How carbon markets should evolve to meet net-zero ambitions

The world needs more integrated, transparent, and robust carbon markets to decarbonize at scale. Stakeholders should act now to foster cross-border and cross-market convergence while working to raise the bar on certification standards.

Key takeaways

- Carbon markets play a fundamental role supplementing the avoidance and reduction of greenhouse gas emissions in the global transition to a low-carbon economy. Yet, they are not meeting their full potential.

- Voluntary carbon markets have been hampered by concerns over market fragmentation, carbon credit quality, and transparency of project and transaction data. To help overcome these challenges, stakeholders should collaborate on common certification criteria, market infrastructure upgrades, and financial innovation. Many cap-and-trade systems could also benefit from greater integration.

- Several industry associations and supernational organizations are piloting novel approaches to help improve carbon market infrastructure, simplify trading processes, and deliver greater benefits to local communities. These initiatives include new methods of financing small projects and prototypes of blockchain and tokenization. Still, much more can be done to strengthen the global carbon trading ecosystem.

- COP28 could further boost confidence in carbon markets and offer clear next steps on a host of outstanding issues. Pressure is mounting for negotiators to agree on the methodologies and activities that should be eligible under the Article 6 framework. They could also finalize decisions on the functional architecture of United Nations (UN)-run international carbon markets.

The world has about a decade left to avert irreversible damage from climate change,1 but charting the path to a more sustainable future will require significant financing, targeted investments, and global cooperation to address emissions impacts in a meaningful way. Carbon markets can contribute to all three of these goals, but to do so, they should first become more robust and credible. Otherwise, the current state of this ecosystem—characterized by fractured marketplaces, frameworks, and approaches—could preclude it from bringing about rapid decarbonization at scale.

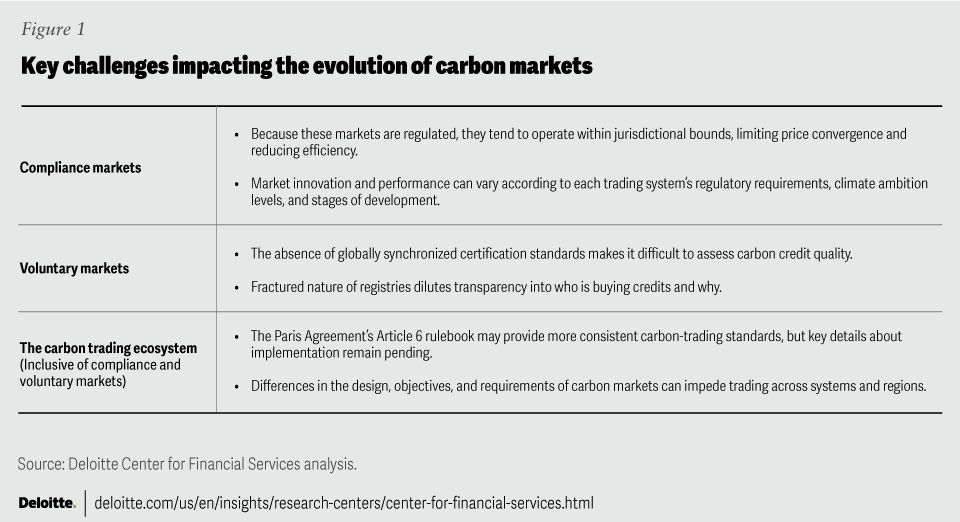

While carbon market infrastructure has rapidly evolved over the past five years, it tends to be highly fragmented with several structural and operational challenges hampering progress, including a lack of trust in the environmental integrity, credibility, and additionality of carbon credits (figure 1). While compliance carbon markets (CCMs) are well established on their own, diverging regulatory requirements across jurisdictions, different levels of climate ambitions, and varying stages of development are preventing greater convergence among markets. Voluntary carbon markets (VCMs), where governments, organizations, and individuals can purchase credits at will, also tend to be fractured, in part because of the sheer number of actors who operate within them.

As a result, buyers, sellers, and intermediaries may find it challenging to monitor and validate underlying credits in a systematic, credible, and consistent way. This has introduced possible reputational risks and contributed to lower demand: some companies, for example, have stopped including carbon credits in their climate pledges and net-zero targets altogether.2 Such reluctance from potential buyers may also be keeping carbon prices low.

{kind=link}

One important tool to elevate the effectiveness of carbon markets and enable greater cross-border trading is the Paris Agreement Work Program. In particular, the guidance on cooperative approaches under Article 6.23 and the rules, modalities, and procedures (RMPs) for the Article 6.4 mechanism agreed upon at COP264 set up a functional architecture for implementing international carbon markets and clarify how governments should account for credits in national emissions targets. Through cooperative approaches to transfer carbon credits between countries, known as internationally transferred mitigation outcomes (generally referred to as “ITMOs”), the provisions outlined in Article 6 could help bolster voluntary markets by enabling corporations and individuals to participate in a synchronized global system that abides by the same policies for authorizing carbon emission reduction claims as governments do. It could also be effective in promoting further decarbonization: If countries reinvest the savings from using ITMOs into additional climate measures, they can collectively double their total emissions mitigation worldwide.5

Although substantial progress has been made, this is not a simple undertaking, and pressure is mounting for negotiators to clarify key implementation details before the conclusion of the 2023 UN Climate Change Conference in Dubai.

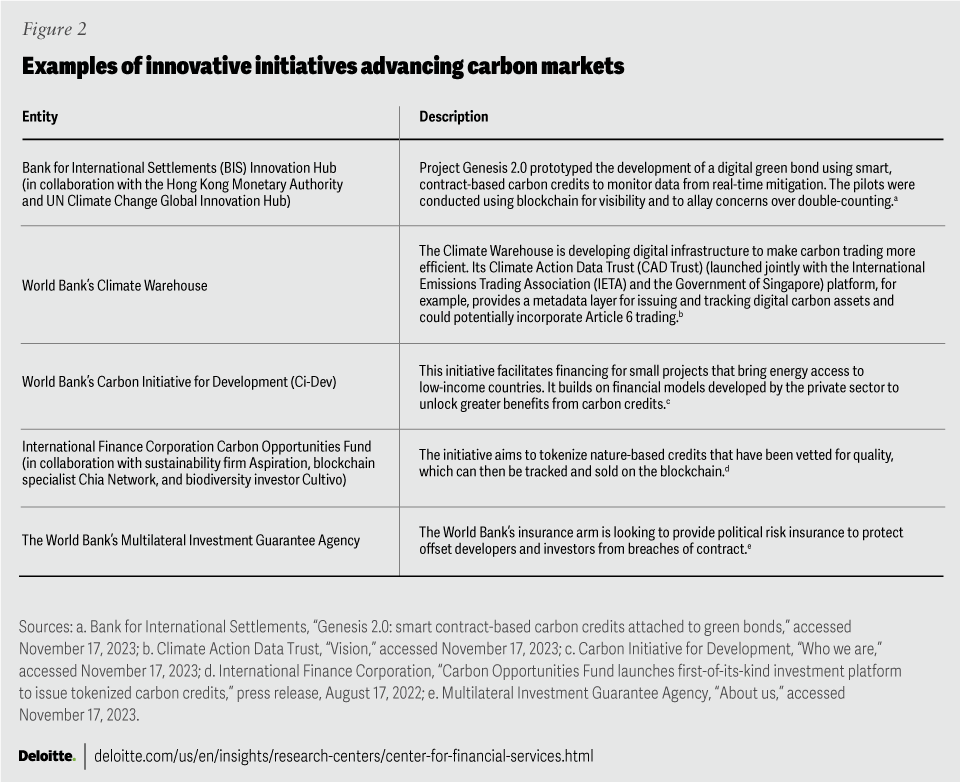

In addition to the UN’s efforts, industry associations and other global organizations are also advancing initiatives to help bolster market transparency, foster innovation, and deliver carbon credit benefits. Private-sector groups, such as the supply side-focused Integrity Council for the Voluntary Carbon Market and the demand side-focused Voluntary Carbon Markets Integrity Initiative, are working to build trust in the supply of carbon credits and guide businesses on how to use them in their net-zero pathways.6 Other groups are piloting novel approaches to refine carbon trading operations and enhance their outcomes (figure 2).

{kind=link}

The momentum to improve transparency and create more consistent global standards is gaining ground and should be pushed ahead. Greater connectivity between compliance carbon markets and voluntary carbon markets can improve fungibility, making trading networks more efficient, credible, and liquid. And stakeholders from across the business community and public sector can collaborate to build a system that supports a net-zero future by delivering measurable carbon emissions reductions throughout the global economy.

How the Paris Agreement could breathe new life into carbon markets

After six years of negotiations, the Paris Agreement’s Article 6 rulebook has been widely seen as a milestone to help grow carbon markets. This rulebook lays the groundwork for a UN-run global trading system modeled after the Kyoto Protocol’s Clean Development Mechanism. Article 6.2 specifies how carbon credit transfers should be accounted for,7 while Article 6.4 sets up a functional architecture for implementing international carbon markets and clarifies how governments should account for credits in national emissions targets.8

Credits authorized under the Article 6 rules also incorporate a “corresponding adjustment” to certify that a carbon credit’s emission reductions are not included in the seller country’s national climate goals, and can thus be claimed by outside buyers. This accounting mechanism would allow nongovernmental organizations to purchase UN-accredited carbon credits, which provide assurance that the buyer alone will retain its climate benefits.

The implementation of Article 6 rules could create two tiers of credits. The first would consist of “adjusted” credits that help ensure emission reduction claims are only granted to the end buyer; while the second tier would offer “non-adjusted” credits that could be used for purposes other than offsetting, such as facilitating results-based finance or addressing unavoidable emissions.9 It’s expected that demand for Article 6 compliant credits could cause the latter to be seen as lower quality, which would drive down prices and present concerns over reputational risk.10 In anticipation of this potential outcome, some voluntary carbon credit certifiers have begun prepping for a decision on whether to align crediting standards with Article 6 frameworks, tweak methodologies to be more competitive, or let supply-and-demand forces take their course.11

Article 6 in action

Article 6.2 agreements are gathering momentum around the world, as countries seek more tools to achieve their nationally determined contributions (NDCs). Switzerland, for example, has entered commitments with a dozen countries, including Ghana, which it authorized at COP27.12 For its part, Ghana is also actively building out Article 6.2 capabilities. It has launched a carbon market office, unveiled a national Article 6 framework, and made enhancements to the Ghana Carbon Registry.13

Japan has also emerged as a prominent buyer country in Article 6.2 pilots.14 Additionally, it has established the Article 6 implementation partnership to help countries share leading practices.15 Similarly, the Climate Market Club, comprising national governments and private entities, seeks consensus on common principles and approaches for piloting activities under Article 6.2.16 These countries should consider making a pledge to incrementally increase their climate ambitions over time to avoid the perception that they’re relying on ITMOs—and not domestic mitigation efforts—to meet their NDCs.17

As governments continue to pilot Article 6 programs and share support for capacity-building, it should become easier for neighboring countries to pursue greater collaboration and integration at the regional level. These regional carbon markets may provide the infrastructure and groundwork for the future emergence of a global carbon trading system.

In addition, increased interlinkages between emissions trading systems (ETSs), or cap-and-trade programs, can also spur the global transfer of ITMOs. For example, the EU and Switzerland plan to trade emission allowances between their ETSs for NDC achievement as permitted under Article 6.2, but the countries are still contemplating how to prevent the influx of mitigation outcomes from increasing caps on emission credits.18

As debates continue about how to operationalize a UN-initiated carbon trading system,19 countries can pursue efforts to reach bilateral and multilateral agreements as permitted by Article 6.2. These agreements should also extend to letters of authorization, fulfilling reporting requirements, monitoring mitigation activities, and recognizing the transfer of mitigation outcomes between registries.20

Article 6: Key outstanding considerations

Operationalizing Article 6 is not a simple endeavor, so negotiators should clarify key implementation details during the 2023 UN Climate Change Conference in Dubai. Among the many questions are:

- How to fit voluntary carbon markets into the global carbon trading system if they are not Article 6-compliant:21 Market participants are clamoring for agreement on the eligibility of activities and methodologies for Paris-approved trading, especially as they pertain to the role of carbon avoidance and removals.22

- The mechanics of authorizing Article 6 credits:23 Carbon credits under Article 6.4 are not expected to be issued until 2024 or 2025, given that decisions on crediting methodologies, registry operations, and human rights safeguards remain unresolved.24

- How the functional architecture for a UN-run carbon market may be designed and implemented: The market infrastructure to support ITMO transfers remains under development. COP27 made strides in developing registries, an Article 6.2 database, and a central accounting and reporting platform, but these tools are not expected to be functional until 2025.25

There is reason to believe that progress will be made at COP28. COP28 Director-General Majid al-Suwaidi has called on attendees to instill trust in carbon markets by coalescing around shared carbon crediting standards,26 and participants of the 2023 Bonn Climate Change Conference delved into technical discussions that should influence the COP28 agenda.27 Taken together, these talks could give way to decision-making on the authorization and possible revocation of Article 6 credits, the role of carbon removal activities, and how Article 6.4 registries should operate.28

To meet decarbonization needs at scale, compliance carbon markets should push for greater integration

At the start of 2023, more than two dozen compliance markets operated around the world, and several more are expected to launch in coming years.29 These include:

- Cities such as Shenzhen and Tokyo;

- States and provinces, such as California, Quebec, and Guangdong;

- Nations, such as Mexico, South Korea, and New Zealand; and

- Supranational entities, such as the EU Emissions Trading System (ETS).30

To facilitate greater market integration, many governments are starting to link their compliance markets. This move can bring a number of potential benefits, including expanding their scope of coverage and enabling progress in local jurisdictions, such as states or cities, where national-level mandatory climate action may not be feasible.

Linking markets can also lead to price convergence.31 Establishing a common carbon price across systems can minimize price fluctuations and increase liquidity. Additionally, linkages can cause the overcall cost of emissions to fall by allowing companies in regions with higher abatement costs to purchase allowances from regions where abatement is cheaper. This, in turn, can prompt countries to set more ambitious climate targets for their public and private sectors. In fact, a 2017 study found that an international linkage of worldwide ETSs could reduce the total expense of achieving NDCs by 32% before 2030, and by 54% before 2050.32

The 2014 linkage between the cap-and-trade systems in the state of California and the province of Quebec systems (the first international linkage) is an example of a relationship that delivered value to both entities by significantly reducing emissions while generating billions of US dollars in revenue. The initiative has been so successful that the state of Washington is considering joining, nearly a full decade later.33 These jurisdictions are also considering states and provinces beyond North America and may soon try to recruit additional states within Mexico and Brazil.34

States in the Northeast United States are also espousing the benefits of linkages. New York, for example, is already part of the 12-state Regional Greenhouse Gas Initiative (RGGI), which sets regional caps on emissions from power plants.35 Its forthcoming “cap-and-invest” program seeks to return one-third of revenues to consumers, while the rest would support renewable energy projects.36 This revenue model is similar to California’s cap-and-trade system that funds the Greenhouse Gas Reduction Fund, which has generated US$9 billion for investments in energy-efficiency, public transit, and affordable housing. The governor of New York has indicated that its program will be designed to easily link with other jurisdictions.

There are also varying degrees of linkages that jurisdictions can pursue, depending on their capabilities and how closely they wish to be interlinked. Direct or “full” linkages permit jurisdictions to buy and sell allowances across trading systems. The Swiss ETS and the EU ETS have a direct linkage that creates a single carbon price and permits members to use allowances in both systems. The UK ETS, which was created in 2021 after Brexit, may seek a direct link with the EU ETS, or possibly a new multilateral arrangement altogether.37 Indirect linkages, on the other hand, are less formal, but can involve sharing design elements, leading practices, or experiences and information.

When China was setting up its new carbon market, the state of California offered advice on design, reporting and verification protocols, and enforcement mechanisms. As a result, the California-Quebec carbon market and Chinese ETS have similar emission thresholds and reporting requirements, and firms doing business in China and California may swap or trade credits from one carbon market for credits in the other through structured financial deals.38 Eventually the governments may seek a more direct linkage.39

National-level cap-and-trade programs can also embed Article 6.2 accounting principles into their linking agreements so the resulting change in emission flows are reflected in their NDC calculations. Although Article 6.2 provisions are not a prerequisite for linkages, they can help reduce the risk of double counting and make it easier for countries to stay on track toward NDCs.40 When negotiating new forms of voluntary cooperation, leaders can incorporate Article 6.2 through memorandums of understanding, treaties, or informal agreements, as Singapore did with countries such as Bhutan, Cambodia, Colombia, Kenya, Peru, and Sri Lanka.41 These agreements can add more credibility to carbon market collaborations since Article 6.2 accounting, reporting, and disclosure obligations were designed to boost transparency and environmental integrity.

Linkages may be easier to establish between countries in close proximity, especially if they share similar environmental goals, economic backgrounds, and histories of mutually beneficial trade agreements.42 The linkage of the EU’s carbon market with the Swiss market is an example of a relationship that has benefited from existing ties. Carbon markets are also easier to converge when they have compatible design and market structures, including similar methodologies for certifying carbon credits, platforms for storing registry data, and penalties for noncompliance.

Moreover, linkages centered on regional hubs can harmonize governance and design frameworks, as several US and Canadian jurisdictions did when drawing up the Western Climate Initiative (WCI). This program design not only laid the groundwork for California and Quebec’s partnership,43 but it has been used as the model for carbon markets in British Columbia, Manitoba, Ontario, New Mexico, and Washington state.44 Some jurisdictions in Latin America are also considering entering the WCI, which could open the door to more Pan-American linkages, and possibly even a Western Hemisphere–wide carbon market.45

Other parts of the world are also making moves to become carbon-trading hot spots. Singapore, for example, is heavily investing in its capabilities, building upon its experience in commodities trading in the hopes of emerging as the central trading hub within Asia.46 And during the inaugural African Climate Summit, Kenya signaled its intention to become the continent’s carbon trading powerhouse.47 The country’s September 2023 Climate Change Act will introduce a national carbon registry and help regulators guide participation in global carbon markets, including through Article 6 mechanisms.48 These efforts could be impeded by countries imposing trade restrictions that keep the social benefits of emission-reduction projects within their own borders. Malawi, Zambia, and Zimbabwe are redirecting revenues from projects to local stakeholders,49 for example, while India50 and Papua New Guinea51 have temporarily banned external sales entirely.

Creating new regional carbon markets or facilitating greater integration among them using Article 6.2 cooperative approaches can create common infrastructure, align pricing mechanisms, and attract new players. These regional markets could eventually serve as the groundwork for a global trading regime, helping ensure that countries are better prepared for greater market convergence. Just a handful of countries working together to establish a minimum carbon price could provide a marked boost to carbon markets. The G20 economies together will account for 85% of the world’s emissions in 2030—and their alignment on a carbon price floor could advance climate equity, given their record of historical emissions.52

Voluntary markets should aim for more robust architecture and standards

Greater market integration would also be advantageous to the splintered and siloed voluntary carbon markets, which generally lack common standards, contract terminology, regulatory frameworks, and trade infrastructure. One of the key elements missing from VCMs is a platform that can aggregate and harmonize carbon credit market data collected from various project registries, which typically use their own private crediting standards.53 A meaningful share of carbon credit retirements—which occurs when credits are taken out of circulation because stakeholders claimed their climate benefits—often do not provide information about who purchased the credit or why, thus diluting transparency.

Improving visibility into market transactions is important for preventing double counting, which happens when emissions reductions are claimed by more than one entity. It could also help with verifying additionality (showing that the benefits of carbon offsets projects go above and beyond business-as-usual operations). Increased transparency could likewise hold project developers, brokers, and end users accountable for the way they transact in and benefit from the emission claims of carbon credits. Currently, many trades in the spot and futures carbon markets are still executed over the counter, potentially diluting price discovery and market efficiency.54

Other significant challenges for voluntary markets include:

- New accounting standards: Some market participants are calling on the International Accounting Standards Board (IASB) to update the definitions of financial instruments for carbon offsets and set up specific standards for the novel asset class.55

- Lack of standardized terms and documentation for carbon credit contracts: Especially in the secondary market, where carbon derivatives are regulated as financial instruments, there is a need for clear and consistent terms for delivery and payment obligations. This should apply to futures and forwards contracts regardless of the registry involved in the transaction.56 Global regulators should also determine whether carbon credits qualify as commodities, and if so, how they should meet thresholds for title, quality, and fitness.57 Voluntary markets should also have more explicit guidelines on steps for handling issues that could occur during a carbon credit trade, such as a settlement failure or a delivery that goes awry.58

- Unclear role of offsetting in net-zero pathways: Some organizations are reluctant to use carbon credits to accelerate their transition to renewable energy until the UN, or standard-setters such as the Science Based Targets initiative (SBTi), specify the extent to which they can incorporate it into their decarbonization efforts. Some companies that have used offsetting to describe their products and services as “carbon neutral” are facing legal challenges over the veracity of those claims.59

- Insufficient fee transparency: Some exchanges, brokers, resellers, and vendors that buy and sell carbon credits currently fail to disclose their commissions and markups from those transactions. This has led to concerns that credits may be changing hands too many times, preventing funding from reaching its climate mitigation project destinations.

- Ongoing legal and compliance matters: There are several outstanding questions, including whether carbon credits are considered personal property,60 the divergence of carbon credits being treated as intangible assets or contractual rights depending on jurisdiction,61 and uncertainty about navigating Basel III capital requirements.62 In addition, conflicting bankruptcy laws may result in disparate approaches in how countries recognize carbon credits following insolvency.63

Despite these setbacks, stakeholders should not lose sight of the potential for voluntary markets to make strides on global decarbonization targets and bring about progress toward net-zero goals. While some may be quick to dismiss VCMs in the wake of negative press, heightened public scrutiny, and declining valuations, it would be short-sighted to ignore the significant strides that have already been made to evolve these markets. In the past decade, voluntary markets have not only reached US$2 billion in value,64 but they have taken significant steps to enhance monitoring and oversight mechanisms, refine methodologies for quantifying the cobenefits of underlying projects, strengthen accounting and reporting principles, and intensify the focus on communities and land rights in host countries. Even though some of these structural challenges may persist in the near term, continued investments in knowledge-sharing, capacity-building, and collective action to resolve systemic limitations can push voluntary markets forward.

How market infrastructure providers are fueling carbon market advancements

Both traditional market exchanges such as Intercontinental Exchange and CME Group and new operators such as Air Carbon and Climate Impact X have broadened the scope of opportunity for voluntary market participants by increasing the fungibility of heterogenous carbon credits and speeding up trading through standardized instruments that contain multiple offsets with similar characteristics, such as underlying project type or category.65 These exchanges also enable private deals to settle on their platforms, which can thereby enhance transparency and trust.66 By acting as central counterparties, exchanges also help to reduce credit risk, deepen market liquidity, and improve price discovery—and, with their positioning as intermediaries in global capital markets, exchanges can drive the development of technology, products, platforms, and services that mobilize capital to green solutions. Some exchanges are launching carbon credit markets that set listing rules for those companies that finance carbon reduction and offsetting projects, while others are exploring partnerships to advance token trading.67

In addition, innovation in derivatives markets that offer risk management should also spur greater participation. Banks, for example, working on behalf of suppliers, often look to lock in the price of carbon futures to cover project development costs.68 Similarly, corporate treasuries could also aim to hedge the risk of future prices of carbon credits as their business works toward net-zero objectives.69

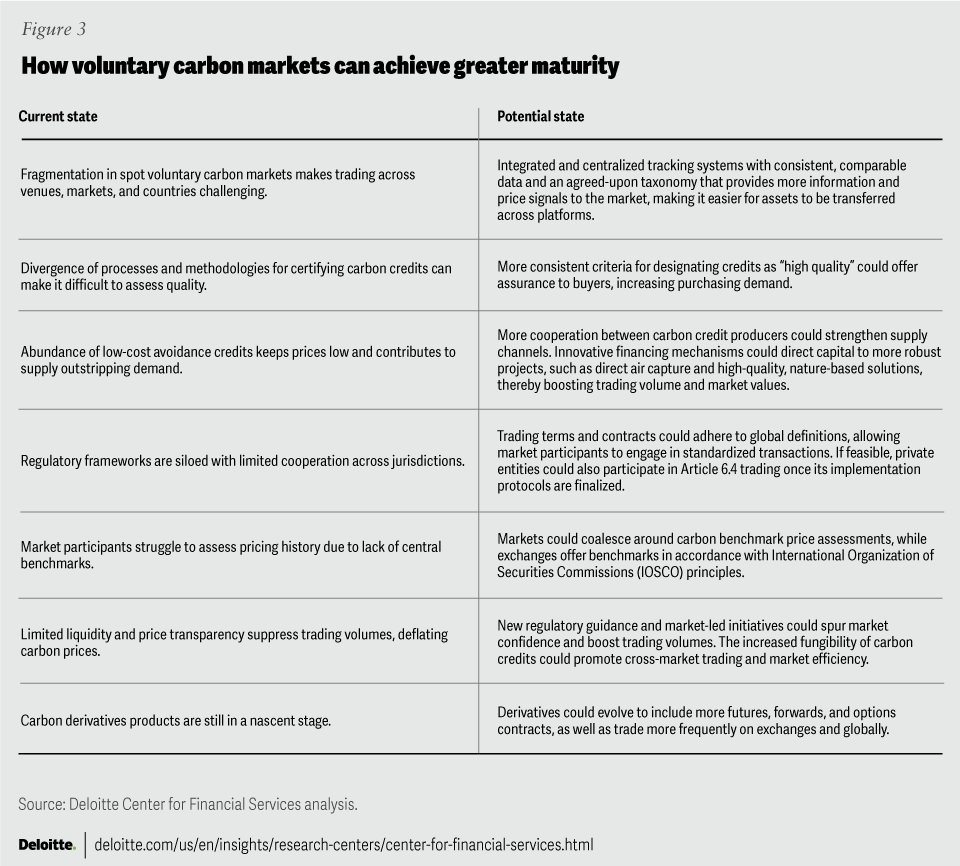

There is still more work to be done (figure 3). Concerns about carbon credit quality and the environmental integrity of VCMs have caused markets to contract from their 2021 peak, and futures prices fell between 38% and 77% between January and September of 2023.70 But efforts to establish trust and credibility could reignite demand as soon as 2024. Currently, it is believed that VCMs will be more effective if prices range between US$50 and US$100 per metric ton of carbon dioxide by 2030. Any price below the US$50 threshold may not be enough of an incentive to seek low-carbon alternatives.71

According to analysts from BloombergNEF, the aspirational state of well-functioning markets is an “Olympic pool,” insofar as they would be broad (covering many emission-intensive sectors) as well as deep (reflecting ambitious climate goals).72 If the veracity of carbon credits improves and voluntary markets have more credits from removal technologies that are often priced at a premium, BloombergNEF’s analysis suggests the size of the market could reach US$1 trillion by 2037.73 At the moment, only about 3% of carbon credits are currently based on pure removal projects, while durable removal credits—which effectively reverse the impact of releasing carbon dioxide into the atmosphere—are essentially nonexistent.74

{kind=link}

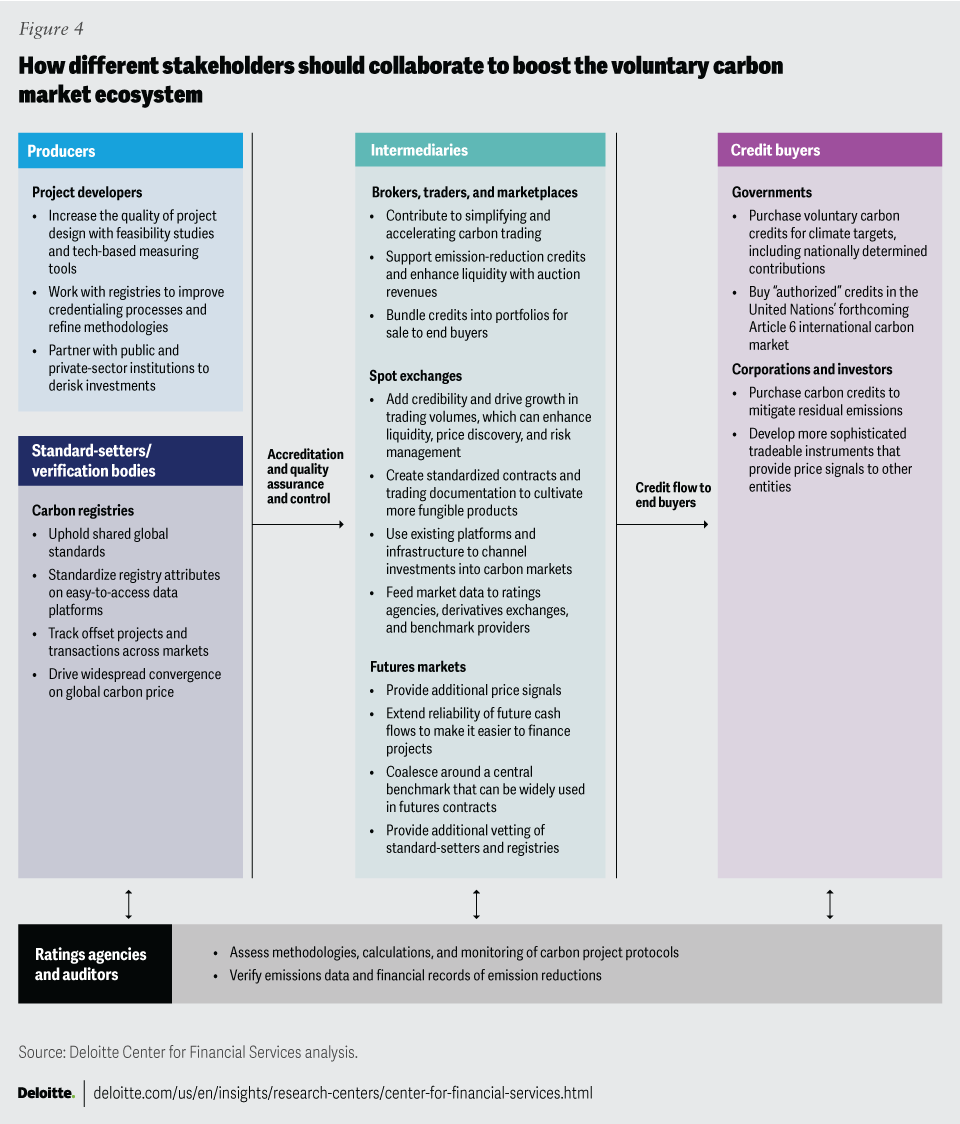

Industry-led efforts can also infuse more trust in the VCMs (figure 4). The Integrity Council for the Voluntary Carbon Market has released Core Carbon Principles (CCP) that certify whether credits and methodologies meet a minimum threshold of governance, emissions impact, and sustainable development goals. The first standardized carbon credits with a CCP label is expected to be released at the COP28 climate summit in late 2023, and accredited futures contracts could soon follow.75 It is estimated that about 20% of currently registered carbon projects would qualify under the eligibility criteria.76 On the demand side, the Voluntary Carbon Markets Integrity Initiative (VCMI) has issued a Claims Code of Practice to help companies integrate carbon credits into net-zero trajectories. It calls on these businesses to pivot away from using carbon credits as a tool for offsetting in favor of using them for “above and beyond” decarbonization strategies.77

{kind=link}

Market convergence can provide much-needed consistency

Although cap-and-trade systems and voluntary carbon markets may have been designed with different goals in mind, creating the conditions for greater connectivity and integration between the two can yield more substantial progress toward net-zero. As a result, carbon markets are becoming increasingly interlinked, especially as governments take greater action to spur voluntary market participation. This convergence of market structures can improve fungibility, ultimately making trading networks more efficient, credible, and liquid.

On the supply side, carbon credit certifiers are producing more voluntary carbon credits that can be traded in regulated regimes. The Swedish government plans to use voluntary credits to meet some of its national climate targets.78 Similarly, countries such as Chile, Colombia, Singapore, and South Africa permit mandated firms to pay the national carbon tax using carbon credits from the voluntary markets.79 To accommodate compliance carbon market demands and to prepare for the pending wave of Article 6 trading, voluntary carbon registries are designing certification standards that meet the thresholds sought by governments. These carbon credits can then be used in both compliance and voluntary markets, helping to close the gap between different trading regimes.80

Some countries are taking even more assertive action to promote carbon trading. Japan, for example, recently unveiled the GX League, a 10-year initiative that creates a voluntary carbon market for domestic industries. In the future, the ETS could grow to include a cap-and-trade program and carbon levy.81 So far, more than 600 companies responsible for 40% of the country’s emissions have chosen to participate since the market became operational in April 2023.82 Similarly, Australia’s government has also put a voluntary carbon market in place that’s primarily centered on Australian government-issued credits.83 Businesses can purchase these credits if they exceed the emission caps established by the Australian government. In both instances, increasing the comparability of credits has made supply more trustworthy and easier to track.

Created through the International Civil Aviation Organization (ICAO), the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) is another example of a hybrid program. More than 100 countries agreed to particulate in the voluntary pilot phase, which will become mandatory between 2027 and 2035.84 Each government consented to abide by two standards: one that establishes credibility in the program (such as by requiring that host companies attest they will not use the underlying projects for their NDCs), and another that creates parameters on which verified carbon units (VCUs) can be used as CORSIA-eligible carbon credits. Airline operators have accounted for more than 96% of their emissions between 2019 and 2021,85 and the cooperative approach is expected to mitigate 164 million tons of carbon a year, the equivalent of the Netherlands’ annual output.86

Because the United States lacks a national ETS, it is trying to spur voluntary carbon market activity through more of an incentive-based approach. In 2021, the US Senate voted to establish voluntary carbon markets for farmers, many of whom want to adopt greener practices but need funding to upgrade operations.87 The US Department of State is also partnering with the Bezos Earth Fund and The Rockefeller Foundation to launch an Energy Transition Accelerator that will create a carbon market program consisting of host countries in emerging markets and private companies or government buyers.88 A nonprofit will be responsible for generating the credits, and participants will be encouraged to buy advanced purchase agreements to provide stable financial flows.89

Maturing the carbon trading system will require participation from all stakeholders

All stakeholder groups have a role to play in making carbon markets more robust, efficient, and credible to drive greater emission cuts and catalyze innovation in renewable energy solutions. Below is an outline of recommendations for each stakeholder group to help prioritize their efforts to instill more confidence and rigor to carbon trading systems.

Governments, policymakers, and regulatory agencies: Clarify guidelines to build confidence

Given the growing complexity of the carbon trade ecosystem and the nascency of many carbon-trading networks and platforms, government leaders and their oversight bodies can instill more credibility into carbon markets and offer guidance on how to participate in them. Whether they are project developers on the local level or large corporations with a global presence, stakeholders need clarity on the protocols they should use to generate and transact carbon credits. Public-sector institutions should particularly aim to provide guidance on Article 6–inspired initiatives, illuminate how to structure contracts for different types of carbon credits, help stakeholders navigate multiple legal jurisdictions, and assist with standardizing trading terms, definitions, and rulebooks.

Other actions to help advance the evolution of carbon markets include:

- Investigating and remediating allegations of misconduct, which can include trading “phantom” credits that may no longer exist; trading credits that overstate the extent or permanence of greenhouse gas mitigation; listing of credits with insufficient due diligence; and manipulating tokenized carbon credits.

- Working with other governments and supranational organizations, such as UN-affiliated bodies, to converge on carbon market regulations, so there is greater uniformity across the globe.

- Promoting the production of centralized trading platforms for voluntary carbon markets. For example, Australia and Japan developed government-issued carbon credits to legitimize assets and promote consolidation.90

- Allowing more high-quality, nature-based credits into compliance markets. Most cap-and-trade systems either forbid or severely restrict the use of these credits,91 even though nature-based solutions such as reforestation and soil carbon capture can have a major impact on emissions.92

- Providing guidance to emerging carbon commodity markets, similar to how the US Federal Energy Regulatory Commission advised on energy markets and the US Department of Agriculture assisted with agricultural futures products.

- Passing tax laws that urge the development of climate innovation to increase the supply of tech-based carbon credits in the market.

- Creating legislative frameworks to promote liquidity in mandatory carbon markets. For example, South Korea could begin allowing financial entities to participate in its ETS and China could permit trading of derivatives.

Industry groups, supranationals, and climate alliances: Identify and solve shared industry challenges

Since global carbon markets lack a single oversight body, industry groups and coalitions should adhere to shared commitments, standards, and goals. Industry associations can also play an important role in capacity-building and infrastructure development thanks to their collective knowledge and problem-solving abilities. In addition, alliances can work together to promote leading practices and encourage greater participation from governments, intermediaries, and buyers.

Other actions to help advance the evolution of carbon markets include:

- Drafting voluntary standards clarifying how organizations and countries can use carbon credits in their transition plans, specifying the extent to which they fit into net-zero frameworks and how those actions should be disclosed.

- Working with securities exchanges, both traditional and emerging, to support more liquid carbon markets through new products, platforms, and listing standards. They can also encourage consistency in contracts and products across markets.

- Developing and using certifications that advance robust sustainable development-related outcomes, promote high environmental integrity, and empower Indigenous people and local communities.

- Accelerating efforts to find convergence on a global carbon price or set a price floor based on thresholds for developed economies, high-income emerging economies, and low-income emerging economies.93

- Setting and enforcing a definitive global threshold for high-quality carbon offsets. These guidelines could provide a common approach for disclosing the projects’ qualifying criteria, additionality tests, and third-party audited data. Guidelines should continue to evolve as research on climate change mitigation and the effectiveness of offsetting continues to advance.

Buyers: Prioritize emissions reductions and take a rigorous approach to vetting offsets

The onus is on buyers to prioritize the reduction of emissions across their value chain, then use carbon credits to account for any residual emissions. They can also facilitate the creation of higher-quality carbon credits by adopting rigorous vetting procedures and signaling that “junk” assets will not be tolerated. They can prop up emerging voluntary standards for demand-side institutions by using new methodologies to account for carbon credits in their transition plans. And since many emerging solutions—whether they’re nature-based projects in developing economies or startups piloting new technologies—need massive amounts of capital, they should look to support or finance new producers that meet the quality and certification criteria.

Other actions to help advance the evolution of carbon markets include:

- Developing risk, compliance, and internal audit controls to assess the quality of carbon credits, oversee valuation, and evaluate how carbon credits fit into the organization’s overall carbon management plans. As part of this process for monitoring quality, they should have a plan to pivot from avoidance credits to carbon credits representing permanent carbon removal and storage.

- Investing in early-stage financing of carbon projects to catalyze new types of nature-based activities or to provide upfront investments for nascent technologies, even if they come with long-term offtake agreements, or contracts in which buyers remain committed regardless of future market price.

- Committing to significant purchases in regions that are looking to build out their carbon crediting infrastructure. For example, the private-sector coalition UAE Carbon Alliance has agreed to buy US$450 million worth of credits generated in Africa by 2030, and London-based Climate Asset Management plans to put forth US$200 million to support the African Carbon Markets Initiative’s projects.94

- Choosing carbon credits that have been acknowledged by registries or rating agencies to produce equitable outcomes in the locations where underlying projects are carried out. These describe projects that support local and Indigenous communities, respect traditional land rights, and preserve ecosystems.

- Align disclosures about carbon credits to appropriate regulatory regimes. Consumer protection laws such as the EU’s Corporate Sustainability Reporting Directive95 and California’s Assembly Bill 130596 may require communication about the quality of offsets and how they will be incorporated into net-zero plans.

Sellers and project developers: Spur capital flows

Project developers play an important role in supplying carbon credits that provide demonstrable climate benefits. They should work with government agencies, climate organizations, and researchers to stay current with the latest developments in carbon reduction and removal strategies, and to adopt leading practices whenever feasible. In addition, they can encourage peers to join crediting programs, and share knowledge, technical assistance, and resources to help them get started.

Other actions to help advance the evolution of carbon markets include:

- Reassure buyers of the integrity of the carbon credits they are selling by aligning projects with high-quality crediting standards. One impediment to obtaining CCP labels, for example, will likely be lack of project documentation,97 so updating procedures for compiling and submitting evidence may be essential.

- Project developers working without intermediaries may offer legal or insurance buffers against common risks, such as insolvency or the reversal of sequestration through climate-related events like wildfires.

- Consider trading on public exchanges, instead of over the counter, to reach a larger pool of market participants and further establish credibility as adherents to high environmental standards.98

Financial intermediaries, including exchanges, brokers, banks: Improve access to capital and drive efficiencies

Carbon markets need robust and reliable infrastructure that can facilitate capital flows and foster efficiency. Financial intermediaries have been hard at work developing the architecture for a global carbon trade, and they should continue striving to make products, platforms, and processes run as smoothly as possible. Innovation can take many forms, and in some cases, these entities may be able to build new capabilities on top of existing structures. The London Stock Exchange Group, for example, recently launched a new market for carbon credits that sets listing rules for companies that finance carbon reduction and offsetting projects.99 Intermediaries can also consider launching new tools that help carbon markets grow and evolve. Banks and financial firms can work to develop futures and forwards positions that channel implicit financing to climate investments.

Other actions to help advance the evolution of carbon markets include:

- Continuing working to securitize carbon credits and develop tradeable instruments that offer price signals to other entities. Providing liquidity to bridge the gap between bids and offers may also be essential.

- Establishing more robust spot-price benchmarks and risk management tools. Carbon markets should continue working toward common benchmarks that can help establish a fair market price, facilitate long-term contracts, and reduce information asymmetry.

- Investigating how to bring more efficiency into clearing and settlement processes in the secondary market.

- Having insurance providers develop products to mitigate market risks for carbon credit buyers. These buffers can give protection against risks related to physical losses, poor performance, contract exposures, and political turmoil.

Collective goals should guide progress

In addition to using their capabilities and experience to advance carbon markets, stakeholders should proceed with collective goals in mind. Efforts should be made to:

- Expand the scope of carbon credits to include other greenhouse gases, especially methane.

- Encourage buying and selling of credits that include cobenefits such as supplemental investments in community development, job creation, and biodiversity.

- Develop carbon markets in an equitable direction, with equity outcomes for Indigenous and local communities.

The way forward

Carbon markets are on the brink of attaining the size, depth, and maturity they need to mobilize capital flows to clean-energy solutions and advance the global economy’s net-zero transition. Stakeholders are essential to raising the bar on crediting standards, developing trade infrastructure, pushing for transparency and accountability, and introducing financial innovation. COP28 can open the door to global cooperation, and delegates should make it a priority to finalize long-awaited decisions on operationalizing Article 6 rules. The world showed its willingness to walk the talk on climate ambition when it passed those rules in a breakthrough vote at COP26; three years later, it’s time to see them through.

By

Freedom-Kai Phillips

Ricardo Martinez

Val Srinivas

Jill Gregorie

The authors would like to thank the following Deloitte colleagues for their extensive contributions, guidance, and support: Stephen Engler, Paul Kaiser, Erik Kiaer, Derek Pankratz, Elizabeth Payes, David Schatsky, Jonathan Schuldenfrei, and Steven Watkins.

Cover image by: Jim Slatton

Visit the Deloitte Center for Financial Services

Access more insights for the banking and capital markets, commercial real estate, insurance, and investment management sectors.