The agentic AI productivity wave is heading for wealth management

Agentic AI capabilities could help firms lower cost-to-serve, enhance advice quality and delivery, improve adviser and client experience, and drive competitive differentiation

Wealth management firms are caught in a workload bind: Clients want advice that’s always on and frictionless, while advisers are busy managing larger, more complex books. Advisers spend nearly 70% of their time on behind-the-scenes work, leaving just 30% for where they add the most value—building client relationships.1

Artificial intelligence, especially agentic execution, has the potential to flip that equation. The Deloitte Center for Financial Services predicts that adviser productivity uplift—defined as the increase in adviser capacity achieved through AI-driven time savings within existing work hours—could reach roughly 30% to 100% by 2032. At an industry level, that implies that between 25% and 50% of adviser time could be freed from lower-value operational work, adding meaningful capacity back into the system—and potentially shifting the issue from adviser scarcity to adviser capability.

In terms of assets under management (AUM), that uplift could expand industry capacity by the equivalent of US$10 trillion to US$35 trillion in additional client assets. At typical advisory fees of 1% of AUM, this productivity uplift translates to between US$100 billion and US$350 billion in potential annual revenue (see “About this prediction”). But realizing that value depends on how firms redeploy freed capacity—toward client acquisition, deeper service, or operational efficiency—and on the level of autonomy regulators ultimately permit.

Evolving AI technology is already showing signs that it can help advisers in meaningful ways to minimize many important but repetitive manual duties. But the gains will not be uniform. How much value firms capture from AI may depend on three levers: the adviser’s own propensity to adopt AI, the wealth firm’s willingness to redesign processes and controls around it, and whether the underlying tech stack is AI-ready. Of the three, the tech stack may be the biggest swing factor: even motivated advisers and supportive firms will struggle to scale AI if data is fragmented and systems are hard to integrate.

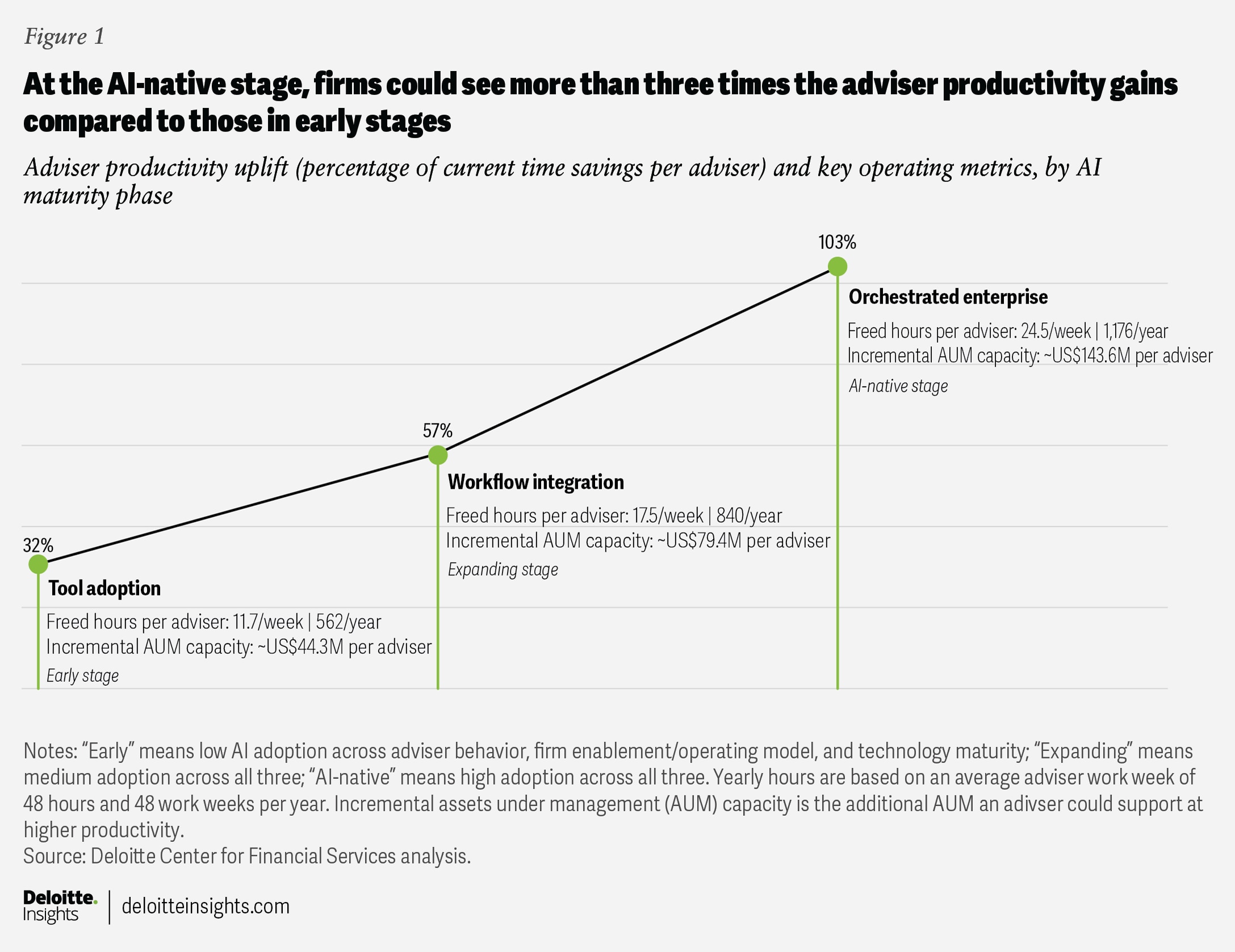

We analyzed adviser capacity uplift in three stages. In the early stage, where all three levers lag, AI is used mainly as an assistive tool, and advisers typically see modest productivity gains of roughly 32% (figure 1). As firms move into the expanding stage, where copilots are embedded in workflows and governance frameworks allow bounded delegation, productivity uplift rises to about 57%.

Recent use cases illustrate this transition. Morgan Stanley’s AI Debrief, for example, automatically summarizes meetings, generates follow-ups, and logs notes into the customer relationship management system, reducing manual documentation and freeing advisers to spend more time on client conversations rather than administrative tasks.2

Productivity gains are highest in the AI-native stage—at roughly 103% uplift—when all three levers reach high maturity and automation can run multistep, end-to-end workflows. In this environment, advisers increasingly operate with a team of digital agents, supervising AI systems that handle preparation, monitoring, and routine servicing. Emerging platforms such as Altruist’s Hazel AI—which can analyze tax returns and portfolio data to generate tax-planning insights and scenarios in seconds—illustrate how AI can handle complex analytical tasks that previously required hours of manual work.3

In practice, most firms will progress through some combination of low, medium, and high AI adoption and tech maturity across those three levers (see “The AI adoption matrix: Three levers of success”). When the levers are misaligned, value capture is typically capped by the weakest one; where they advance together, productivity gains can accelerate and reinforce one another. For example, tool access alone rarely delivers full value. The real lift comes when firms redesign workflows and governance around these tools and build an AI-ready data foundation.

We’re not there yet. Many wealth firms are just starting to scale pilots, and few have redesigned day-to-day workflows. Industry estimates suggest that while 73% of advisory firms use AI in some capacity, only 6% use agentic tools and 5% have implemented cross-system AI integration.4

The AI adoption matrix: Three levers of success

Adviser behavior

At low adoption, advisers receive limited training and use AI for basic tasks such as drafting reports and summarizing research, with manual review required. At medium adoption, copilots are embedded in daily workflows, with human-in-the-loop oversight. At high adoption, advisers receive continuous training and apply AI across the most complex workflows.

Firm enablement

At low adoption, AI rollout is often a patchwork, with compliance constraints blocking key capabilities. At medium adoption, firms standardize tools, build playbooks and training, expand compliance support, and implement governance so adoption can scale. At high adoption, firms redesign the operating model around AI, creating infrastructure for larger team-based practices and tying incentives to outcomes: more capacity means more client coverage and higher client satisfaction scores.

Technology stack

At low adoption, siloed systems constrain firms to simpler use cases with many manual steps. At medium adoption, the adviser workstation and core systems are integrated on a unified data layer with stabilized application programming interfaces, and enterprise search and workflow orchestration become reliable for key journeys. At high adoption, the stack becomes event-driven and end-to-end orchestrated through real-time data fabric and policy-as-code, enabling safer agent autonomy.

What greater adviser productivity can mean for clients, advisers, and firms

At an industry level, agentic AI will do more than improve efficiency; it will likely reshape how advice is created, packaged, and delivered.

For clients, the bar should rise quickly. Faster responses, more tailored insights, and more proactive outreach should become minimum standards. This shift presents a real opportunity to address one of wealth management’s most persistent challenges: client experience. Advisers will still be the face of the firm, so the differentiators will be trust, transparency, and accountability, especially as AI shows up in the service experience.

For advisers, the work shifts up the value chain. Less time is spent on operational tasks, while more time is devoted to higher-value conversations and judgment-heavy moments. But working with a digital agent team also changes the adviser’s required skill set; advisers will need to supervise outputs, validate assumptions, manage exceptions, and communicate AI-assisted recommendations in a clear, defensible way within governance controls. Over time, the model may shift away from individual effort toward apprenticeship, specialization, and technology leverage—driving more teaming, greater practice consolidation, and a higher premium on leaders who can mentor, develop clients, and scale larger teams.

Agentic AI can help firms extend high-touch planning to a broader client base. By reducing manual processes involved in tax, legal, and insurance-related workflows, firms can serve less complex clients more economically while still delivering personalized advice. Better orchestration also allows systems to track deadlines, needs, and opportunities continuously, while bringing in the human adviser when judgment or a client conversation is needed.

The capacity gains from agentic AI can also become a growth lever. In practice, that means using freed-up adviser and support capacity to deepen relationships, cover more households, extend service to new segments, and improve operating leverage through more automated end-to-end processing. Done well, this can help firms protect existing AUM through better service while creating more capacity for acquisitions, cross-selling, and wallet-share growth.

Margin expansion for some, pressure for others. Lower cost-to-serve can expand margins for firms that execute and maintain pricing. At the same time, competitive pressure may compress fees as planning outputs become easier to compare. Firms with strong distribution, disciplined governance, and effective orchestration will likely scale profitably.

Three considerations for scaling agentic AI in wealth management

To help make agentic AI core to their operating infrastructure—ensuring data and workflows connect cleanly across front-, middle-, and back-office systems—firms can take the following actions:

1) Start with low-risk, end-to-end internal workflows, not isolated use cases

Deploy agentic AI first where risk is lower, data is more readily available, and workflows are not overly constrained by fragmented systems. Internal processes such as onboarding, service requests, customer relationship management follow-up, and policy support are strong early candidates, allowing agents to handle end-to-end execution while humans retain oversight and judgment.

Put guardrails around scope, require explicit approvals for consequential actions, and maintain full audit trails. Raymond James’ internal operations agent, Rai, is a good example. Rai was initially launched for select business units, with explicit human-in-the-loop oversight rather than open-ended autonomy.5

2) Ensure the right content, controls, and testing are in place before scaling

Scaling often stalls on fundamentals: fragmented content, unclear access rights, and weak testing. Establish a permissioned, trusted source for operational data, enforce role-based access, and institutionalize use-case-specific evaluations supported by regression testing and logging.

Build in compliance and supervision from the start, such as an approved use-case inventory, vendor due diligence, required recordkeeping, and disciplined external claims about AI. Morgan Stanley’s rollout illustrates this pattern: expert review, improved retrieval, and frequent testing before expanding to more use cases.6

3) Develop an enterprise operating model and clear business metrics

AI adoption is often highest when it is built into the tools and workflows advisers already use, not offered as a standalone tool. To scale effectively, firms should consider setting up a center of excellence that brings together business, platform, compliance, risk, data, cybersecurity, and architecture teams.

Further, as the adviser role evolves, firms may also need to build new capabilities—analytical fluency, comfort with AI governance, effective exception management, and the ability to adopt new tools and mentor junior advisers to do the same. Success should be measured with clear operational metrics, such as adviser time saved, fewer service exceptions, faster post-meeting follow-up, and greater client capacity per adviser.

Against the backdrop of a US$124 trillion generational wealth transfer and a widening adviser shortage, wealth management stands at an inflection point.7 AI is no longer just a productivity tool—it can be a source of competitive differentiation. Those that succeed may be the firms that use it to create a fundamentally simpler adviser experience, unlock hyper-personalization at scale, and help their advisers grow faster than anyone else in the industry.

But technology alone won’t decide the race. The biggest gains will likely go to firms with the transformational DNA to reimagine workflows, scale change across the enterprise, and turn innovation into measurable performance. These firms already stand apart: they’re tripling their peers’ compound annual revenue growth rate, growing AUM four times faster, and delivering nearly 30% operating margins versus 22% for the rest.8

In the AI-native era, the question isn’t whether to adopt AI—it’s whether firms are willing to redesign the business around it. The firms that do so will likely define the next generation of wealth management.

About this prediction

This prediction estimates how AI could boost adviser productivity and AUM capacity. We start with baseline time allocation across tasks, apply time-reduction assumptions for AI tools (copilot and agentic systems), and adjust for realistic adoption rates based on adviser behavior, firm support, and tech stack maturity. Time savings convert to productivity gains and additional AUM capacity. AUM capacity reflects serviceable headroom rather than actual AUM captured, with outcomes dependent on how firms deploy freed capacity and on external market dynamics. The analysis is based on Cerulli Associates’ adviser time allocation data.

by

Jeffrey A. Levi

Samia Hazuria

The authors, Jeff Levi and Samia Hazuria, would like to thank executive sponsor Puneet Kakar for his support.

They also extend sincere appreciation to the Deloitte subject matter leaders who contributed to the research for this chapter: Snehal Waghulde, Tom Kirk, Steve Hillas, Karl Ersham, Josh Uhl, and Steve Corman.

Additionally, the authors would like to acknowledge and thank the Deloitte Insights, marketing excellence, and public relations teams.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover image by: Sofia Laviano

Knowledge services: Rishitha Bichapogu