Delivering on space development growth

The space industry could be worth US$800 billion by 2027, but it must tackle multiple issues, like regulatory reform and space debris, to sustain this growth

Today, the space industry is expanding at a steady pace, offering benefits to countries and citizens around the world. A thriving space economy contributes to technological progress, economic growth, and strategic advantages. For example, innovations such as the Global Positioning System—developed in the United States—have become a catalyst for global economic progress.1

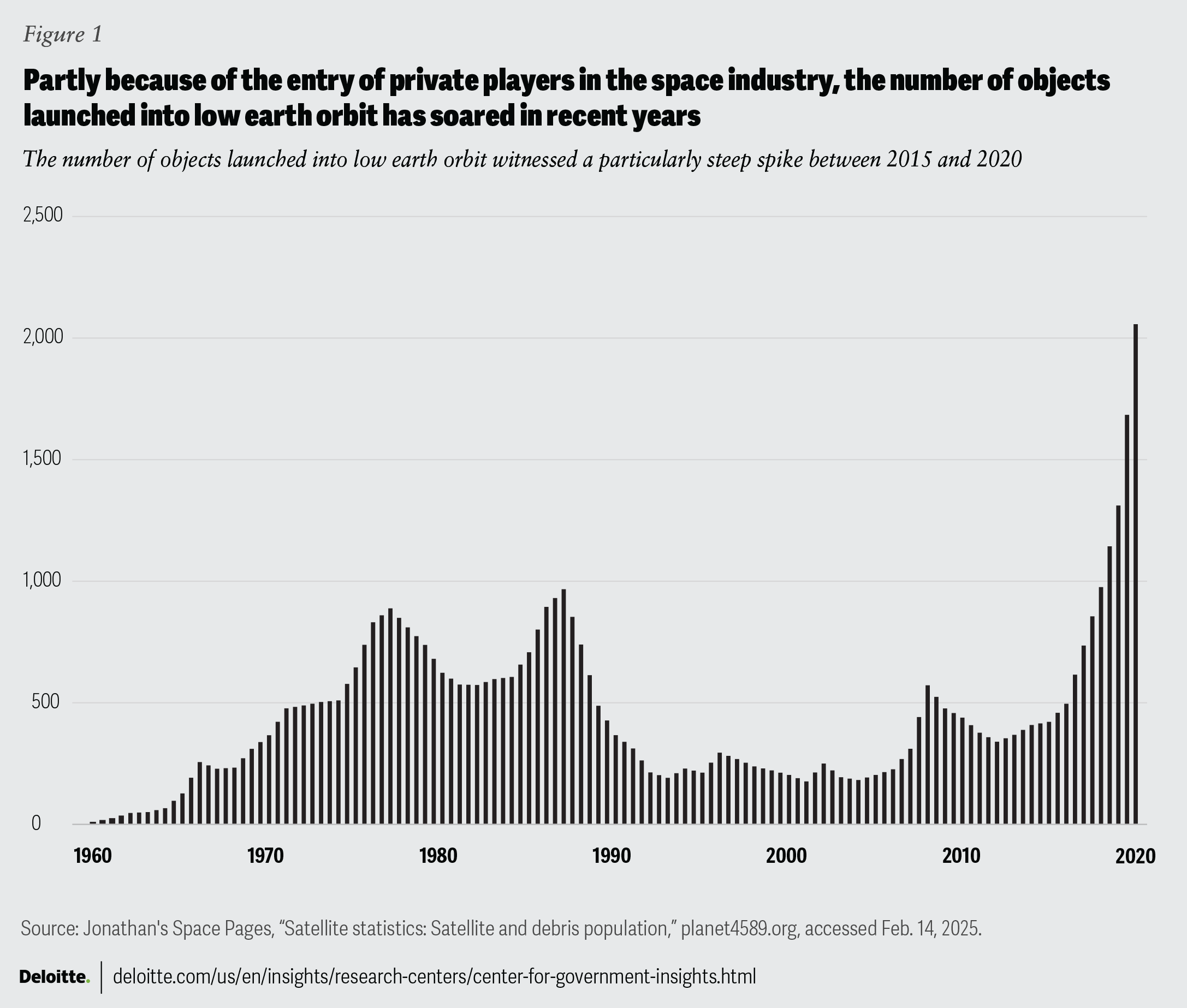

Many countries are increasing their investments in space exploration because of the advantages it provides, leading to more collaborations and advancements in space technology. Between 2007 and 2022, the total value of space activities worldwide more than doubled, and some estimates suggest that the value could reach nearly US$800 billion by 2027. Meanwhile, the total number of objects launched into orbit each year has surged (figure 1).2

Space-based technologies and services are important across various sectors—from agriculture, finance, and transportation to weather monitoring and insurance—and the economic opportunities are expanding as well. New space activities, like in-orbit manufacturing, hold an additional promise for more growth and new innovations.

{kind=link}

More than the economic benefits the space industry provides, a military’s sophistication can be measured, in part, by its space capabilities. Modern military operations across the globe rely on satellite-based communications, navigation, and intelligence services. The importance of space capabilities for military operations has been, and will continue to be, a source of fuel for industry growth.

However, commercial and government pursuit of a larger and more capable space industry can also present challenges that could stunt progress. The government will need to balance industry growth against potential industry challenges, like the possibility of losing access to critical earth orbits due to space debris or military conflict that extends into space. The benefits of a robust space sector are growing as new space industry innovations, like larger launch vehicles, more sophisticated earth-imaging satellites, and entirely new activities, like manufacturing in orbit, mature. The opportunity for governments and industry is there for the taking.

Key challenges

- The investor calculus is changing. Several years of what appear to be overly optimistic industry projections have led to less-attractive returns for some investors, encouraging greater risk aversion and a better understanding of the space industry's investment dynamics.

- Crowded orbits may threaten access. Space development has come at an environmental cost in the form of space debris.3 Left unchecked, mounting space debris could close off access to critical earth orbits.

- Competition intensifies. More than the expected economic competition for new space industry markets or innovations, geopolitical competition has added a layer of complexity to space industry growth. Some countries are searching for ways to bolster military space technologies without creating additional geopolitical insecurity or threatening access to earth orbits.

- International cooperation is necessary but can be harder to come by. Whether developing international rules for space traffic or expanding commercial markets, international cooperation can help deliver space development, but political tensions can make increased and sustained cooperation more difficult to develop.

Trend in action

Driving space innovation through public-private partnerships

Innovation in the commercial space sector is reshaping the understanding of the planet and enhancing everyday life. Large constellations of commercial satellite broadband networks provide globally accessible internet, connecting communities around the world and aiding national security. In fact, they’ve proven so important that countries are racing to deploy their own versions of them. The European IRIS2 program plans to improve connectivity for governments and the private sector.4 Other systems, like the "Thousand Sails" satellite constellations, seek to provide similar capabilities in Asia.5

Indeed, while commercial companies are often in the spotlight for their innovations, governments, through space agencies and ministries or departments of defense, are working hard to catalyze private sector innovation. In the United States, for instance, NASA is playing a key role in catalyzing low earth orbit destination markets through its Commercial LEO Destinations program.6 In India, the Indian Space Research Organization is encouraging private space sector growth through technology-transfer agreements and has recently added another 75 such agreements to a quickly growing list.7

Closer public-private partnerships between governments and commercial space companies are an important feature in today’s space industry because they often benefit governments and the private sector equally. Many pioneering projects, like the International Space Station, laid the groundwork for further commercialization, and today, private companies can build on initial governmental efforts by delivering more affordable and innovative space services that governments require, including crewed spacecraft and national security support.

Industry growth to date has already reshaped perceptions of roles and opportunities in space, and more innovation is on the way.

Moving beyond traditional space activities

Historically, investments have concentrated on traditional industry areas like launch services, satellite communications, and earth observation. While these remain critical, unlocking entirely new markets can require the development of novel technologies and services. Emerging areas such as in-orbit servicing, assembly, and manufacturing (ISAM); space traffic management; space debris remediation; new military capabilities; and ambitious civil space programs (for example, the Artemis program in the United States or the Chandrayaan family of lunar missions in India) can open entirely new opportunities for industry growth and innovation.

Many of these new markets are the product of years of public-private partnerships. For instance, in-orbit facilities, such as the International Space Station have been used to manufacture pharmaceuticals, semiconductors, and even human-grade knee cartilage through partnerships with national space agencies like NASA.8 And new space companies are leveraging those lessons learned to develop commercial products, like making pharmaceuticals in orbit and returning them to Earth.9 Other instances of initial government investment spurring commercial products and services touch nearly every space industry sector.

The promise of these new activities is often why governments and the private sector are closely collaborating. Take in-space servicing, for example: The governments of Japan, the United States, the United Kingdom, and other countries are investing alongside private sector investors in commercial space companies that are developing entirely new ways of servicing satellites in orbit and cleaning up space debris.10

These new activities and associated markets can help the industry move beyond familiar sectors, such as satellite communications or imagery, to sectors that offer new ways of exploring and developing space. For example, as in-space servicing and assembly technologies progress, they could unlock different ways of building more affordable and sophisticated satellites in orbit, like larger scientific telescopes or even manufacturing facilities. However, advancements in these emerging fields are not guaranteed.

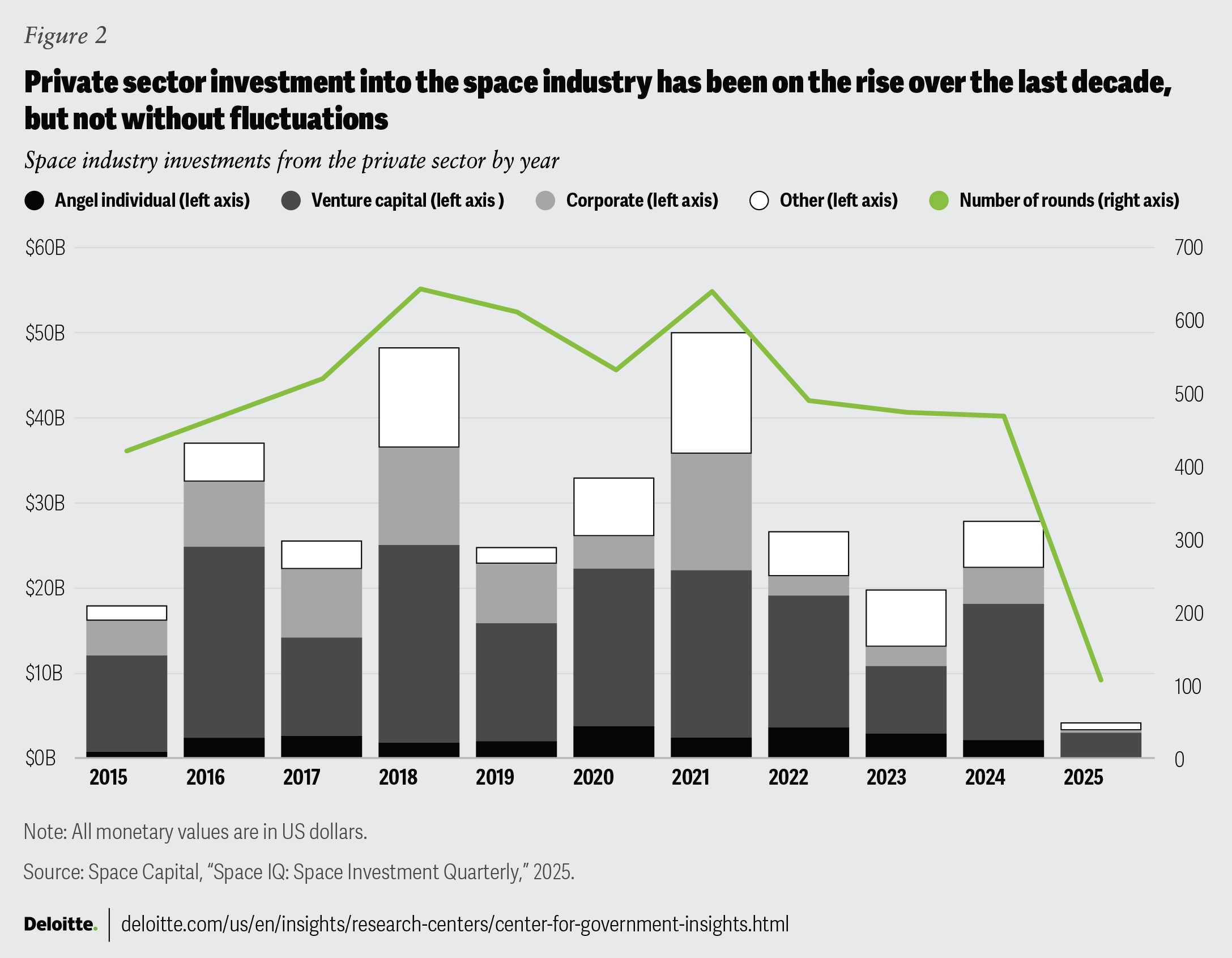

Maintaining momentum in the global space sector should include thoughtful collaboration and sustained investment from both governments and the private sector. Recent cycles of private investment—from venture capital to private equity—have sometimes followed overly optimistic forecasts characteristic of a growing industry.11 Investment levels dipped in 2022, reflecting a more cautious climate after some investments underperformed, but recovered in 2023, with around US$12.5 billion raised—albeit still below previous peaks (figure 2).12 This evolving investment landscape may suggest that investors are gaining a clearer understanding of how to minimize investor risk while trying to spur industry growth.

{kind=link}

At the same time, government spending is up globally (figure 3). The increase in government investment is likely due to a renewed appreciation for the economic, scientific, and national security advantages afforded by space technologies. Disparities in government budgets also reflect an enduring reality: Space exploration and development continue to be a financially expensive endeavor. While new innovations in launch services and electronics have driven down costs in recent years, developing, deploying, and operating large numbers of commercial or government space systems in orbit continues to be an activity for relatively few countries. However, commercial products and services and government partnerships have expanded access to space technologies and services to more countries.

{kind=link}

Though the space industry is growing, and signs suggest that it will continue to do so, industry growth is not without prominent challenges. Three major ones are governance, space debris, and geopolitics.

International governance of space

Earth’s orbits are a shared space, the providence of mankind.13 While some international agreements formed in the 1960s and 1970s provide some guidance for activities and behaviors in orbit, more clarity is needed on the international rules for space exploration and development.14

Take managing space traffic, for example. The surge in satellite deployments—with more than 11,000 active satellites currently15—has led to unprecedented congestion in Earth’s orbits. With active satellites now accounting for over half of all payloads ever launched and predictions estimating up to 20,000 satellites in orbit by 2030, the risk of collision and interference continues to grow.16 Importantly, many of these satellites are part of constellations and are intended to be replaced with upgraded versions every few years, which increases space traffic as satellites are deorbited and substituted.

Between 2021 and 2022, reported close approaches between satellites increased by 58%, spotlighting the urgent need for comprehensive space traffic management systems.17 Yet, with the growth in orbital use occurring internationally, space traffic cannot be managed solely at the national level. There will need to be an international agreement about how satellite operators manage traffic, just as there are international rules for managing civil aviation or shipping traffic.18

Between 2021 and 2022, reported close approaches between satellites increased by 58%, spotlighting the urgent need for comprehensive space traffic management systems.

Data about where spacecraft are in orbit is a critical piece of managing space traffic, and some countries are working together to acquire and share space situational awareness data. Through the Traffic Coordination System for Space program, the US government aims to provide a better way of collecting and sharing space situational awareness data for commercial and government operators.19 The European Space Agency and other countries also have programs designed to track and catalog space objects to help manage space traffic.20 Although data-sharing is increasing, cooperation between countries is required to use that data to manage traffic most effectively.

Beyond managing space traffic, new international agreements covering a host of emerging space activities can help pave the path of space development and safeguard commercial and national security interests in space. Addressing these challenges requires robust international cooperation and the establishment of global norms and other international agreements. Initiatives like the Artemis Accords—led by the United States but embraced by a growing number of international partners—illustrate how collaborative efforts can set standards for responsible space exploration and use.21 Developing these rules becomes more pressing when considering the challenging state of space debris.

Addressing the proliferation of space debris

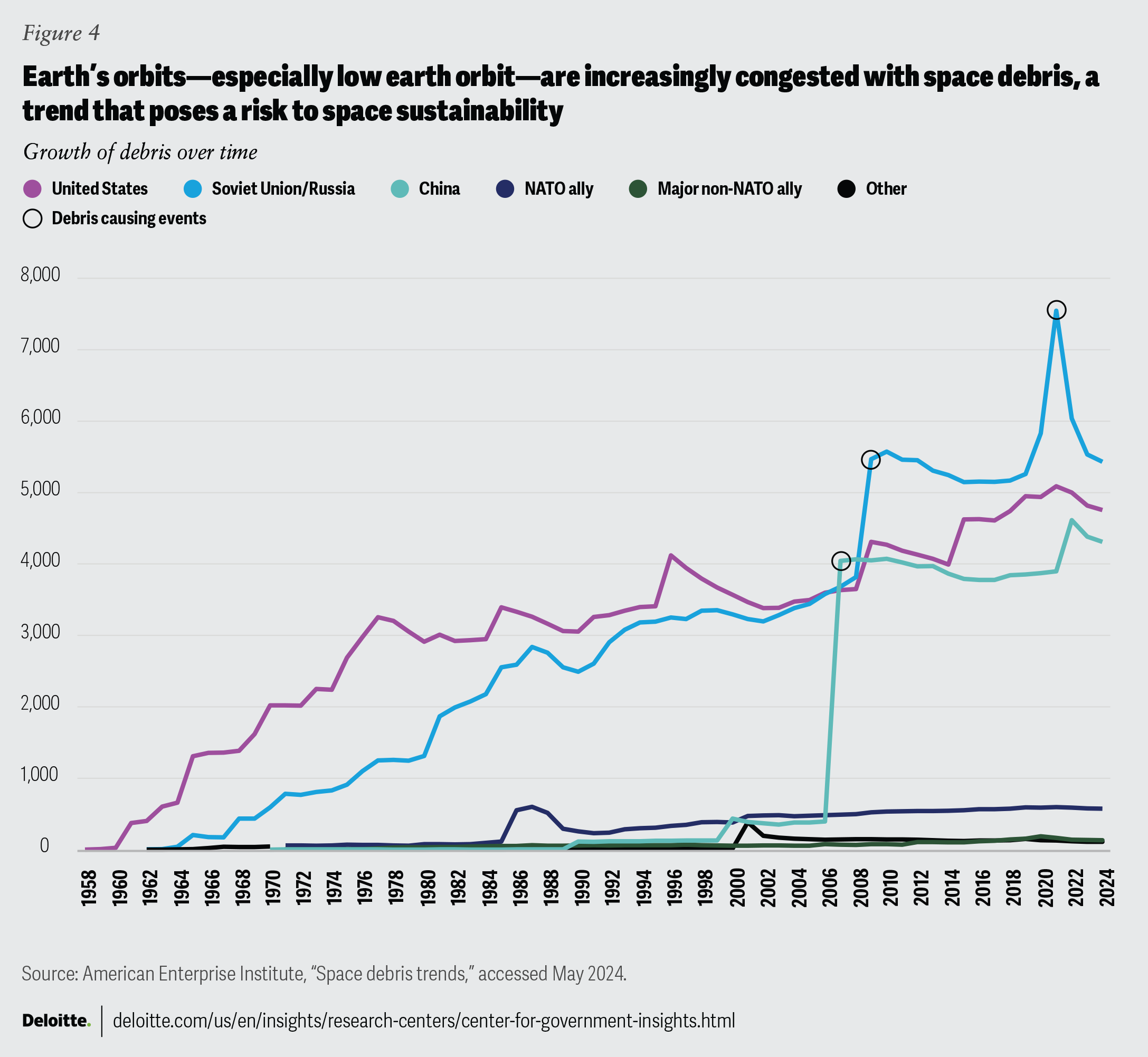

The rapid growth of the space industry has created junk in orbit, which exacerbates orbital congestion challenges and increases risks to satellites. Space debris—ranging from defunct satellites and spent rocket stages to fragments from satellite collisions—poses risks for operational spacecraft and vital services. There are tens of thousands of pieces of debris in orbit currently, and more than half of this debris is concentrated in low earth orbit, the region where most commercial activities occur (figure 4).22 In early 2024, a near-miss between space debris and a non-maneuverable satellite underscored the potential for catastrophic collisions that could generate thousands of additional debris fragments, further cluttering Earth’s orbits and endangering active satellites.23

{kind=link}

These issues are recognized globally. The United Nations Committee on the Peaceful Uses of Outer Space has produced guidelines intended to limit the creation of debris, and many countries have national regulations intended to do the same.24 Yet, solutions to date only address part of the problem.

Some governments and companies are taking action to reduce the creation of new debris, but there is currently no means of actively removing existing debris. Efforts are underway by several governments and companies to develop the technologies to do so. For example, the Japanese Aerospace Exploration Agency’s Commercial Removal of Debris Demonstration mission leverages a partnership with private space companies to develop debris removal technologies.25 Similar public-private partnerships to address space debris are ongoing in Europe and the United States. Of note, many of the technologies needed to remove debris from orbit are the same technologies found in ISAM activities, which means investments in ISAM can both expand access to new markets and help preserve the markets that already exist.

Geopolitical competition in space is heating up

Historical precedents, such as the Cold War space race beginning in the 1950s, show that competition can stimulate rapid progress. Today, geopolitical competition is helping to stimulate growth in the commercial space sector as governments seek new innovations and ways of addressing national security needs through private sector companies. However, racing to capture markets and to develop new military technologies can also create tensions in the space industry.

Space holds strategic military value, providing critical national security capabilities such as communications, intelligence, early warning, and navigation. For decades, military space systems—once developed in relatively low-risk environments—have contributed to national defense. In recent years, however, as more countries improve their space technologies, existing assets have become more vulnerable to threats ranging from electronic warfare and cyber interference to direct kinetic attacks.26

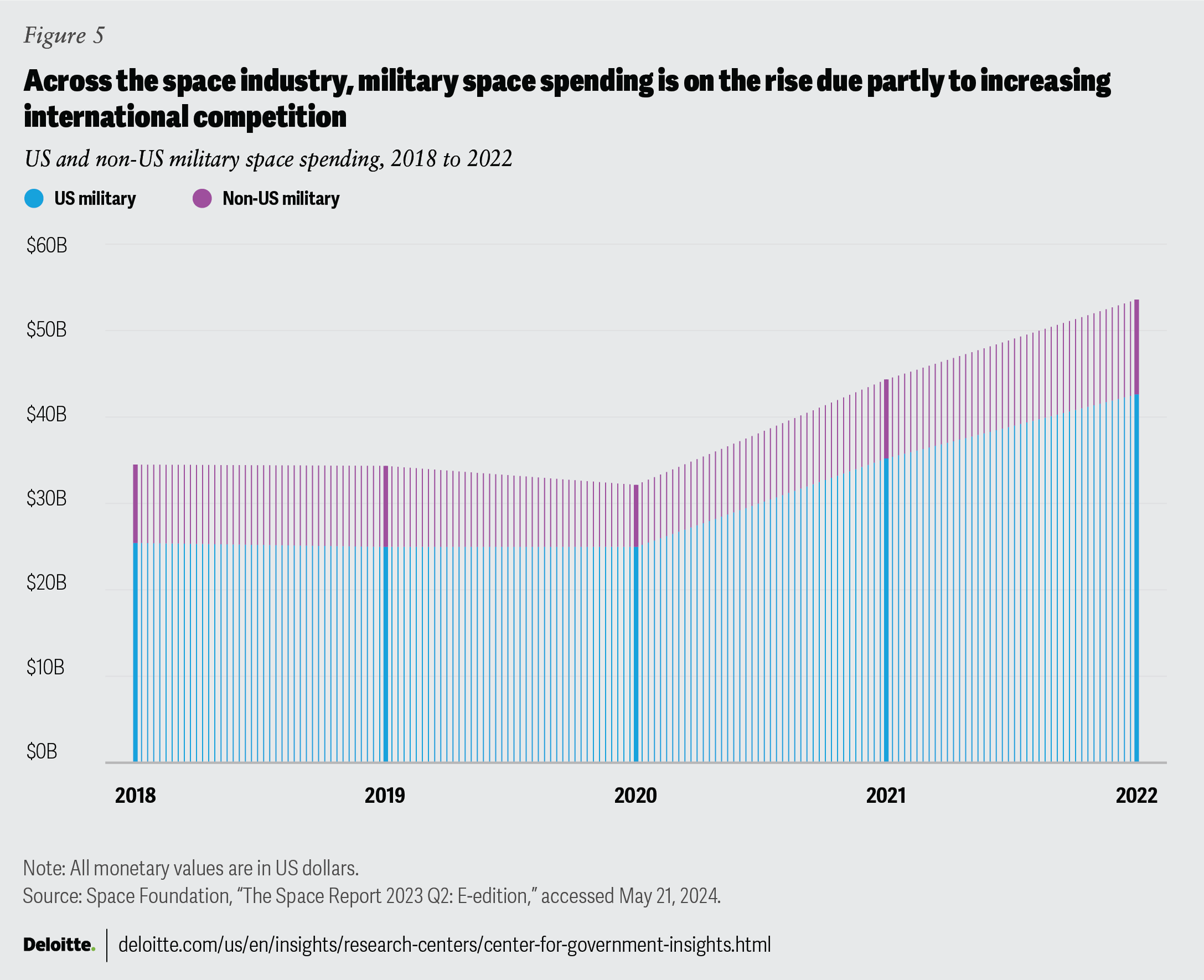

Similarly, as novel space activities increase, it can lead to uncertainty regarding their intentions. Unfamiliar space activities can also create additional risks of military escalation.27 Indeed, there have even been reports of military “dogfighting” satellites in orbit (similar to aircraft dogfighting in combat).28 Evidence of countries placing greater importance on space assets for national security is reflected in recent global budget increases for military space programs (figure 5).

{kind=link}

Economic competition for space industry markets and even space-based resources can also create tension within the industry. For example, some developing countries worry about their ability to compete in an important industry compared to more developed nations.29 For these countries, capturing value from the space industry can involve deciding between purchasing space services from foreign providers—an often easier and more affordable option but one that makes them a customer—and devoting more of their resources to developing and operating their own satellites and systems to capture their own customers. The choice can require what may be difficult trade-offs, but it can also be a source of industry innovation or advantage. For example, some developing countries have presented more affordable options for developing space systems than more developed countries. Take, for instance, how the Indian Space Research Organization has managed several accomplishments with lunar and Mars exploration programs at a fraction of the costs spent on similar missions by more developed countries.30

The number of industry stakeholders is increasing dramatically. Today, numerous countries, companies, universities, and other entities have spacecraft in orbit.31 This means that a military conflict that extends into space would likely affect not just a select few government satellites but also possibly thousands of satellites from around the world. For instance, as competition for markets and military advantages encourages the development of large constellations of thousands of communications and other types of satellites, it could add to the congestion and debris challenges that affect other space actors as well. 32

Expanding the commercial space sector could help reduce the likelihood that military actions in orbit leave lasting effects that foreclose access to important Earth orbits, though it’s no guarantee. Emphasizing the economic benefits of space could raise the threshold for engaging in certain types of military actions, like those that cause space debris, because doing so could create an indiscriminate risk to space assets, meaning the country that created the debris would also likely be affected by it. Additionally, establishing certain norms of behavior for military space activities and clear lines of communication could help to avoid confusion that could lead to unintentional escalation. One example of a positive norm of behavior that is gaining international support is the United Nations’ proposed ban on debris-generating anti-satellite weapon tests.33

Tools and strategies to deliver on space development growth

Looking forward, governments can consider several actions to foster industry growth, including:

- Synergistic investment: Combine private sector funding targeted at traditional space activities with government investment in promising emerging areas like space traffic management, debris remediation, and in-space infrastructure. Public funds can bridge the gap until these technologies become commercially viable.

- International market collaboration: Strengthen global partnerships by developing stronger commercial relationships for existing industry markets and emerging ones. This cooperation can spur innovation and also provide a platform for creating robust international norms and standards.

- Specifically, these collaborations should include developing tools and resources to provide foreign companies with information about national processes, regulations, funding opportunities, and other relevant aspects to help them bring their technology to countries with investment opportunities and markets.

- Governments should also consider how to establish consistent, long-term investment demand to facilitate the flow of more private capital into the system.

- International governance to preserve access: Additional international agreements focused on space debris and space traffic management are necessary. These efforts should be inclusive of like-minded countries, but developed to evolve quickly with changes in technologies and governance needs.34

- Balancing military and commercial objectives: Champion the economic benefits of space—and the promise of an ever-more-beneficial industry—to help balance the development of commercial space capabilities with military objectives.

- Establishing norms of behavior and open lines of communication: Norms of behavior for avoiding military miscalculation and escalation could focus on distinguishing between commercial and military behaviors to ensure commercial activities aren’t confused with military actions. Similarly, clear lines of communication between private sector operators and governments and between governments could expedite the sharing of important information and offer a chance to clarify where confusion may be present.

The space industry is on a growth path. Whether that path remains straight and smooth or indirect and bumpy depends on how governments nurture emerging space markets and balance commercial development with potential challenges stemming from geopolitical competition. Of course, the private sector has a role to play as well. Bringing these factors together will require focused government time and attention, but the payoff—delivering on space development growth—will be worth it.

By

Brett Loubert

Jason Bender

Ryo Katagiri

Adam Routh

The authors would like to thank Deloitte Insights editorial and design team, including Aparna Prusty, Rupesh Bhat, Pubali Dey, Arpan Ku. Saha, and Kavita Majumdar, for their expertise and support in publishing this article.

Cover image by: Sofia Sergi; Getty Images; Adobe Stock

Visit the Deloitte Center for Government Insights

Access more insights for the defense, security and justice, government health care, state and local government, transportation and infrastructure, human services, and higher education sectors.