Self-driving cars are on the way—is your city ready?

State and local officials have the power to determine how AVs can best enhance their cityscapes

Anant Dinamani

Jeff Hood

Rodolfo Dominguez

Tiffany Fishman

Autonomous vehicles are here, but uncertainties remain

Autonomous vehicles have arrived on the streets of American cities and are making their way to more. Over the last decade, massive investments are taking shape in the form of robo-taxis and self-driving delivery vehicles, with more mobility options on the horizon. Now it’s up to policymakers and regulators to work out how autonomous vehicles may figure into the future of their cities.

Different approaches will yield different outcomes, and thoughtful planning and regulation are essential: No one wants flotillas of aimless AVs cruising city streets already choked with cars, bicycles, pedestrians, scooters, and e-bikes. State and local leaders need to determine their key objectives—such as fewer crashes, less parking demand, improved air quality, less congestion, and economic development—and how AVs can contribute to achieving them. A simulation done by the International Transport Forum illustrated how a large-scale deployment of shared vehicle fleets that provide on-demand transportation in a midsized city could eliminate congestion, reduce traffic emissions by a third, and require 95% less space for public parking.1 Leaders should aim to understand the ways in which these vehicles—if introduced and overseen effectively—have the potential to reshape urban navigation for the public good.2

Many questions remain unanswered in a dynamic mobility ecosystem, with technology rapidly changing and new players emerging as others exit the market. After a number of widely reported incidents, advocates have far to go in convincing the public at large that AVs can be safe and beneficial,3 and some major companies have pulled back on their planned investments. There’s still plenty of skepticism among consumers, regulators, and the various ecosystem players.4 And the unknowns have led some states and cities to wait for San Francisco, Phoenix, and other early AV adopters to work out the kinks.

The new administration appears to be supportive of a favorable regulatory environment that will accelerate AV adoption.5 Moreover, manufacturers have solved some of the stickiest technical problems, and increasing visibility will likely boost acceptance, although grudging at first. All in all, the AV question has largely shifted from “Will it happen?” to “When and how will it happen?”

How AVs can benefit cities

Cities stand to reap the benefits of AV deployment—with some already observed in tests and early operations and others expected with broader deployment. Some of the potential benefits include:6

- Safety: By removing human biases and driver errors, autonomous systems drive more reliably and improve safety for passengers and surrounding traffic: 85% observed a lower likelihood of Waymo AVs being involved in an injury-causing crash than the human-driving benchmark (upon analysis of 7 miles of Waymo AV operations in California and Nevada).7

- Economic and social: Automated mobility improves freight efficiencies, avoids costly interruptions (that is, crashes), and releases personal vehicle–oriented land uses. An estimated US$75 billion of potential annual economic savings can be achieved from reduced traffic incidents, along with associated injuries and fatalities—under a scenario with a 25% adoption rate of “standard” AVs.8

- Efficiency and convenience: AV platooning reduces congestion and returns time to roadway users. Forty percent observed reduction in fuel consumption, as well as 15% increase in vehicle throughput, due to the impact of AVs optimizing traffic flow and dissipating stop-and-go traffic patterns (achieved when AVs are just 5% of the overall fleet mix).9

- Mobility: AV systems carry enormous potential to reach seniors, people with disabilities, and other populations previously limited in personal mobility. There was approximately 10x estimated improvement in access to jobs, health care facilities, and education due to the impact of shared AV taxi and micro-transit fleets, measured by the ratio between the locations accessible in 30 minutes to the 10% best-served person to the 10% worst-served person.10

How city and state leaders can help prepare for AV deployments

Right now, there’s a stubborn gap between capabilities and trust.11 But government agencies and other industry participants have an opportunity to help close that gap through collaboration and transparency. In crafting regulatory guardrails and policy guidance, officials are likely to achieve their desired outcomes by proactively engaging the full range of stakeholders.

While responsibility for establishing testing standards lies with federal regulators,12 it is state and city policymakers and regulators who have the authority to draw a road map for how a region’s citizens can best realize AVs’ benefits. As government embraces the next generation of community-facing technologies, their success—including that of AVs—is achieved when leaders bring to the forefront the fundamental needs and priorities of communities themselves.

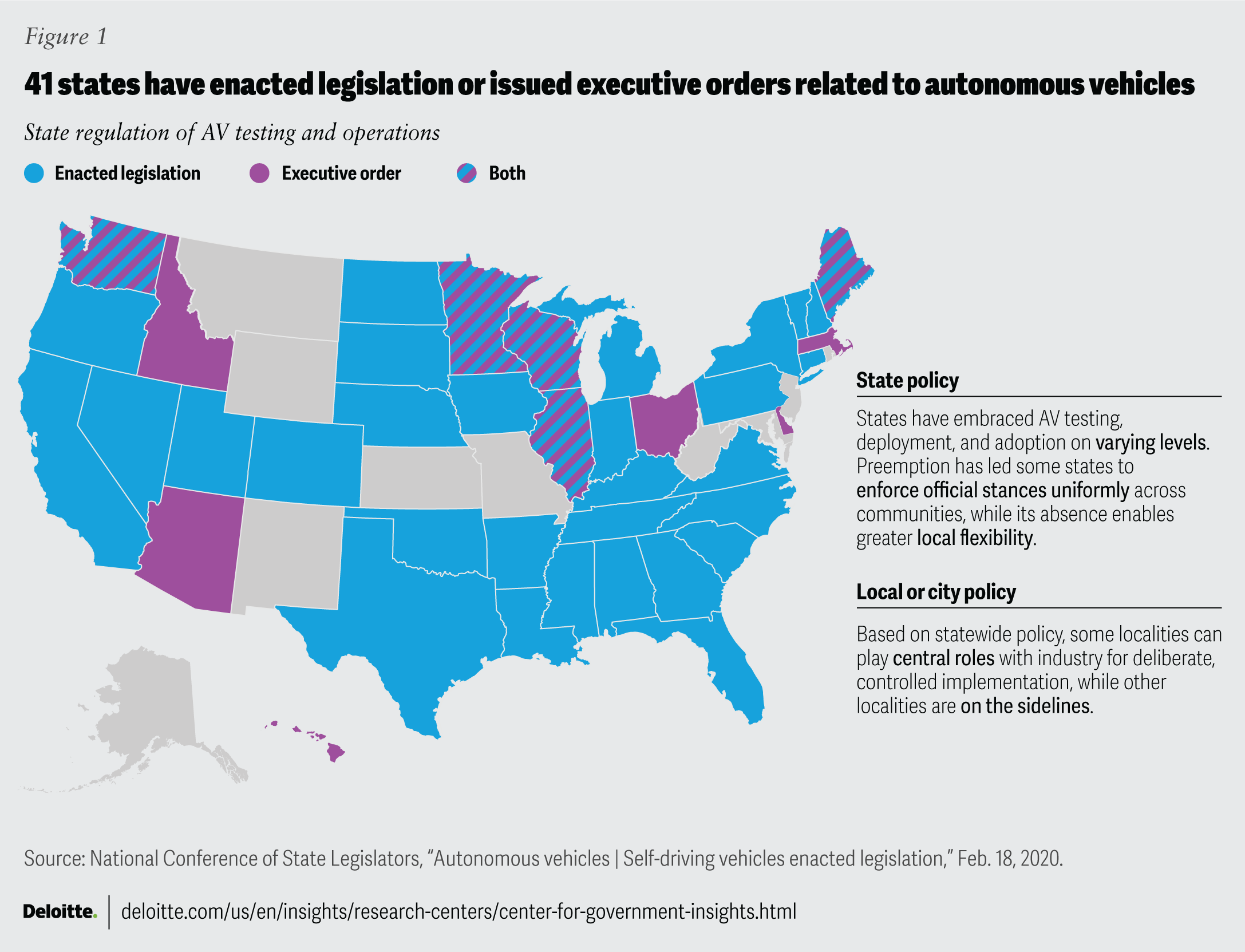

Most states have passed AV legislation, largely focused on testing (figure 1): Twenty-five states explicitly allow for some level of AV deployment. While many of these state statutes permit testing on public roads, they often have their own individual nuances to address the particular needs, habits, and geographies of their jurisdictions and constituents. Within those states, early-adopter cities have taken different routes to make their streets safe for AVs, showing a range of possibilities for policymakers looking to create optimal deployment conditions.

{kind=link}

Whether focusing on shared or individually owned AVs, ride-hailing, or package delivery, short commutes or long road trips, state and city leaders can explore policy options to avoid having other ecosystem players impose a future that may be far less aligned with their objectives. Consider how municipalities had to scramble to address the disruption of ride-hailing services after citizens had made those companies wildly popular.13

Jeff Farrah, chief executive officer of the Autonomous Vehicle Industry Association, observes that companies’ attitudes have shifted, as they move past early pilots toward broader deployment. “Rather than viewing the regulatory void as a license to operate, they now desire clear legislation or testing regimes,” says Farrah.14 With AV innovations and commercial partnerships bringing technology ever nearer to more people, state and local governments have the opportunity to achieve the outcomes they want by designing a holistic regulatory and stakeholder engagement approach. Firm leadership—and a well-planned road map—can allow cities and states to harness the power of AVs to better constituents’ lives now and in the future.

Who’s (not) driving today: Where AV usage stands

Since 1983, when the US Defense Advanced Research Projects Agency launched the Autonomous Land Vehicle program, as part of its Strategic Computing Program AI initiative, public sector institutions have helped guide several waves of AV technological breakthroughs. Along the way, corporate investments have gathered momentum, through the first commercial autonomous ride-hailing vehicles in 2018,15 and legacy automakers competing with tech giants to make AVs ready for city streets.

Recently, some large companies and investors have accelerated capital spending,16 even as others have tapped the brakes in favor of other tech horizons, particularly generative AI.17 Chinese investors have overtaken their US counterparts in funding the sector.18 And with AI applications expanding, some mobility startups are attracting unexpected investment.19 Overall, AV investment is expected to grow from US$57 billion in 2021 to upwards of US$788 billion by 2028.20

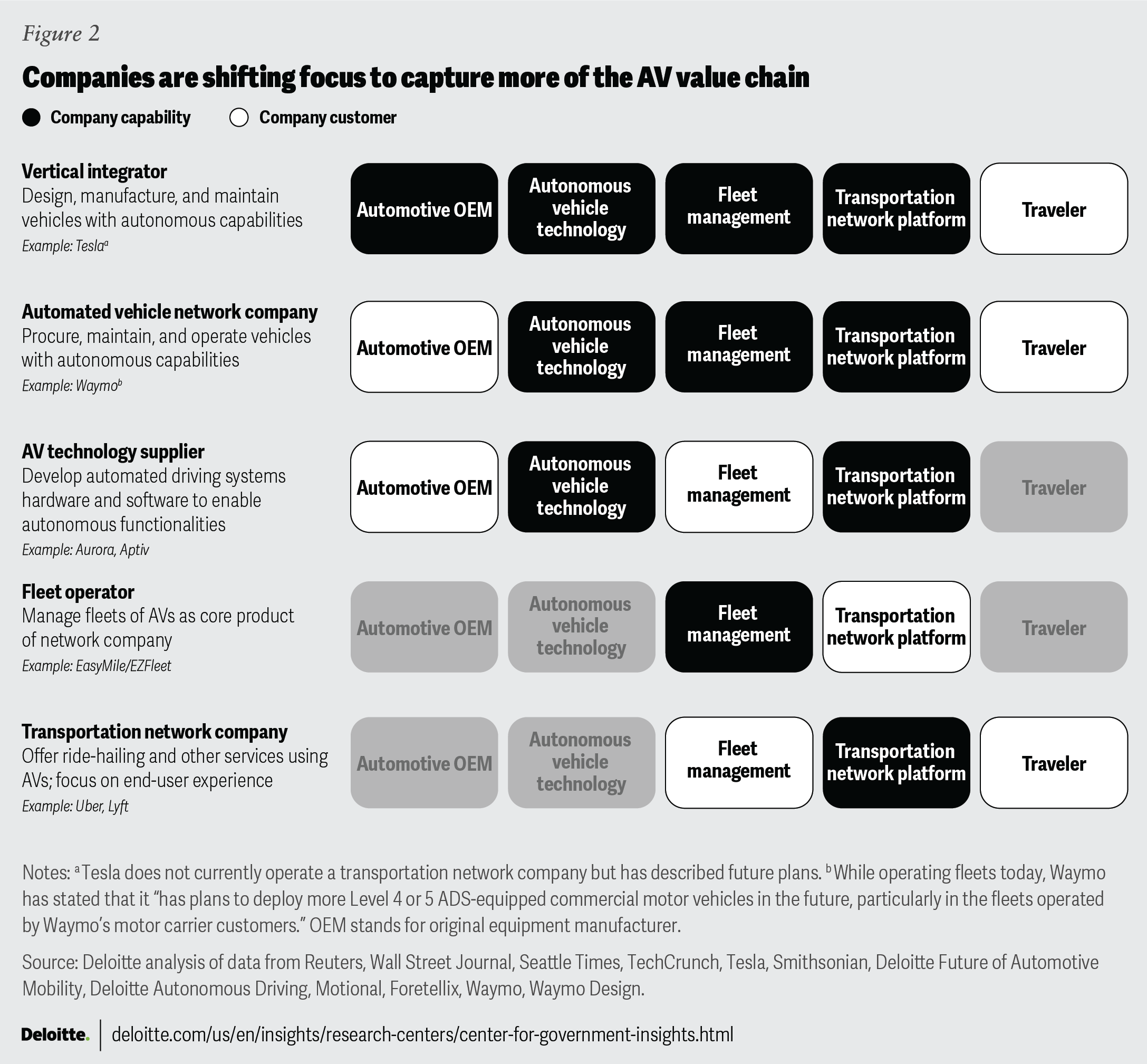

Today’s AV landscape, then, is a little unsettled, with players regularly entering and leaving the mobility ecosystem, and those that remain exploring a range of different business models (figure 2). Policymakers have had to regularly reassess who their private sector partners are, and what vehicles and technologies those partners might be looking to introduce—including what degree of autonomy future AVs might feature (see “How autonomous is autonomous?”). But analysts see renewed momentum in the “autonomy economy,” with more investments and skyrocketing market size,21 despite tepid growth forecasts for US autonomous vehicle sales over the next decade—a market share of less than 1.5% by 2034.22

{kind=link}

How autonomous is autonomous?

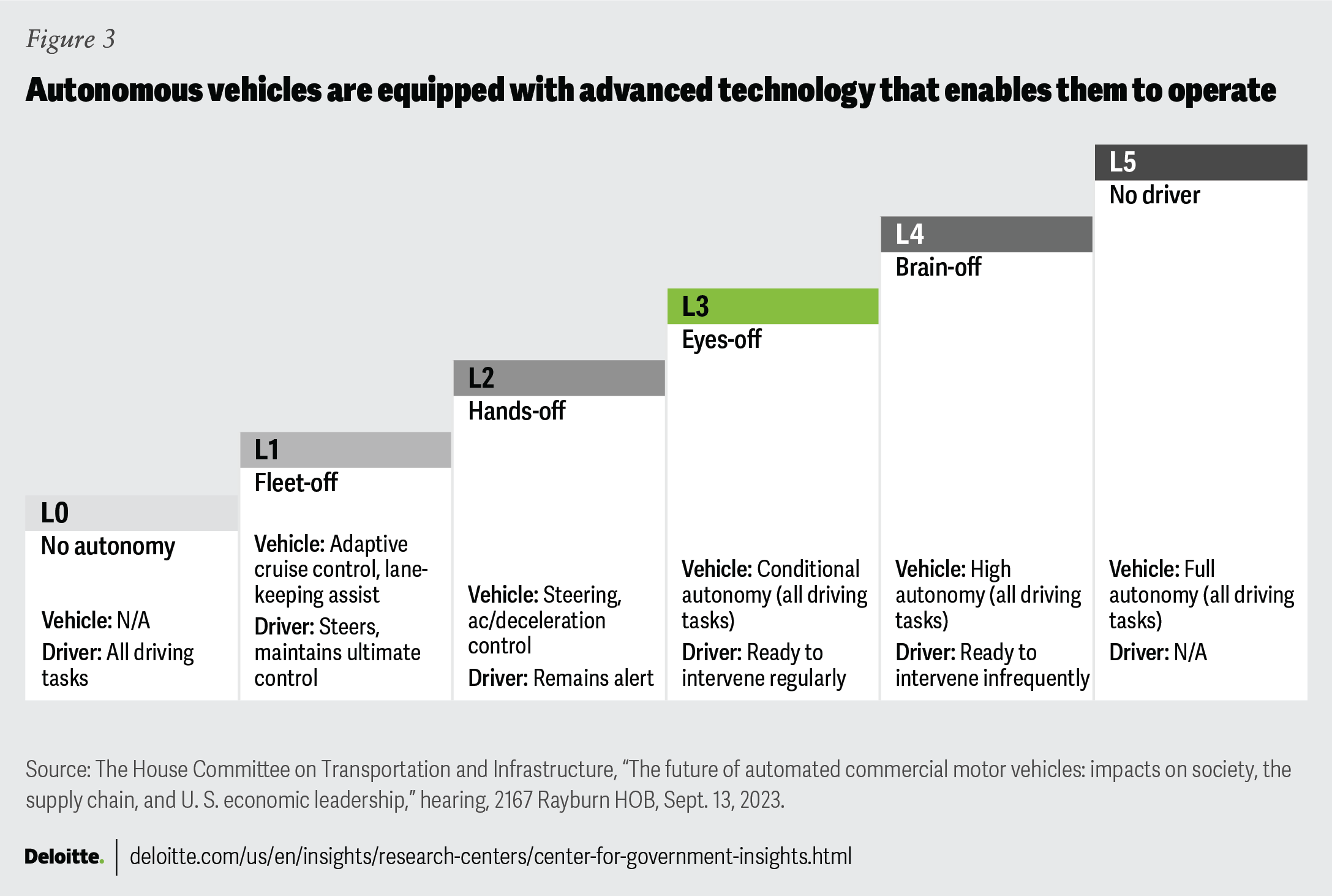

As policymakers working on AV regulations quickly learn, there are varying degrees of self-driving, with differing ramifications for how states and cities set up guardrails and incentives. SAE International defines six levels of vehicle autonomy, widely adopted across industry and US government agencies (figure 3):

Level 0: No driving automation

Level 1: Driver assistance

Level 2: Partial driving automation

Level 3: Conditional driving automation

Level 4: High driving automation

Level 5: Full driving automation

{kind=link}

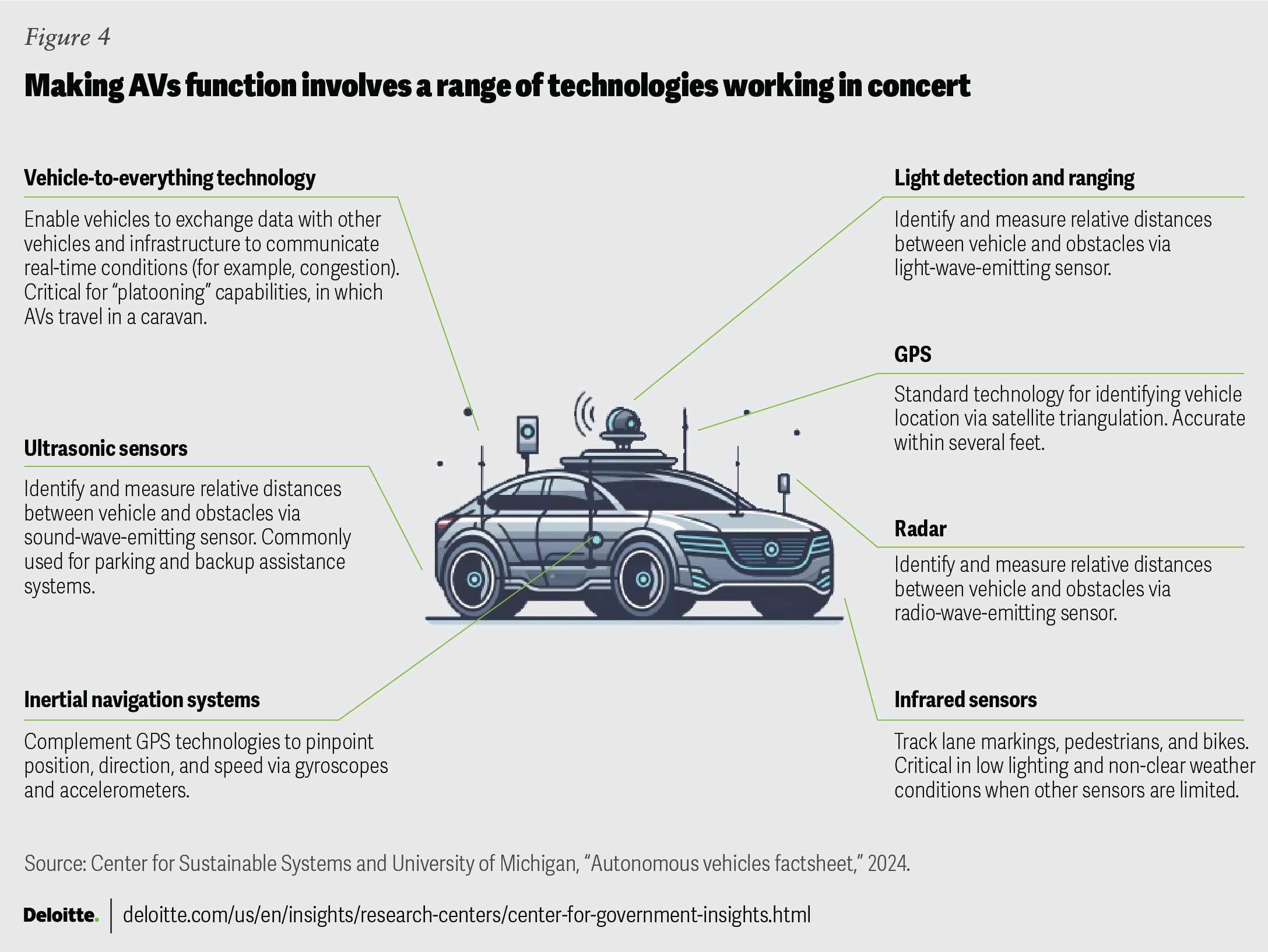

No one should be surprised by automakers’ start-stop-start-stop progress toward AV deployment: Making self-driving cars safe and efficient in a dense urban environment involves tremendous complexity (figure 4). As Jamey Tesler, former secretary of the Massachusetts Department of Transportation, observes, “Unlike many other heavily regulated industries, transportation is a ubiquitous good. Everyone uses the system every day. A common thread across all new mobility technology—from e-bikes to AVs—is that they need to be tested and piloted not just for safety, but for consumer awareness and political legitimacy.”23 To avoid some of the same potholes that previous mobility innovations entering the market hit, AV deployments demand close coordination with other players, especially public sector officials and policymakers responsible for keeping traffic moving and everyone safe.

{kind=link}

Policymakers and regulators have an integral role to play in shaping the AV landscape. City and state leaders want to consider a holistic view of the overall landscape and to understand how changes in the capabilities, incentives, or attitudes of any of the stakeholders—whether tech developers, automakers, fleet operators, network providers, or end users—could alter how AV regulations might need to shift. There are, for instance, open questions about the viability of different AV business models. Even with improving technology, the operational and business case is challenging for at-scale AV deployment. Many firms have a limited timeframe to achieve commercial sustainability, and this pressure influences the pace and scale of their commercial expansion. More than a decade after Zipcar founder Robin Chase outlined two—“heaven or hell”—trajectories for AV deployment,24 state and local governments can leverage business partners—and business models—that align with their objectives.

An overview of the US autonomous vehicle market

For cities, the AV landscape involves six primary stakeholders and an array of secondary players, who have different responsibilities.

- Governing bodies: Governing bodies across federal, state, and local jurisdictions who strive to guide development and implementation to best serve the public:

- Enable safe, secure transportation and communication infrastructure

- Uphold shared responsibilities (publishing standards, guidelines, etc.)

- Ensure attestation and enforcement

- Refine legislation and support economic development

- Technology developers: Commercial tech providers and research organizations focused on developing technical components of AVs and refining them to adhere to standards:

- Innovate technical components for efficiency, reliability, and safety

- Integrate service centers into software and hardware

- Ensure end-to-end cybersecurity

- Encrypt connected devices and secure the code of onboard units

- Auto manufacturers: Traditional auto manufacturers and new organizations established solely for autonomous vehicles:

- Strengthen technical manufacturing relationships for complete, secure component integration

- Adhere to existing broader motor-vehicle stations (for example, safety standards)

- Fleet operators: Organizations that manage the use, upkeep, logistics, and oversight of AVs; connect the finished product to customer-facing services (network provider):

- Track efficient location, speed, and status to boost efficiencies and performance

- Manage adherence to compliance and safety requirements

- Monitor fuel use, maintenance schedules, and driver patterns to lower operational costs

- Network providers: Operations that connect a product (that is, a car) to operations within the context of social, regulatory, and infrastructural environments:

- Ensure service availability and connectivity

- Provide channels for two-way communications with users (for example, announcements, guidelines, feedback, concerns)

- Understand and adhere to jurisdictional requirements and restrictions

- End users: Passengers or firms primarily seeking access to safe, reliable, and efficient alternative modes of transportation:

- Enjoy AV services as designed, without intentionally threatening performance

- Adhere to user-focused regulations and guidelines

- Provide feedback about system performance

Of all the stakeholders, end users may have the veto power: If the vast majority of people remain unwilling to climb into a self-driving car, adoption—and investment—will likely hit a wall, and the benefits that broad AV usage could bring for states and cities may never materialize. And even though safety has improved, with only a handful of fatal crashes over millions of test miles, multiple surveys suggest that consumer apprehension has increased markedly just when automakers were hoping to dispel fears. An annual American Automobile Association survey shows the number of Americans who characterize themselves as “afraid” of AVs rising from 54% in 2021 to 66% in 2024.25

The key players, especially those who have invested billions in AV technology, are very much aware of the problem. In April 2024, the Autonomous Vehicle Industry Association unveiled a set of five principles aimed at shoring up public trust: transparent interactions with government officials and the public, responsible AV integration into communities and deep engagement with law enforcement and first responders, upholding high cybersecurity and privacy standards, establishing safety-first culture and governance, and advocating policies to boost public trust.26

The public sector is integral to all of these principles. Realizing the potential public benefits of AVs, from reducing congestion to aiding senior mobility to boosting businesses that lack parking, will require both regulators and automakers to take action to build confidence in vehicle safety and security. That means far more than pointing out that driverless cars have fewer crashes per mile than human drivers27 it will involve agencies working with stakeholders across the AV landscape to coordinate policy and communication, aligning players’ interests to keep everyone moving in the same direction.

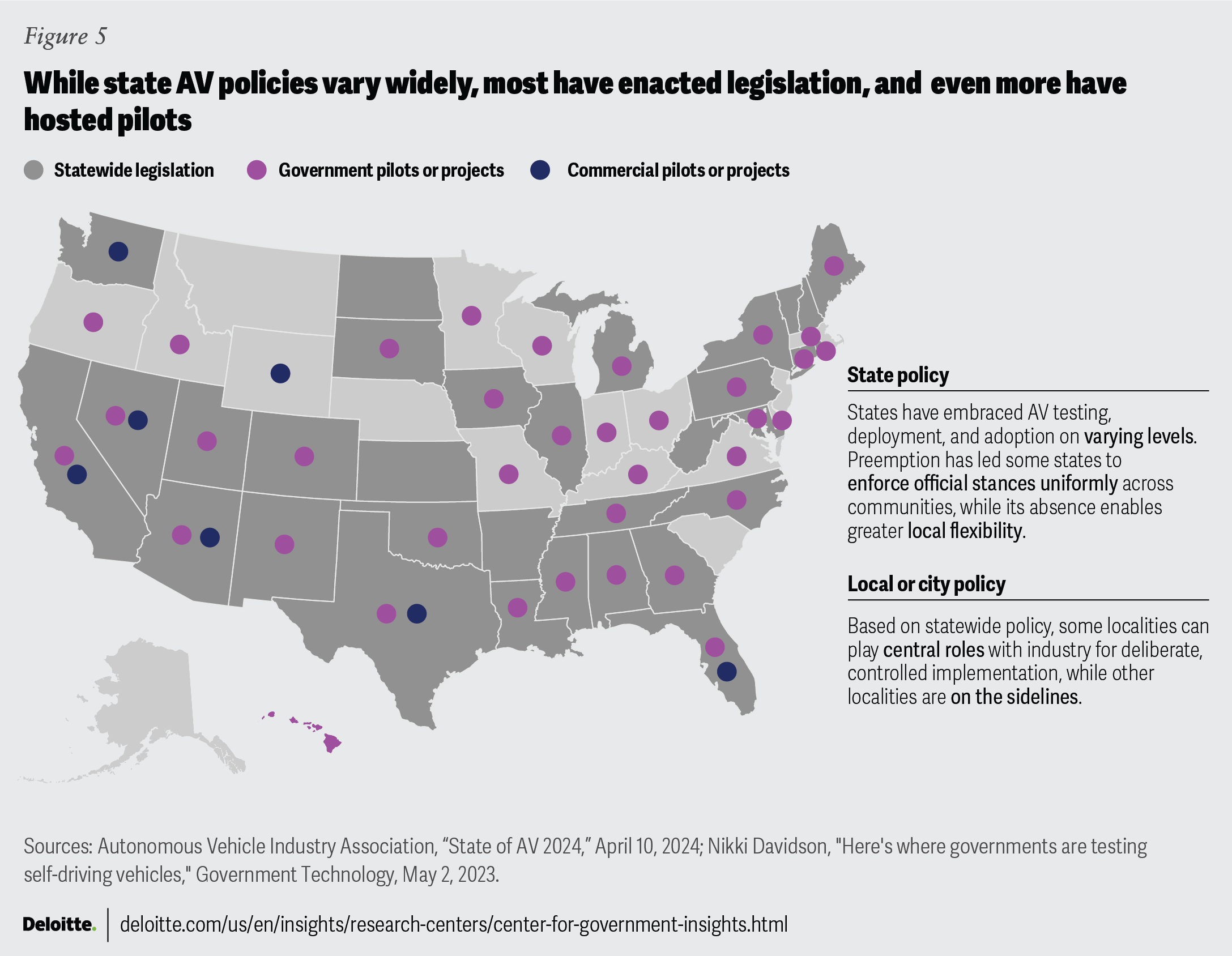

Some of that alignment has already taken place. Across the United States, regulators have set up state guidelines for AV testing and deployment, and both agencies and companies have piloted AV projects in all but a few states (figure 5). Policymakers and regulators at all levels of government, from federal to local, need to coordinate to ensure that rules don’t conflict.

{kind=link}

Government leaders can study early-adopter states to understand how their policy assumptions and frameworks influenced AV testing and deployment on actual city streets.

California was an early adopter in US AV innovation, with state-driven legislation and fast-moving pilot programs for rideshare services. There has been tension with local governments over top-down regulatory approaches, especially after a widely reported San Francisco crash and pedestrian injury brought federal investigations and popular backlash.28 California cities are pushing for more control over AV policy as well as greater data transparency.29

Since the 2015 executive order that established guidelines for AV testing, Arizona has become a hub for AV technology, with widespread AV testing and deployment, including personal delivery devices and truck platooning.30 In 2022, state legislators established driverless, low-speed AVs as a new vehicle category. But software issues have forced automakers to recall some of these vehicles,31 and federal investigators are looking into traffic incidents.32

As governments prepare for an era of at-scale autonomous vehicles, even early leaders like California and Arizona are reconsidering key assumptions and policy frameworks.

Competing visions for AVs in the city

We see states following one of three approaches in AV research, testing, and deployment: state-level control, local control, or a hybrid of the two. Each approach features distinct levels of regulatory flexibility across policy domains, with different jurisdictional levers appropriate to states’ particular AV markets.

No matter which AV protocol states and cities adopt, leading policy practices are consistent:

- Clear ownership and accountability: Establish clear terms for incident liability across the vehicle’s original equipment manufacturer, AV technology provider, or fleet manager; develop robust insurance requirements, indemnity provisions, and risk protocols to help ensure that responsible parties take appropriate action and sufficiently resolve issues.

- Uniform standards: Develop and enforce consistent standards across federal, state, and (if possible) local levels to avoid regulatory patchwork; enact legislation that can evolve with technological advancements and emerging safety data.

- Public-private partnerships and community engagement: Create opportunities for cross-sector deliberation and demonstration of AV technology; engage the public through pilot programs, such as autonomous shuttles for sporting events, to gather feedback and build trust.

- Data-sharing and privacy protections: Establish robust data privacy and reporting protocols between AV companies and regulatory bodies to monitor and ensure safety while protecting consumer data and proprietary business information.

- Infrastructure and workforce readiness: Invest in programs that prepare the workforce for technological and regulatory changes in the transportation industry. While connected infrastructure is not a prerequisite for safe AV deployment, investment in smart infrastructure, such as connected traffic signals, can support AV operations.

Measures of success are consistent as well, including:

- Safety and compliance: High compliance rates with regulations; reduction in crash rates, injuries, and fatalities; and high implementation rate of robust inspection protocols.

- Mobility: Improved traffic flow and reduced congestion, as well as enhanced transportation options for underserved and disadvantaged communities.

- Economic environmental impact: Creation of new jobs; increased investment in research and development and the workforce; operational efficiency gains; and reduction in emissions, fuel consumption, and pollution.

- Public acceptance: Increased public trust in AV technology and future initiatives.

State-level control

In a state-led regulatory environment, frameworks typically evolve as municipalities report differing impacts, even with limited agency. As AV use matures and scales, state-level regulatory frameworks may be considered, which could impact local governments’ control. Perhaps unsurprisingly, AV companies have an easier time with centralized and streamlined policymaking; if state agencies sign off on allowing testing and even limited deployment, automakers can proceed without local government. More freedom, and clearly defined regulatory guardrails, can generate innovation and insights, accelerating breakthroughs. And state investment in AV-supportive infrastructure can improve safety along with public perception and acceptance.

Communities and local governments are less enamored with state preemption of AV regulation, especially considering the wide range of urban, suburban, and rural environments in every state.

Local control

In jurisdictions where AV initiatives may be city- or county-led, local governments have more autonomy to permit AV testing and deployment. In these jurisdictions, communication and coordination are key for regulators and policymakers locally and statewide. While the absence of a statewide policy may reduce regulatory overhead, leaving space for AV companies to operate, discontinuities across localities can create uncertainty and limit the ability to mature and scale. Companies, communities, and local governments can collaborate across cities to develop a comprehensive approach.

Locally specific regulation carries benefits and challenges for all parties. While leaders can fashion AV policies to suit a community’s specific geography and demographics—and promote street-level public-private partnerships—those policies can be susceptible to swings in public sentiment, potentially derailing ongoing plans and investments by both providers and agencies. To promote greater stability, local officials and policymakers can assess how industry objectives might align with lasting community goals. To avoid drastic variations in legislation and deter industry from launching pilots and initiatives, municipalities can look to collaborate with similar, peer communities on AV research and policy development.

State-local hybrid approach

Some states have adopted a hybrid approach to regulation and policy, wherein AV activities are regulated at the state level and additional local oversight is permitted or encouraged, with state agencies deferring a subset of policy decisions to localities.

State-level legislation may catalyze follow-along legislation at the local level, permitting regulatory continuity and policymaking efficiencies across localities. In some cases, there has been increased collaboration between state government, municipalities, and manufacturers that specialize in research, design, and deployment. Cities’ partnerships with AV rideshare companies can speed innovation and illustrate how service can integrate into communities, as a model—or a cautionary tale—for other municipalities in the state.

Coordination is key: Uncertain regulatory environments and nonuniform frameworks between local and state governments can create a patchwork model of engagement for technology companies. Potential conflicts on operating limitations between regulators at different levels can leave the AV operating environment unsettled.

Choices facing public policymakers

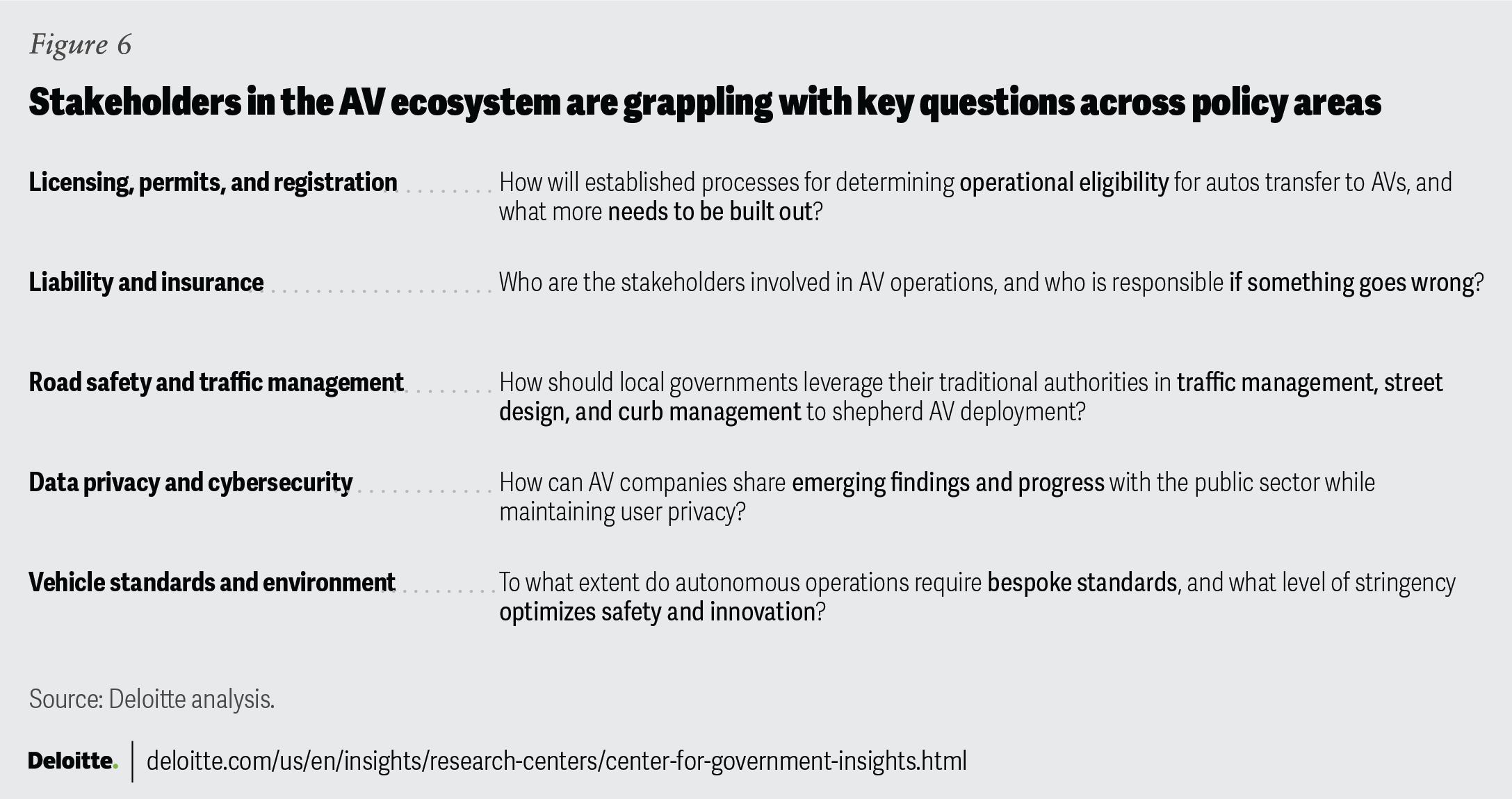

According to Mark Fagan of Harvard Kennedy School’s Autonomous Vehicles Policy Initiative, "State-level policy preemption is here and not going anywhere. But the goal should be to allow communities to have greater influence on implementation speed and scale in the future.”33 That influence can be exerted in many ways. In assessing possibilities over the years to come—and the potential benefits to citizens, businesses, and the environment—regulators and policymakers need to grapple with a host of issues to ensure that AV use is on the right track (figure 6). Each policy area requires a particular blend of oversight and collaboration with public and private entities.

{kind=link}

Cities are, of course, surpassingly complex entities, differing in ways that often only locals can see. Intentional AV implementation requires regulatory strategy rooted in each municipality’s realities and needs. Regardless of jurisdictional power, city leaders first need to decide the role they want AVs to play on their streets—and the role that they want to have in the AVs’ eventual deployment. These decisions could lead to vastly different outcomes for all stakeholders.

Introducing AVs into any city environment involves great unpredictability, but some impacts are likely: AV deployment will increase traffic complexity, at least temporarily, as drivers, pedestrians, cyclists, and others adjust to a new form of mobility; replacing drivers of any vehicle type with automated systems will introduce second-order effects, whether in citizens’ travel behaviors, patterns of business activity, the timing of rush hour, or other changes; and AV use will have impacts on safety, the environment, public health, landscape, and vehicle ownership.

Policymakers—even those who know their cities better than anyone—are not likely to be able to foresee the full scope of what introducing AVs might do to each of these players and systems, much less to a multilayered city ecosystem.34 What leaders can consider is which variables they need to factor in and allow space for—and which are thus far unknown and unknowable. State and city regulators may wish to consider a long list of questions before finalizing AV policies. For many identified areas, policymakers may want to lead with determining whether AVs can be treated simply like traditional motor vehicles or whether regulators need to specify limited accommodations or innovative rethinking of current frameworks.

As it turns out, local officials may have more control than they assume. For example, with regard to AV deployment, city officials can exercise policy levers relating to roadway design, data-sharing, and pricing. If they regulate all vehicles and for-hire services, local authorities can still comply with state rules. By addressing AV issues within broader policy frameworks, localities can maintain their own voice even when the state has issued its own comprehensive AV plan. In the face of risks and uncertainties about how AVs might ultimately affect urban mobility and society, local government leaders need to take a proactive approach to defining objectives and asserting their influence—regulatory, political, and informal—to create the future they want.

Questions for regulators to consider

In formulating AV policy, questions across a range of known risks and issues will impact decision-making.

- Licensing, permits, and registration

- How will AVs be identified and tracked by authorities?

- How will permits be issued and monitored to ensure compliance?

- Should there be a special license for individuals or companies operating fleets?

- What permits and registration processes are necessary for testing and deploying?

- How, if at all, will different restrictions honor out-of-jurisdiction permits?

- What conditions should be attached to permits and registrations?

- Liability and insurance

- How should insurance policies be structured?

- Who is liable in the event of different types of incidents?

- How will insurance premiums be calculated compared to traditional vehicles?

- How do we know if early policies are protecting enough?

- What legal frameworks need to be established to address liability issues?

- Who should be the responsible person, persons, or entity for different obligations?

- Road safety and traffic management

- How will traffic laws and regulations be applied and updated?

- How will curb space be allocated for pickups or drop-offs?

- How will emergency situations—both inside and outside the AV—be handled?

- What measures will be taken for safe interactions with human drivers, cyclists, and pedestrians?

- What road infrastructure changes are necessary?

- How should AVs be involved in traffic management plans for major events?

- Data privacy and cybersecurity

- What data will AVs collect, and how will it be used?

- How will cybersecurity standards be enforced for manufacturers and operators?

- What cybersecurity measures are necessary to protect AVs from threats?

- How will the privacy of individuals be protected?

- Is there a place for inter-vehicle communications with AVs across modes?

- How do jurisdictions understand potential threats and their role in responding?

- Vehicle standards and environment

- How will updates to AV software or hardware be regulated?

- How should AVs be tested for a variety of driving conditions?

- What safety standards should AVs meet before operating?

- What thresholds should be used for performance?

- Should there be incentives for lower emissions?

- How should AVs be monitored for compliance and community trust?

As new issues come to light during deployments, regulators will need to ask additional questions to find solutions to these issues.

How state and local regulators can build trust

Consumer skepticism is a key factor holding back AV deployment, with trust actually falling over the last few years.35 Many more people have heard about AV glitches, crashes, and recalls36 than have seen the vehicles in action—much less been a passenger in one—and many are still learning details of how self-driving cars function. While some may find comfort in discovering that, for instance, humans remotely supervise most purportedly autonomous vehicles,37 while others may feel as though that fact highlights ongoing technological shortcomings.

Emphasizing AVs’ social benefits could help build trust, as consumers and partners learn more about why advocates are encouraging states and cities to allow testing and deployment.38 Pilot programs such as Detroit’s Accessibili-D, which uses self-driving shuttles for elderly and disabled residents, are illustrating how the technology can directly help people underserved by current transportation options.39

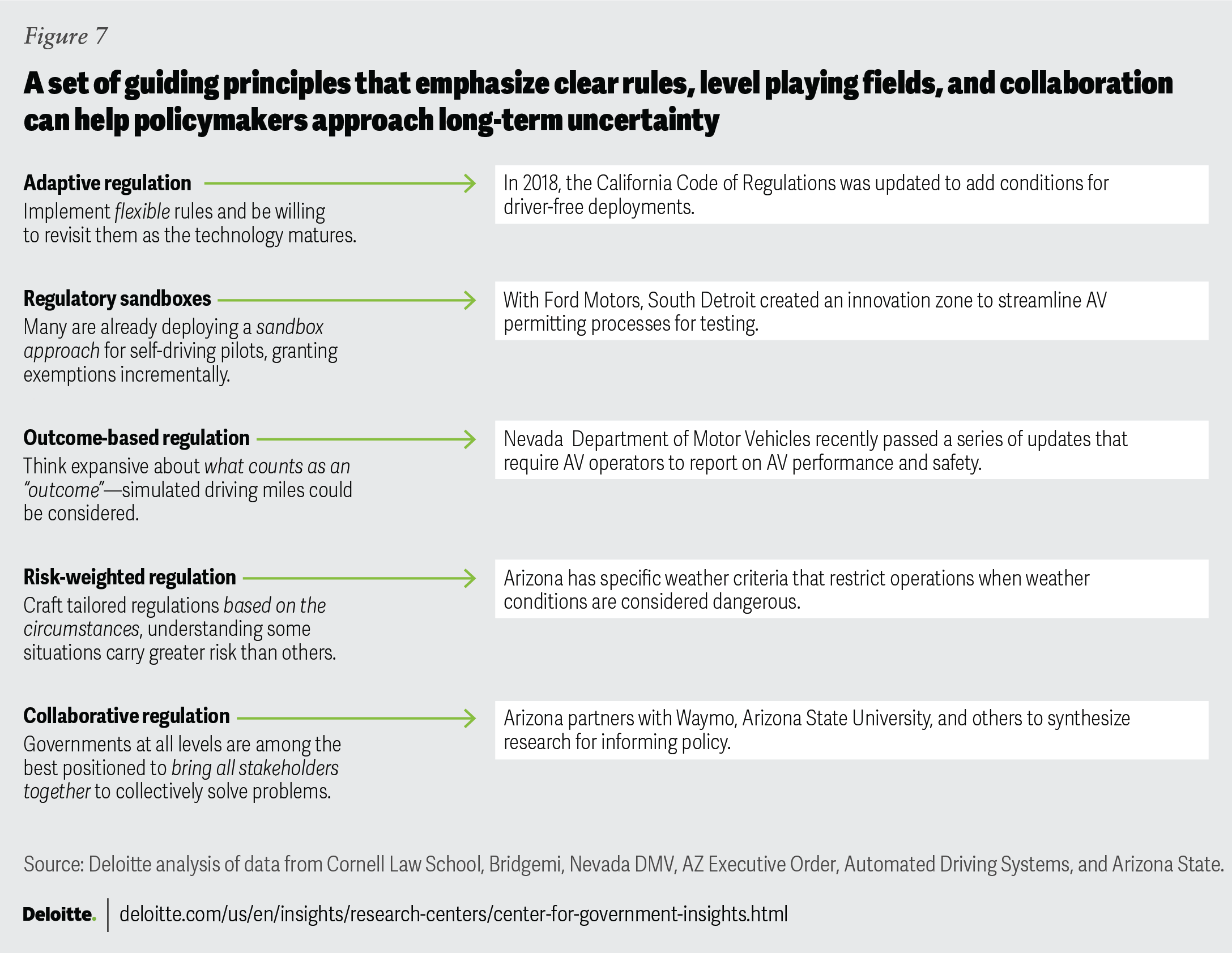

But transparency and clear regulation will likely make the biggest difference to public opinion.40 States and cities are under pressure to step forward and offer guidance. A regulatory framework that emphasizes clear rules, level playing fields, and collaboration can protect citizens and ensure fair markets while letting innovation and businesses flourish (figure 7). Whereas many current legislative frameworks contain one-time, blanket approvals, a deliberately incremental approach may allow for cities to opt in or companies to advance toward full commercial deployment as certain safety-related milestones are achieved. Regulators, too, may consider more expansive cost-benefit analyses that don’t focus solely on transportation system performance, but also take into account economic development, expanded mobility access, and indirect impacts on roadway safety.

{kind=link}

Dealing with so many variables and players is a challenge for any team of regulators—considering cities and mobility, the list of stakeholders includes pretty much everyone—and agencies face particular difficulty in coordinating to provide consistency for the overall mobility ecosystem. After all, highways don’t terminate at city limits. Building trust in AVs’ benefits and safety includes making users confident in the vehicles no matter their point of origin or current location. Local and state government officials can help by showing citizens what responsible, transparent usage looks like.

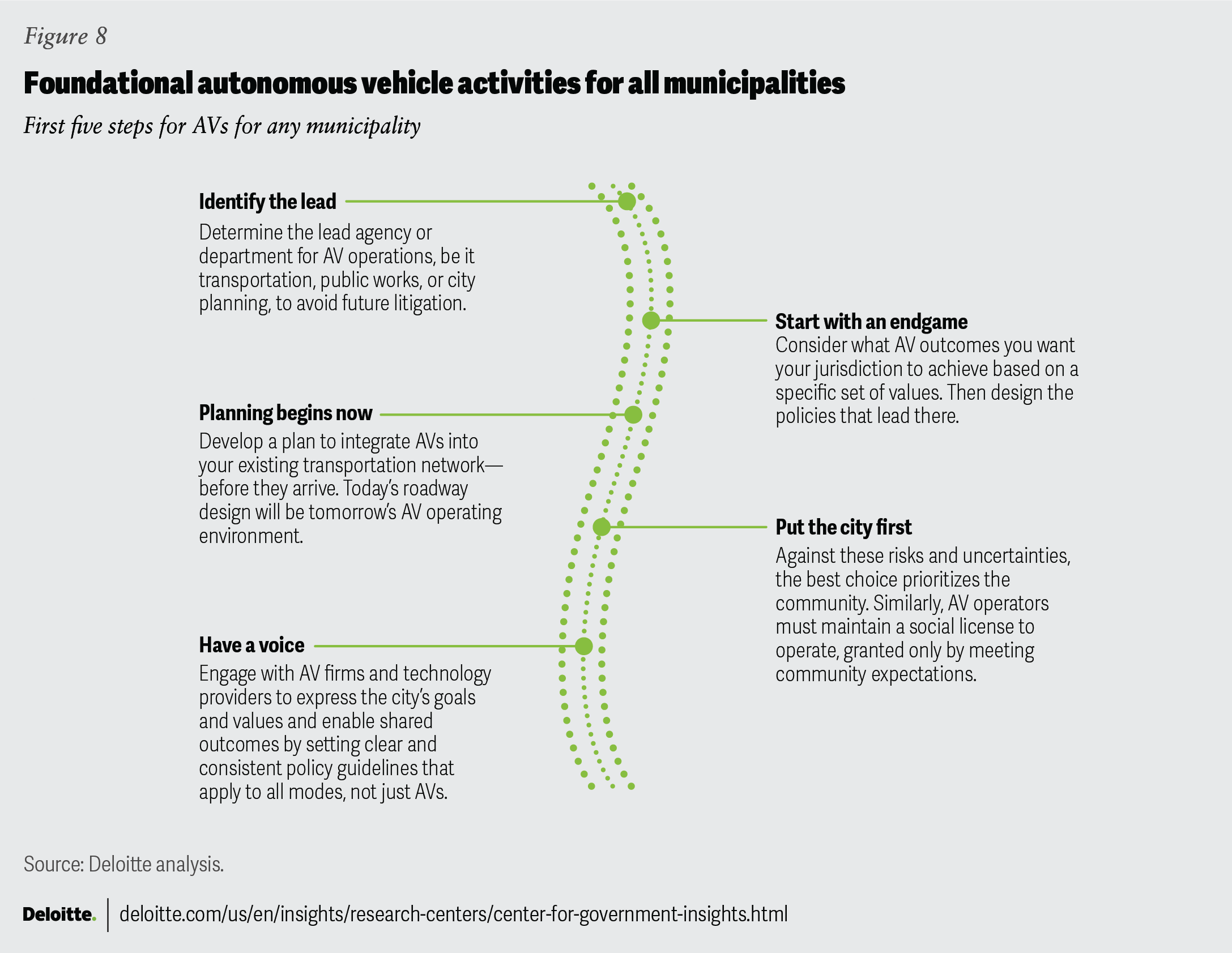

While some AV regulatory principles are simple extensions of traditional transportation policies, the broad societal impact and suites of new technologies demand a fresh approach, evaluating how to apply existing regulatory principles to AVs before taking less-familiar roads (figure 8).

{kind=link}

Looking ahead

In the nearly 140 years since manufacturers introduced motor vehicles to cities, urban environments have evolved in ways no one could have anticipated. It’s safe to say that no one knows for certain exactly what city streets will look like a decade from now—after all, only several years ago, few had envisioned e-bikes, scooters, and other forms of micromobility taking over the streets and bike lanes of American cities as they have.41 Innovation can come quickly.

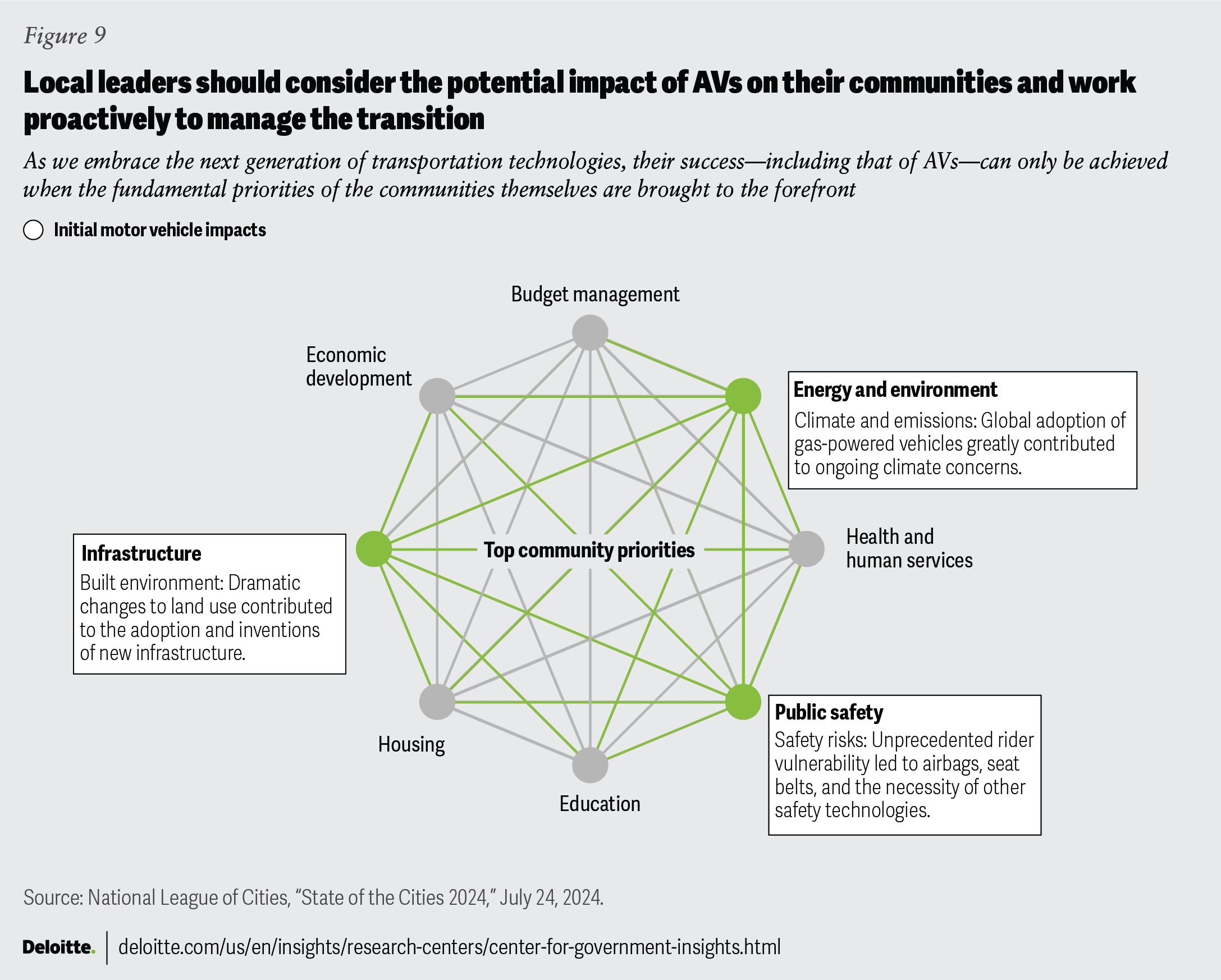

Autonomous vehicles have the potential to disrupt mobility—and cities themselves—in ways both minor and dramatic. Before introducing and tweaking regulatory frameworks, policymakers need to carefully consider the potential landscape of tomorrow’s urban environment and how AV technology might contribute to that state. As leaders embrace the next generation of community-facing technologies, it’s important to remember that those technologies—including AVs—can succeed only when the fundamental priorities of the communities themselves are brought to the fore (figure 9).

{kind=link}

Continue the conversation

Anant Dinamani

Jeff Hood

Rodolfo Dominguez

Tiffany Fishman

by

Anant Dinamani

Jeff Hood

Rodolfo Dominguez

Tiffany Fishman

Cover image by: Sonya Vasilieff; Adobe Stock

Visit the Deloitte Center for Government Insights

Access more insights for the defense, security and justice, government health care, state and local government, transportation and infrastructure, human services, and higher education sectors.