Exploring new paths for funding the energy transition in the US power sector

Electric companies are expected to make massive investments to modernize and decarbonize the grid. Deloitte’s analysis outlines innovative strategies to help fund the transition.

Key Takeaways

- The US power sector is expected to require massive and sustained capital investments over the next two to three decades to fund the energy transition. Investments could total US$1.5 trillion to US$1.8 trillion from 2023 to 2030 – with similar expenditures until about 2050.

- The power sector’s energy transition costs are rising, and the complexity is deepening, with rising electricity demand, increasingly extreme weather, and macroeconomic pressures.

- The sector’s traditional funding avenues—filing rate cases and issuing debt and equity—may not suffice. Customer electricity bills rose 21% between 2019 and 2023, potentially leaving less room for further increases. High interest rates have often increased financing costs.

- Some electric companies are exploring alternative funding avenues, such as government incentives, private capital, and cooperation with power-intensive, green-leaning sectors like the technology industry.

- Private capital involvement in the power sector has grown since 2016, and some investors are adopting innovative investment paradigms. Many power and renewables companies have been selling unregulated assets, non-core businesses, and project platforms.

- To reduce costs and boost customer affordability, the power sector can also work with regulators to reform the industry regulatory model, deploy more renewables and non-wire alternatives, and use artificial intelligence to achieve operational efficiencies.

Electric power companies are under pressure from customers, regulators, and ratings agencies to enhance the safety, reliability, and resiliency of the US electric grid, all while reducing carbon emissions, expanding output to serve rising demand, and keeping customer electricity bills affordable. But achieving this transition is expected to require massive and sustained capital investments over the next two to three decades. And successfully financing it will likely compel a paradigm shift in funding strategies, combining traditional and innovative mechanisms, regulatory reforms, and public-private collaboration. Deloitte’s analysis discusses how utilities can address these challenges while minimizing customer rate increases.

Massive and sustained capital expenditures are expected

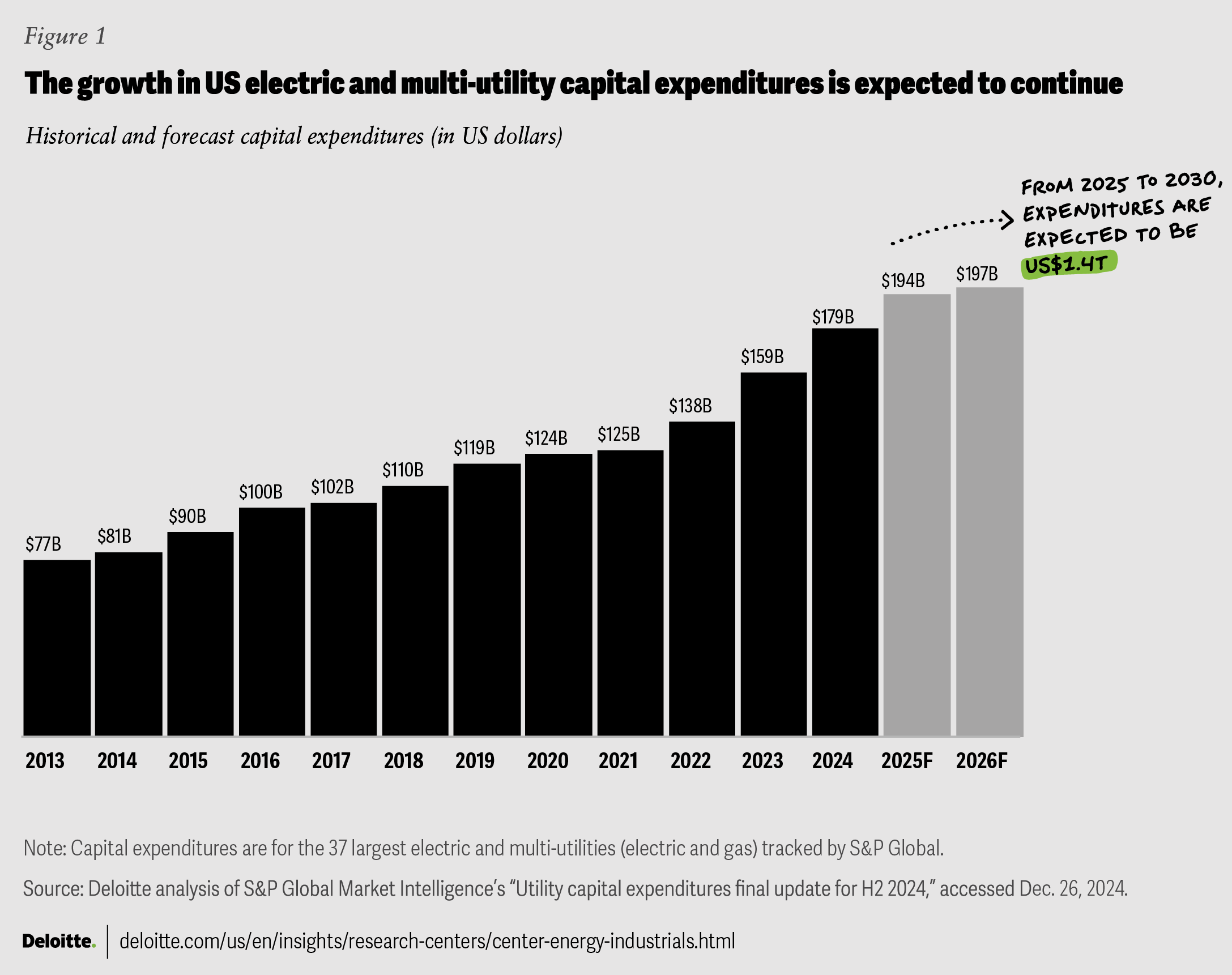

Between 2013 and 2024, a group of the largest US electric power companies have invested more than US$1.4 trillion to upgrade, modernize, and decarbonize the power grid.1Capital expenditures rose at a compound annual growth rate (CAGR) of over 7% during that period, and they’re projected to reach at least US$184 billion in 2025 (figure 1).2 Industry-wide investments could total US$1.5 trillion to US$1.8 trillion from 2023 to 2030, with similar expenditures expected during the following decade and beyond.3

{kind=link}

Much of the investment is directed toward the generation, transmission and distribution systems. This includes replacing fossil-fueled generation with cleaner, and often less expensive, resources such as wind and solar power, backed up with battery storage, as well as modernizing and expanding the system to accommodate those sources and serve growing load.4

Energy transition complexity and costs are rising

Utilities have long contended with challenges such as aging infrastructure, increasingly extreme weather, growing cybersecurity threats, insufficient transmission capacity, lengthy permitting and grid interconnection timelines, and the need to maintain customer affordability. But more recently, some of these trends are intensifying and new trends are emerging, often further boosting the complexity, and costs, of the energy transition.

Rising demand

- Some utility and business leaders forecast a tripling of US electricity demand nationwide by 2050, due to growing electrification of energy end uses.5

- This could spur a 15% to 20% increase in just the next decade when combined with demand from data centers running AI, cloud, and other advanced applications; new manufacturing facilities; economic growth; and changing weather trends.6

- One study projects that data center load alone could grow from 4% of US annual electricity generation in 2024 to as much as 9% by 2030.7

- Utilities are coordinating with technology companies on power supply solutions, especially clean power,8 while the tech sector is exploring new ways to achieve greater energy efficiency.

Increasingly extreme weather and climate events

- Weather trends are intensifying, leading many utilities to boost spending on grid resilience, recovery, and insurance, which can impact their credit ratings.9

- In 2023 alone, there were a record 28 weather events in the US that cost more than US$1 billion each.10 And 2024 is tracking similarly, with 19 confirmed disasters of this magnitude by mid-August.11

- Such events have risen steadily since the 1980s, when there were on average 3.3 disasters per year that cost US$1 billion or more (inflation-adjusted).12

- For utilities in many areas, the cost to mitigate, restore, rebuild, and cover liability claims from wildfires alone has skyrocketed. Areas designated as high wildfire risk have expanded across the country, and some utility credit ratings were downgraded in the past year due to wildfire damages and liability.13

Macroeconomic pressures and trade policy

- The global COVID-19 pandemic and Russia-Ukraine war led to supply chain constraints and global inflation, which boosted the cost of materials, labor, shipping and fuel in the power sector.14

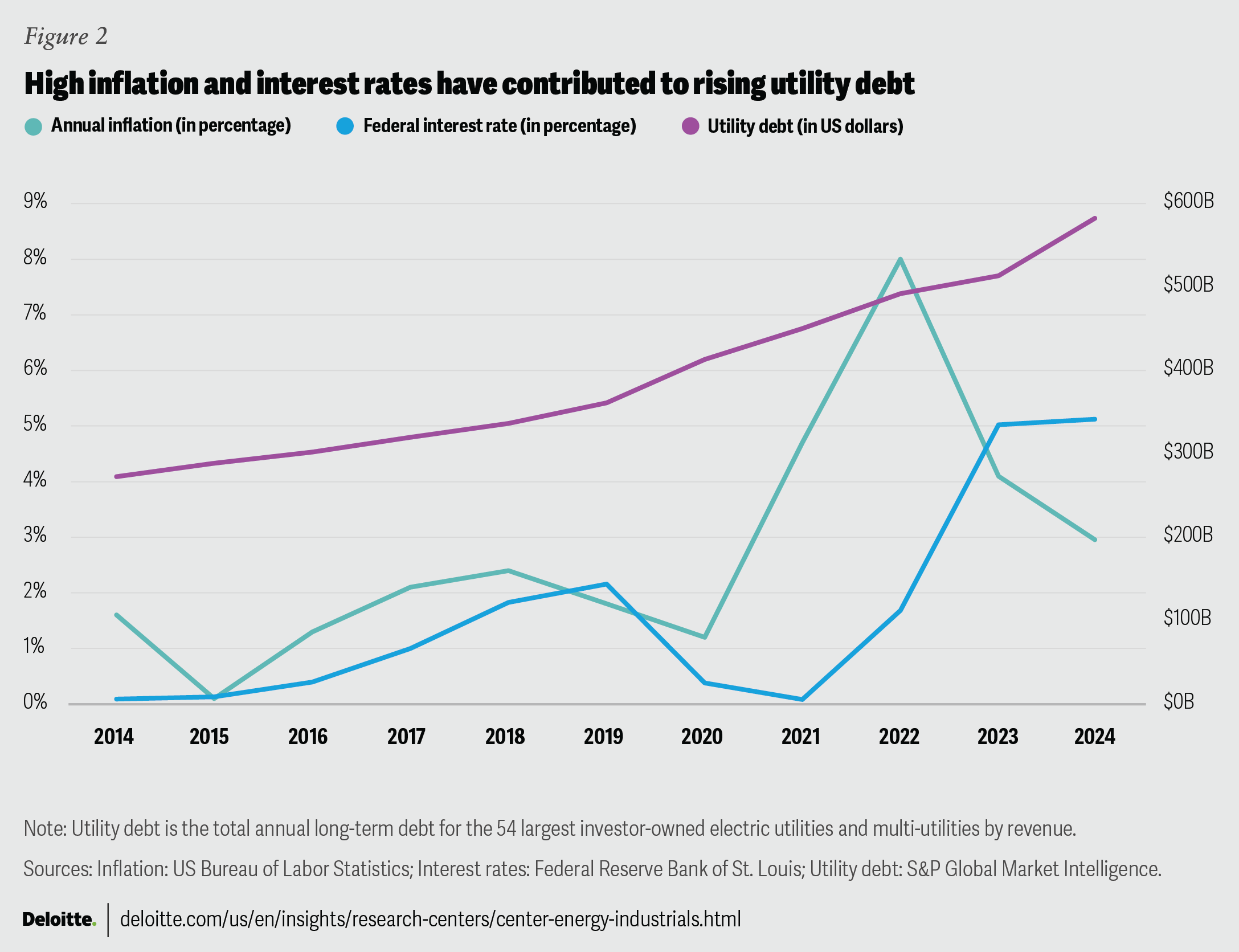

- Some costs are easing, but high interest rates have contributed to rising utility debt levels (figure 2). The renewable energy industry was especially hard hit by high interest rates due to its relative capital intensity and reliance on debt.15

- Tariffs on some imported solar panels and other components have also increased renewable energy and battery storage costs,16 though solar and wind are still the least expensive energy sources in most cases.17

{kind=link}

Traditional funding avenues may not suffice

US investor-owned electric companies have traditionally funded capital programs by filing rate cases with state regulatory commissions to recover the costs of investments through customer rate increases, and by issuing debt and equity.18 But recently both of these avenues have become more challenging.

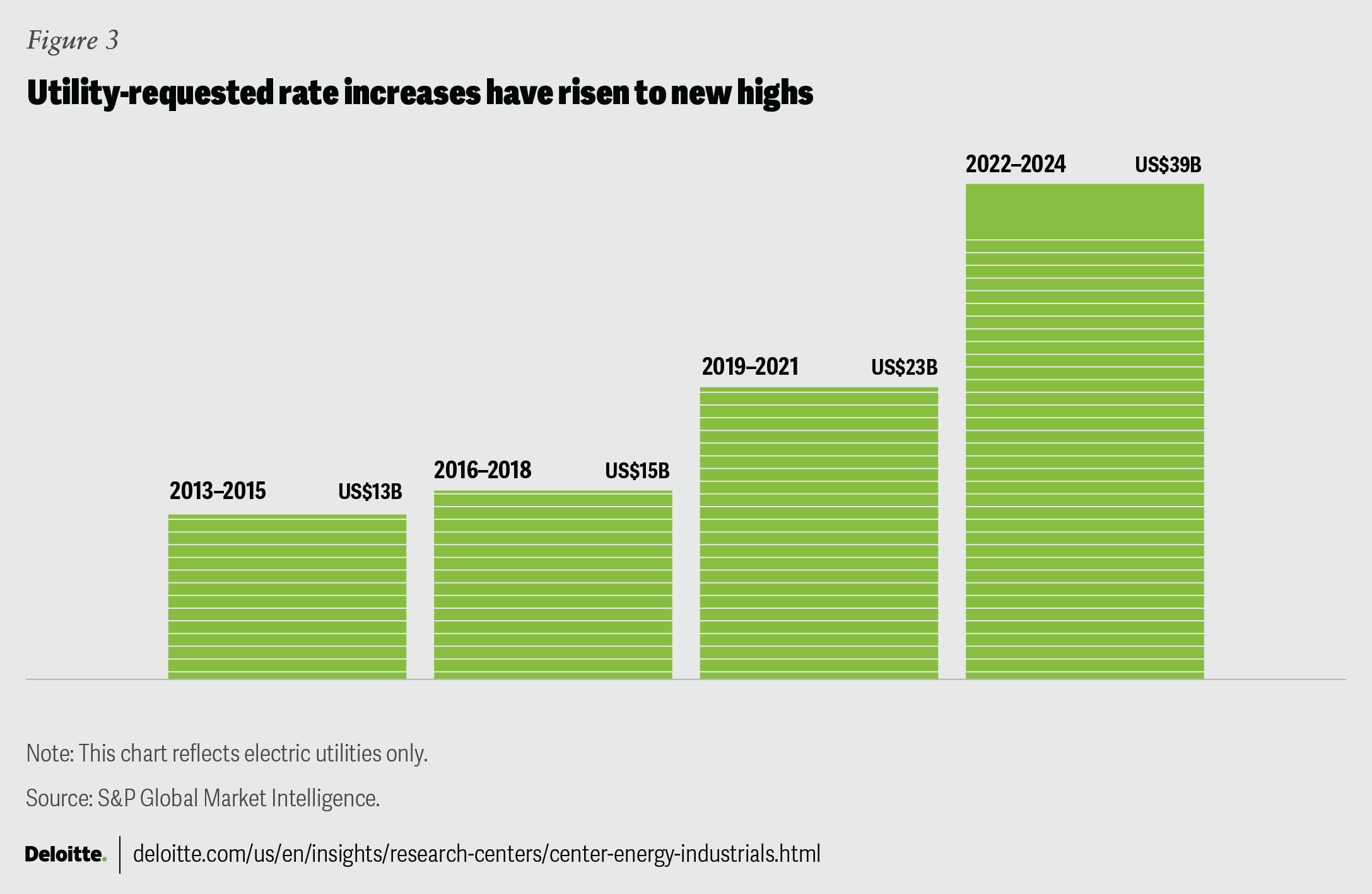

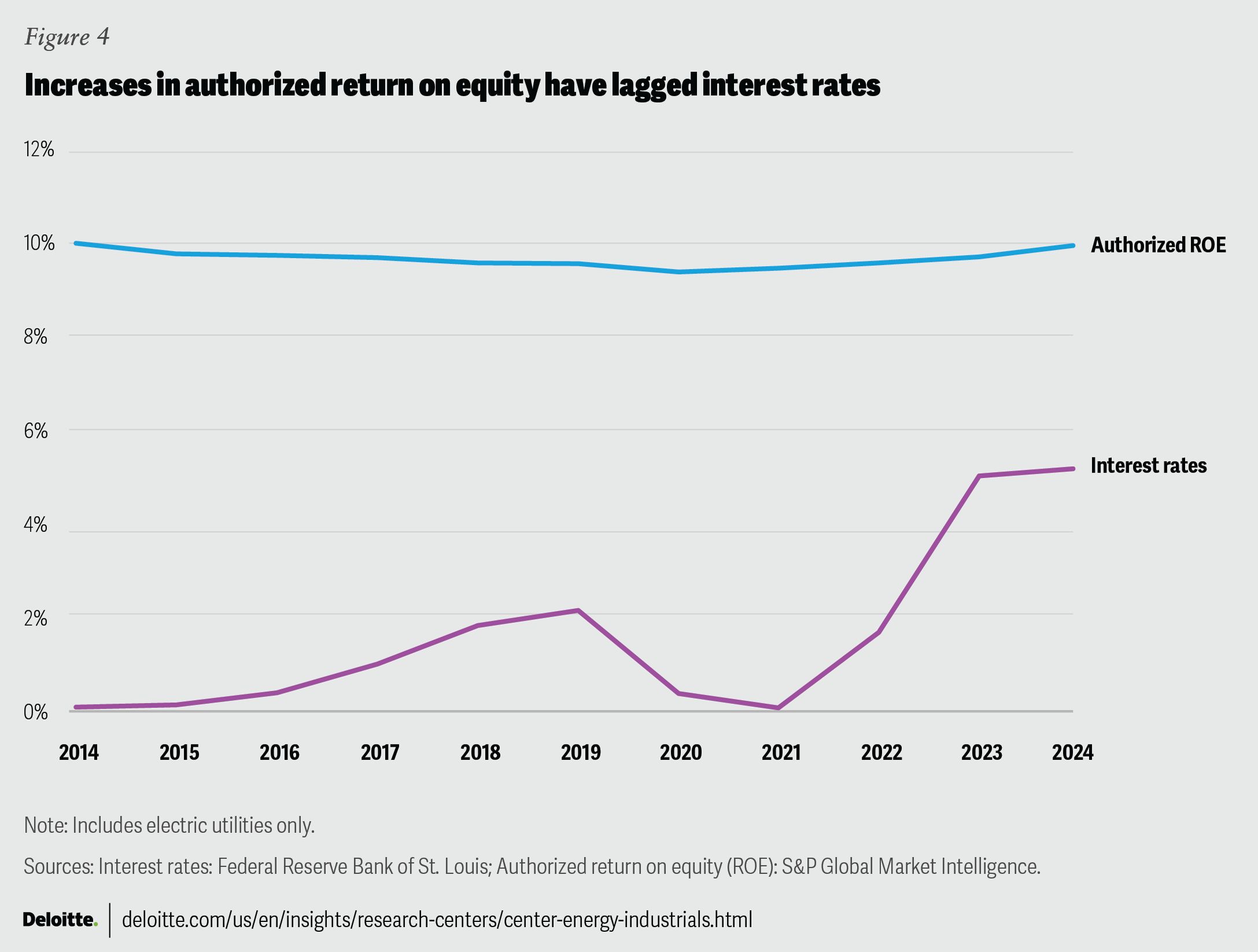

- Rate case limitations – Utility requested rate increases rose to record highs from 2020 through 2023 (figure 3), largely due to rising grid maintenance, upgrade and decarbonization costs.19 Fossil fuel price spikes combined with these costs to boost retail electricity prices nearly 21% across all customer segments from 2019 to 2023, while residential prices climbed nearly 23%.20 These increases, combined with economy-wide inflation, have made some state regulatory commissions hesitate to allow further customer rate increases.21 This can make it harder for utilities to recover capital investment costs. Authorized return on equity (ROE) increases have lagged interest rate increases for the same reason (figure 4), and this can weaken the industry’s financial performance and pressure credit quality.22

{kind=link}

{kind=link}

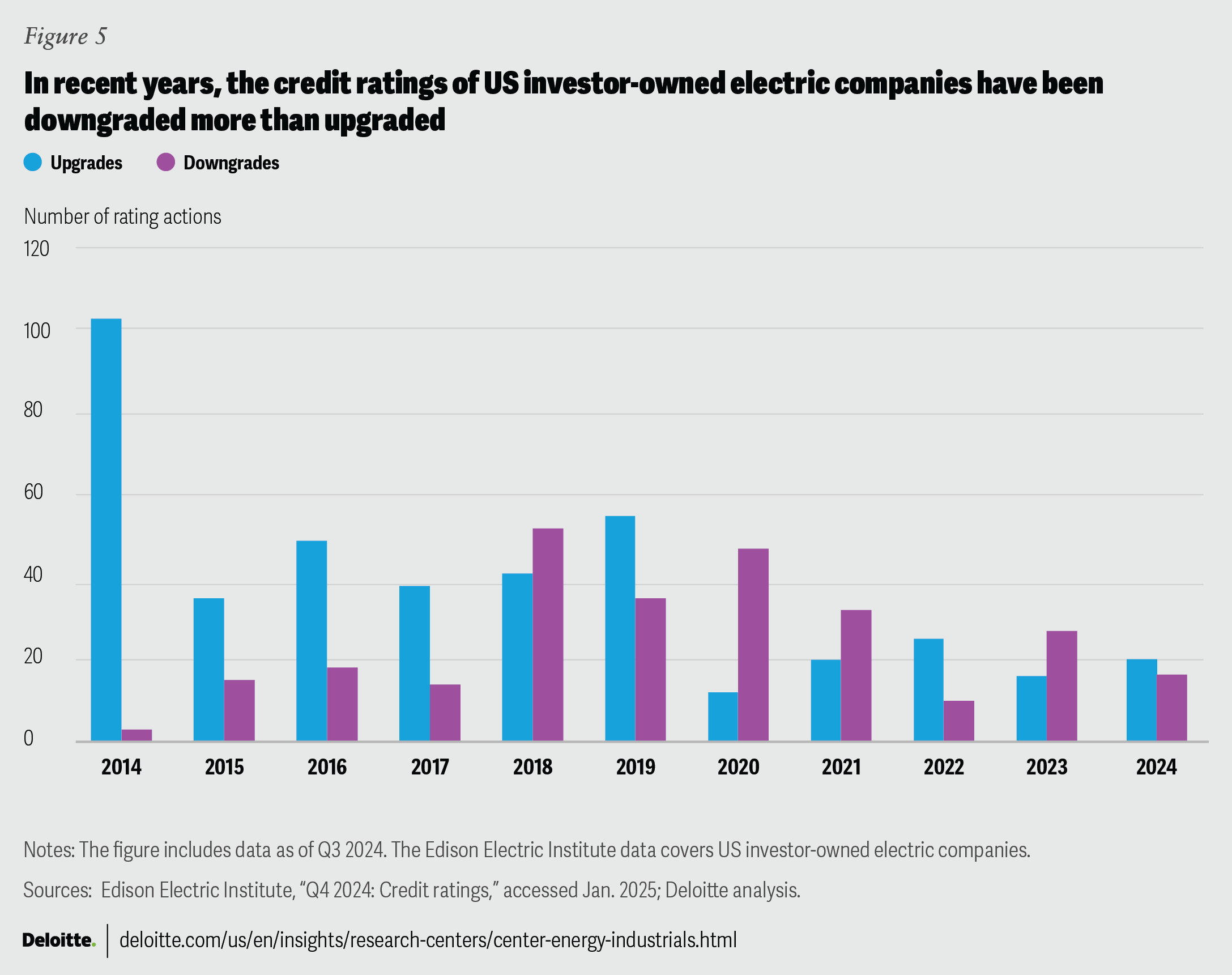

- Debt and equity market challenges: High interest rates and regulatory lag have raised the cost of debt financing. Combined with rising capex, this has caused some utilities to become overextended, making them more susceptible to credit rating downgrades.23 During three of the last four years (2020-2023), more utilities have had their credit ratings downgraded than upgraded (figure 5).24 Given the challenges around both raising debt and raising cash through rate cases, some utilities are planning to issue more equity to maintain a balanced mix of debt and equity.25 Utility holding companies are projected to need at least US$25 billion in equity annually each year in 2024 and 2025 to fund their capital investment plans.26 Many have been selling non-core assets to avoid issuing further debt or equity.

{kind=link}

These traditional funding avenues are not expected to raise the capital needed to fund capex for the energy transition in the near or longer term while maintaining customer affordability. Therefore, the industry is exploring potential new sources of funding, such as government grants, loans and tax incentives; private capital markets; and the power-hungry technology sector or other deep-pocketed, green-leaning corporates. In addition, the industry could pursue several paths to further reduce transition costs and boost customer affordability, including revising the utility regulatory model, deploying more low-cost renewable energy and non-wires alternatives, and achieving operational efficiencies.

Utilities are exploring alternative funding avenues

1. Government incentives may be more than a drop in the bucket, though likely not enough to fill the bucket

When it comes to the decades-long, multi-trillion dollar energy transition in the US power sector, recent government grants, loans and tax incentives were designed to provide critical support and create a multiplier effect by catalyzing private sector investment. Clean energy provisions in laws such as the 2021 Infrastructure Investment and Jobs Act (IIJA) and the 2022 Inflation Reduction Act (IRA) and Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act are helping reduce transition costs for electric power and renewable energy companies, but it’s not likely to be enough to underwrite the whole energy transition.27 And some of the provisions in these laws could potentially be impacted by a change of administration in 2025.28

The IIJA allocated nearly US$94 billion in grants and loans that could support many power sector transition goals (figure 6; for more details on the spending categories and amounts, please refer to figure 7 of 2024 power and utilities industry outlook).29 The IRA included an estimated US$287 billion in funding and tax credits effective until 203230 or when US electricity sector carbon dioxide emissions are equal to or below 25% of 2022 levels, whichever comes later.31 While the CHIPS Act was largely intended to develop the US domestic semiconductor industry, it also authorized US$100 billion for Department of Energy programs related to science, advanced energy, technology, and regional innovation.32

Together these three laws provide more than US$480 billion of investment into areas that could either directly or indirectly support the electric power sector energy transition. But the largest group of investor-owned utilities are investing almost US$180 billion in 202433—and that’s been growing at a 7% CAGR. So even if government expenditures matched industry needs exactly and utility investment remained steady at US$180 billion per year, the US$480 billion of investment from the legislation would be equivalent to less than three years of utility capital spending.

{kind=link}

In addition, depending on the results of the November 2024 presidential election, spending could be slowed or even halted for some programs by a new administration assuming office in January 2025.34 As of April 2024, just US$60 billion of the IRA’s estimated US$145 billion in direct spending on energy and climate programs had been announced, according to one analysis.35 In addition, less than US$700 million of CHIPS’ total US$54 billion had been awarded and less than US$125 billion of the IIJA and American Rescue Plan’s combined pot of US$884 billion.36 Even sums that have already been announced could be affected.37 Pending Treasury Department rules could be rewritten to make tax incentives less attractive, or to steer money toward alternate projects.38

2. The role of private capital is evolving and could fill more funding gaps

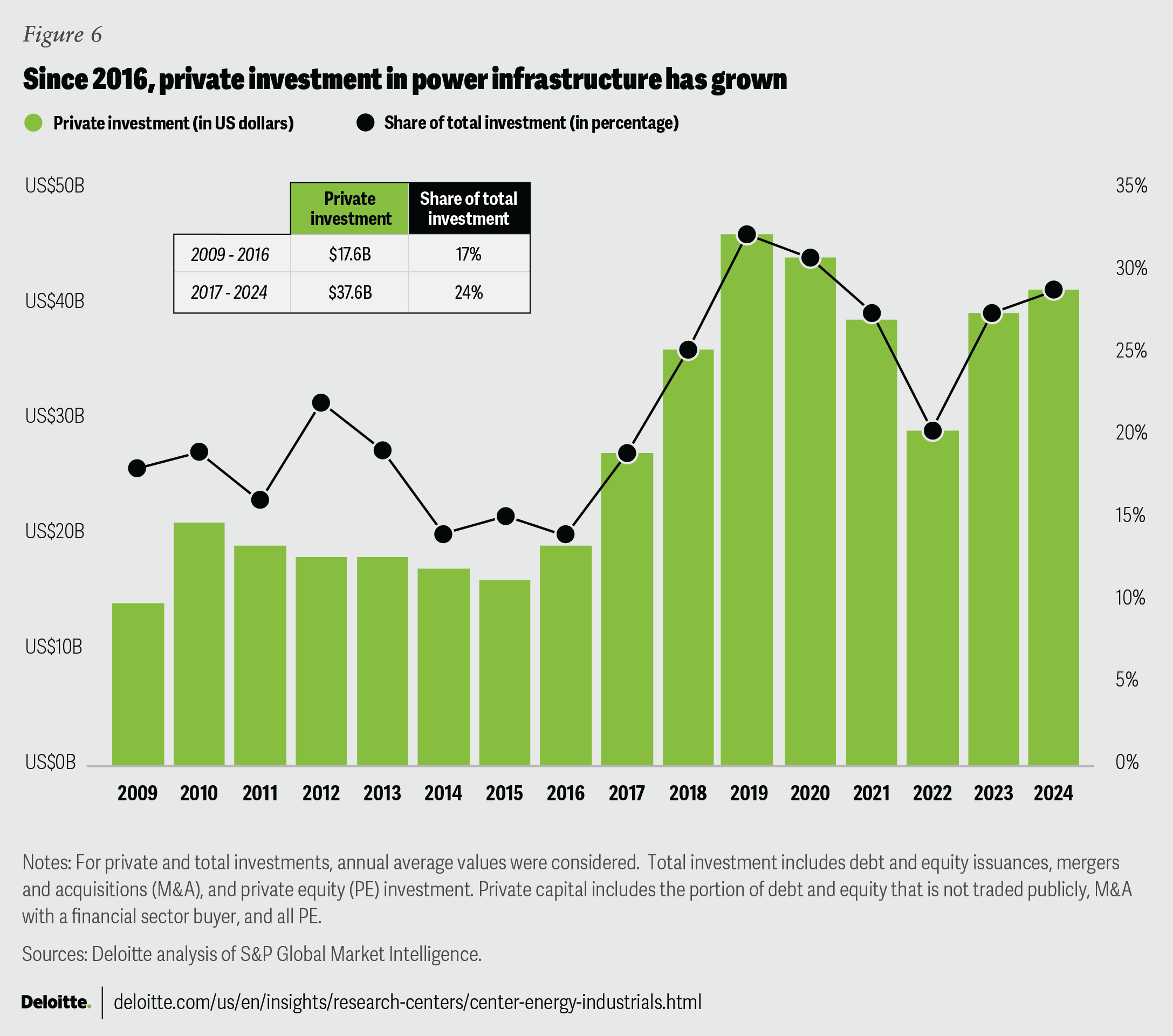

Electric power companies and renewable energy developers are increasingly turning to private capital sources, such as private equity and infrastructure funds (figure 7).39 Private capital involvement in the sector isn’t new, but it has reached higher levels since 2016 and investors are adopting innovative investment paradigms. Private investment in the power and renewable sectors is often driven by attractive government incentives, growing corporate clean energy demand, innovative technologies, declining costs, and the perception of renewable energy assets as a source of long-term, stable returns.40 Private equity and infrastructure funds increasingly seek to invest in assets at the intersection of sustainability and innovation such as data management, clean energy, clean transportation infrastructure, and assets critical to related supply chains.41 These investors can often deploy needed capital rapidly and multiply the impact of government investment in the energy transition.

{kind=link}

Some electric companies are exploring new types of equity deals with private capital funds, and renewable energy developers are bringing private funds into the renewable project cycle earlier. Some of the types of deals that seem to be gaining traction at the intersection of electric power and private capital are:

- Asset sales: Facing rising capital requirements and an increasingly expensive debt market, electric companies have been divesting non-regulated assets such as solar and wind plants, often to private equity and infrastructure funds. For example, in 2022, funds managed by Blackstone Infrastructure Partners agreed with Caisse de dépôt et placement du Quebec (CDPQ) and Invenergy to invest approximately US$3 billion in Invenergy Renewables, an independent power producer.42 In 2023, Invenergy, CDPQ and funds managed by Blackstone Infrastructure Partners partnered to form IRG Acquisition Holdings (IRGAH). The consortium acquired American Electric Power’s 1,365-megawatt (MW) unregulated, contracted renewables portfolio, valued at US$1.5 billion.43 IRGAH also agreed to sell US$580 million worth of renewable energy tax credits to Bank of America Securities, enabled by the new provision for tax credit transferability in the IRA.44

- Business sales: Some electric power companies have sold non-core businesses or minority interests in their regulated businesses to private capital investors. For example, Duke Energy sold its unregulated utility-scale wind and solar development business to Brookfield Renewable in a deal valued at US$2.8 billion in 2023.45 Soon afterward, Duke sold its commercial distributed generation business to an affiliate of ArcLight Capital Partners, LLC.46 While infrastructure investments can yield lower returns than other opportunities for private equity firms, their stability and long-term returns can make them attractive.47 This reasoning, as well as growth potential, may also be behind infrastructure funds’ investments in regulated utilities. In 2023, NiSource sold a 19.9% indirect equity interest in Northern Indiana Public Service Co. (NIPSCO), a gas and electric utility, to an affiliate of Blackstone Infrastructure Partners.48 The deal created a joint venture in which Blackstone will share more than US$2 billion of NIPSCO’s energy transition costs and receive a cash flow stream of regulated returns on its investment as well as cash dividends.49 Other utilities are said to be seeking similar deals and there are likely to be structural innovations on these types of deals.

- Platform investments: Renewable asset deals used to often involve purchases of individual projects, but private capital firms are increasingly acquiring portfolios of assets or businesses to achieve scale, consolidate fragmented markets, and optimize operations. The aforementioned sale of Duke Energy’s renewable development business to Brookfield and the Blackstone investment in Invenergy’s renewable portfolio are examples of project platforms. Renewable energy developers are also increasingly selling projects to private equity and infrastructure funds at earlier stages than has historically been the norm. The developers are initiating projects, obtaining permitting and project finance, and then selling the projects to funds that have a lower cost of capital. This can help the project offer the lowest possible rates to offtakers while also providing long term, stable returns to investors.

- Strategic partnerships: Joint ventures between power companies and private capital funds are becoming more common. The aforementioned deal between NiSource and Blackstone is one example. Another is a joint venture between Stonepeak and Dominion Energy Virginia to invest in a newly formed subsidiary to construct and operate an offshore wind farm.50 This regulated subsidiary will be a public utility in Virginia, able to recover prudently incurred costs,51 which could enable Dominion to improve its credit profile and access the additional capital needed to build the project while providing Stonepeak a stream of regulated returns on its investment.

- Electric company transition to private ownership: In one case, an electric company’s need for energy transition capital led to an agreement to be acquired by a private equity and infrastructure fund partnership.52 Minnesota-based ALLETE Inc., which includes regulated utilities and renewable energy companies with a national footprint, is expected to be acquired by Canada Pension Plan Investment Board and Global Infrastructure Partners for US$6.2 billion, including the assumption of debt.53 ALLETE's chair, president and CEO Bethany Owen said: “Transitioning to a private company with these strong partners will not only limit our exposure to volatile financial markets, it also will ensure ALLETE has access to the significant capital needed for our planned investments now and over the long term.”54

3. Big Tech’s big demand for clean energy could expand its support for the transition

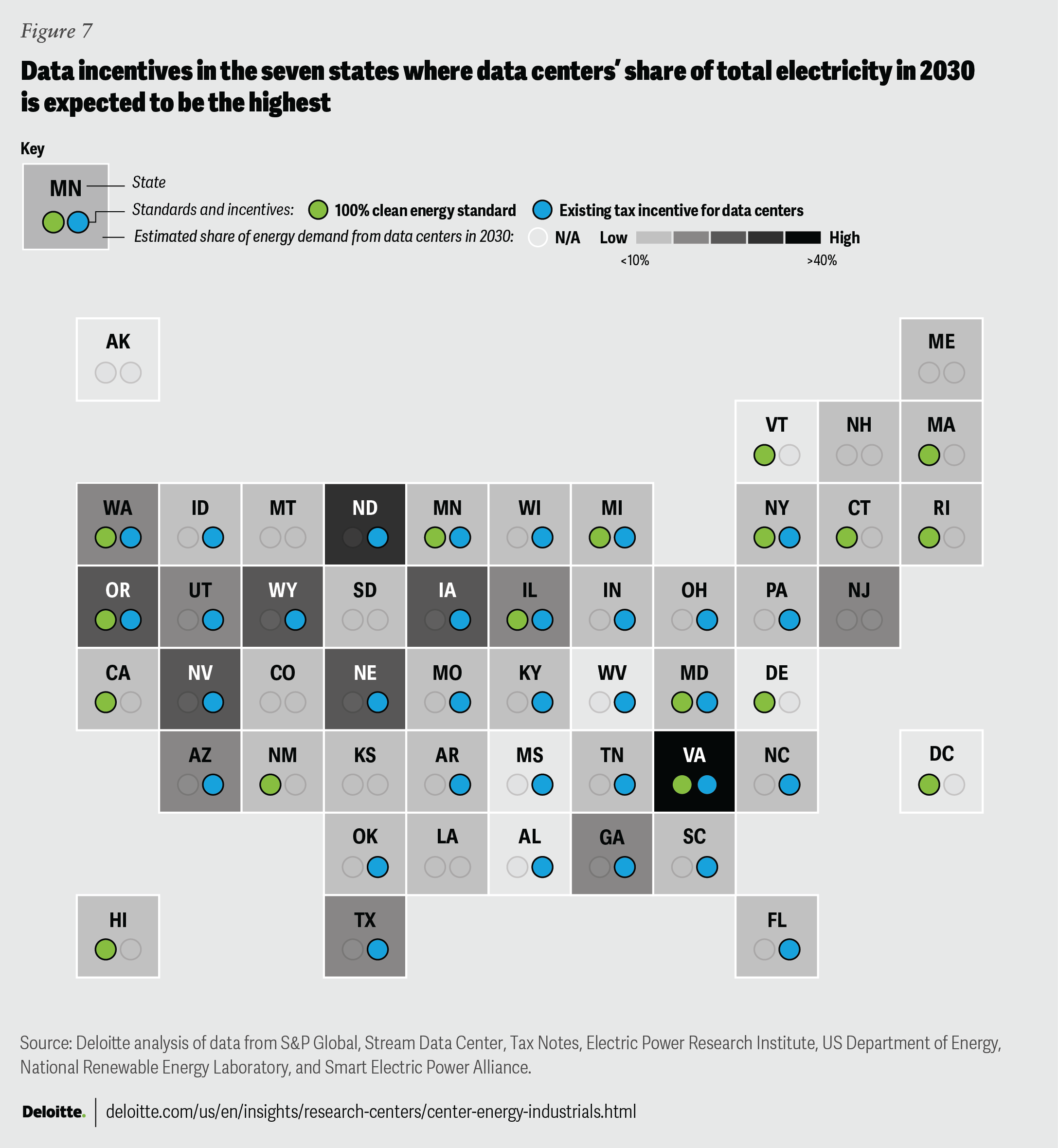

The largest companies in the technology sector have consistently been the top corporate buyers of renewable energy, whether through power purchase agreements with renewable project owners, green tariffs with utilities, or by other means. Recently, skyrocketing data center power demand combined with Big Tech’s commitment to clean energy have led the power and tech sectors to seek innovative solutions.55 The United States currently has nearly 3,000 data centers located in all 50 states and the District of Columbia (figure 8),56 but heavily concentrated in Northern Virginia, Texas, and Northern California.

{kind=link}

Some electric companies may seek to harness tech sector investment in innovation to advance and commercialize clean energy technologies. For example, Duke Energy has been working with large technology companies on a plan to enable them to purchase more clean energy by bankrolling construction of advanced energy technologies such as long-duration energy storage, or the eventual deployment of small modular nuclear reactors.57 Duke has proposed a suite of new tariffs to regulators that would enable it to sell power to corporations from onsite generation or from dedicated renewables and battery storage projects, as well as a “Clean Transition Tariff” that would help fund testing of new technologies until their performance justifies a larger grid rollout.58 Such financial support from willing corporate customers could help scale emerging technologies faster.59

The power sector could take further steps to cut costs and boost affordability

While the industry addresses funding the energy transition, it could potentially improve the equation by reducing the amount of cash required through strategies such as working with regulators to further align regulatory incentives with energy transition goals, deploying more low-cost renewable energy and non-wire alternatives, and pursuing operational efficiencies.

1. Regulatory reform could help align incentives to contain costs

One way to potentially increase customer affordability is to provide utilities incentives to contain costs through the regulatory model. Today, investor-owned utilities in most states operate under the “cost-of-service” (COSR) regulatory model, which typically rewards capital investment.60 The model allows utilities to earn a guaranteed rate of return on investments that the state utility regulatory commission deems prudent and necessary, through rate cases, and to pass those investment costs on to customers through rate increases. This incentive implies that utilities could tend to overinvest in capital-intensive projects, such as generation, transmission and distribution infrastructure, and underinvest in less capital-intensive alternatives, such as energy efficiency, demand-side management, and distributed generation.61 Research has shown this to be true even when these non-wire alternatives can meet customer needs at a lower cost than larger infrastructure investments.62

The current focus on transitioning to an increasingly reliable, resilient, and carbon-free electric grid while maintaining customer affordability could suggest that continuing to reward utilities for spending may be counterproductive. Regulators have explored rewarding utilities based on performance instead, with performance-based regulation (PBR), since the 1980s. And it’s become more common in recent years.63 Under PBR models, regulators—sometimes in coordination with utilities and legislators—can develop performance incentive mechanisms (or PIMs) to incentivize utilities financially with quantifiable and measurable goals. The goals are often in specific priority areas such as:

- containing costs,

- enhancing reliability and resilience,

- reducing emissions,

- deploying certain technologies,

- improving operational efficiency

- addressing energy equity, and

- improving customer satisfaction.

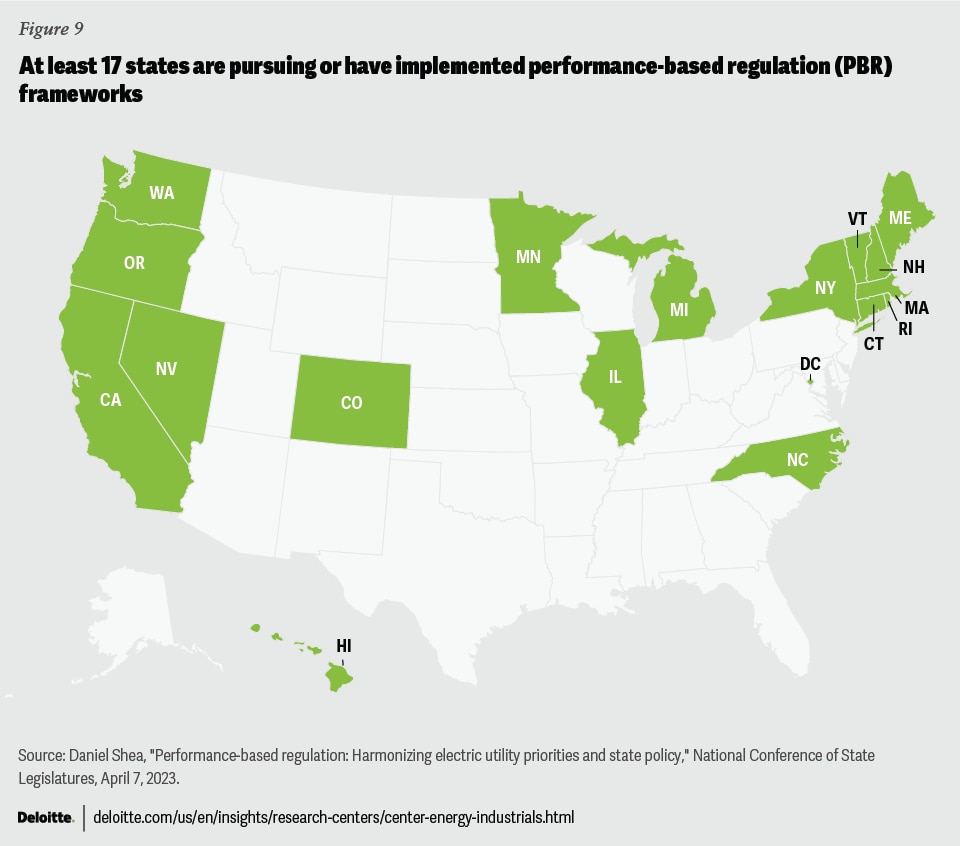

The majority of states apply some PBR mechanisms, usually within a COSR framework. But at least 17 states and the District of Columbia are pursuing or have implemented more comprehensive PBR frameworks (figure 9).64

{kind=link}

While PBR can counter the COSR model bias toward large capital expenditures and against lower cost alternatives, the transition may not be simple. It can be challenging for utilities to move to a new regulatory system, and potentially expensive until they’ve had time to earn incentives for meeting new performance goals.65 Reforms should be carefully designed, and could focus on guidelines such as:

- Creativity, innovation, and balance may be required to develop adequate metrics.

- The stakeholder process should be flexible and provide realistic timelines.

- PIMs should be specific and should reward utilities for achievements without over- or under-compensating them.

- The process should be iterative; trial and error may be required.

- Stakeholders should try to recognize mistakes and use lessons learned to improve the system.

- It’s important to keep working toward change, even if it’s small at first.

PBR models vary in how and when they apply components such as PIMS, multi-year rate plans (MYRPs), and revenue or profit adjustments. Regulators can learn from a growing array of models across states and countries, such as the United Kingdom,66 which are trying to reduce the costs of the energy transition and reward the attributes that advance it.

Another way that utilities and their regulators can contain costs relates to the additional grid infrastructure required to serve large new customers such as data center and cryptocurrency mining operations. Utilities in many states may welcome inquiries from data centers proposing to build in their territories. But some utilities are asking regulators for new contract and tariff provisions to help enable efficient cost recovery of the grid investments required to serve massive new loads and to help ensure that other customers won’t be burdened with these costs if the expected demand doesn’t materialize.67 Below are a few provisions that utilities have requested from state regulatory commissions, some of which could become more common:

- Upfront payments for data center hookups to utility infrastructure68

- Accrued allowance for funds used during construction of new infrastructure, as it can take three to five years for a data center to begin operations and start consuming and paying for electricity after contract signing69

- A 10-year commitment by data centers with more than 25 megawatts of demand to pay for a minimum of 90% of the electricity they’ve requested, even if they ultimately use less (95% for cryptocurrency miners).70

2. Renewable energy and non-wire alternatives can reduce costs and boost affordability

In addition to being carbon-free, renewable energy resources such as wind and solar are already among the most wallet-friendly electricity generation choices for utilities and consumers, and costs are expected to continue declining over time.71

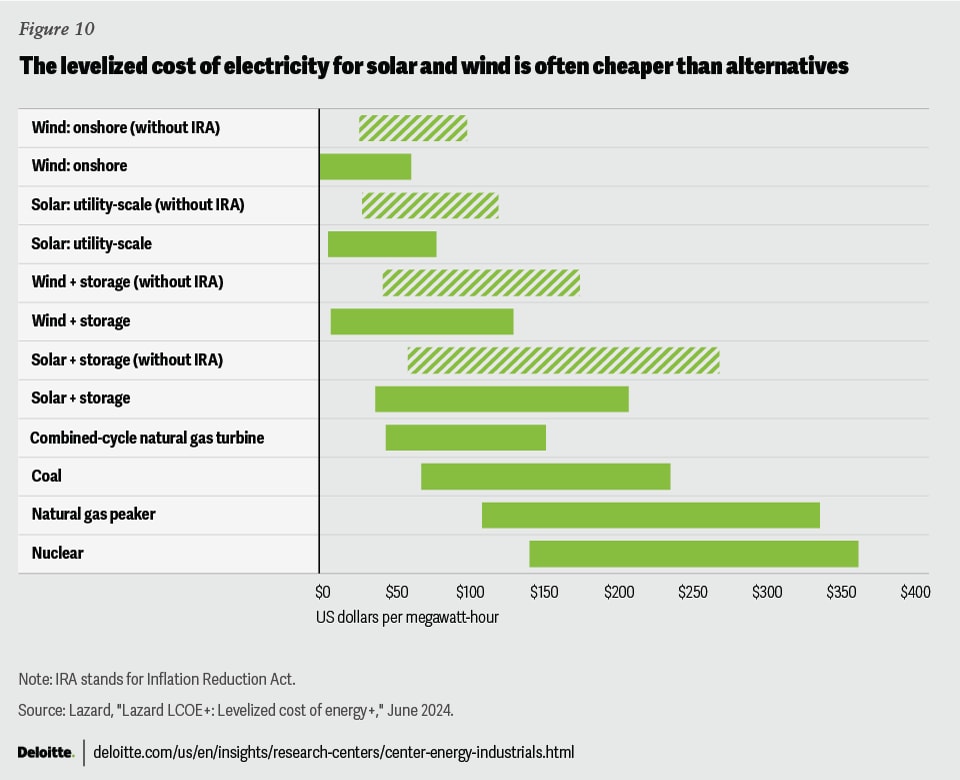

- Utility-scale power generation: Wind and solar are the lowest cost utility-scale power generation options in many cases, increasingly even when paired with battery storage to boost dispatchability (figure 10).72 This is typically the case when IRA tax credits are included, and often even without them,73 and renewable costs are expected to continue declining.74 Figure 10 compares the levelized cost of electricity (LCOE) for new utility-scale solar and wind generation versus natural gas, coal and nuclear power plants.

{kind=link}

- Retail electricity: Renewable energy has already helped households and businesses save on their electric bills, with consumers in several states receiving utility bill credits based on IRA-driven cost reductions.75 In Texas, widespread adoption of renewables was found to have reduced wholesale electricity costs by about US$31.5 billion between 2010 and 2022, saving consumers significantly from what they might otherwise have had to pay.76 While retail electricity bills have generally been increasing nationwide recently, this is primarily attributed to extreme heat and the lingering effects of previous natural gas price spikes.77 Renewable energy sources do not use fuel and the transition to clean energy sources could help slow rising temperature trends over time.

- Future savings: In later stages of the energy transition, potentially by about 2045, some utilities estimate that households could be saving as much as 40% on monthly energy bills.78 Savings could be achieved once vehicles; heating, ventilation, and air conditioning systems; and appliances were largely transitioned to electric alternatives powered by low-cost renewable energy, as this would contribute to reducing household expenditures on gasoline, natural gas and propane.

Another option that grid planners could consider to reduce costs is to use non-wire alternatives (NWA). NWA include any electric grid investments that can help defer or avoid more costly construction or infrastructure upgrades.79 Utilities can deploy strategies, technologies, and programs such as demand response, energy efficiency, or tapping into distributed energy resources such as rooftop solar, home energy storage, electric vehicles and smart thermostats to potentially serve load more cost effectively than procuring or investing in new generation or transmission resources (see Households transforming the grid: Distributed energy resources are key to affordable clean power for examples).

3. Achieving operational efficiencies can help boost customer affordability

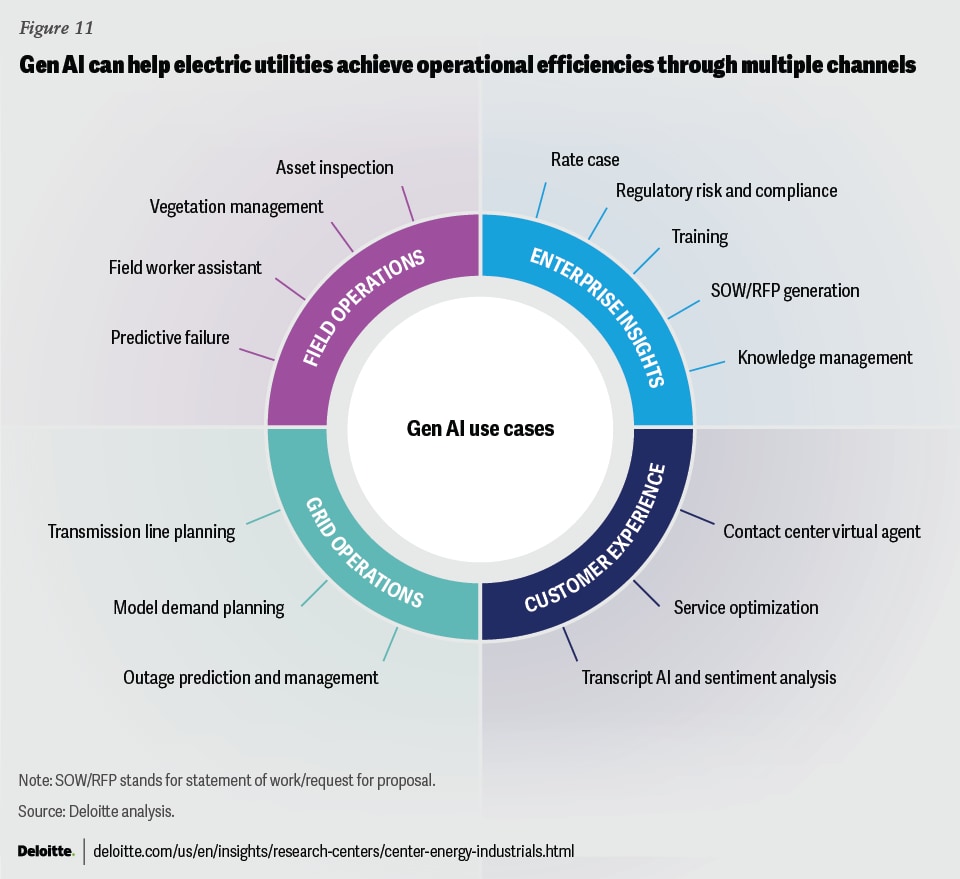

Many electric companies seek to achieve operational efficiencies by improving their performance and reducing costs, or doing more with less. Regulated utilities are often required to pass those savings onto customers, which can help maintain customer affordability in an era of rising capex. Some common ways for electric utilities to achieve operating efficiencies could include: implementing smart grid technologies, optimizing asset management, leveraging data analytics, or deploying cloud computing and digital customer service platforms. Increasingly, electric companies may turn to generative AI (gen AI) to gain efficiencies (figure 11).80

{kind=link}

Several US-based electric utilities have implemented advanced AI models across a diverse range of mission-critical operations, such as:

- using light detection and radar (LiDAR) to potentially prevent fires and outages by detecting and predicting vegetation encroachment near power lines;

- combining AI with edge computing, computer vision, and gen AI to automate asset inspections; and

- utilizing satellite images to assess storm damage and inform resource deployment for faster service restoration.81

Some utilities are realizing significant enterprise benefits from these AI applications, such as improved safety, operating efficiencies, deferred capital expenditures, and additional revenue. Below is an example from a large US utility that created synthetic image data to train and improve the accuracy of its defect detection computer vision AI model.82

Synthetic data generation

- Existing defect images used to initially train the model were scarce and time-consuming to manually label and annotate for training the model.83

- Through synthetic data generation, the utility was able to create a series of base asset models that could be tailored to reflect a variety of field conditions and expedite training of the model.

- Demonstrated 67% performance improvement in defect detection by using more than 2,000 3D synthetic images in 4K resolution.

Conclusion

In an environment of deepening complexity and challenges, electric companies are forging the path to a cleaner, more reliable, resilient, and affordable electric grid. Vast amounts of capital are expected to be required over as much as three decades and the industry is turning to new funding sources while also seeking ways to cut costs. Reforming regulatory paradigms, deploying low-cost distributed and renewable energy sources, and pursuing operational efficiencies can help reduce costs. New funding avenues may include government sources such as IRA, IIJA and CHIPS loans, grants and tax credits or coordination with electric power-hungry, green-leaning corporate customers such as technology companies. Finally, among the most promising sources of capital could be investors such as the private equity and infrastructure funds that are stepping into the picture with their ability to rapidly deploy large amounts of capital, pioneer innovative financing mechanisms, and engineer creative collaborations to help bridge the financial gap in the power sector’s energy transition.

By

Jim Thomson

Marlene Motyka

Keith Adams

Kate Hardin

Suzanna Sanborn

The authors would like to thank Jaya Nagdeo, who provided research, analysis and editorial support and Akash Chatterjee, who provided research and analysis for this article. The authors would also like to acknowledge Micah Bible, Adrienne Himmelberger, Khalid Behairy, Subhani Syed and Katie Gibson for their subject matter expertise and review; Kim Buchanan and Randy Brodeur for driving the marketing strategy and related assets; Alyssa Weir for her leadership in public relations; and Clayton Wilkerson, Elizabeth Payes, Aparna Prusty and Harry Wedel for operational, editorial, and graphics support.

Cover image by: Rahul Bodiga

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.