Beyond cost cutting: Considerations for redefining financial agility in engineering and construction

Amid rising costs and tighter capital, US engineering and construction firms are focusing on four financial strategies to enhance resilience and flexibility

As US engineering and construction firms navigate rising costs and structurally thin margins, financial discipline has increasingly become a leadership priority. Traditional cost cutting and reactive financial management may no longer be enough to protect margins and maintain investment flexibility amid persistent inflation, interest rate volatility, and supply chain disruptions. As a result, some firms are tightening their focus on sustaining liquidity, strengthening balance sheets, and improving the quality and timing of cash flows.

This shift signals a move from cost containment toward capital optimization and balance sheet optionality.1 Some leaders appear to be taking a more deliberate, forward-looking approach to internal levers such as planning cadence, investment choices, capital allocation, and portfolio actions, while continuing to navigate external pressures from regulations, tariffs, and supply chain volatility.2

Project pipelines are also evolving beyond traditional segments toward data centers, energy generation facilities, and advanced manufacturing, reshaping capital needs and resource priorities.3 Strategic agility will increasingly depend on how effectively firms convert disciplined financial management into faster decisions, greater operational flexibility, and resilience across cycles.

To better understand how executives are evaluating financial priorities, risks, and capital decisions, Deloitte analyzed earnings call transcripts of around 20 publicly listed US engineering and construction (E&C) companies from Q4 2024 to Q3 2025. By examining how executives discuss financial priorities, risks, and capital decisions, we identified four strategies that firms are using—or could adopt—to help cushion against ongoing uncertainty and strengthen financial resilience.

Four strategies for financial agility and resilience

As the industry undergoes a shift toward strategic, scenario-based planning and risk management, the E&C companies whose earnings calls were analyzed are focusing on four areas or segments to build resilience.

1. Cost and capital efficiency driven by technology

Amid sustained material and labor cost pressures and tighter financing conditions, US E&C firms are sharpening their focus on cost and capital efficiency to drive productivity. A 2025 Autodesk study shows that cost control and management rank ahead of technology and AI adoption as the top concern among US architecture, engineering, and construction firms.4

To help address cost leakage and capital inefficiency, some organizations are investing in technology and process improvements. The Autodesk study highlights that digitally mature companies are more optimistic about their financial performance, underscoring that digital investments are increasingly justified by measurable financial outcomes rather than transformation alone.5 Automation of finance and accounting functions, improved job-cost visibility, and digitally enabled procurement can help firms reduce overhead, improve forecast accuracy, and manage tariff- and supply-driven cost shocks.

Beyond technology, firms are also exploring scenario planning, control towers, and command centers that continuously re-forecast project and portfolio outcomes as external conditions change, strengthening resilience. Additionally, predictive finance models and rolling forecasts, increasingly complemented by design-to-cost frameworks, can enable tighter alignment between design decisions, delivery strategy, and margin protection.6

Procurement is also shifting from reactive, project-by-project buying to longer-horizon strategic sourcing and contract-linked risk management to reduce input-cost exposure.7 This includes managing tariff impacts and supply volatility through supplier diversification and more resilient contracting.8

Some firms are embedding these “no-regrets” investments in digital capabilities and delivery capacity into capital planning.9 These moves, particularly those that shorten cycle times and improve visibility from field to finance, can collectively help to sustain cost discipline, stabilize working capital needs, improve enterprise productivity, and enable efficient capital allocation.

Why it matters

With margins increasingly exposed to volatility across labor, commodities, and funding markets, many firms are shifting their focus from periodic cost cutting to more systematic, data-driven cost and cash management across the project and portfolio life cycle. These capabilities can allow leaders to respond more quickly to disruptions, turning ambiguity into a managed variable rather than a surprise.

2. Liquidity and balance sheet strength

Liquidity and balance sheet strength are expected to continue to elevate as core elements of financial strategy, particularly as interest rate volatility and project complexity persist. Borrowing costs remain structurally higher than before 2022,10 and lenders are applying tighter underwriting standards.11 In response, some contractors and developers are tightening leverage targets, prioritizing debt reduction, and actively managing maturity profiles to reduce sensitivity to rate movements and enhance financial resilience. This has contributed to conservative balance sheet targets, accelerated debt paydown, and a stronger emphasis on staggered maturities to reduce refinancing risk and exposure to rate swings.12

Maintaining liquidity is becoming equally important. Healthy cash reserves, committed credit facilities, and flexible capital structures can allow firms to absorb near-term disruptions, such as delayed owner payments, supply chain interruptions, or regulatory changes, while continuing to fund strategic investments. In cases where federal or state co-funding is available, some developers are opting for lower leverage to help protect balance sheet flexibility, maintain borrowing capacity, and retain optionality for higher-priority projects or opportunistic growth.13

Balance sheet strength becomes particularly important in high-growth, capital-intensive segments such as data center development and advanced manufacturing facilities.14 These projects often require substantial upfront investment, long procurement timelines, and access to scarce specialist labor, creating extended cash conversion cycles.15 Firms with robust liquidity and disciplined balance sheets are better positioned to self-fund early-stage costs, manage working-capital swings, and selectively pursue large, multiyear programs, making financial strength a differentiator in the US E&C landscape.

Why it matters

In the transcripts of companies we analyzed, corporate disclosures increasingly frame liquidity not merely as a defensive buffer, but also as a strategic growth enabler, with commentary from chief financial officers emphasizing capital structure optionality and balance sheet headroom as sources of competitive advantage.16 Some firms appear to increasingly recognize that strong liquidity supports faster decision-making, improved negotiating power with lenders and suppliers, and the ability to scale or pause investments as market conditions evolve.

3. Risk, tax, and legislation agility

Deloitte analysis of E&C firms’ earnings calls indicates that they are focusing on risk management, tax optimization, and legislative agility amid macroeconomic uncertainty, policy shifts, and market volatility. These changes are also necessitating more adaptive financial strategies across the project life cycle.

Some firms are moving away from traditionally rigid fixed-price contracts toward hybrid and collaborative delivery models that emphasize shared risk and transparency.17 Contract structures such as cost-plus, guaranteed maximum price, and alliance-based models are gaining traction, particularly for complex, capital-intensive projects.18 These approaches are often paired with advanced procurement strategies, such as early contractor involvement, bulk purchasing, and supplier prequalification, to help reduce exposure to material price volatility, supply chain disruption, and schedule risk.19

Digital enablement is likely to play a growing role in strengthening risk resilience. Advanced analytics, integrated project controls, and real-time cost and schedule monitoring tools can enable firms to identify emerging risks earlier, model mitigation scenarios, and make faster course corrections.

Owners and contractors, particularly in fast-growing segments such as data centers, advanced manufacturing, and energy infrastructure, are adopting standardized and repeatable delivery models to improve certainty.20 For example, data center owners may rely on multiyear framework agreements, preferred supplier ecosystems, and standardized modular designs21 to help limit cost overruns and accelerate project payback. These approaches can reduce design variability, shorten construction timelines, and improve capital efficiency, ultimately lowering execution risk.

Recent legislative incentives under the One Big Beautiful Bill Act22 can offer opportunities through provisions including bonus depreciation, immediate research and development expensing, increased business interest deductibility, and targeted incentives tied to domestic manufacturing, energy transition, and infrastructure development.

Some E&C firms are increasingly integrating tax strategy directly into capital planning and project selection decisions.23 By aligning investment timing, entity structures, and delivery models with available incentives, companies can improve after-tax returns and strengthen the business case for large-scale projects.

Contract terms are also being updated to include escalation clauses, index-based pricing, and tariff pass-through provisions are becoming more common, helping firms to reduce exposure to trade policy changes, tariffs, and supply chain shocks.24

Why it matters

Risk management is increasingly shifting toward predictive, data-driven capability embedded within core operations. Organizations that actively monitor policy developments and rapidly adjust commercial, tax, and operational strategies could be well-positioned to protect margins and capture growth opportunities.

4. Strategic mergers and acquisitions

Recent mergers and acquisitions activity in the E&C sector reflects a shift in how, rather than pursuing growth alone, some transactions appear to be increasingly focused on improving delivery reliability, cash flow visibility, and balance sheet flexibility.

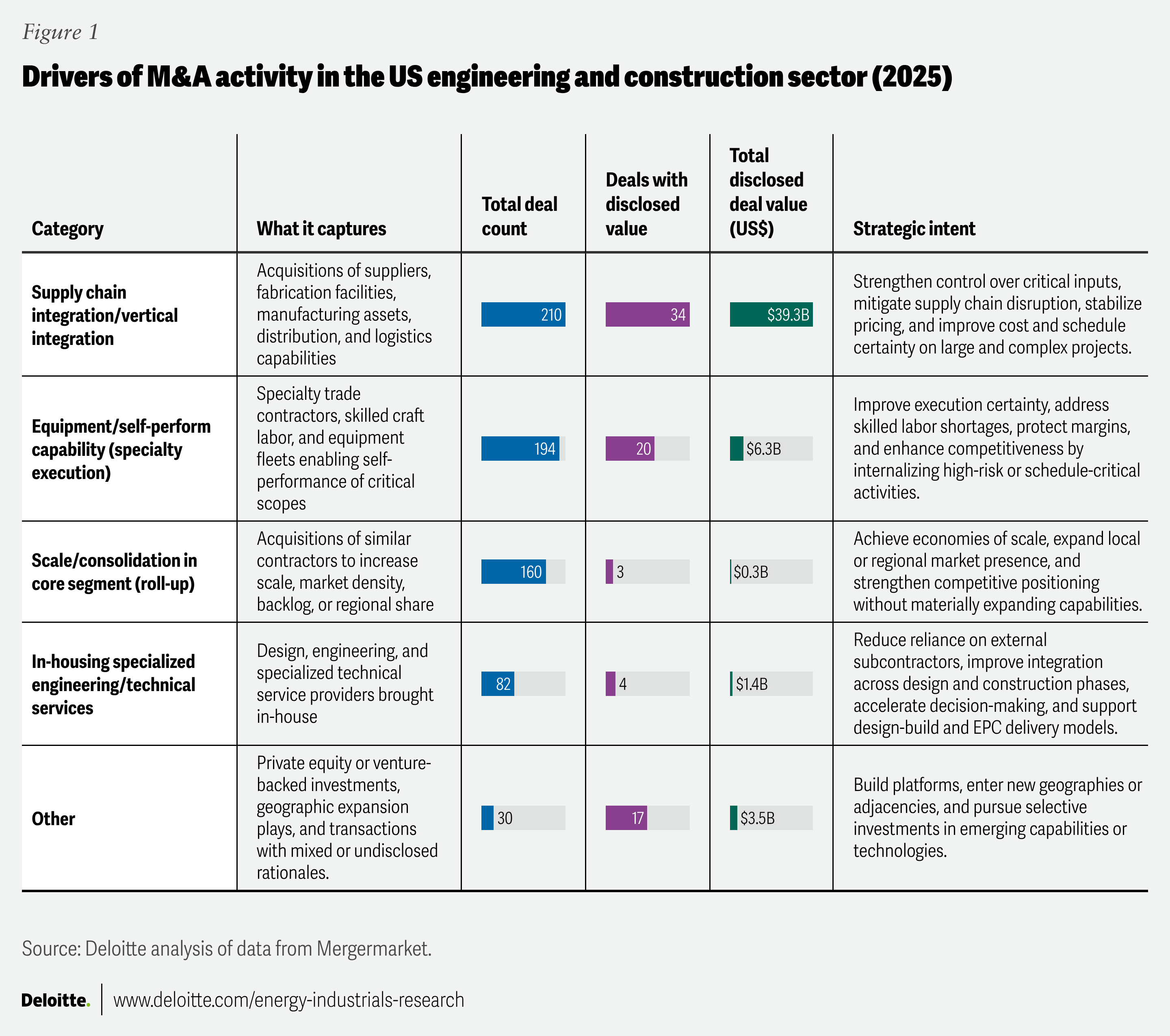

In 2025, over 670 US E&C-related M&A deals were completed, representing approximately US$50.8 billion in disclosed deal value.25 Most of the activity was concentrated on core construction, which accounted for over 340 transactions and nearly three-quarters (US$39.5 billion) of total disclosed deal value. This concentration supports the strategic importance of assets that directly influence execution certainty and margin performance, often in complex, schedule-sensitive work.

Beyond construction, deal activity extended into adjacent and enabling segments, including industrial products and services and energy, reflecting investment tied to infrastructure modernization and industrial expansion. Transactions across services and technology–oriented sectors suggest a broader ecosystem approach to capability building, despite smaller individual deal sizes.

To better understand the underlying drivers of M&A activity in the US E&C sector, we analyzed all identified transactions and consolidated them into five strategic intent categories based on the primary rationale behind each deal (figure 1).

Why it matters

The dominance of deals related to supply chain integration and self-perform capability highlights the value placed on predictability, execution reliability, and greater control over costs and timelines. By contrast, relatively fewer large consolidation deals point to a more disciplined approach to balance sheets. Taken together, these trends point to an industry prioritizing financial resilience and operational flexibility, rather than scale alone, amid ongoing uncertainty.

Conclusion

As volatility reshapes the US E&C landscape, financial agility is no longer defensive, but is becoming a strategic differentiator. Firms are using varied financial strategies to improve decision speed, protect margins, and preserve capital flexibility. When embedded into core operations, these strategies can help firms allocate capital more optimally and respond effectively as conditions change.

Continue the conversation

Meet the industry leaders

Steve Shepley

Michelle Meisels

Kate Hardin

by

Michelle Meisels

Sami Alami

Kate Hardin

Scott Welch

Anuradha Joshi

The authors would like to thank Kruttika Dwivedi for her key contributions to this report, including research, analysis, and writing.

Deloitte advisory board:

Jeffrey Kummer, Anand Desai, Hogan Miller

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Kimberly Prauda and Neelu Rajput for driving the marketing strategy and related assets to bring the story to life; Courtney Flaherty for her leadership in public relations; and Rithu Thomas and Aparna Prusty from the Deloitte Insights team for supporting the report’s publication.

Editorial (including production and copyediting): Rithu Thomas, Aparna Prusty, Pubali Dey, and Cintia Cheong

Design: Molly Piersol, Pooja Lnu, and Harry Wedel

Cover image by: Pooja LNU

Knowledge Services: Vanapalli Viswa Teja

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.