Housing market shifts could reshape rental operating models for commercial real estate owners

A surge in US renter households by 2035 could create opportunities for property owners who invest early in living-as-a-service offerings across their portfolios

The population of renters in the United States is expected to increase over the next decade amid challenges to home ownership and other emerging trends. For commercial real estate owners of multifamily rental properties, the expected rise in renters may open new pathways to capture excess value from subscription-based, living-as-a-service operating platforms.

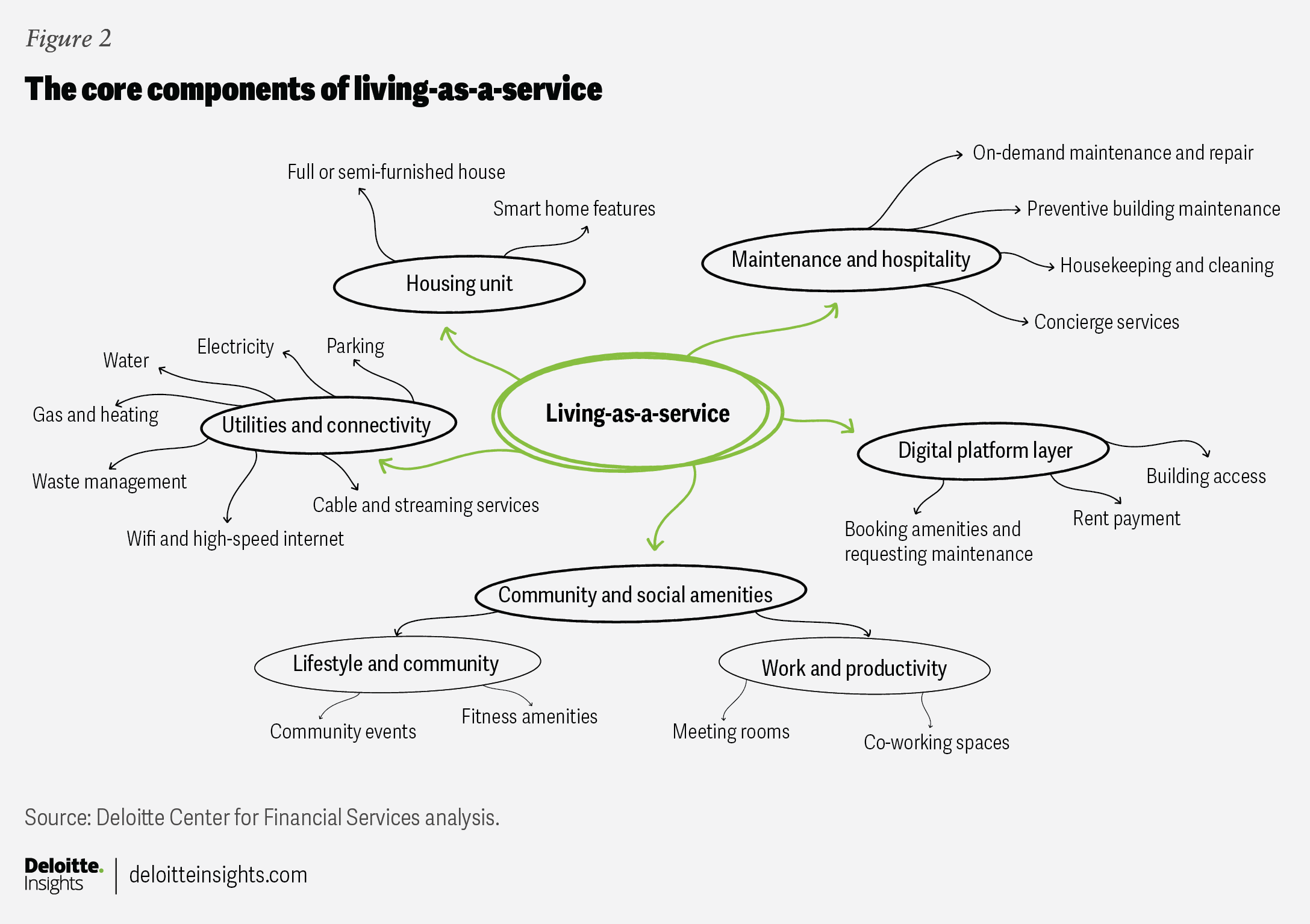

The living-as-a-service model (LaaS) repositions rental housing as an integrated service experience between buildings and even metros. Instead of focusing solely on lease terms for single-cycle occupancy, it emphasizes flexibility, mobility, and access through a subscription service. By bundling a range of value-added services, such as maintenance, connectivity, and amenities, among others, for lease options across a portfolio, owners can potentially ease the burdens of tenant responsibility, capturing the loyalty of renters to a single platform for the long term.

This subscription-style approach could also allow renters to adapt their living arrangements more easily as their needs evolve, while benefiting from a more seamless and supported residential experience for their current rental units and future ones. Such platforms may be particularly attractive to households that prioritize convenience and housing-related services over long-term ownership commitments.

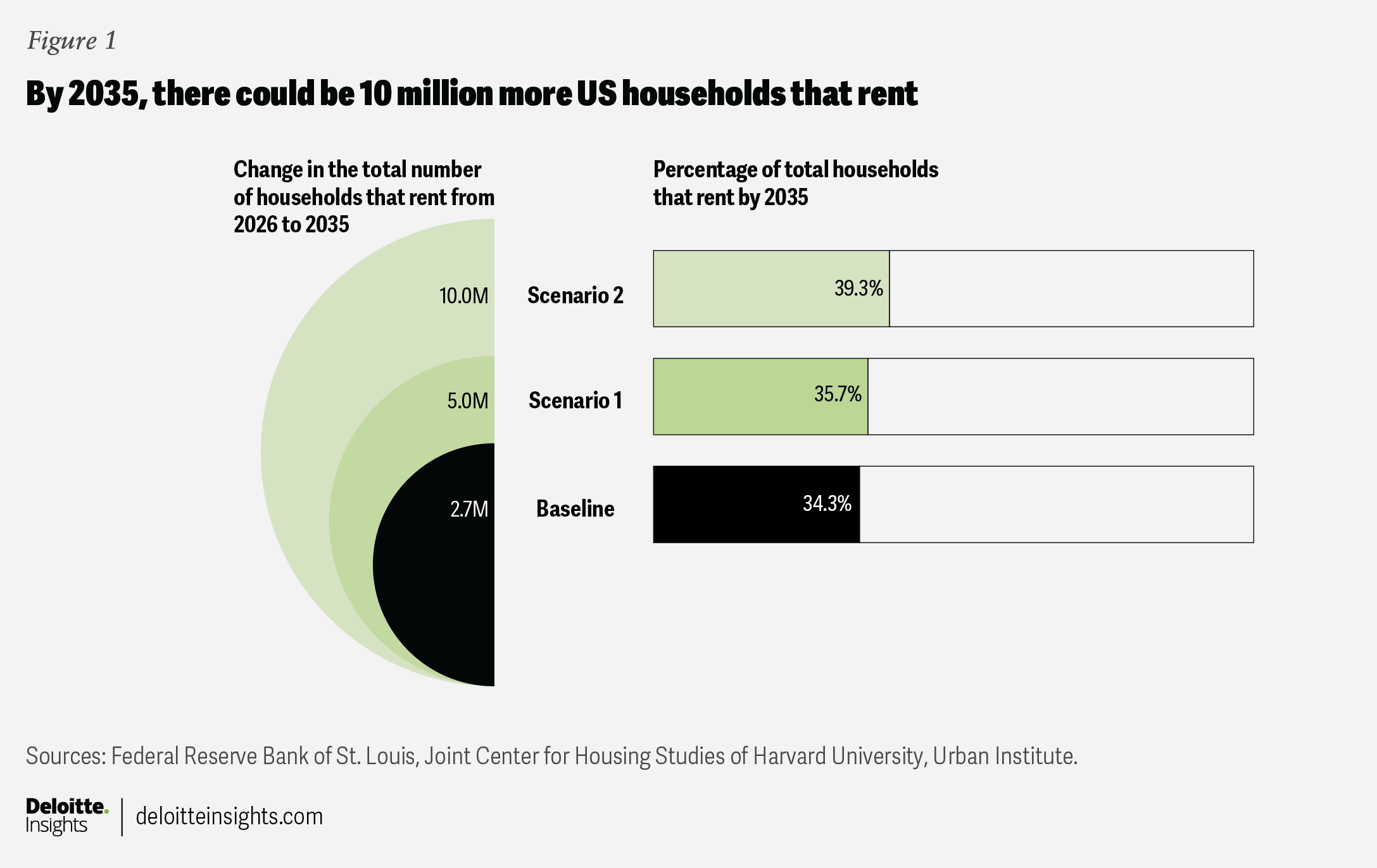

Ongoing demographic shifts, along with renewed homeownership challenges, are expected to broaden the appeal of house and apartment renting over the coming decade. The Deloitte Center for Financial Services analyzed three possible scenarios for the future number of renters in the United States. The first is derived from Deloitte’s first-quarter economic forecast. The second and third are based on forecasts for 2035 by industry housing and research organizations, modeled using Deloitte’s own estimations and assumptions. Based on these findings, we predict the number of US households that rent could increase by as much as 21.7% by 2035 to 56.3 million from today’s 46.2 million. The same research finds the percentage of households that rent could reach 39.3% by 2035, up from 34.3% today (figure 1) (see “About this prediction”).

How homeownership pressures could fuel rental growth

Pricing compression. Steadily rising home prices in many regions of the United States are widely seen as a main factor suppressing near-term buying growth. Prices have outpaced income growth, raising income thresholds needed for home purchases.1 Elevated levels of upfront capital are needed to meet downpayments, especially in competitive markets.2 Rising homeownership operating costs, including property insurance and taxes, are also putting pressure on household budgets.3 In terms of financing, mortgage rates remain elevated relative to the exceptionally low levels that defined much of the past decade. While 30-year fixed-rate mortgages dipped briefly below 6% in the first quarter of this year—nearing their lowest level since 2022—they remain double the rates that were available in the 2010s.4

Demographic friction. Consumer trends and preferences are also shaping the housing market. The time it takes to transition from renting to owning is lengthening, and those seeking flexibility, either geographically or due to family or life circumstances, may opt to own for shorter periods than in the past. The median age of first-time home buyers is now 40 years old, up from the late 20s in the 1980s, as households delay purchasing due to financial limitations.5 At the other end, those entering retirement are choosing to downsize or move into rental housing that requires less maintenance and offers more conveniences.6 Changing lifestyle preferences may also be influencing tenure decisions. These can include geographic flexibility for evolving career paths and remote work opportunities, making long-term ownership less appealing to some.

Marketplace dynamics. In many regions, new for-sale housing construction has not kept pace with population growth and household formation, limiting available inventory and putting upward pressure on prices. The trend has been exacerbated in recent years by rising construction costs.7

What a renter-centric future could mean for housing

Rental housing could move from being transitional to becoming a core household infrastructure as the composition of the renter base evolves. A notable shift came from renters ages 65 and older, whose share of rentals increased by nearly 30% between 2013 and 2023 as more retirees chose renting to reduce maintenance and property tax burdens,8 while allowing closer proximity to family or health care.9

The number of high-net-worth renter households in the United States more than tripled between 2019 and 2023,10 suggesting that renting is increasingly viewed as both a lifestyle and a capital preservation choice among higher-income households. Renters are also stretching leasing periods, with renewals accounting for about 57% of leasing activity, an indication of high tenant retention.11 Large operators reported record-low turnover rates, as low as 7.9% in early 2025.12

Some property owners are taking action to accommodate these changing expectations. Several real estate investment trusts are prioritizing occupancy stability in slower leasing periods to sustain revenue and net operating income.13 Retention has become financially critical, with turnover costing about US$4,000 per unit, a figure that includes vacancy loss, concessions, and unit make-ready costs.14

The strategic opportunity of LaaS

In a scenario where the number of new renter households swells by as much as 10 million in the next decade, owners of multifamily rentals have a strategic opportunity. Those that consider a LaaS operating model could have early-mover advantages as the rental housing market evolves. The goal is to provide a simplified, predictable, and flexible housing experience for renters for the duration of their renting experience, wherever they choose to live (figure 2).

For commercial real estate owners and investors, the LaaS model can offer several strategic advantages for both their tenants and their businesses. Replacing traditional leases with flexible, service-oriented plans could appeal to renters who value mobility. A multi-metro model, for example, could allow tenants to move seamlessly between units within a rental portfolio network—catering to the needs of remote workers as well as gig economy and work-at-home professionals.

This shift toward service-oriented living is already visible in other living segments, like senior housing, of which investors are taking notice. The oversubscription to public offerings such as the Janus Living IPO may signal growing demand for integrated services, lifestyle amenities, and convenience-driven experiences15—highlighting how expectations are evolving beyond simply securing a place to live.

For building owners, LaaS models can benefit from scale. Large multifamily operators could be well-positioned to aggregate services such as utilities, maintenance contracts, and technology platforms across multiple properties and cities in their portfolio. Centralizing these functions could lower per-unit operating costs while enabling consistent service delivery.

Lastly, LaaS introduces potential new revenue streams beyond base rent. Operators could capture additional income through bundled service premiums, optional add-on services, and partnerships with third-party providers. Even a modest adoption of bundled services across a large portfolio could generate meaningful revenue increases and consistent income streams while strengthening resident retention and satisfaction. This approach could help rental unit owners transition from traditional rent collection to a more diversified, service-oriented operating platform.

Next steps toward adopting the LaaS model

Rental owners and investors looking to adopt LaaS can consider the following steps.

- Reposition portfolio strategy toward platform integration. Technology will be the enabler, getting LaaS off the ground and implemented at scale. Owners should invest in operating systems that can enable bundled billing, marketing available units across a portfolio, and standardized service layers across properties.

- Target properties aligned with structural rental growth. These include multifamily properties in high home-price-to-income metros; build-to-rent or master plan communities where rental homes are highly concentrated; and markets with strong household formation but limited housing inventory.

- Implement clear, itemized lease terms and billing that transparently break out all services included in any bundled offering. Provide tenants with visibility into costs, optional add-ons, and usage-based charges. Establish consistent communication and auditing practices to build trust, avoid perceptions of hidden fees, and reinforce the value proposition of a service-oriented rental model.

- Start building service capabilities. LaaS will require an established network of partnerships that enables the model to run efficiently. At the onset of adoption, owners should aggregate utility providers, scale maintenance capabilities, leverage bulk pricing for furniture acquisition, and establish a subscription-ready billing infrastructure.

- Implement resident analytics platforms and tenancy life cycle tracking. Deploy property management platforms that can capture tenant satisfaction, service requests, and amenity usage, as well as financial metrics, including renewal rates and turnover. Monitor how service usage and satisfaction correlate with retention to help refine bundled offerings, address points of friction, and potentially reduce churn.

Building a bundled offering like LaaS takes deep coordination and planning on the part of rental property owners. Those that start preparing early for the technical, analytical, and partnering requirements have an opportunity to establish new in-demand business channels for an expanding rental marketplace.

About this prediction

At the end of 2025, 46.2 million households identified that they live in rental housing, or 34.3% of all households.16 Using the recent pace of household formation of approximately 859,000 new households per year, we estimate there will be 143.4 million households by 2035. This total household count forecast was then used as the final 2035 estimate across scenarios one and two.

Our scenario details and forecast assumptions are as follows.

Baseline: The Deloitte US economic forecast and straight-line assumption

In the base case, we assume that today’s homeownership rate of 65.7% will not change by 2035. We leverage Deloitte’s latest US economic forecast for homeownership growth, but the distribution of new renters is no larger or smaller than what it is today.

Scenario one: Pressures persist, but the system works

In this scenario, we base estimates on the forecasted rate of 64.3% homeownership by the Joint Center for Housing Studies at Harvard University.17 Using our final household forecast, that would mean roughly 51.2 million households would be renters by 2035, a 5 million increase from today’s total or a 10.6% increase.

Deloitte assumptions applied to reach this total:

- Of the new households formed over time, 60% become renters.

- Owner-to-renter conversions are negligible, as we assume current owners would choose to remain owners rather than give up equity, retain their lower-than-market mortgage payments, or potentially aim to pass their properties on to their families.

- In this scenario, prices and rates remain elevated, down payment hurdles are still in place, but there is no major foreclosure wave or credit crisis.

Scenario two: Tough affordability, tight credit, and owner conversions

For the second scenario, the forecasted homeownership rate settles at 60.8% by 2035 as estimated by the Urban Institute.18 By 2035, this would equate to 56.3 million households, a 10 million or 21.7% increase from 2025.

Deloitte assumptions applied to reach this total:

- Nearly 90% of the new households formed over this period become renters.

- There is an incremental conversion of owners to renters, forced by life circumstances to rent, including downsizing trends, divorce, and retirees shifting to rentals.

- Rates and home prices also stay higher for longer, enough so that first-time home buying remains muted.

- There is an increase in government incentives for developers to build in the interest of renters, more often with products like build-to-rent or LaaS.

The authors wish to acknowledge John Quigley, Brian Ruben, and Gaurashi Sawant for their extensive contributions to the development of this report.

They would also like to thank Akrur Barua, Parul Bhargava, Ankit Narechania, Kirby Rattenbury, and Rohini Sanyal for their insights and guidance.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover artist: Sofia Laviano

Knowledge services: Vanapalli Viswa Teja