2026 Mining and Metals Industry Outlook

The US mining and metals industry faces a pivotal moment, as global trends, policy shifts, and rapid technological and workforce changes reshape competitiveness

This analysis was prepared and finalized based on market information and developments available before March 2026. While subsequent geopolitical developments may influence near-term market conditions, the structural conclusions presented here remain focused on the broader mechanisms most relevant to the US mining and metals industry.

The US mining and metals industry’s resilience will likely be tested in 2026 as energy and trade policy changes continue to affect operational shifts. US-based mining and metals companies are expected to shape their strategies around five important trends:

- Policy and national security reshape domestic value chains

- Financing for projects hinges on mined resource quality, contractable demand, and schedule certainty

- Portfolios are rotating toward demand-aligned positions and circular platforms

- Cost pressures demand higher efficiency from US operators

- Workforce training and upskilling are becoming differentiators

1. Policy and national security reshape domestic value chains

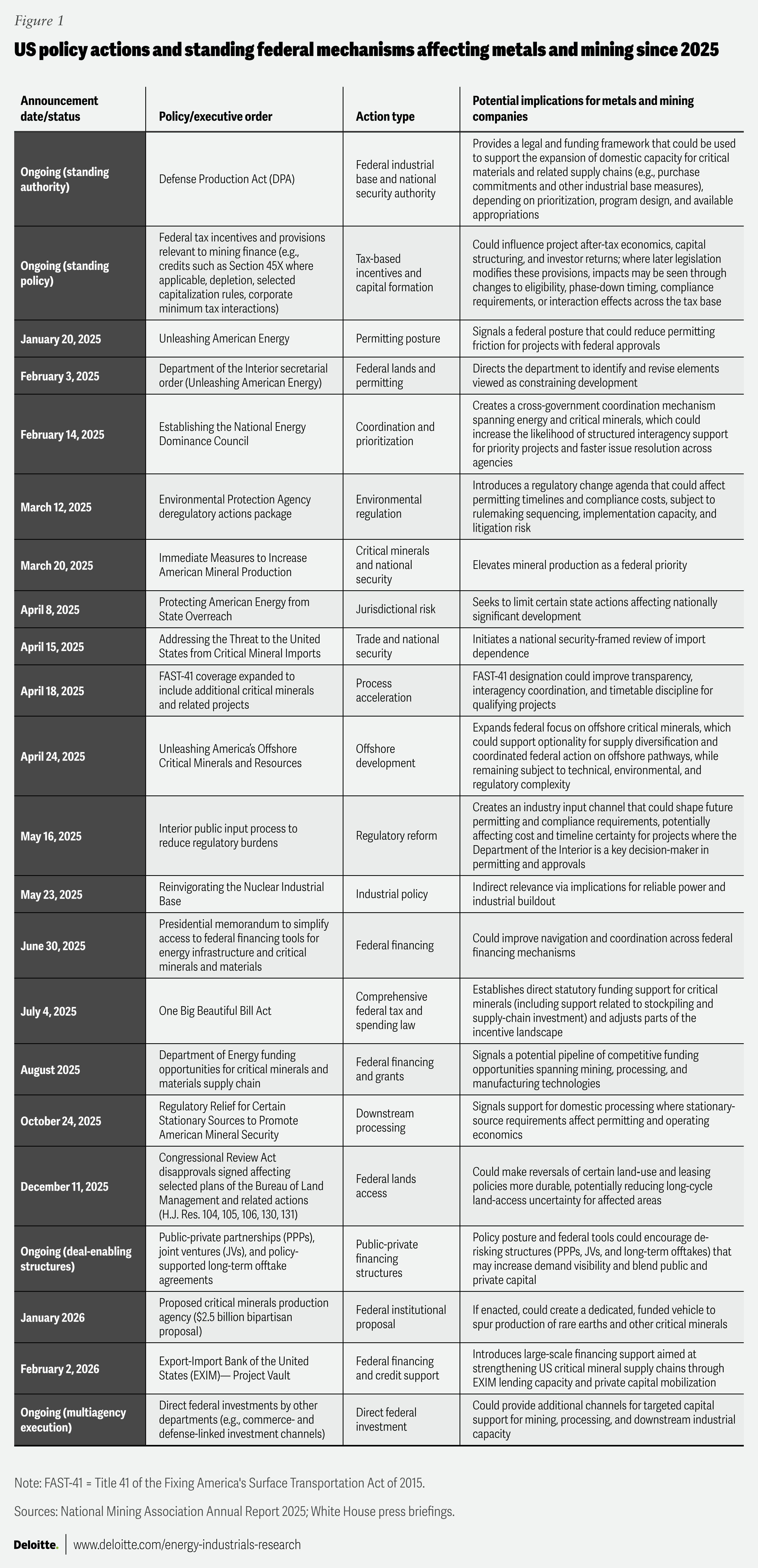

Amid evolving geopolitical dynamics, national security objectives and policy alignment are driving the United States to prioritize the development of domestic supply across the mining and metals value chain, from mining and processing through downstream industrial inputs. It is also part of a broader effort to build (or, in some cases, rebuild) secure, resilient supply chains in strategic sectors.

US import dependence remains significant, but policy actions are targeting bottlenecks that slow domestic supply growth (figure 1).1 The US Department of the Interior’s alternative compliance process under the National Environmental Policy Act aims to compress review timelines for projects requiring a full environmental impact statement from nearly two years to roughly 28 days, while FAST-41 and the Federal Permitting Dashboard reinforce schedule transparency and interagency coordination.2 Meanwhile, initiatives such as Project Vault and the Forum on Resource Geostrategic Engagement seek to address supply concerns.3 Even so, scaling processing and conversion capacity could still take years for many minerals.

Table of contents

- Policy and security-driven reshoring

- Financing shifts to bankability

- Portfolio repositioning

- Efficiency and smart operations imperative

- Workforce as a differentiator

- Conclusion

Expectations for 2026

- Projects with a clear delivery path that also reinforce domestic value chains are likely to advance first: Near-term progress could favor assets with a clearer line of sight to approvals and fewer sequential dependencies, including phased developments and brownfield expansions. This reflects a tighter focus on permitting timelines, constructability, and maintaining a social license to operate, alongside the push to secure domestic value chains. For projects selling products in thinly traded markets, government policy and public sector financing may help bolster project economics.

- Evolving trade conditions are likely to reshape value chain footprints: Shifting tariffs and trade remedies (for example, expanded Section 232 coverage and product-specific duties), and eligibility-driven sourcing rules (for example, rules of origin and Section 30D foreign-entity-of-concern restrictions tied to clean-tech demand) are likely to push supply chains to optimize for traceability and jurisdictional resilience, not just cost.4 This can increase the value of adaptable processing configurations (for instance, modular plants) and the ability to route material between domestic facilities and trusted partner-country processing under enforceable contracts.

2. Financing for projects hinges on mined resource quality, contractable demand, and schedule certainty

Scope for further financing innovation exists for critical minerals traded in small, illiquid markets with limited price transparency and concentrated demand, including inputs for defense, energy, and technology infrastructure. Many projects may require financing structures that reduce revenue risk and secure reliable offtake where private markets cannot efficiently absorb early-stage uncertainty.

The Colorado School of Mines Payne Institute’s CM3 taxonomy outlines three core drivers of bankability: market size and pricing structure, production pathway, and the quality of offtake.5 For projects supplying critical inputs that may otherwise struggle to raise capital, the US government is enhancing project bankability by cofinancing development through grants, loans, and, in some cases, minority equity stakes in companies.6 This market-making toolkit is rapidly expanding and increasingly combines these tools with equity-like warrant instruments and other mechanisms that improve price and revenue certainty, which can help accelerate project underwriting.

As Payne’s CM3 taxonomy notes, index-priced materials can face volatile processing margins (feedstock versus refined prices), increasing interest in revenue-stabilization mechanisms such as contracts for difference.7 Government actions may shape project finance through strategic stockpiles or public procurement to create demand, onshoring incentives and tax credits, public loans or guarantees to lower financing costs, and tariffs or export controls to shift supply and pricing.

Early demand linkages are also important in financing, and there are discernible shifts underway, which can help projects reach financing and scale more quickly. For instance, original equipment manufacturers (OEMs) across automotive, battery, magnet, technology, and aerospace and defense sectors are moving downstream and securing their tier 2 and tier 3 supply chains through long-term supply contracts, joint ventures, and equity-type partnerships, while some public sector players are pursuing offtake contracts.8

Expectations for 2026

- Selective “market-making” is expected to remain decisive: Price floors, offtake commitments, and public capital are likely to concentrate on a narrower set of critical minerals with opaque pricing, concentrated supply among a few producers, complex processing pathways, and long buyer-qualification cycles that make revenues harder to underwrite.

- “Path to customer” could matter as much as “path to ore”: Projects involving strategic materials with volatile pricing and weak market signals may advance faster when a buyer is clearly identified. This is likely to translate into more long-term offtake and partnership structures that reduce risk and support commercial readiness. For example, partnerships and contracts with OEMs and their tier-1 suppliers across several sectors, or domestic processors building conversion capacity could help provide a credible path to secure sales. Commercialization is increasingly shifting away from spot sales toward structured agreements such as multiyear offtakes, qualification-linked ramp commitments, tolling or processing contracts, and strategic partnerships or equity that anchor demand and reduce scale-up risk.9

- Underwriting may prioritize shorter risk windows: Private capital may increasingly hinge on tests that include a credible timeline, secured early demand, and a competitive cost position, increasing the emphasis on near-term, after-tax cash flow timing, not just long-run resource quality. Brownfield expansions, recovery or reprocessing, and incremental processing additions may be preferred when they shorten commissioning and qualification timelines.

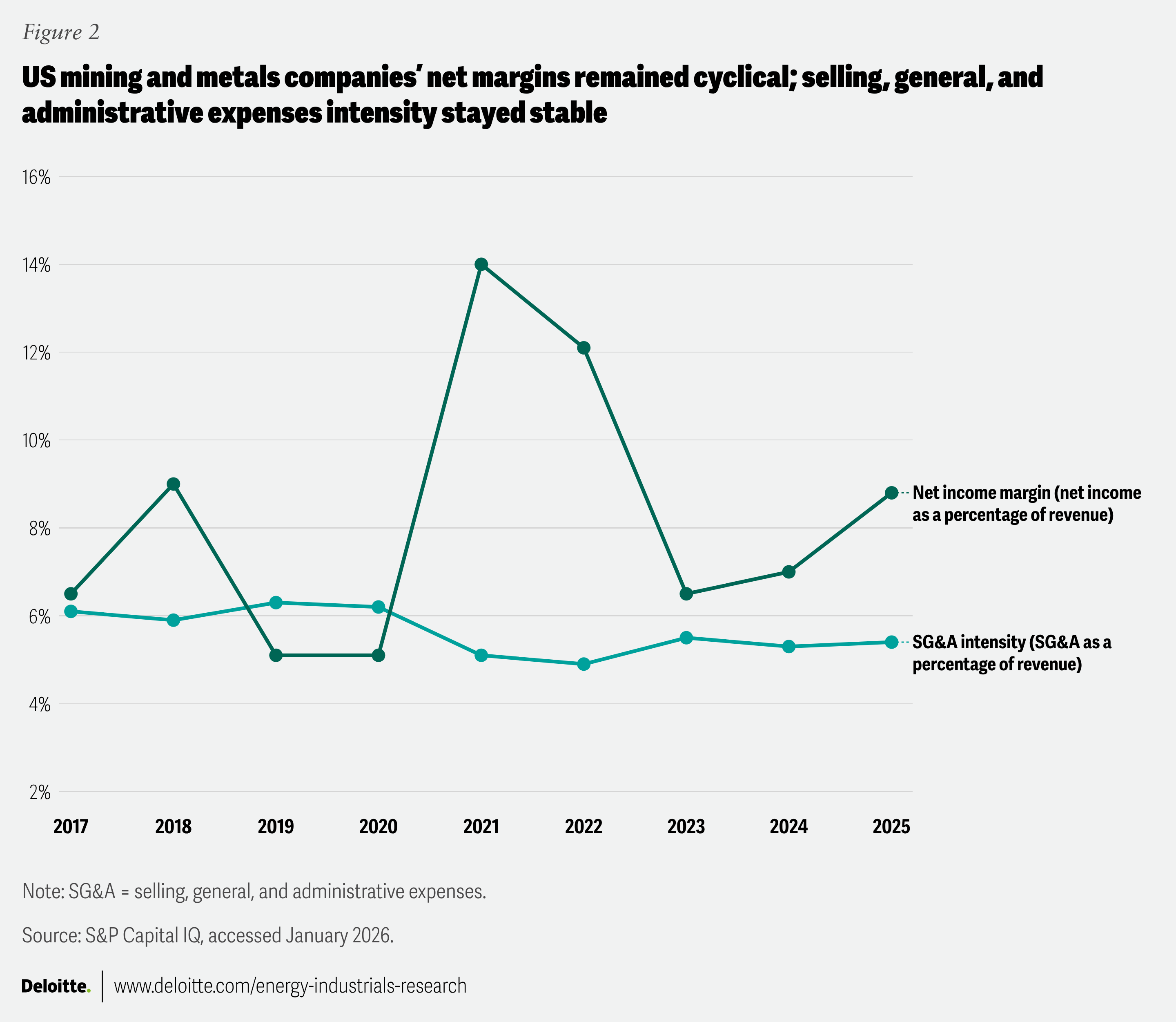

- Tax assumptions are likely to become an upfront diligence and documentation prerequisite: For US mining and metals companies, net margins typically move with market cycles, while overhead expenses, represented by the selling, general, and administrative expense intensity, remain relatively stable (figure 2).10 This limits the ability to offset ramp-up shortfalls through overhead actions and increases scrutiny on early cash generation. Investors will likely pressure-test tax assumptions that affect near-term cash taxes and after-tax cash flows. These include accelerated depreciation (such as bonus or additional first-year depreciation), depletion-related limits, and minimum-tax interactions.

3. Portfolios are rotating toward demand-aligned positions and circular platforms

Some companies appear to be repositioning their portfolios around two priorities:

- Gaining exposure to minerals and metals where demand is strengthening and where domestic supply is prioritized

- Securing harder-to-access circular feedstocks11

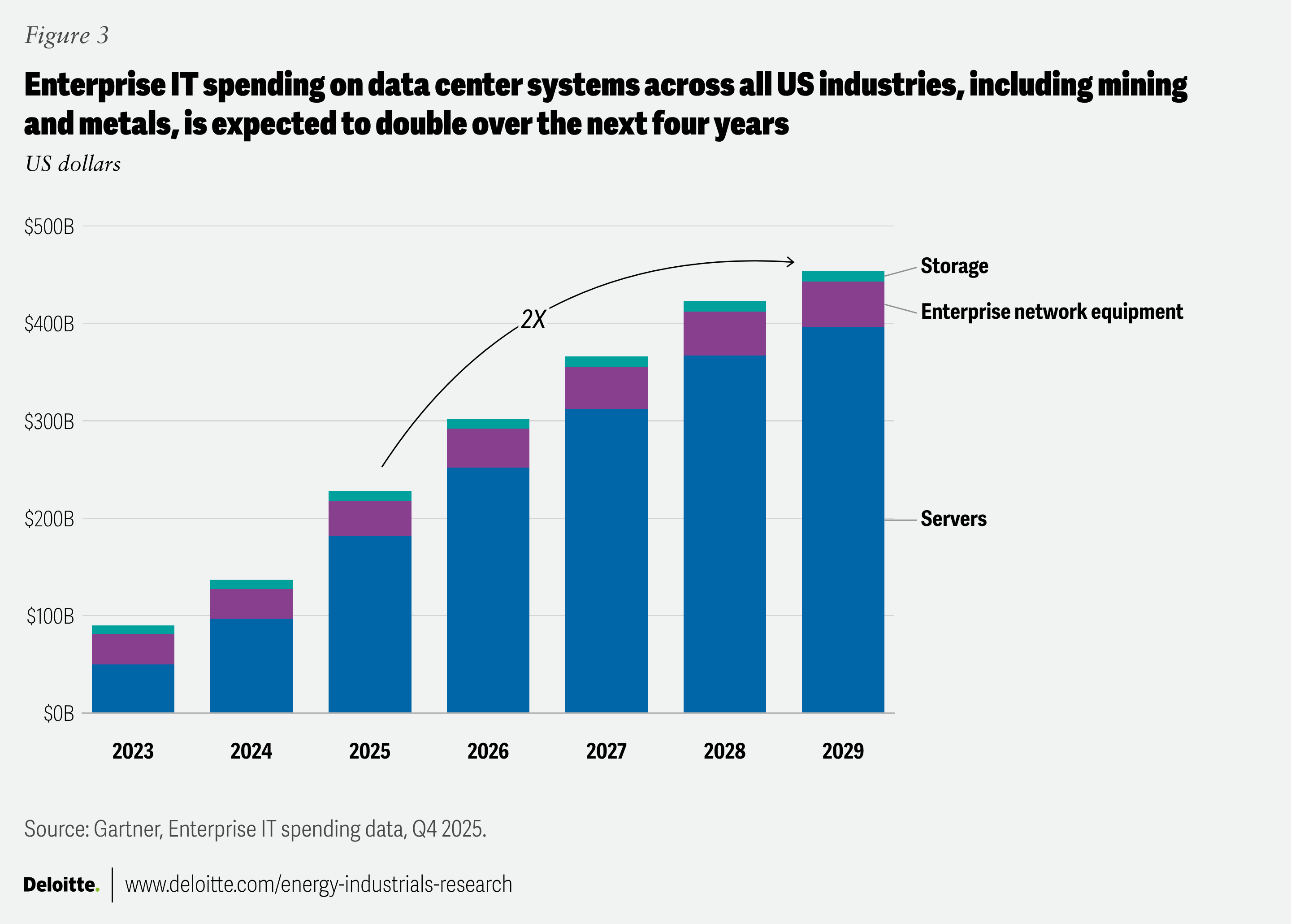

Rising data centers and AI-related infrastructure spend (figure 3) is reinforcing the investment case for copper and other grid- and battery-related materials, prompting portfolio shifts as new supply remains slow to ramp up.12 Some companies are also pursuing end-to-end value chain positions and targeted transactions to secure additional supply and new processing technologies. Funding, especially for rare earth elements, is coming from venture capital investments, including government sources.13

In steel and aluminum, circular feedstocks are increasingly being treated as strategic inputs, with emphasis on consistent, specification-grade, and traceable material that supports product quality and operating reliability.14 Policy is reinforcing the premium on domestic and traceable supply, as the One Big Beautiful Bill Act’s material-assistance requirements are expected to spur demand for US-sourced metals and minerals among taxpayers seeking to qualify for production tax credit benefits.15

Expectations for 2026

- Exposure could become more selective by mineral and pathway: Portfolios are likely to rotate from a broad “battery minerals” positioning to more explicit choices, favoring copper, lithium, and graphite pathways, while staying cautious in oversupplied markets. This can also increase the value of recovering byproducts from existing operations rather than relying only on greenfield growth.

- Circular platforms may move deeper into feedstock quality and product capability: In steel and aluminum, improved grading, sorting, and capture may increase access to specification-grade inputs and reduce quality variability. In steel, the availability of high-quality metallics (especially prime scrap) may become a tighter constraint, especially as electric arc furnace capacity expands and product requirements rise. This can increase the value of better scrap grading and blending, and greater use of direct reduced iron or other ore-based metallics to supplement scrap and meet target chemistry and product needs. In aluminum, improved sorting and alloy separation can preserve higher-value scrap streams and reduce downcycling.16 Low consumer recycling rates in some end uses may continue to constrain clean scrap supply, increasing the value of closed-loop supply, contracting, and upgrading recycling capacity.

- Rare earth value chains may see accelerated, venture-style dealmaking to build capacity: US-based companies are expected to move quickly to secure rare earth supply and processing and build end-to-end positions. With processing being complex and, in some cases, environmentally intensive, execution and permitting risk and customer qualification will be important. Many deals may include bets on early-stage processing technologies and unproven resources. Some of the transactions are also likely to focus on vertical integration, linking upstream resources with downstream activities such as separation, metal or alloy making, and magnet supply (often via direct OEM or customer partnerships) to create integrated mining-to-manufacturing entities.

4. Cost pressures demand higher efficiency from US operators

For commodity metals and minerals where prices are largely set by global markets, operational performance becomes a primary lever for protecting margins. Meanwhile, the cost and complexity of supply are rising as ore grades decline. Average copper grades have fallen by roughly 40% since 1991, increasing the value of stable throughput and consistent recovery.17 US producers face additional pressure due to structurally higher production costs (for instance, unit net costs for copper extraction are nearly twice those in Australia).18

This cost pressure has knock-on implications for US critical minerals supply, since several critical minerals (including some rare earth elements) are byproducts or coproducts of larger base-metal operations.19 If higher costs force host mines to curtail production or close, associated byproduct streams may disappear, which could reduce domestic availability of otherwise lucrative and strategically important critical minerals.

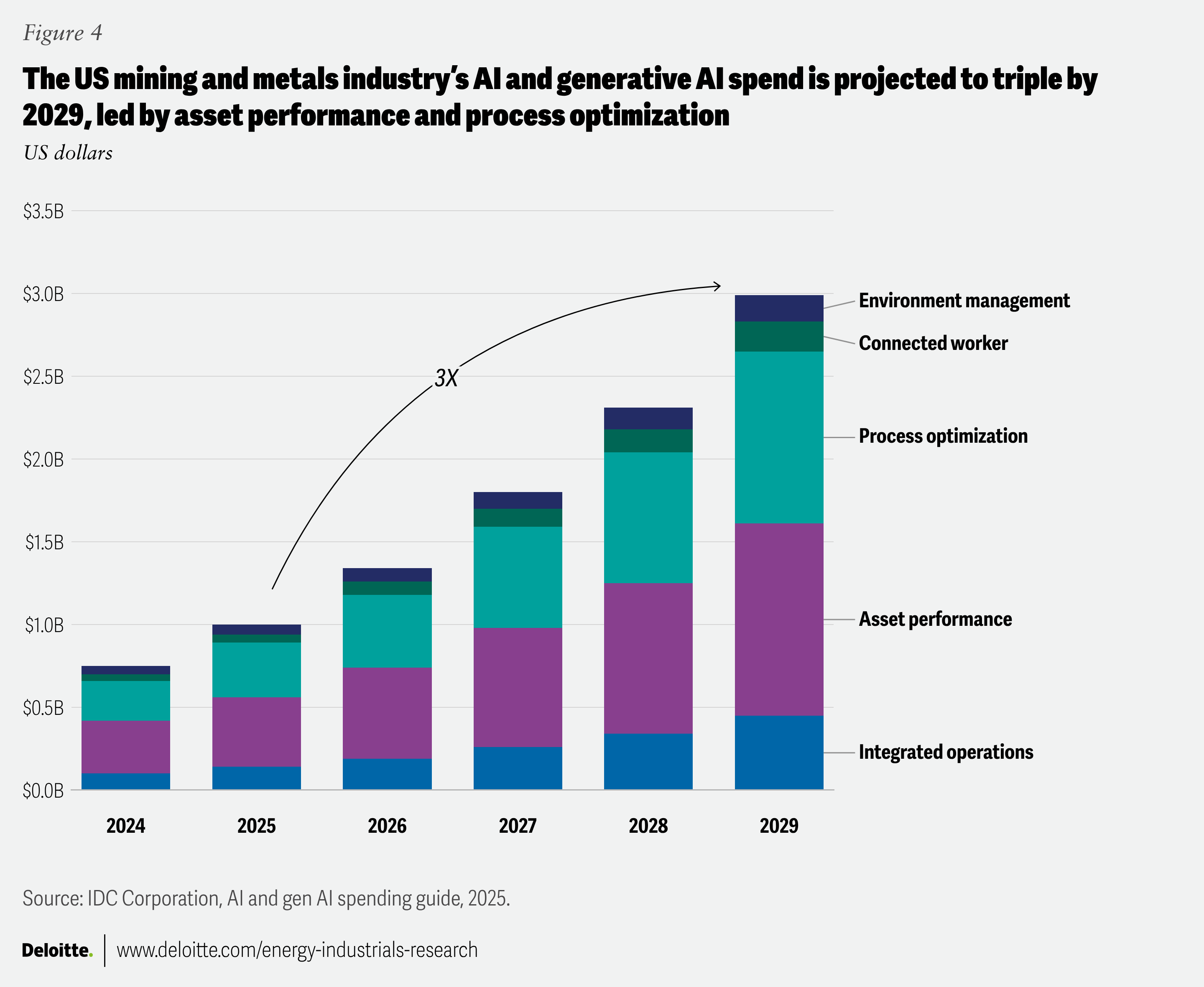

In response, some companies are deploying next-generation technologies, including artificial intelligence and generative AI (figure 4), to help reduce costs, stabilize throughput, improve recovery, and cut unplanned downtime.20

Expectations for 2026

- Mining may move from pilots to scaled operating systems: Advances in next-generation and smart operation technologies have laid the foundation to bring more resources to market. US miners targeting more complex ore bodies are expected to leverage autonomous and semi-autonomous hauling and drilling, AI-enabled process control, and predictive maintenance across fleets and sites. Adoption is likely to be fastest where operations are standardized, shifting the performance bar from proof of concept to repeatability across assets, crews, and operating conditions, enabled by remote monitoring and tighter operational governance.

- Digital technologies can help boost exploration efficiency: Exploration and recovery approaches are expected to advance through AI-enabled subsurface modeling and remote sensing, leading to faster decision cycles and improved targeting and resource definition, thereby unlocking lower-grade or previously uneconomic resources.

- Digital technologies may increase efficiency in scrap and recycling value chains: For producers exposed to scrap and recycling markets, performance differentiation is likely to come from better feedstock intelligence, sorting, and quality-control capabilities that stabilize yields under input variability. In aluminum, automation in power-intensive environments is expected to expand as operators pursue tighter control, safety, and execution consistency.

- AI may help mitigate cost volatility: Electric arc furnace mini mills represent around 70% to 72% of US raw steel production, increasing exposure to electricity cost volatility.21 With industrial electricity prices potentially rising in 2026, operators may prioritize energy-aware scheduling, demand management, and tighter process control to protect unit costs.22

- Operating model redesign may become necessary to capture value at scale: Capturing value could depend less on technology selection and more on how work is organized and governed. Companies are likely to scale workflow automation and selective agentic approaches for multistep processes (for instance, maintenance triage, inventory actions, and exception management), while keeping humans in control of safety-critical decisions. Remote operations centers and standardized digital work execution can centralize monitoring, reinforce operating standards, and accelerate interventions.

5. Workforce training and upskilling are becoming differentiators

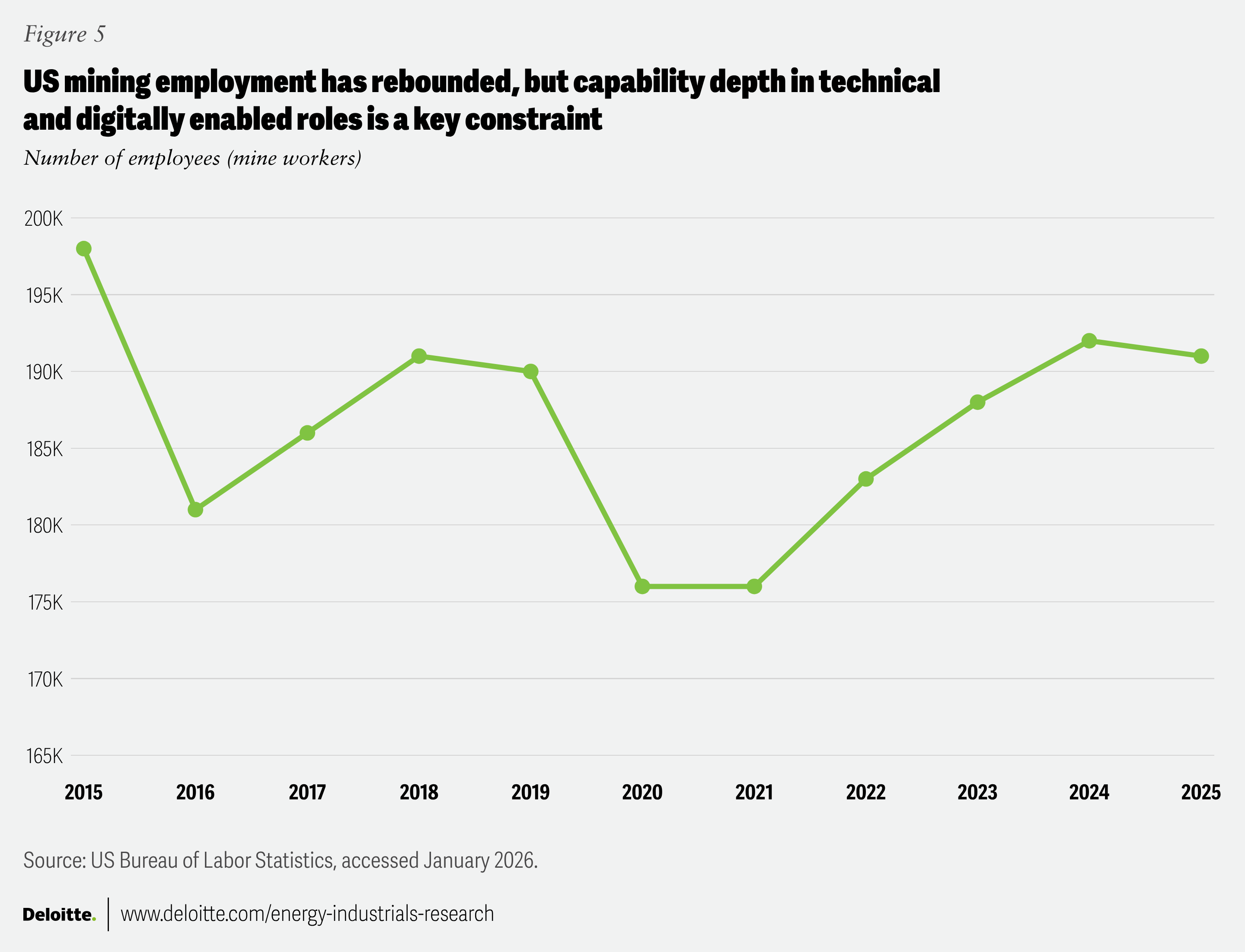

While mine employment in the United States has largely recovered to pre-pandemic levels (figure 5), some operators are struggling to fill critical roles, especially as experienced employees exit faster than organizations can train their replacements and as technical requirements increase across maintenance, process control, and operations.23 Meanwhile, the talent pipeline is weakening, with US mining and mineral engineering programs declining to decade-low graduation levels.24 Compounding this challenge is an impending retirement wave, with more than half of the US mining workforce, or about 221,000 workers, expected to retire by 2029.25 As operating models digitize, capability needs are also broadening beyond traditional frontline roles into functions that govern execution, performance management, and decision-making across sites.

Expectations for 2026

- Workforce plans could become milestone-based and tied to delivery capacity: As digital and AI-enabled operations scale, differentiation will likely increasingly come from how effectively operators manage the feedback loop between scaling technology and scaling capability. Companies are likely to shift from episodic hiring to workforce plans aligned with technology implementation and delivery timelines. The ability to mobilize integrated teams across engineering, permitting, commissioning, qualification, and ramp-up should be supported by leadership, contractors, and technical partners. Companies may also take advantage of tax credits or incentives that encourage hiring and training for the future workforce.

- AI fluency may become a baseline requirement: Demand is expected to increase for technicians who can run and troubleshoot automated systems and digitally controlled processes. Broader AI literacy and fluency are also likely to become expectations across functions, including finance, procurement, maintenance planning, and operations leadership. Trust in AI-enabled tools should extend up the management chain, supported by governance, training, and clear decision rights, so that outputs can be used appropriately and understood as productivity multipliers and not replacements for judgment. Human capabilities, including problem-solving, risk awareness, collaboration, and critical thinking, are expected to remain essential.

- Partnerships and structured knowledge can accelerate skills-based capability building: With the talent pool not scaling fast enough, operators are likely to deepen partnerships with universities, technical schools, and apprenticeship programs, while expanding internal training in priority technical domains. Some publicly financed regional innovation initiatives reinforce this approach by funding apprenticeship expansion and worker support programs tied to the lithium and critical materials economy.26 In parallel, accelerating retirements are likely to shift channels for knowledge transfer away from static training manuals and playbooks toward real-time knowledge management, enabled by data and AI platforms.

Looking ahead

The US mining and metals industry faces a pivotal moment as global trends, policy shifts, and rapid technological change reshape competitiveness. To help navigate this environment, operators may increasingly:

- Leverage the broadening array of policy and financing tools to address value chain gaps. Where markets are illiquid or less transparent, these approaches, combined with strong offtake arrangements, can speed commercialization.

- Prioritize demand-aligned metals and circular platforms, and secure partners that help speed qualification and commercialization.

- Move beyond fragmented, value chain-specific pilots to an integrated digital approach, accelerating exploration technologies while scaling smart operations to improve efficiency and agility across the value chain.

- Align workforce planning with organizational initiatives to digitize and automate certain processes. Enable real-time knowledge transfer through digital tools and build AI literacy while keeping human judgment central.

Continue the conversation

Meet the industry leaders

John Diasselliss

Samrat Das

Cole Johnson

Brett Scodova

Kate Hardin

Abhinav Purohit

by

John Diasselliss

Samrat Das

Cole Johnson

Brett Scodova

Kate Hardin

Abhinav Purohit

The authors would like to thank Anshu Mittal and Ashlee Christian for their extensive contributions to this report, including their input in narrative development.

The authors would also like to thank Brad Johnson, Richard Longstaff, Ivan Kozak, John O’Brien, Kristen Hooks, Carissa Kilgour, Andrew Thompson, Kelsey Carvell, Steve Flagg, Lindsey Ferrara, Ryan Meyers, Aaron Uddin, Philip Hueber, Kate Keller, and Susanna Samet for their subject matter input and review.

Finally, the authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Katrina Drake Hudson and Dario Failla, who drove the marketing strategy and related assets to bring the story to life; Kaitlin Pellerin for her leadership in public relations; Rithu Mariam Thomas, Aparna Prusty, and Pubali Dey from the Deloitte Insights team, who edited the report and supported its publication; and Harry Wedel for the visual design.

Editorial (including production and copyediting): Rithu Thomas, Pubali Dey, Aparna Prusty, Aditi Rao, Cintia Cheong, and Anu Augustine

Design: Harry Wedel and Molly Piersol

Cover artwork: Sanaa Saifi and Adamya Manshiva

Knowledge Services: Rishitha Bichapogu

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.