic tariffs are likely to spread, exposing hyperscalers to real-time signals.

3. Smarter systems: Integrate analytics and AI to optimize efficiency

Utilities are under pressure to deliver more reliability with the same resources. That requires analytics and automation to drive capital and operational efficiency—creating the foundation to scale their AI deployment. Enterprise-scale adoption is being driven by two converging forces:

- Energy for AI as utilities plan for rising data center load

- AI for energy as intelligence is embedded to optimize the grid

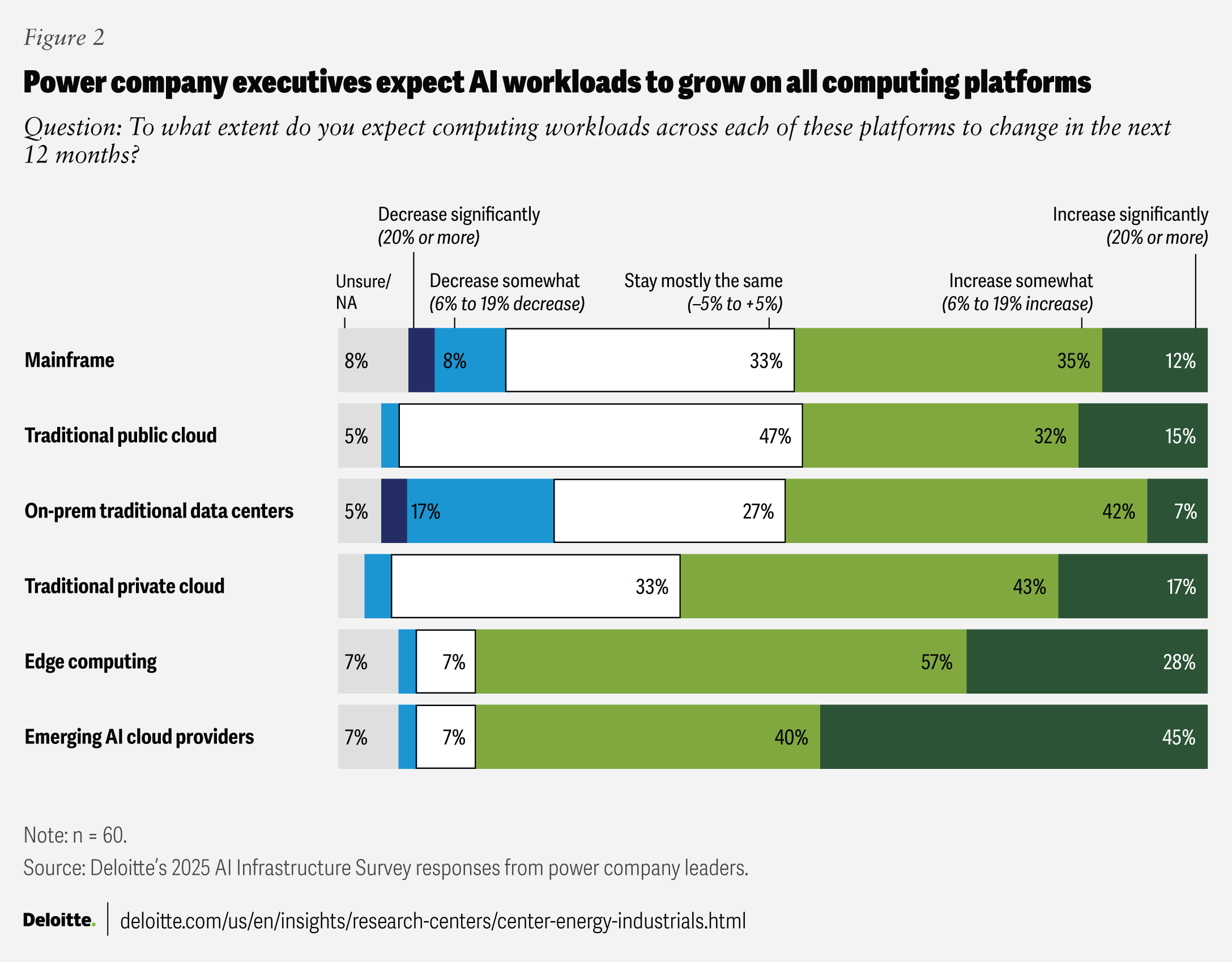

Power companies are building computing infrastructure that blends edge, cloud, and on-premises capabilities (figure 2).35 Edge AI—from drones to substation sensors—enables millisecond-level decisions. Some AI models are deployed on-premises to handle critical functions that cannot be moved outside of secure environments. Additionally, utilities are exploring federated learning techniques to improve models across sites while keeping data local, offering a secure path to expand system intelligence.36 Together, this infrastructure can help balance resilience, compliance, and scalability for enterprise adoption.

{kind=link}

AI applications are driving efficiencies across the utility value chain.

- In grid operations, it can augment traditional predictive maintenance to help utilities prioritize work, reduce failures, improve crew productivity, enable proactive wildfire detection, and ensure faster outage restoration.37 By 2027, it’s expected that nearly 40% of utility control rooms will use AI.38

- For the workforce, gen AI copilots trained on manuals and incident logs can guide technicians in real time, boosting first-time fix rates, while edge-enabled drones and field sensors shorten inspection cycles.39

- At the grid edge, embedded intelligence could enable millisecond-level control of events, voltage, and distributed energy resources, allowing feeders and microgrids to self-adjust in real time under operator oversight.40

- Within the enterprise, AI could support streamlining compliance, finance, and customer service by automating repetitive tasks and increasing transparency.41

As AI adoption broadens, utilities should explore strengthening governance, cybersecurity, and cost-recovery frameworks. Human oversight (human-in-the-loop) is essential to ensure strong governance. The North American Electric Reliability Corporation (NERC) guidance emphasizes that AI should serve as a decision-support tool rather than an autonomous controller.42 In line with this, the industry is beginning to put safeguards in place—such as model registries, audit trails, and risk controls.

Cybersecurity standards remain uneven. However, initiatives like the National Association of Regulatory Utility Commissioners distributed energy resources security baselines and the Electric Power Research Institute’s Open Power AI Consortium are creating reference points for validation and digital trust.43

Many cost-recovery frameworks are also underdeveloped. With no standardized AI-specific approaches, utilities often lean on cloud and software-as-a-service precedents,44 while some regulators pilot approaches such as trackers and riders.45

In 2026, utilities are likely to expand AI-assisted analytics in control rooms, widen adoption of gen AI copilots across operations, and formalize oversight frameworks—with human oversight remaining central.

4. Supply chain resilience: Ensure resilience through reshoring and diversification

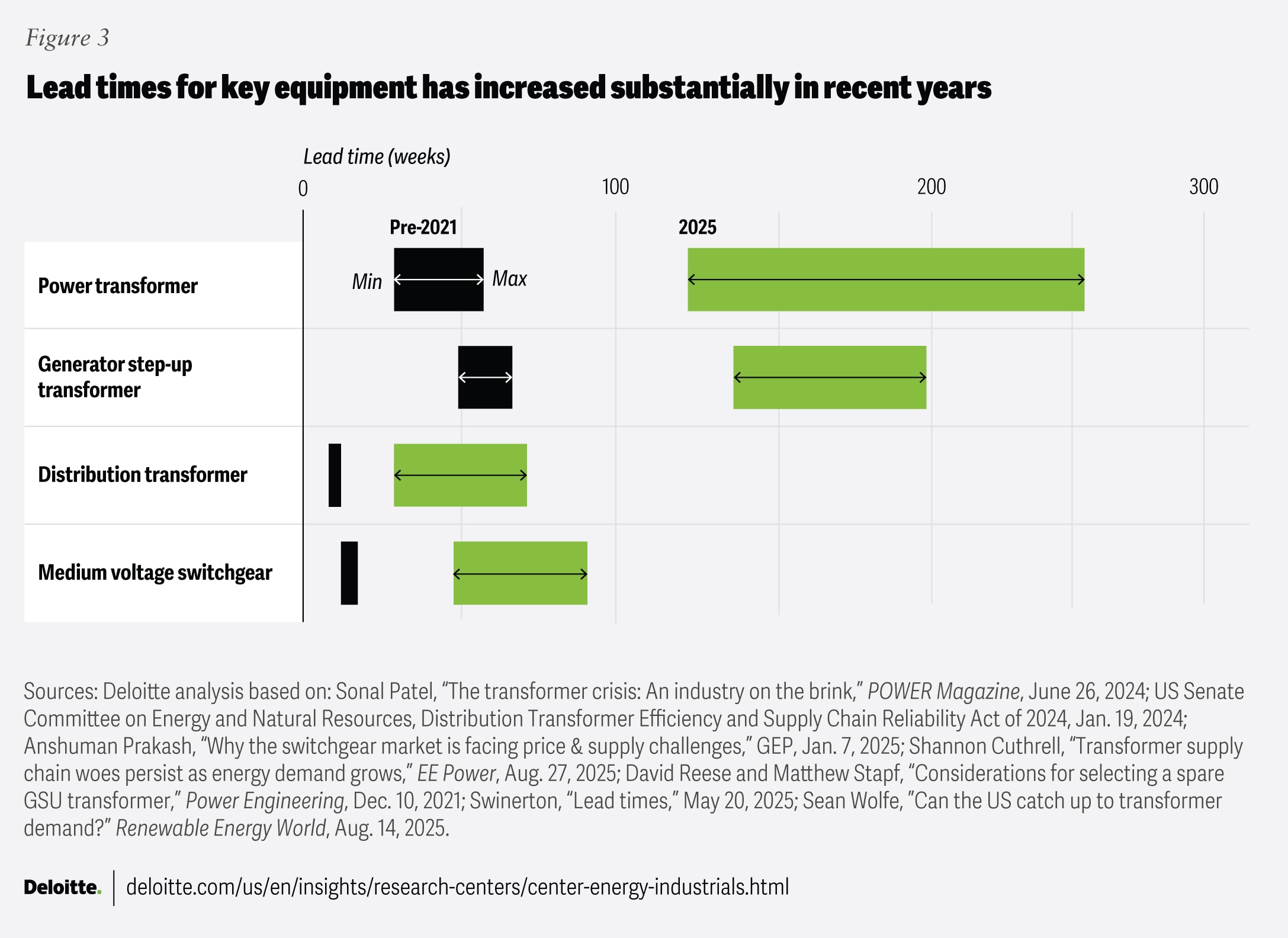

Over the past few years, lead times for critical grid equipment such as transformers and switchgear have stretched to multiple years (figure 3), while equipment and project costs continue to rise. The cost of a new gas-fired power plant has surged to more than two and a half times that of projects built just a few years ago.46

New tariffs may also affect lead times and costs. These include tariffs on steel (including grain-oriented electrical steel) and aluminum, and certain copper products, in addition to expanding probes into solar, wind, and battery supply chains.47 The recent tightening of domestic content and sourcing requirements further adds complexity.

{kind=link}

In response to this broad set of challenges, the industry is pursuing three main strategies:

- Reshoring, diversification, and reservations: Suppliers are expanding US production capacity to shorten lead times and localize critical equipment supply.48 To reduce dependence on single vendors, utility leadership boards are pushing for supplier diversification through dual-sourcing strategies and multi-award contracts.49 At the same time, utilities are reserving production slots years in advance, securing critical equipment before supply tightens further.50

- Deploying grid-enhancing technologies (GETs): Alongside reshaping supply, utilities are considering GETs and flexible loads to unlock near-term capacity and defer capital builds. While GETs carry their own supply risks, they can be deployed faster than decade-long 500-kV projects. Utilities are embedding GETs into integrated resource plans, supported by FERC Order No. 1920.51 By mid-2025, at least 14 states had enacted legislation and another nine were considering measures requiring utilities to evaluate GETs or advanced transmission in planning or investment filings.52

- Leveraging sandboxes to accelerate modular innovation: Regulatory sandbox programs are helping deploy modular substations, mobile transformers, and spares under accelerated oversight.53 About a dozen states are piloting frameworks that allow utilities to test new technologies, cutting review times from years to months.54 For example, Connecticut vets grid transformation proposals within 18 months.55

In 2026, supply resilience is becoming part of core reliability planning. Utilities are expected to integrate multi-year, multi-vendor supply agreements, embed grid-enhancing technologies, and use digital tools to track supplier and inventory risks in real time.

5. Capital innovation: Unlock flexible financing to scale affordably

The US electric power sector faces record capital needs—more than US$1.4 trillion through 2030—even as affordability pressures intensify.56 Traditional equity and debt financing are no longer sufficient amid growing concerns about rising prices for customers.57 In response, utilities are reshaping portfolios and capital flows through mergers and acquisitions and portfolio rotation.

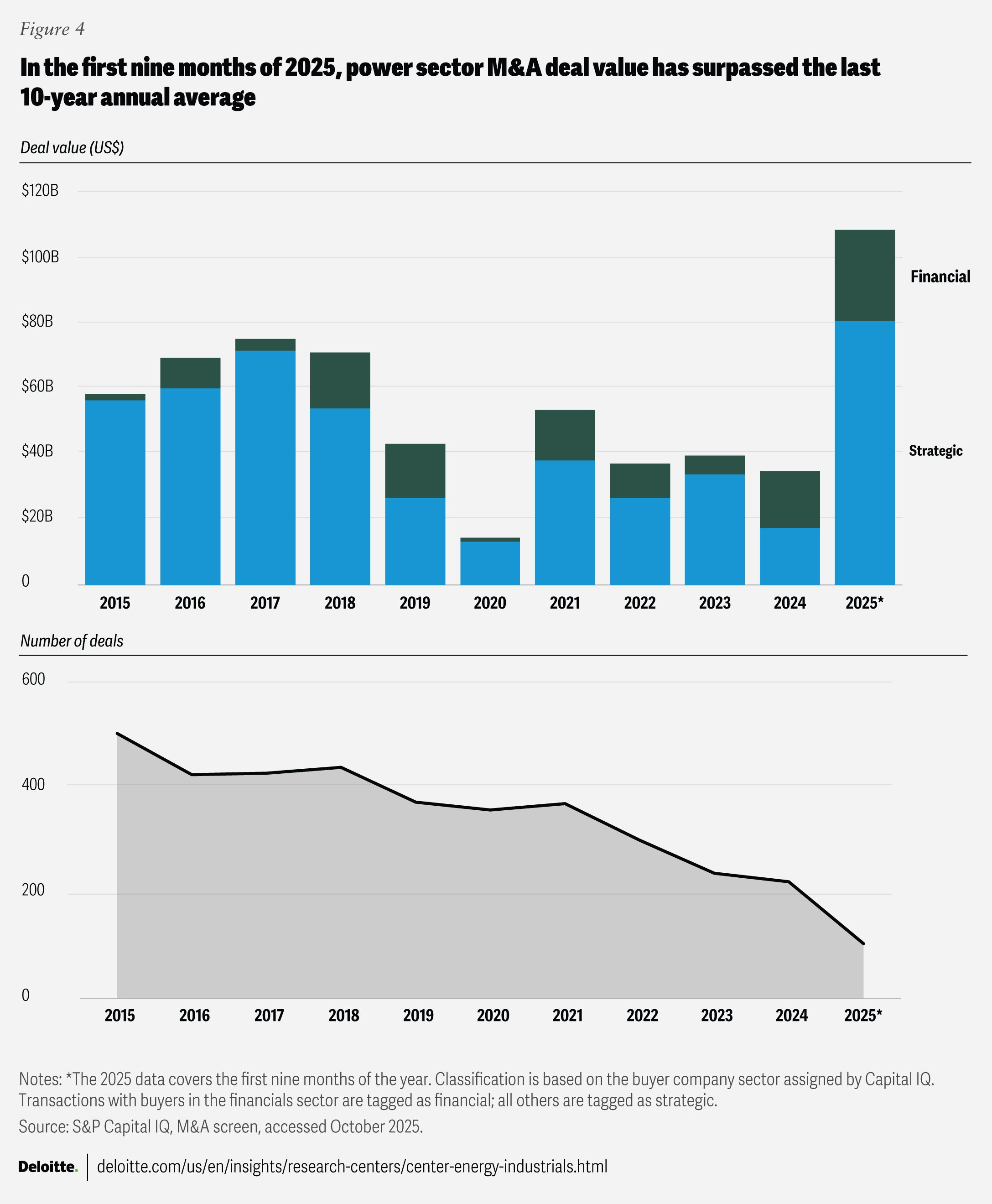

In the first nine months of 2025, M&A activity in the US electric power sector exceeded US$109 billion, driven by strategic repositioning (figure 4).58 Some electric power companies are acquiring dispatchable assets to meet digital and industrial load now, while others are divesting slower-growth assets to reinvest in regulated networks, firm generation, and clean infrastructure.59 At the same time, institutional investors are deepening their stakes in regulated utilities and contracted fleets, drawn by stable yields.60 These moves mark the emergence of utilities as capital hubs, while private capital provides scale.

{kind=link}

A new set of business models is giving utilities financing flexibility:

- Portfolio coinvestment: Joint ventures, strategic partnerships, and service-based contracts are being used to spread construction and technology risk while ensuring that firm capacity is delivered through long-term agreements.61

- Securitization, labeled debt, and equity issuance: Securitization is increasingly used to spread extraordinary costs over time, such as storm recovery.62 This can help save customers money while also preserving balance sheet capacity. Equity issuance remains a key lever. Many utilities are tapping markets through public offerings and dividend reinvestment plans to fund record capital expenditures while preserving credit metrics.63

- Service-based capacity contracts: To procure outcomes while shifting life cycle risk off their balance sheets, utilities are using mechanisms such as pay-for-performance structures, storage resource adequacy contracts, virtual power plant agreements, and energy-as-a-service microgrids.64

- Tax-credit monetization: Transferability provisions allow developers to sell unused federal clean-energy tax credits, thereby unlocking liquidity. Nearly US$30 billion in credits traded hands in early 2025, with volumes projected to reach US$50 billion by the end of the year.65

To scale these innovative models, regulatory frameworks need to evolve. By mid-2025, at least 28 states were exploring performance-based regulations, with 17 states and Washington, D.C. having enacted enabling legislation.66 This shift rewards outcomes—capacity delivered, reliability, affordability—rather than gross capital deployed, and can create space for coinvestment, securitization, and service-based contracts.

In 2026, capital strategy is likely to be measured less by gross spend and more by capacity per dollar and bill impact per incremental megawatt. Utilities that can blend self-financed projects with partnerships, securitized financing, and outcome-based models will likely deliver more capacity, faster, without overburdening customers.

2026 imperatives: Delivering under pressure

Utilities face a pivotal year in 2026, as converging pressures demand that they scale both smarter and faster. Key inflection points will likely include the repeal or phaseout of certain clean energy tax credits, evolving tariffs, new foreign entity of concern–related procurement requirements, and the integration of AI into core operations. Utilities that set the pace will be those that embed financial, operational, and digital flexibility into their playbooks—delivering capacity where and when it’s needed while safeguarding affordability.

Future in focus: Utilities are expected to transform to deliver flexibility

Meeting surging demand will require more than new megawatts. Utilities will pair firm capacity with AI-driven operations, flexible planning, and innovative finance to sustain affordability and reliability under stress. AI will enable real-time optimization of dispatch, asset performance, and outage response, while stronger supply chains support infrastructure. Together, these shifts will redefine reliability as the ability to sustain capacity, agility, and resilience while keeping power stable, flexible, and affordable.

Access the archive

Continue the conversation

Meet the industry leaders

Thomas L. Keefe

Kate Hardin

By

Thomas L. Keefe

Kate Hardin

Jaya Nagdeo

The authors would like to thank Carolyn Amon for her subject matter input and review.

Deloitte Advisory Board:

Micah Bible, Brian Boufarah, Craig Rizzo, Tom Stevens, Khalid Behairy, Jian Wei, Ian McCulloch, Martin Stansbury, Christian Grant, Jason Jacobs, Adrienne Himmelberger, David Yankee, Adam Keith, Marlene Motyka, and Ethan Erickson

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Rand Brodeur and Kim Buchanan who drove the marketing strategy and related assets to bring the story to life; Kaitlin Pellerin for her leadership in public relations; Elizabeth Payes and Aparna Prusty from the Deloitte Insights team who edited the report and supported its publication; and Harry Wedel for the visual design.

Cover image by: Pooja Lnu, Sanaa Saifi, and Jim Slatton

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.