Unleashing a new era of productivity in investment banking through the power of generative AI

How can generative AI technologies transform investment banking? By bolstering employee productivity and efficiency while supporting superior customer experience and rapid innovation.

Generative artificial intelligence (AI) could well be one of the most transformative technologies for the investment banking industry. Deloitte predicts that the top 14 global investment banks can boost their front-office productivity by as much as 27%–35% by using generative AI.1 This would result in additional revenue of US$3.5 million per front-office employee by 2026.

The allure of generative AI powered by transformer models2 has not escaped investment bankers’ attention. The potential of the technology to transform investment banking activities seems to be vast, and the applications are far-ranging.

Investment banks can benefit from generative AI in multiple ways

AI and automation are not new to investment banking. In fact, machine learning/deep learning algorithms and natural language processing (NLP) techniques have been widely used for years to help automate trading, modernize risk management, and conduct investment research. However, despite the billions of dollars spent on automating the various functions across the transaction life cycle, there are still a fair number of tasks that are conducted using precious human capital.

But large language models (LLMs) could help automate many tasks, not only saving money but also improving worker productivity. It could also free up resources to spark innovation and enable front-office staff to focus more on productively interacting with clients.

Generative AI can have a large impact on productivity across financial services

Results of recent studies on generative AI’s impact on productivity look promising. One study by Stanford researchers found that generative AI boosted a call center’s productivity by 14%.3 Another study by Massachusetts Institute of Technology concluded that generative AI helped reduce time and improve the quality of work for marketers, consultants, and data analysts.4 One common finding is that the technology can level the playing field and can, in particular, assist lower-skilled employees improve their outputs and productivity. Nonetheless, initially, lower-skilled workers may need to exert greater validation efforts.

Given such promise, the industry is swarming with numerous proofs-of-concept (POCs) and experiments. JPMorgan Chase recently applied to trademark a product called “IndexGPT” that offers investment advice to customers.5 Wells Fargo is using LLMs to help determine what information clients must report to regulators and how they can improve their business processes.6

When Federal Reserve researchers evaluated GPT models’ ability to “decipher Fedspeak” (i.e., classify Federal Open Market Committee announcements as dovish or hawkish), they found that the algorithms not only were superior to other methods but also demonstrated reasoning abilities on par with humans.7 Several institutions are already using similar GPT models to analyze official statements and speeches produced by central banks.

Vendors to investment banks have also increased their investments in the new technology. Bloomberg recently launched “Bloomberg GPT,” a large language model built on 50 billion parameters and tailored for finance.8 Similarly, Pitchbook has a new tool called “VC Exit Predictor” that uses a machine learning algorithm to predict a startup’s potential growth prospects.9

How generative AI can help investment banking front-office operations

Generative AI should be especially fruitful in areas where the output generation effort is high and validation is relatively easy.10 In the investment banking context, this capability can enable front-office employees to do their jobs better across a spectrum of activities, including marketing, sales, decision support, research, and trading, thereby boosting productivity. Professionals in these areas spend an enormous amount of time creating pitch books, industry reports, investment theses, performance summaries, due diligence reports, etc. Generative AI can help reduce the cost of content creation, enhance analytical capabilities, improve the electronification processes, and even reduce client call transfer rates.

Investment banks such as Goldman Sachs are also leveraging generative AI to help developers and coders create robust code more efficiently.11 Such competence is only expected to improve as these LLMs are trained on more parameters.

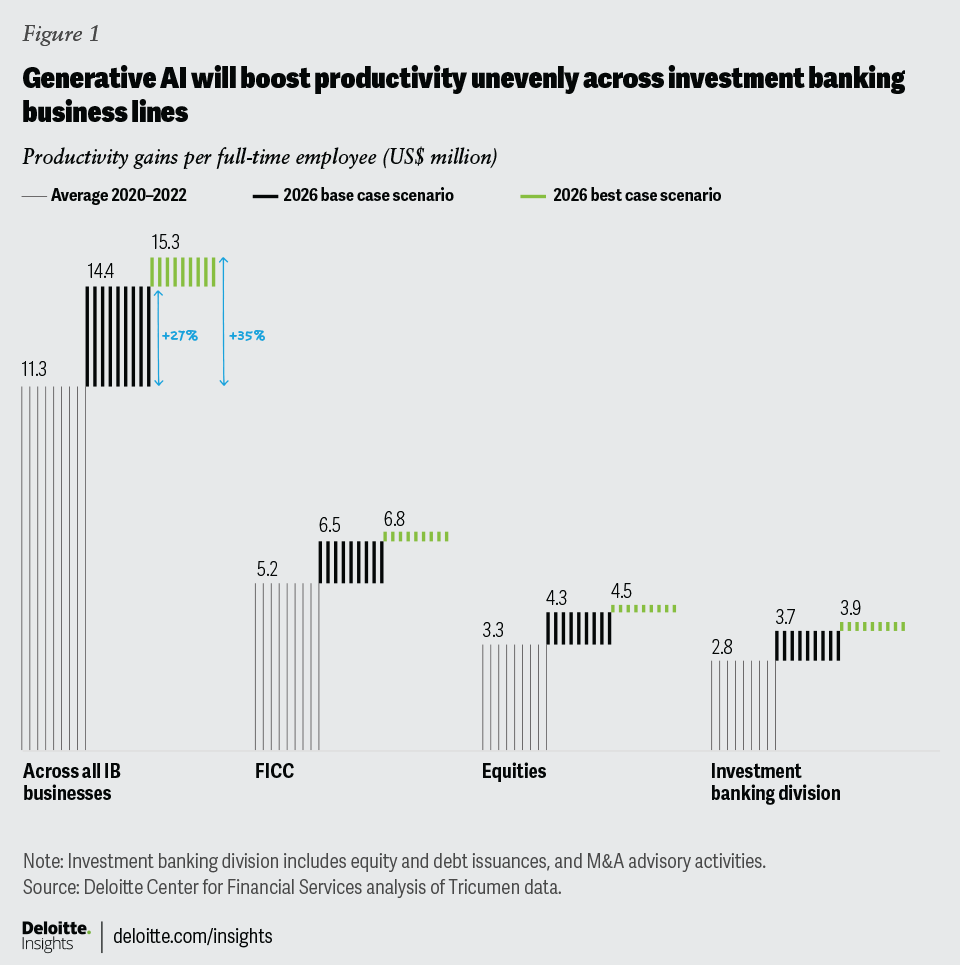

Our analysis suggests that the use of generative AI can boost productivity for front-office employees by as much as 27%–35% by 2026, after adjusting for inflation.12 This translates to an additional revenue of US$3 million to US$4 million per employee from an average of $11.3 million during 2020–22 (figure 1).

{kind=link}

Productivity gains will likely vary by the inherent complexities of the underlying business. We estimate that gains will be the highest for the investment banking division (IBD), followed by equities, and then by FICC (fixed income, currencies, and commodities) trading.

The IBD, which includes equities and debt issuance, mergers and acquisition, and advisory, may benefit the most from generative AI, as it involves more repetitive tasks: We estimate that IBD productivity can be improved by an average of 34%. The technology can help generate initial deal structures and conduct due diligence, compliance, and valuation. In the areas of underwriting and issuance, generative AI can help with prospectus and term-sheet drafting and legal documentation.

Generative AI may also have a profound impact on trading. Automation and low-latency trading infrastructure have already morphed trading dramatically, possibly leading to greater market efficiencies, and reduced transaction costs.13 Traders leverage NLP and sentiment analysis to analyze markets, generate synthetic data for risk modeling, and optimize trading strategies. We estimate generative AI’s impact on such activities could significantly reduce time to understand market sentiment, catch anomalies, and place orders more easily and at greater scale.

In equities trading, generative AI can help traders quickly analyze, summarize company and industry fundamentals, run valuation models, conduct backtest trading strategies, and offer personalized trading recommendations to both institutional and retail clients.

FICC trading, on the other hand, often demands complex analysis and valuation, since it may also involve swaps/derivatives and a diverse array of trading strategies and risk parameters. Additionally, FICC markets tend to embody more systemic risk, so there is typically more regulatory scrutiny. While this offers space for generative AI to monitor bond yields, assess credit ratings, and provide real-time insights, the market-related uncertainty and volatility would require continuous validation from seasoned experts. These unique features may dampen productivity gains from generative AI, compared with equities trading.

Generative AI may create new risks and alter competitive dynamics

The infusion of generative AI into the investment banking value chain will most likely come with potential legal, reputational, and other operational risks. It may also alter the dynamics with buy-side clients; as they also embrace this technology, the outputs they are able to generate with greater efficiencies may reduce dependency on the sell-side. Some clients may want to independently develop their own value streams and turn to banks only for the most high-value-adding services. Additionally, productivity gains could level the playing field by reducing barriers to entry, and further intensifying competition. But as investments needed to develop these LLMs become more substantial, this technology may also widen the gap among market participants and may put the smaller, boutique firms at a disadvantage.

How can investment banking leaders help prepare their firms for generative AI adoption

Here are some key considerations investment banking leaders should explore when implementing generative AI into front-office functions:

- Determining focus and scale. The benefits of LLMs may not be uniform. In addition to the vaunted gains, leaders should consider the potential ease of execution and the associated risks.

- Leveraging productivity gains. As initial use cases become real, banks will likely have to realign their workforce to more purpose-driven tasks. Reducing mundane activities could help enable new talent, such as junior traders, to scale up faster and develop more valuable proficiencies.

- Assessing, mitigating, and managing risks. Generative AI’s outputs could require constant validation for hallucination (i.e., fabrication of confident responses that cannot be grounded in real-world data), accuracy, and biases. Banks may need to redesign their existing risk frameworks, risk governance, and, more generally, prepare for a more dynamic risk management.14

- Bolstering stakeholder trust. Ensuring the credibility of the outputs and convincing employees, clients, partners, and regulators of their validity may be key in scaling generative AI applications. Aligning stakeholder interests and ensuring that ethical and responsible AI practices are adhered to will be paramount.

- Integrating generative AI with existing systems, applications, tools, and technologies. Leaders should consider how these AI tools will fit within the broader context of digital transformation, cloud migration, and data and analytics strategy and operations. Generative AI should be integrated with existing AI and digital infrastructure. Leaders should keep an eye on how other emerging technologies, such as quantum computing, can add to the multiplicative power. Sharing hardware resources and computational and server loads across various technologies and applications will be another challenge.15

- Monitoring advancements to gain a competitive edge. Generative AI should spur greater innovation and creativity. As LLMs become ubiquitous, though, using generative AI to gain a competitive edge in areas such as cost management may diminish.

- Interacting with regulators. Regulators will likely provide new guidelines for the application of generative AI for data privacy, copyrights, and intellectual property issues. Investment banks should be careful about how they use client and market data and institute new compliance processes. Banks should proactively engage with regulators on these matters and shape new policies for everyone’s benefit.

- Partnering on implementation. Fintechs and technology organizations have proved to be effective partners for investment banks in the past. Generative AI will likely require both horizontal and vertical partnerships. Large banks may have to ponder the age-old build vs. buy decision. Smaller institutions may be at a disadvantage in establishing partnerships; they may need to design new partnership models.

BY

Sriram Gopalakrishnan

Abhinav Chauhan

Val Srinivas

The authors would like to thank the following Deloitte Center for Financial Services colleagues for their extensive contributions and support: Jim Eckenrode, Patricia Danielecki, Samia Hazuria, Karen Edelman, and Paul Kaiser.

Cover image by: Natalie Pfaff