How banks can help achieve nature-positive outcomes and preserve biodiversity

Deloitte estimates that US banks have at least US$1.7 trillion of loan exposure to sectors facing potential natural capital loss—and that’s just one area of risk.

Key takeaways

- The world is facing a potentially catastrophic future if we don’t act soon to restore and protect the physical environment. Many of the natural systems on which our society relies for sustenance are disintegrating, marked by the precipitous decline of terrestrial and aquatic biodiversity.

- These losses of “natural capital” not only exacerbate global warming and intensify the impacts of climate change, but also stunt economic growth, disrupt supply chains, and affect the provision of essential goods and services. US banks are estimated to have at least US$1.7 trillion of loan exposure to sectors facing potential natural capital loss. In addition, nature-related risks extend beyond credit to other domains as well, including market risk, operational risk, and reputational risk.

- Despite the urgency of the issue, natural capital is seldom considered in banks’ business models and risk management processes. Few US banks are prioritizing the identification, assessment, and management of nature-related risks. While some banks have set targets and commitments on individual issues like deforestation or water conservation, very few have explicit nature-positive strategies and commitments.

- As key financial intermediaries, banks can play an essential role in addressing this crisis by valuing natural resources and achieving nature-positive outcomes—a concept that combines financial investment with nature protection, regeneration, and sustainable use of resources.

- However, the sheer number of frameworks, standards, and tools to enable institutions to address nature-related risks can make it challenging for banks to determine which ones are most relevant, and how best to implement them. The latest recommendations from the Taskforce for Nature-related Financial Disclosures build on existing work and are meant to provide an actionable path forward.

- Banks could implement a nature-positive road map comprised of three key elements: prepare, integrate, and execute to build on existing net-zero initiatives. Existing environmental and social risk management programs can be the foundation on which to build nature-positive policies.

An unfolding crisis

Nature is already degrading on an alarming rate, and the world will likely face a catastrophic future if this depletion persists. According to a recent NatureServe report, 34% of plants and 40% of animals in the United States are at risk of extinction, while 41% of ecosystems are at risk of range-wide collapse.1 Another study estimates that bird numbers have declined by 29% in North America since 1970, and2 since 2001, the United States has lost 104 million acres of forests, resulting in a 15% decline in tree cover.3 Meanwhile, biodiversity loss in the United States is estimated to cost the food industry over $450 billion a year.4

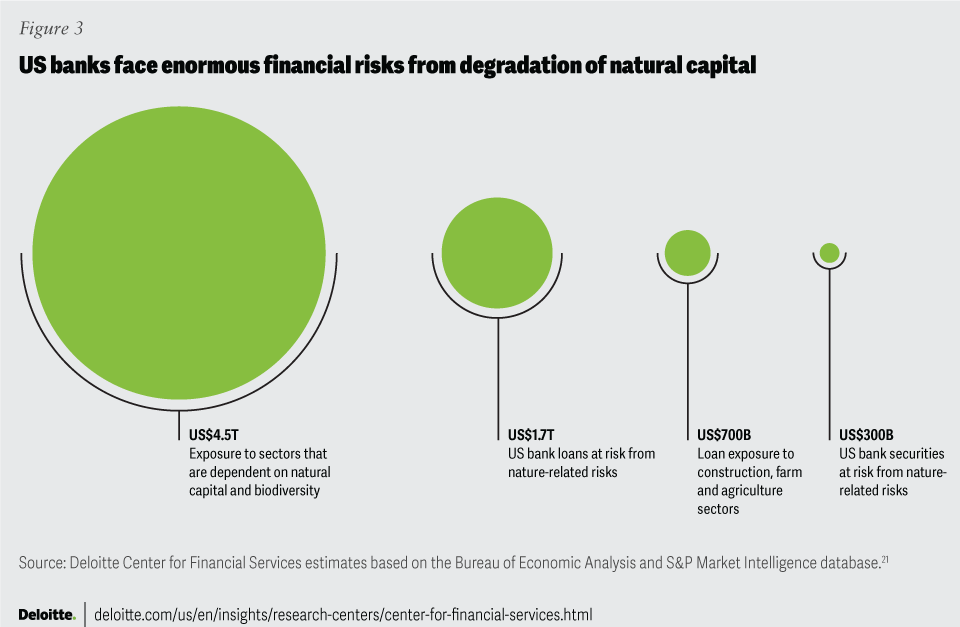

Such loss of biodiversity and “natural capital”—the various natural resources and ecosystems that underpin our economy and society—could stunt future economic growth, disrupt supply chains, and affect the flow of essential goods and services. According to Deloitte’s calculations, close to US$4.5 trillion, or 18% of US gross domestic product is exposed to sectors that are highly or moderately dependent on nature and biodiversity.5

Why should US banks focus more of their attention on natural capital and biodiversity? What are the risks and challenges they face? What practical steps should they consider integrating into their business strategies and risk management?

What is natural capital and biodiversity?

Natural capital describes the various natural resources and ecosystems that enable the flow of goods and services to the economy.6 Ecosystem services are derived from natural capital and refer to the flows of benefits such as clean water, healthy soils, and other climate regulating services that are vital for societies and economies. Unlike financial capital, natural capital is not a fungible asset and, therefore, requires its inclusion in the decision-making process of each industry.7

Biodiversity can be defined as the variety of all living things that exist within terrestrial, marine, and other aquatic ecosystems and their interactions with nature. It is not only a measure of the state of nature but also is critical to the health and stability of natural capital, as it provides resilience to natural shocks, like floods and droughts, and supports fundamental processes such as the carbon, nitrogen, and water cycles.8

Loss of natural capital is a major risk for most US banks

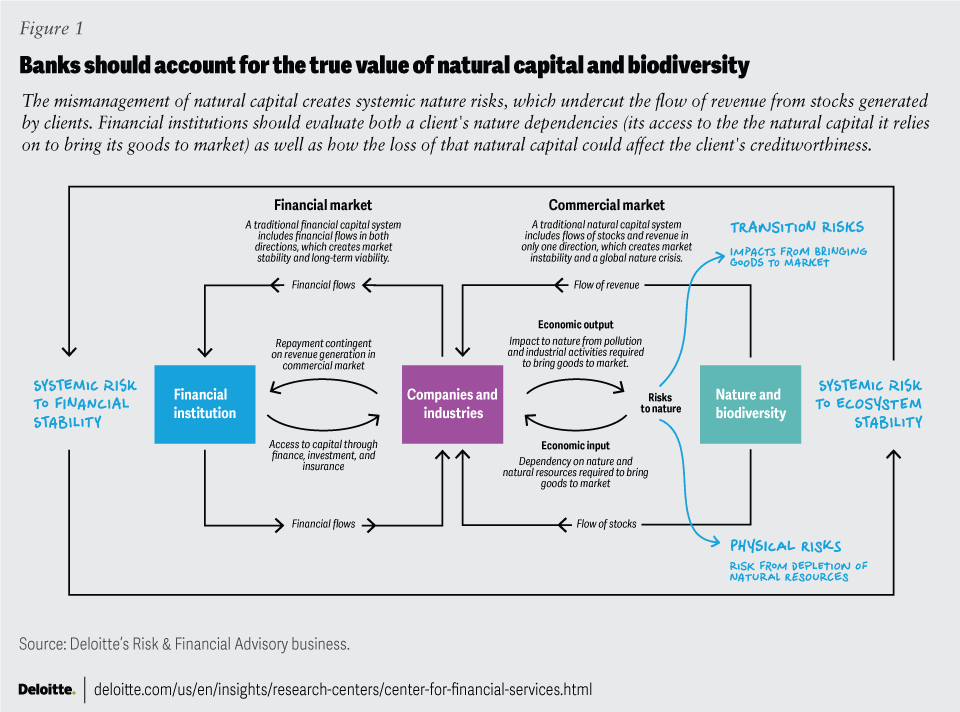

Depletion of natural capital can affect the banking industry in multiple ways (figure 1). For instance, Deloitte estimates that US banks have at least US$1.7 trillion of loan exposure to sectors facing potential natural capital loss.9 US borrowers also seem to be more exposed to biodiversity risks compared to borrowers in other countries.10

{kind=link}

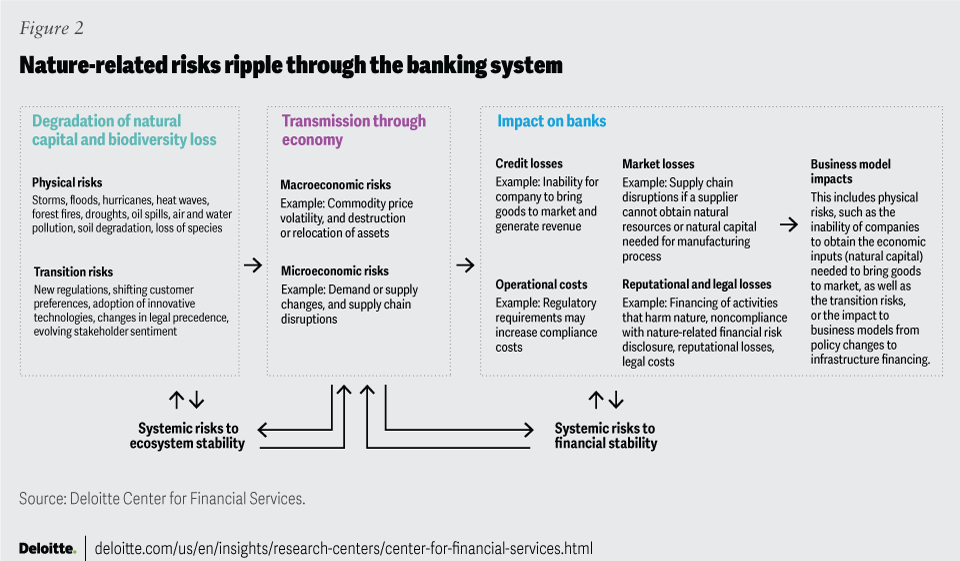

Banks’ vulnerabilities extend beyond credit to include concerns related to market losses, operational costs, and reputational damages. The Taskforce on Nature-related Financial Disclosures (TNFD), a market-led, government-supported initiative to help organizations act on evolving, nature-related issues identifies three categories of risks—physical, transition, and systemic (figure 2).11 These categories are similar to the Task Force on Climate-related Financial Disclosures’ (TCFD) definition and analysis of climate-related risks.

{kind=link}

According to the Network for Greening the Financial System, nature-related physical risks arise from degradation of natural capital and loss of ecosystem services.12 These can manifest through natural disasters, such as floods, droughts, and storms, or from activities contributing to air, water, and soil pollution. As an example, a significant deterioration of coral reefs may tip the tourism industry into losses of at least US$2 billion currently in the states of Hawaii and Florida alone.13 Such a scenario could, potentially, trigger higher loan losses, asset devaluations, and market losses for US banks operating in those regions.

Transition risks often stem “from a misalignment of economic actors with actions aimed at protecting, restoring, and/or reducing negative impacts on nature,” according to the TNFD.14 These risks can result from new regulations, evolving customer preferences, introduction of innovative technologies, enforcement of legal actions, and changing stakeholder sentiment toward nature.15 Such risks can manifest in the form of stranded assets, changes in demand and supply, and increased compliance and legal costs.

Furthermore, nature-related systemic risks can arise from even partial collapse of ecosystems. According to the TNFD, such “risks are characterized by modest tipping points combining indirectly to produce large failures, where one loss triggers a chain of others, and prevents the system from reverting to its prior equilibrium.”16

Unsustainable levels of physical and transition risks, as well as ecosystem stability risks, could also lead to systemic risks to global financial stability, such as sudden disruption to the functioning of financial markets. Recognizing this connection between nature and financial risks, a group of central bankers have identified biodiversity loss as a significant and under-appreciated threat to financial stability.17

Collectively, nature-related risks could manifest in the form of increased operational costs and losses in loan and investment portfolios. Of course, the severity may vary by banks’ exposure to these risks. The different costs and losses could include the following:

1. Credit losses: Nature-related risk can lead to increased defaults in industries that have strong supply chain linkages to natural capital, such as agriculture, energy, tourism, food and beverage, and construction. As a result, banks can experience higher-than-expected loan losses through these exposures.

According to the European Central Bank, almost 75% of all bank loans are made to borrower companies that depend highly on at least one ecosystem service.18 Similarly, according to Deloitte estimates, US banks have US$1.7 trillion of loans exposed to nature-related risks, and a large portion (US$700 billion) are from the construction, agriculture, and farming sectors (figure 3).19 Furthermore, exposure in sectors such as the manufacturing and non-durable goods industries could double these potential credit losses. Banks’ credit ratings will also likely be affected as rating agencies focus more on how nature-related risks affect borrower creditworthiness.

{kind=link}

2. Market losses: Depletion of natural capital can also affect banks’ securities portfolios through devaluation of assets and price volatility, especially in sectors such as agriculture, fisheries, real estate, and energy. An analysis by the Banque de France estimates that 42% of securities held by French financial institutions are highly or very highly dependent on one or more ecosystem services.20 Similarly, according to estimates, US$300 billion in US banks’ securities portfolios may be at-risk due to nature-related risks.21

Take the example of land degradation, one of the most pernicious environmental challenges for decades. This is already negatively impacting food production, jeopardizing the food security for over 3.2 billion people around the world.22 According to the United Nations Environment Programme, land degradation could lead to a drop in food productivity by 12%, and an increase in food prices by as much as 30% by 2040, globally.23

As a result of potential market risk, banks may be unable to attract co-financers or investors in sectors prone to nature-related risks. With many US banks providing underwriting services to such industries, a significant amount of fee and advisory income may also be at risk. Furthermore, nature loss can lead to sovereign and corporate credit rating downgrades, with far-reaching implications for securities markets.24

3. Operational costs: Another area where nature-related risks can affect banks is their operational infrastructure. There could be a marked increase in banks’ operating costs as banks look to transform their policies to incorporate biodiversity and nature-related risks. These effects will likely be felt most pressingly in credit underwriting, which may require new and alternative data and models. Demand for nature-positive outcomes may also bring in newer regulatory policies and compel banks to disclose more about their nature-related policies and practices, resulting in higher compliance costs.

4. Reputational and legal losses: As stakeholders increasingly demand greater transparency and accountability on environmental issues, banks failing to address nature-related impacts could be exposed to potential reputational losses and decreased market valuations. In the past, some US banks were criticized for financing companies involved in natural capital loss such as oil spills and deforestation. These events, in turn, can lead to reputational losses for banks.25,26 Some banks estimate reputational loss as one of the highest environmental-driven risks.27 There are also legal risks stemming for banks’ financing of activities that may lead to the destruction of natural capital. As a result, banks may face higher legal liability costs in the future.

In addition to the above risks, accounting for natural capital and biodiversity may also impact banks’ business models. For instance, banks that invest in large-scale infrastructure projects, such as dams, or those that finance extraction activities in ecologically-sensitive areas, may be forced to reassess these programs. As a result, they may also be forced to scale back or exit certain subsectors, similar to how banks have withdrawn from financing carbon-intensive activities.

The climate-nature nexus

The dual crises of global warming and degradation of natural capital are intrinsically linked. It is well recognized now that global warming causes nature and biodiversity loss, which, in turn, are also accelerating climate change.28 Land use change, for instance, influences both climate and biodiversity. It is one of the biggest drivers of terrestrial biodiversity loss.29 Similarly, land use in the form of agriculture or forestry accounted for one-fourth of total anthropogenic30 greenhouse gas emissions in the last decade.31

In other words, climate change and nature loss are feeding each other in a perpetual, recursive cycle. For instance, rising temperatures and changing precipitation patterns are already affecting soil health. And deforestation in places like the Amazon rainforest not only affect livelihoods for millions but are also causing rapid depletion of natural carbon stocks and sequestration capacity, thus affecting the planet’s natural resistance to global warming.32

However, an isolated, narrow focus on purely climate-positive initiatives can be counterproductive. Any solution to address climate change should also help ensure it is not unintentionally worsening biodiversity loss or depletion of natural capital. For instance, the installation of wind turbines or hydroelectric power plants in some parts of the world has had a harmful effect on biodiversity, including bird and bat populations and other species.33

So, there is a compelling need for an integrated approach that simultaneously considers climate change and nature, to jointly optimize for both.

A nature-positive economy can be fruitful for banks

Mobilizing finance for nature-positive outcomes can offer new business opportunities for banks. The World Economic Forum estimates that a nature-positive pathway could generate over US$10 trillion in new annual business value, possibly resulting in new financial markets and products to enable new capital flows.34

As key players in the global financial system, banks are uniquely positioned to create nature-positive outcomes, boost economic growth, and contribute to economic stability. Here’s how:

1. Capital flows: Banks will have a bigger role to play in plugging the global biodiversity funding gap than they do today; investments currently stand at an average of US$711 billion per year.35 The current share of private sector funding is only about 14% as compared to 86% from public sector.36 Financing nature-positive projects may also have the indirect effect of reducing their loss exposures. For instance, funding for conservation efforts in agriculture could also help minimize loan losses in that sector.

2. Nature-finance innovation: Evolving customer demands and shifting stakeholder sentiments toward biodiversity loss can also create new financial markets for nature-related products in both developed and developing economies. There is a growing market for securities and funds that focus on minimizing biodiversity loss;37 AXA’s impact investment fund is one such example that focuses on biodiversity protection.38 “Nature-backed securitization” can be another avenue for transferring risk and investing in nature-backed assets, akin to other financial assets.

Another area where banks can facilitate a nature-positive economy is developing novel financial products based on nature and biodiversity. Products such as green bonds, debt-for-nature swaps, blue bonds,39 and biodiversity credits can significantly expand the nature market and the reach of biodiversity-linked investments. Bank of America, for instance, is offering thematic and structured bonds focused on debt-for-nature provisions.40 Similarly, Rabobank launched Acorn, a program that supplies upfront funds to farmers to invest in agroforestry.41 Along the same lines, biodiversity credits could be the next step in climate and nature financing. The market is currently nascent but demand for voluntary biodiversity credits could reach as much as US$69 billion by 2050, according to estimates from the World Economic Forum.42 Sustainability-linked loans are another potential source of revenue for banks.

3. Advisory services: Banks can offer specialist advice and support to their corporate clients in assessing and mitigating their biodiversity footprints. This may include conducting environmental and social impact assessments, developing biodiversity management plans, and implementing leading practices to help minimize negative impacts on biodiversity. Pricing the contributions of nature to the economy can help ensure that businesses and governments account for natural capital alongside physical, financial, and human capital. Banks can also help their clients to better navigate the complex landscape of environmental regulations, standards, and reporting requirements related to biodiversity.

Few US banks are actively pursuing nature-positive strategies

Despite the current precarious state of nature, few US banks are prioritizing the identification, assessment, and management of nature-related risks. While some banks have set targets and commitments on individual issues like deforestation or water conservation, very few banks have explicit nature-positive strategies and commitments.

Most US banks lack formally established and articulated goals, strategies, measures, and procedures to align their business operations and nature-related disclosures. While many have made clear commitments toward climate change, most are not integrated with nature-related risks and opportunities—potentially resulting in minimal effect on both climate and nature. Current biodiversity-related initiatives, where they do exist, reside within the existing environmental and social risk management programs, and are usually part of the International Finance Corporation’s Performance Standard 6.

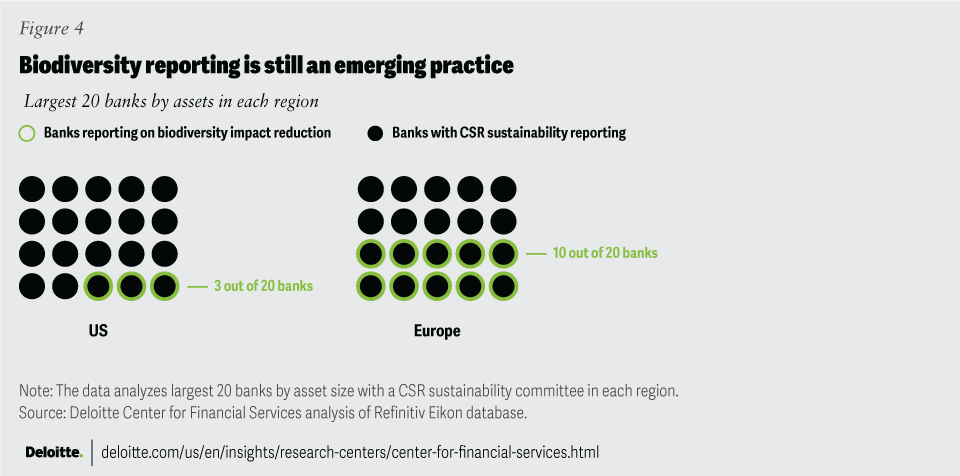

As a result, banks either lack comprehensive policies related to biodiversity and nature-related risks or have only partially implemented any such policies.43 In fact, despite having a corporate social responsibility committee in place, just three of the largest 20 US banks by assets are reporting on biodiversity impact reduction, compared to 10 of the largest 20 European banks by assets (figure 4).44 Even the most advanced institutions do not have robust approaches; and even where they do, they are rather sporadic and weakly implemented.

{kind=link}

In comparison, European banks are developing policies and guidelines on natural capital and implementing them at a rapid pace. Many of these banks also follow the Performance Standard 6 on Biodiversity Conservation and Sustainable Natural Resource Management framework. HSBC and ABN AMRO, for instance, have developed sector-specific policies related to biodiversity, demonstrating their commitment to addressing this pressing issue. These policies require clients to follow sustainable practices, protect natural capital, and help ensure transparency.45

Some European banks are also partnering with corporations to help improve supply chain sustainability related to nature. For instance, HSBC, in collaboration with Walmart, is offering suppliers credit lines and early payment on invoices to encourage investments in sustainability.46 Some European players are also incorporating biodiversity-related goals into their credit policies and setting targets to manage biodiversity-related risks. Rabobank has implemented a new biodiversity-focused tool to incorporate nature into its lending activities.47

One reason for the more intense focus on natural capital and biodiversity among European banks may be the greater regulatory pressure in the European Union compared to United States. European regulators have generally been more vocal and have crafted nature-focused standards and disclosures.

For instance, the European Commission recently adopted the European Sustainability Reporting Standards that will require companies to report on risks and opportunities related to environmental, social and governance (ESG) issues, including biodiversity, climate change, and human rights.48 The European Investment Bank has also strengthened its biodiversity standards from “no net-loss” to “no loss” from biodiversity-related financing projects.49 Furthermore, the European Central Bank is also analyzing the exposure of ecosystem services on financial services.50 Such steps from the central bank have driven European banks to be more proactive in addressing biodiversity loss and integrating it into their operations. European investors have also shown greater interest in nature and biodiversity, leading to meaningful growth in nature-related funds in Europe.51

There are a few US banks, though, that are increasingly recognizing the importance of biodiversity and natural capital and taking action to address the challenges. JPMorgan, for instance, has developed policies for sectors that may have high nature-related risks. The bank has also adopted policies designed to reduce deforestation and other land use activities through client and supplier relationships.52 Similarly, Citigroup’s policies require clients to pursue certification with the Forest Stewardship Council to help ensure that forests used in the supply chain are sustainably managed.53 Furthermore, CDP (formerly known as the Carbon Disclosure Project) reports point to increased management and Board-level attention. Some banks are also participating in peer working groups and thought leadership initiatives, while others are exploring nature-related bonds and credits. These efforts and actions remain far and few, though. There’s much more that the US banks can do to create more nature-positive outcomes.

Challenges plague integration of natural capital efforts

Understanding biodiversity and recognizing nature-related risks is a first step for many banks in their nature-positive journey. Successful implementation and assessment will, however, require US banks to overcome some possible hurdles.

1. Trying to boil the (nature data) ocean: The vast amount of information on biodiversity and natural capital can be overwhelming and confusing, likely making it difficult for many banks to set clear aims and goals. For instance, some banks may struggle to identify the drivers and dependencies of natural capital loss, especially as biodiversity encompasses the complex variability among living organisms across species and habitats. This can lead to a lack of clarity in decision-making and policy implementation.

2. Perceived lack of data: Quantifying nature-related risks and opportunities in their lending and investment portfolios may be a key limitation for some banks, particularly as data on natural capital has not reached the level of sophistication of carbon emissions data. However, it is not the absence of data, but the consolidation from diverse sources which may prove a hindrance for some US banks.

Third-party vendors could play a key role in providing a standard or a baseline to start nature-related risk assessments, just as with the climate change initiatives. However, banks should not wait for third-party data vendors to provide consistent and robust data to initiate nature-related risk assessments. Obtaining the information needed to understand a client or industry’s nature-related risks can be accomplished by integrating nature positive outcomes with the client underwriting process and other risk assessments that currently exist, not by waiting for nature databases to emerge.

Recent developments in assessment frameworks and tools, such as TNFD’s LEAP (locate, evaluate, assess, and prepare) assessment, offer promising solutions to value biodiversity and natural capital more accurately. For instance, a combination of the S&P Global Nature Risk Profile methodology and the ENCORE (Exploring Natural Capital Opportunities, Risks, and Exposure) system can provide a robust start to revamping banks’ credit assessment tools.54 Banks may still face difficulties in integrating these tools into existing risk management frameworks and decision-making processes, due to insufficient specialized expertise and resources. However, the goal is not to put in place a “perfect” nature-related risk program tomorrow; the goal is to get started by assessing the nature-related risk associated with business relationships with a goal of improving the bank’s approach as new information and tools become available.

3. Multiple regulatory frameworks: Both developed and developing nations are coming up with specific nature-focused regulations and standards, with possibly more to come in the future. These standards, which are available in different geographies for different products and industries, will likely create additional complexity for US banks, especially those with a global presence. Banks will need to navigate various frameworks and standards, both local and global, and to adapt their operations efficiently. They should determine which frameworks are most relevant to their specific context and help ensure compliance with multiple, and sometimes conflicting, requirements.

4. Limited cross-disciplinary expertise: Banks may lack the necessary talent and resources to address biodiversity and natural capital issues. Banks should aim to recruit professionals with cross-disciplinary expertise in assessing biodiversity and natural capital risks across the banking value chain, as these fields are relatively specialized. But using existing climate-focused infrastructure and teams can help bridge this gap. Banks should look to scale and upskill existing teams and leverage current resourcing models, rather than start from scratch. They should also look at conducting training programs on biodiversity loss and its direct impact on their value chain.

Multiple frameworks, standards, and tools already exist

Over the years, various governments, independent bodies, and industry-specific entities around the world have issued and recommended a variety of guiding principles and frameworks—many of which are voluntary—for action toward a nature-positive economy. For instance, the Equator Principles, a financial industry benchmark for determining, assessing, and managing environmental and social risk in projects, have emphasized the consideration of nature risks in project finance. These principles were initially formulated in 2003 and were later aligned with the International Finance Corporation Performance Standards in 2006. Performance Standard 6, in particular, focuses on sustainable use of natural resource and biodiversity conservation.55

Similarly, the Natural Capital Protocol, launched by the Natural Capital Coalition in 2016, offers a framework for financial institutions to “measure and value natural capital impacts and dependencies across the entities and portfolios that they finance, invest in or underwrite.”56

And more recently, the Principles for Responsible Banking issued guidance (“Nature Target Setting Guidance”) on how banks could integrate nature-related considerations into their core operations and financing activities, in line with the aims set forth in the Global Biodiversity Framework.57 The January 2024 update to the Global Reporting Initiative’s (GRI) Biodiversity Standard is another significant milestone for external reporting. Organized around four main pillars—supply chain transparency, location-specific impacts, direct drivers of biodiversity loss, and impacts on society—GRI 101: Biodiversity 2024 helps organizations meet growing demands from multiple stakeholders for information on biodiversity impacts.

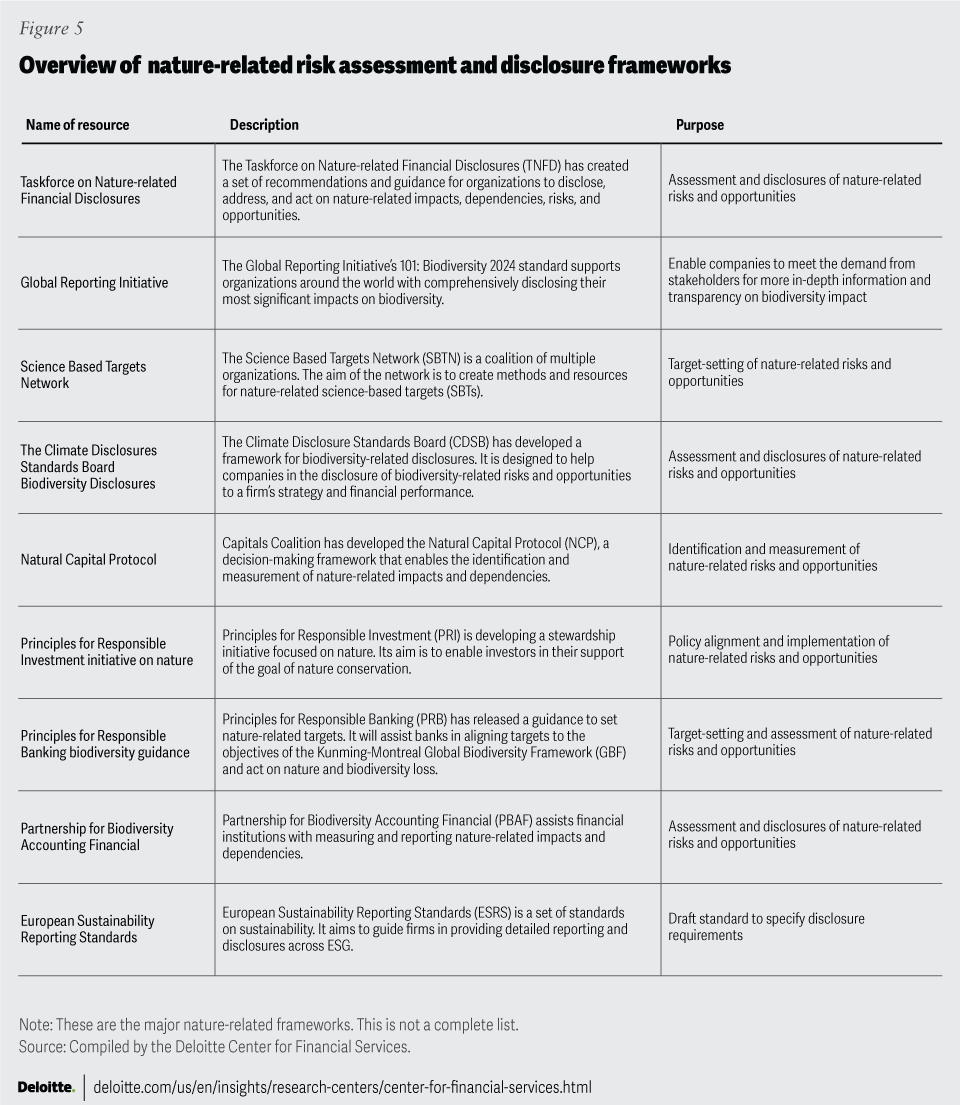

But now, there are multiple principles, frameworks, and standards (collectively labeled as “resources”) that can be leveraged to enable institutions in addressing nature-related risks and challenges. Some deal with principles and targets, some provide standards for assessing, managing, and reporting on nature-related disclosures, and others offer tools for analysis.

However, the sheer number of resources can make it challenging for banks to determine which ones are most relevant, and how best to implement them, in the context of the organization. Figure 5 provides an overview of some of the more well-known resources related to natural capital and biodiversity. While the list is not exhaustive, it can act as a starting reference point.

In addition to the variety of frameworks published, banks can also leverage different biodiversity-related tools that can help them measure their impacts and exposure to nature. For instance, banks can utilize the ENCORE system to capture potential impacts and dependencies on nature to kick start their risk assessment journey. The tool also categorizes the different ecosystem services to highlight how banks may be exposed to natural capital degradation.58 The Integrated Biodiversity Assessment Tool is another tool that can be helpful in banks’ investment processes to screen projects on nature-related risks.59 Many financial institutions are already incorporating it to inform their nature-related decisions.60

{kind=link}

TNFD should be a core guiding framework for nature-related actions within banks

Among the first steps on this nature-positive journey, banks should consider principles and aims of the Global Biodiversity Framework that was finalized at the United Nations Biodiversity Conference (COP15) in Montreal in late 2022.61 For the first time, the Global Biodiversity Framework included specific voluntary commitments by governments to reduce and reverse nature loss by 2030. Specifically, Target 15 under the framework highlights the potential role of business in assessing and disclosing risks, dependencies, and impacts on biodiversity.62

But when it comes to taking action to create nature-positive outcomes, the recommendations set forth in the final TNFD should be embraced.

The taskforce aims to help identify, assess, manage, and report on nature-related dependencies, impacts, risks, and opportunities (“nature-related issues”), encouraging organizations to integrate nature into strategic and capital allocation decision-making.63

The TNFD framework is built around the same four pillars of governance, strategy, risk and impact management, and metrics and targets—consistent with the approach of Task Force on Climate-related Financial Disclosures (TCFD).64

Recommended disclosures within the “governance” pillar deal with banks’ oversight, role, and policies related to nature. The “strategy” pillar focuses on the material effects of nature on business model, strategy, and financial planning. The “risk and impact management” pillar highlights the processes to identify, assess, and manage these effects in direct operations, supply chains, and overall risk management processes. “Metrics and targets” describes the nature-related metrics in use, and targets and goals set by the bank, along with its performance on the same.65

One key aspect of the TNFD recommendations is that they incorporate existing frameworks, assessment metrics, and disclosure practices—including those of the International Sustainability Standards Board (ISSB) and the GRI.66 Other features include:67

- Alignment with GBF: TNFD explicitly incorporates the Kunming-Montreal Global Biodiversity Framework’s goals, including the reporting of nature-related risks, dependencies, and impacts.

- Consistency with TCFD framework and ISSB: TNFD closely aligns with TCFD, ISSB, and the EU’s Corporate Sustainability Reporting Directive, providing a strong basis for nature-related disclosures. In fact, TNFD included all the 11 TCFD-recommended disclosures, which have now been incorporated into the ISSB Standards. Those banks that have adopted TCFD disclosure practices should be at an advantage in implementing TNFD.

- Accommodation of different approaches to materiality: Different jurisdictions and users define materiality differently, resulting in non-uniform disclosures. TNFD recognizes this divergence and offers a “double materiality lens.” The first, as a baseline, should be the International Sustainability Standards Board’s definition and approach to material information for general purpose financial reports. The second, if required, may use an additional materiality approach such as GRI and ESRS, that are incremental to the global baseline.

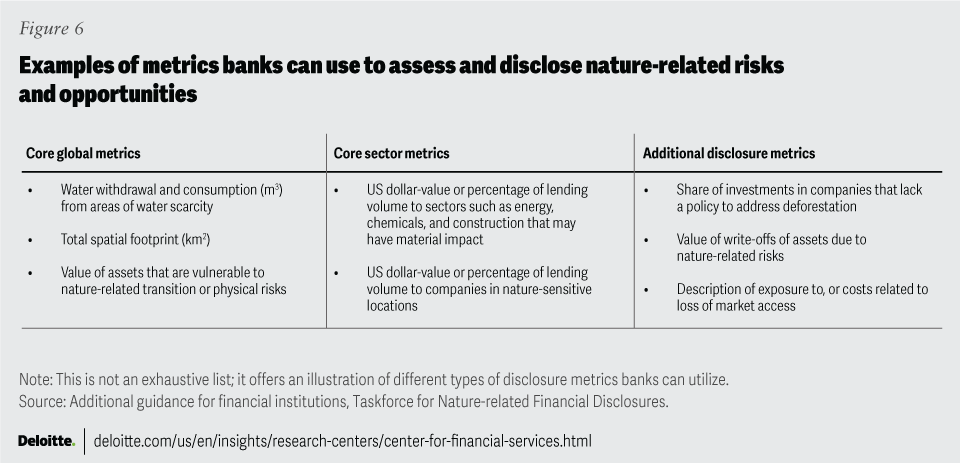

- Specific guidance on metrics assessment: Considering the complexity and vastness of nature, measuring an institution’s impacts on nature and biodiversity can be a daunting task. It often requires multiple metrics and indicators, that may not be uniform or easily comparable. To simplify this process, TNFD recommends three different categories of metrics: a small set of core global metrics that apply to all sectors, core sector metrics for each sector, and a set of additional metrics that best describe and capture the institution’s risk and exposure profile. Banks should look to use a combination of all the three aforementioned categories based on individual risks considerations to assess and disclose their impacts on nature and biodiversity. Figure 6 offers some examples of metrics that can be used by banks.

{kind=link}

- Use of the LEAP approach: TNFD also recommends using its LEAP framework (locate, evaluate, assess, and prepare)—a four-phased assessment approach to assess and manage nature-related issues. This acts as a “how to” guide for firms to identify potentially material issues. It builds on existing frameworks including the Natural Capital Protocol and the Science Based Targets Network methods.

TNFD recognizes that certain nature-related data may be hard to collect, creating roadblocks in implementation. However, improvements in data collection techniques and innovations in machine learning could help overcome the data challenges. TNFD’s Nature-related Data Catalyst initiative is an example of an effort that can help to accelerate such solutions and offer ways to accelerate the development and access to nature-related data.68

Current ESRM policies may require a revamp to adopt nature

For years, environmental and social risk management (ESRM) programs and policies have been an integral part of banks’ efforts to identify and manage environmental and social risks. In fact, many top US banks have adopted IFC PS6 in their existing ESRM programs. However, the current approach collectively remains largely inadequate as many of them are yet to address biodiversity and natural capital risks explicitly and comprehensively. ESRM programs should be seen as the foundation on which to build nature-positive policies. For instance, nature-related scoping assessments can be used to start with current state assessments–looking at what a bank is already doing and building off of that to integrate nature strategy into the bank’s overall sustainability strategy. There are already some tools that can be beneficial in scaling efforts related to biodiversity and natural capital.69

However, looking ahead, there is scope for improving ESRM programs by more explicitly accounting for and managing nature-related risks and opportunities. ESRM teams should also focus on the actionability of nature-related data. They should look to combine its applicability with the current targets on greenhouse gas emissions. The due diligence programs and screening methodology within ESRM can also leverage TNFD’s LEAP approach to streamline their nature-related assessments. Banks should also keep an eye on technology modernizations related to nature and climate. This could be particularly helpful for banks as they integrate environment and social factors into their transaction platforms and, at the same time, comply with evolving regulations.

US banks should start now to potentially reap nature-positive benefits in the coming years

As US banks embark on the journey to create, embrace, and execute nature-positive solutions,70 they should focus on enhancing the understanding of natural capital and biodiversity concepts, frameworks, resources, and metrics among their risk management and business groups, and also the board of directors, senior executives, and other stakeholders.

As banks look to judicially invest their resources, they should consider doing so in three stages: prepare, integrate, and execute.

- Prepare: Despite the increased focus on biodiversity and natural capital, many in the rank and file at banks may not fully appreciate their criticality and potential impact on banks’ risk profile and opportunity sets. Banks should fully understand where they stand in terms of their role and exposures to natural capital degradation and thereby, develop a nature-positive strategy. These programs may include:

o Scoping and identifying nature-related risks and opportunities within a bank’s value chain using internal and external resources. Partnering with external organizations, such as academic institutions and industry associations can enhance understanding and applicability of the various external resources.

o Understanding internal climate or sustainability related initiatives that can be integrated with nature and biodiversity. This may include current state assessment to identify current teams and infrastructures in place such as the ESRM function, that can act as a strong foundation to build nature-related initiatives and policies. Encouraging cross-functional collaboration can also foster a holistic understanding of climate change and nature-related risks.

o Educating business groups, senior executives, board of directors and other stakeholders through nature-focused knowledge-sharing platform and comprehensive internal communication plan, to raise awareness about nature-related risks and opportunities.

o Establishing a nature-focused governance framework to formulate clear roles and responsibilities for nature-related risk management within the organization, helping ensure accountability and ownership at all levels.

o Formulating a robust and comprehensive strategy for nature and biodiversity with the identification of nature-related goals and targets.

o Developing and publishing policy mandates based on high-risk projects, industries, and geographies that require nature assessment to take place during underwriting and financing activities. TNFD’s LEAP method can be particularly useful in informing the policy standards that require ongoing risk assessments of operations, suppliers, and clients.

o Utilizing the TNFD framework to understand the different types of metrics relevant to current and future banking operations.

- Integrate: After ensuring that the organization is sufficiently familiar with nature and biodiversity-related issues, banks should strengthen their analytical capabilities and integrate nature-related policies into decision frameworks. Some steps to consider in this regard are:

o Integrating nature-related goals and targets with ESRM (for more information, read sidebar on revamping ESRM policies).

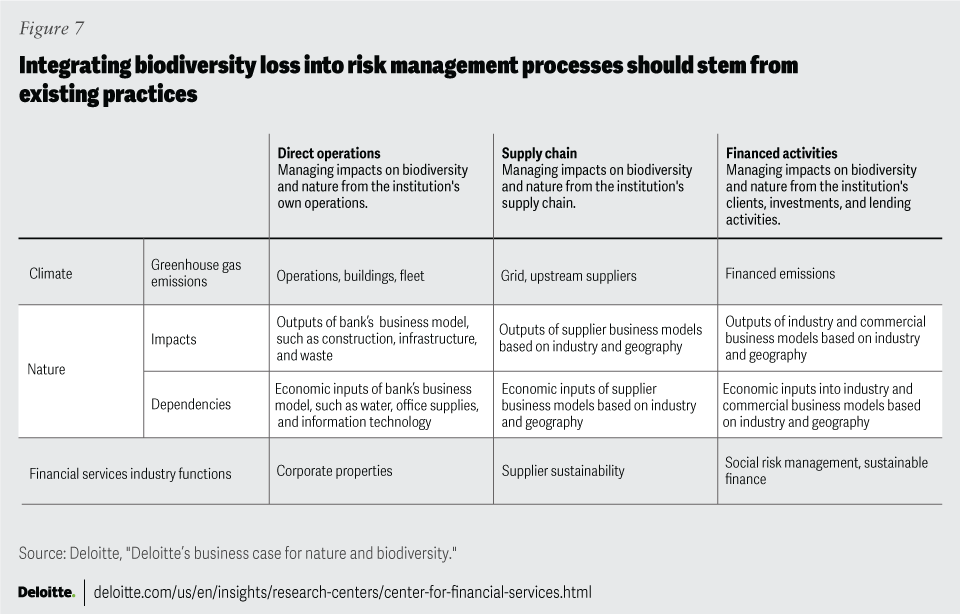

o Aligning nature-focused programs with climate oversight mechanisms. Banks can utilize the existing greenhouse gas scope approach to integrate nature into risk management practices (figure 7).

{kind=link}

o Analyzing portfolio exposure to biodiversity loss, based on high-risk industries and geographies. Tracking the use of innovative technologies to measure, monitor, and analyze biodiversity and natural capital-related data is also important. For instance, banks can use artificial intelligence to catalogue environmental change and generate on-demand data driven information for risk and credit assessments.71

- Execute: The final step is executing on the nature-related strategies and policies and embedding the principles and practices into the organization’s operations, processes, and decision-making. These activities may include:

o Executing policy standards and performing nature risk reviews on clients and suppliers with escalation, decisioning, and mitigation protocols. This may include implementing nature-related policies into underwriting and financing activities as well as assessing supply chain clients to assess impacts and dependencies across the value chain.

o Launching nature-positive products or services such as biodiversity credits in emerging nature-markets. Investing in opportunities related to renewable resources that are targeted for revival of nature and biodiversity. Banks can, perhaps, particularly focus on investments that can amplify other nature and climate related initiatives. For instance, use of solar energy with low carbon footprint aimed at protecting and preserving coral reefs.

o Conducting regular audits and assessments to evaluate the effectiveness of the organization’s nature and biodiversity risk management efforts and identify areas for improvement. Banks should also be conducting ongoing reviews of the firm’s nature strategy and policies to help ensure they remain relevant and effective in the face of changing circumstances and emerging risks.

o Monitoring progress toward goals and determining if targets are still relevant, achievable, and impactful.

o Implementing a nature-positive reporting process to disclose environmental performance progress. Aligning nature-related stakeholder communications with existing ESG reporting and disclosure.

o Engaging external stakeholders, such as customers, suppliers, investors, and regulators to create awareness as well as build a feedback network to further refine the organization’s nature strategy and policies.

o Using social media and other digital communication channels to share nature-related news, updates, and success stories both internally and externally, showcasing the organization’s commitment to addressing nature-related risks and opportunities.

Path forward

As US banks embark on their nature-positive journey, they should explicitly account for nature and biodiversity in their business models and risk management processes. They should recognize the interdependencies between nature and climate change and look for ways to best integrate nature-focused initiatives with existing climate change and net-zero activities. US banks should also adopt standards and frameworks in making this transition.

By

Ricardo Martinez

Stephanie Cárdenas

Sarah Haley

Val Srinivas

Abhinav Chauhan

The authors would like to thank the following Deloitte colleagues for their extensive contributions, guidance, and support:

Jill Gregorie, Elizabeth Payes, Patricia Danielecki, Paul Kaiser, and Jaime Austin.

Cover image by: Jaime Austin

Visit the Deloitte Center for Financial Services

Access more insights for the banking and capital markets, commercial real estate, insurance, and investment management sectors.