Throughput, not just innovation, may define the future of US defense manufacturing and industrial scale

Demand is outpacing production as sub-tier fragility, long qualification cycles, and capacity limits constrain the ability to scale output and sustain delivery

Recent conflicts and sustained support to allies have highlighted a challenge: High-intensity operations can consume critical defense equipment, such as precision munitions and air-defense interceptors, faster than the industrial base can replenish them. When the time to replenish becomes a readiness constraint, throughput—the ability to produce, replenish, and sustain at pace—stops being a factory metric and becomes a national security input.

For decades, competitive advantage in aerospace and defense centered on technical performance and program capture, specifically the ability to design the most advanced capability and secure the contract. Today, a different question is being asked: Can organizations deliver at rate, with quality and certainty, and sustain it under pressure?

In an era of prolonged competition and operational uncertainty, throughput and the industrial system behind it can become a defining advantage. This applies to replenishing already fielded defense equipment as well as clearing commercial aerospace backlogs where deliveries have not kept pace with demand. For new equipment, this means translating proven designs into certified, supply-secure, repeatable production; qualifying suppliers and processes quickly; and expanding output in response to demand shocks.

The ecosystem now faces a widening gap between what can be designed and what can be produced, replenished, and sustained at pace.1 Sub-tier fragility, qualification throughput limits, quality-at-rate challenges, workforce constraints, and compliance requirements can constrain the industrial system.

Recent policies reflect the critical importance of throughput capabilities. Recent executive orders, including “Prioritizing the warfighter in defense contracting”2 and “Modernizing defense acquisitions and spurring innovation in the defense industrial base,”3 emphasize delivery speed, production throughput, and contractor accountability, while acquisition modernization efforts prioritize speed and flexible pathways. In parallel, “Revolutionary FAR overhaul”4 aims to simplify and streamline buying.

Table of Contents

- Demand spikes and capacity constraints

- Prototype to throughput gap

- Sub-tier fragility and supply chain visibility

- Compliance as a throughput constraint

- Automation and distributed manufacturing scale

- Primes, startups, and supplier ecosystems

- Partnerships and precision M&A

- Leadership priorities for scaling certainty

Demand spikes can outstrip production capacity

In high-intensity, contested environments, demand doesn’t ramp—it spikes. Many of these systems are high-unit-cost, long-lead-time items constrained by specialized components, energetics capacity, and a limited pool of qualified tier-2 and tier-3 suppliers. In practice, a force can expend in days what took months (or longer) to produce, while reconstitution can take years because replenishment is constrained by specialized sub-tier capacity, testing and qualification throughput, and award-to-delivery lead times, not just final assembly. Major US defense contractors are carrying historically elevated backlogs, reflecting sustained demand visibility across platforms and munitions.

Public filings show that the three largest US defense primes together hold a combined backlog of US$557 billion, equivalent to 2.7 times 2025 annual sales, implying an order coverage horizon of 30 months at current revenue run rates.5 At the same time, policymakers and industry leaders have signaled intentions to significantly expand production of critical systems,6 including air and missile defense interceptors and long-range precision munitions, with discussions of doubling output over the next several years to address stockpile replenishment and operational demand.7

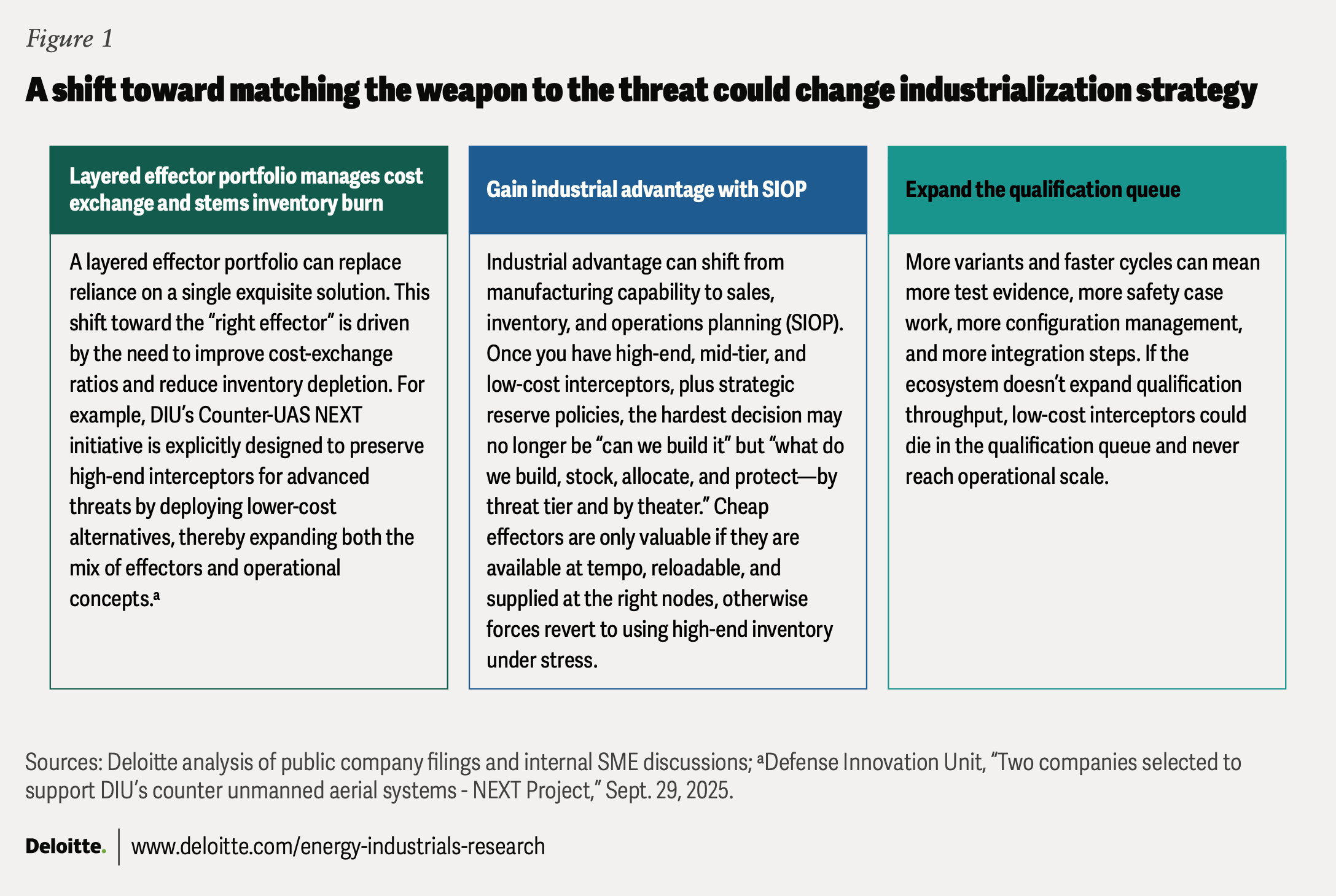

Additionally, matching the weapon to the threat can reserve scarce, high-cost inventory for high-end targets (figure 1). The US Navy is already signaling this shift, calling for a broader mix of munitions and openness to effective solutions that may not meet legacy specifications but are still effective when inventories are constrained.8 The service has explicitly sought lower-cost kinetic counter‑unmanned aircraft system interceptors to address the unfavorable cost exchange of using multimillion-dollar missiles against drones costing thousands.9

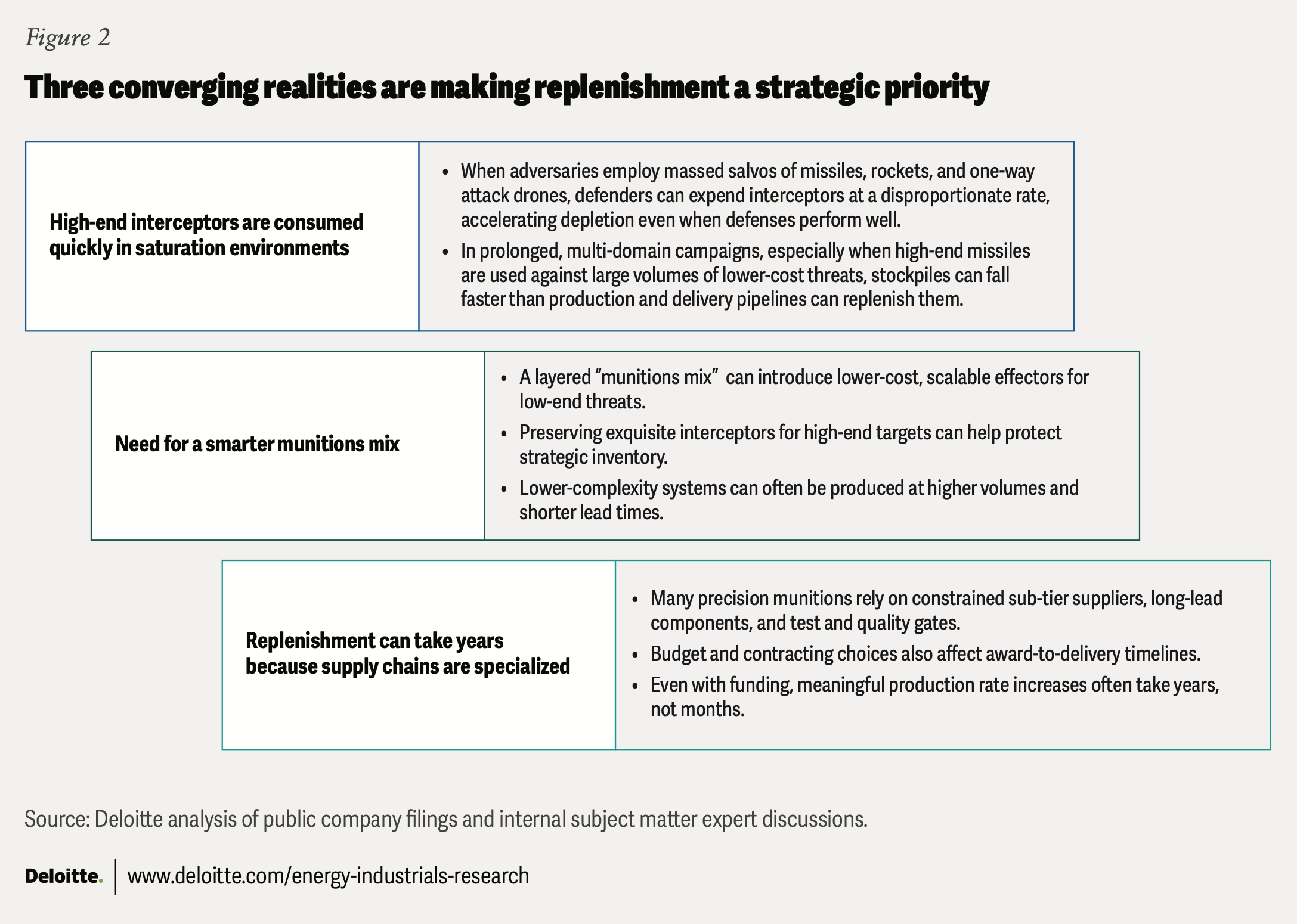

Industrialization is not a single problem. It’s often a portfolio of distinct throughput constraints, including energetics and propulsion, electronics, final assembly, and platform or launcher production. To help address this, some firms are investing in automation, infrastructure, and supply chain resilience to increase throughput. Three structural realities are converging to shape this challenge (figure 2).

Where the system breaks: The gap from prototype to throughput

Replenishment speed is constrained by industrial timelines. While demand for munitions can surge rapidly, procurement lead time timelines often span two to four years.10 Production capacity also varies widely across systems, from dozens of complex launchers to tens of thousands of guidance kits annually.

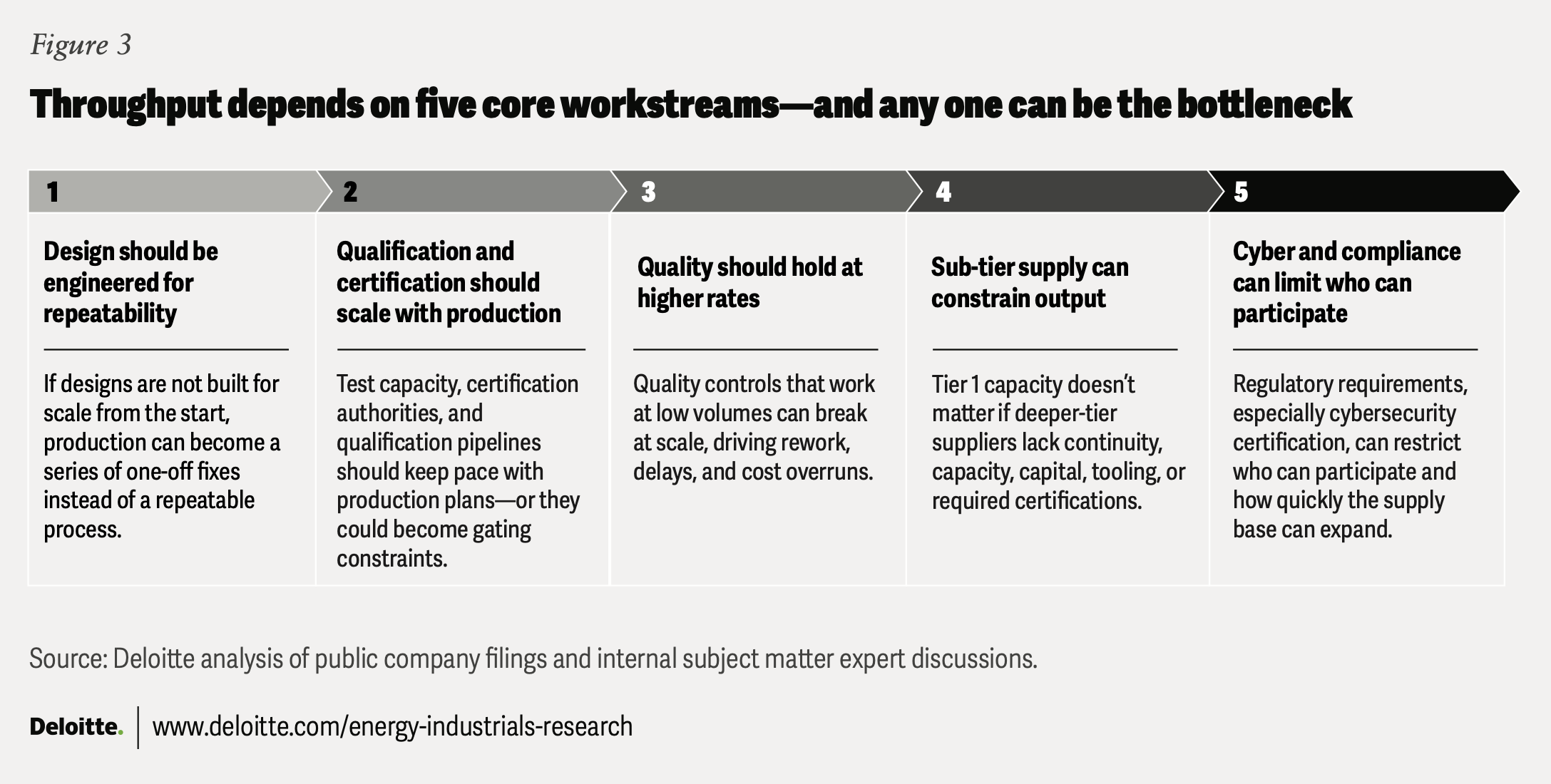

As a result, with allied demand through foreign military sales representing a meaningful share of total orders, expanding production is an ecosystem-level challenge rather than a single-program optimization problem—the slowdown typically occurs at the point where “we can build it” becomes “we can build it repeatedly, compliantly, and at rate.” This is the core coordination challenge. Industrialization at scale should include aligning the full ecosystem, not just optimizing any single node (figure 3).

A hidden constraint: Sub-tier fragility and supply chain visibility

The most acute constraints are rarely at the prime contractor level. They sit deeper in the sub-tier supply chain, where multi-tier visibility is limited, working capital is tight, and qualification timelines are long. In practice, you cannot surge what you cannot see.

Why missile production still lags demand

Solid rocket motors are critical for munitions like the Guided Multiple Launch Rocket System and the Standard Missile family. The supplier base has consolidated, lead times are long, and energetics capacity is constrained. Even when primes have signed contracts and expanded final assembly capacity, output may still fall short of demand because of bottlenecks at tier-2 and tier-3 suppliers.11

The Department of Defense and industry are investing in additional solid rocket motor capacity, efforts to attract new entrants, and modernization approaches such as automation and additive manufacturing.12 One challenge is timing, since these fixes take years to mature. A prime contractor cannot simply demand higher rates if a tier-3 casting supplier lacks the capital for automation, the workforce needed to add shifts or required cybersecurity certifications.

Compliance as a throughput constraint

Compliance is increasingly shaping who can participate in the industrial base and how quickly suppliers can scale. The Cybersecurity Maturity Model Certification (CMMC 2.0) is being implemented through two rulemakings: the CMMC Program Rule (32 CFR Part 170) and the Defense Federal Acquisition Regulation Supplement rule (48 CFR), which govern how cybersecurity requirements appear in contracts.13 The contractual rollout began on Nov. 10, 2025, with phased implementation extending through 2028.

For some sub-tier suppliers, particularly smaller firms without dedicated compliance teams, CMMC can introduce onboarding friction. Certification timelines can slow supplier onboarding and narrow the near-term pool of eligible vendors, shifting schedule and execution risk to primes when a critical node in the chain isn’t ready in time. The practical implication is that primes should consider treating certification as a more-than-simple passthrough requirement.

In practice, enabling suppliers means helping them scale by providing shared templates and control implementations, reference cybersecurity architectures, and joint readiness or qualification efforts that reduce rework and recertification delays. Many of the most significant constraints sit outside the factory, across the broader ecosystem, such as qualification capacity, cyber readiness, supplier working capital, or workforce availability. One shift could be to manage industrialization as an end-to-end production system—designing compliance and sub-tier readiness into the rate plan from the start.

Scaling through automation and distributed manufacturing

Across the US aerospace and defense industry, some companies are investing in new approaches to increase manufacturing throughput and production resilience. Two responses are emerging most clearly: greater use of automation and expansion of distributed manufacturing networks.

Automation at scale: Automation is becoming an important lever for scaling production. Companies are investing in robotics, digital manufacturing tools, and advanced inspection technologies to increase production and maintenance speed and consistency.

For example, one major prime has deployed an enterprise-level digital system that connects approximately 17,000 pieces of equipment across 40 factories into a single platform.14 By integrating operations at this scale, firms can improve manufacturing yield, reduce rework, and increase output—without relying solely on additional labor in an already constrained workforce environment.

Distributed manufacturing at scale: Distributed manufacturing can expand capacity and diversify production risk by shifting production across a network of internal sites and external partners. In some cases, these distributed networks are enabled by the same digital and automation capabilities described above.

Recent moves show two models of distributed capacity: expanding production across multiple company-operated sites and shifting work to partner producers. Several US defense contractors have expanded production of critical munitions and components across multistate networks of company-operated facilities to increase throughput and resilience. In addition, a US military shipbuilding company is expanding capacity by partnering with a distributed network of shipyards and fabrication providers across multiple states to increase throughput and support rising naval demand.15

While distributed manufacturing can help expand capacity and diversify production risk, it can shift the prime contractor’s role from managing a single factory to orchestrating a broader industrial network. However, expanding production across multiple partners introduces new challenges in quality assurance, configuration control, cybersecurity, and schedule coordination.

Ecosystems that align primes, startups, and suppliers

Industrialization at scale should include an ecosystem operating model that aligns primes, sub-tier suppliers, and emerging aerospace and defense startups, supported by coordinated government actions that sharpen demand signals and help relieve bottlenecks that constrain throughput.

Ecosystem partnerships are becoming an important lever for scaling throughput

Aerospace and defense companies are increasingly partnering with technology firms to help bring solutions to market faster, leveraging talent and intellectual property that traditional primes may not have in-house. These partnerships can help solve defense problems using proven commercial capabilities, while reserving capital for areas where these companies must retain core ownership.16

Ecosystem design that focuses on producibility, qualification throughput, quality maturity, and multi-tier readiness can become a competitive advantage. This approach can create repeatable mechanisms that connect innovators, primes, sub-tier suppliers, and demand signals into a production system that scales with rate, quality, and delivery certainty.

It can become repeatable when it includes:

- shared governance and incentives

- shared data and configuration baselines (digital thread)

- repeatable qualification pathways and test throughput

- sales, inventory, and operations planning cadence that continuously reconciles demand, inventory, capacity, and constraints across tiers

Scaling pathways: Partnerships and precision mergers and acquisitions

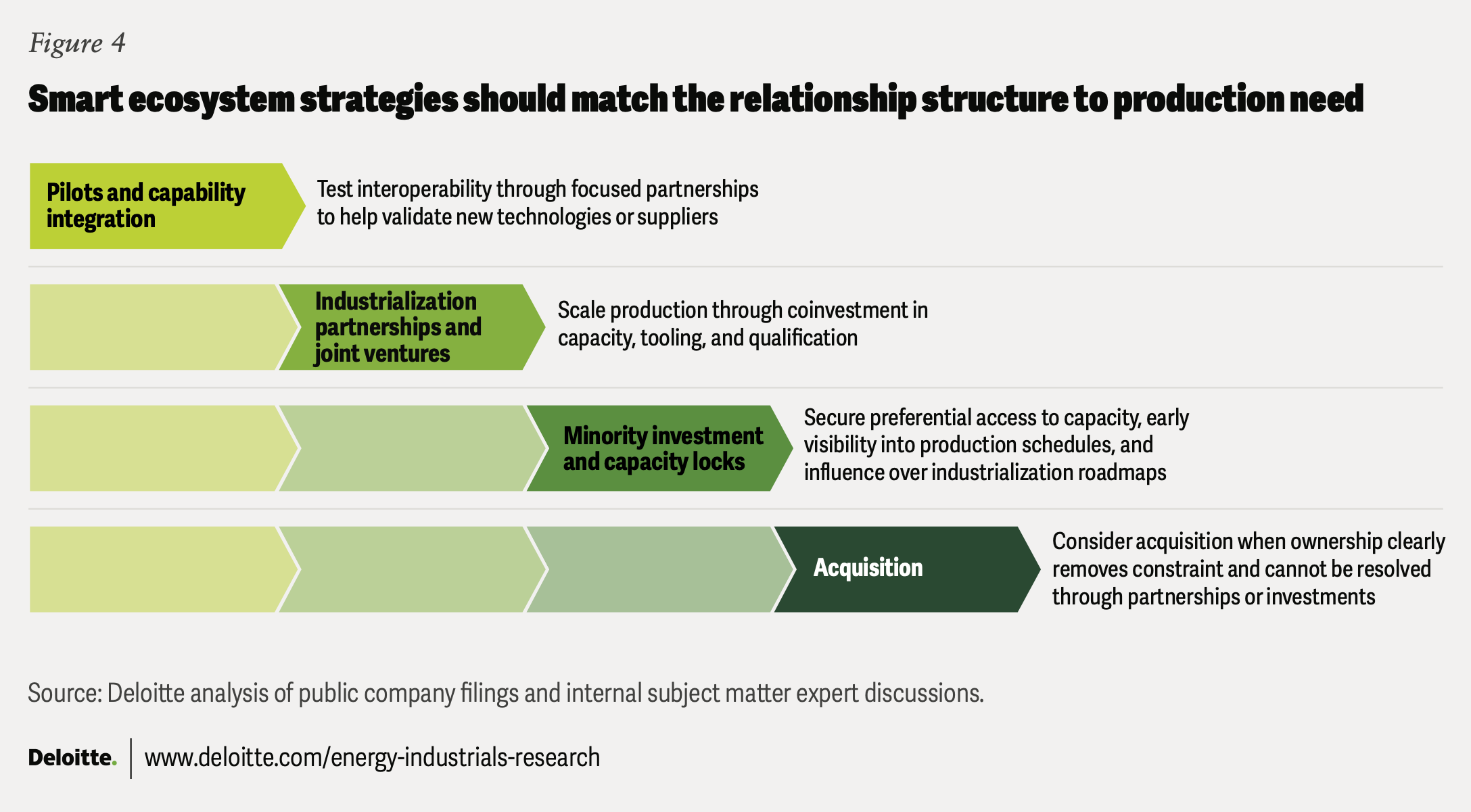

When industrialization is treated as a secondary workstream, programs may face delays, cost growth, or failure. Addressing industrialization bottlenecks often requires more than internal investment. Increasingly, aerospace and defense companies are using a graduated set of ecosystem strategies—partnerships, investments, and selective acquisitions—to help address bottlenecks and scale production (figure 4).

Partnerships are often a first step. Rather than treating suppliers or emerging companies as transactional vendors, some primes are building deeper industrial relationships designed to accelerate production readiness. These collaborations can begin with pilot programs or capability integration efforts that validate interoperability and manufacturability. As production requirements grow, they can evolve into joint industrialization efforts such as shared production lines, joint ventures, or coordinated investments in capacity.

As programs move closer to full-rate production, companies may also pursue targeted investments that secure access to constrained capabilities without requiring full ownership. Minority investments, long-term supply agreements, or capacity reservations can help stabilize critical sub-tier production while allowing suppliers to retain operational independence.

In some cases, however, removing a production bottleneck requires direct ownership. Here, acquisition can become a strategic tool, not primarily for consolidation, but to resolve specific industrial constraints such as limited production capacity, specialized certifications, sustainment capabilities, or fragile sub-tier supply chains.

The key question is whether a partnership, investment, or acquisition measurably increases production throughput within the program’s time horizon. In this environment, industrialization-driven deals tend to be less about scale for its own sake and more about eliminating the constraints that slow the transition from prototype to sustained production.

For example, one recent “invest-and-codevelop” approach involves a planned equity investment and partnership between a jet and turboprop engines manufacturer and an electric vertical takeoff and landing aircraft manufacturer to codevelop a hybrid-electric turbogenerator for civil and defense applications. This approach combines the aircraft manufacturer’s electric-generation capabilities with the engine manufacturer’s certification and manufacturing strengths.17

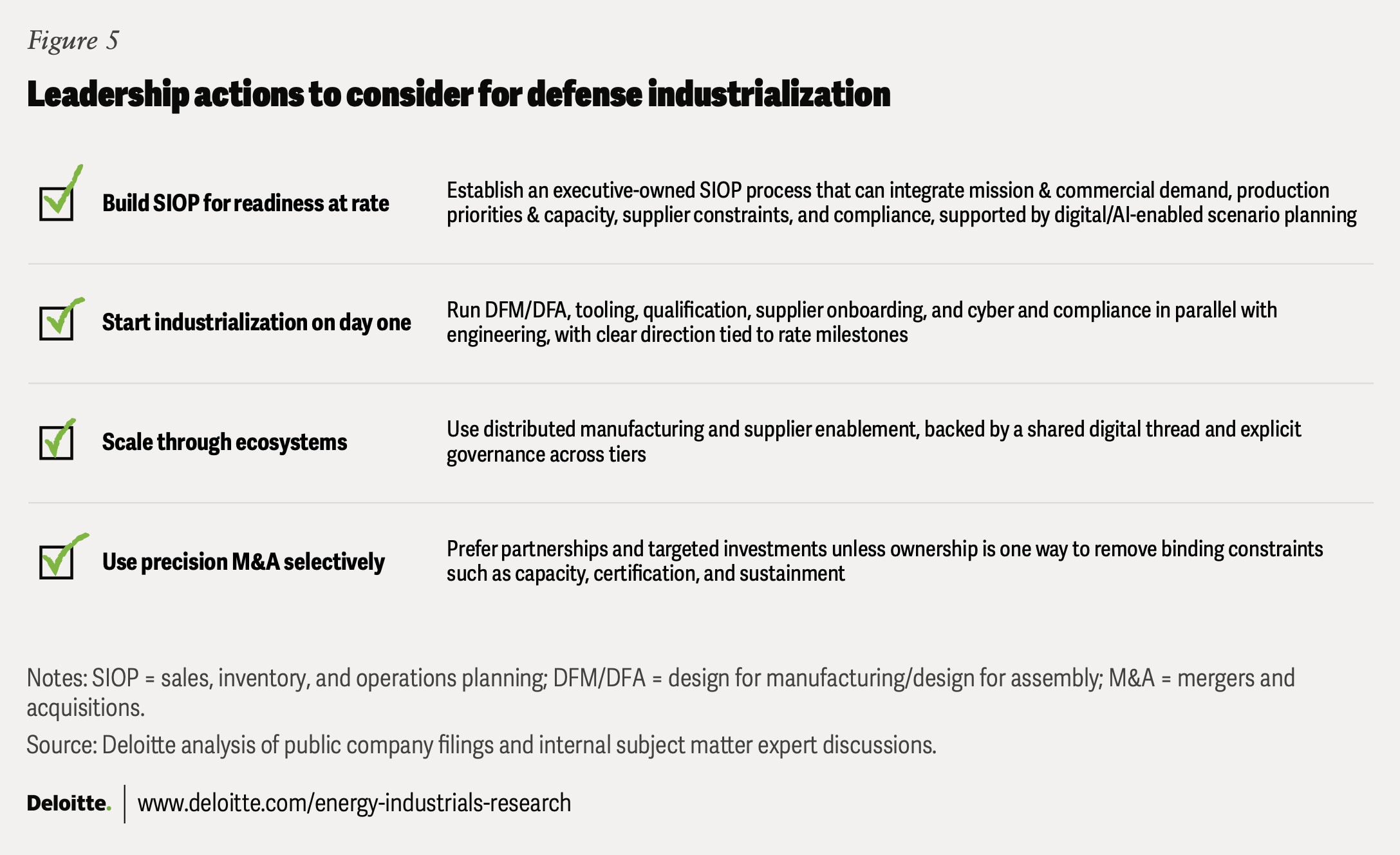

The leadership mandate: Scale with certainty

The aerospace and defense industry’s industrialization gap reflects a coordination challenge: aligning innovators, primes, sub-tiers, and demand signals into a repeatable production system. To meet this challenge, ecosystem players should function as force multipliers so that speed can translate into certified, scalable output, not just faster prototypes (figure 5).

In an era where time to replenish is a strategic metric, technical advantage matters only when it can be produced, certified, delivered, sustained, and regenerated at the rate readiness demands. Throughput is emerging as a defining strategic advantage, and digital, AI-enabled planning can help leaders convert intent into executable rate.

Continue the conversation

Meet the industry leaders

Steve Shepley

Lindsey Berckman

Kate Hardin

By

Lindsey Berckman

Kerry Millar

Ashish Midha

Kate Hardin

Scott Welch

Tarun Dronamraju

The authors would like to thank Jack Koenigsknecht for being a part of our research advisory board and contributing to shaping this research article.

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Kimberly Prauda and Neelu Rajput for driving the marketing strategy and related assets to bring the story to life; Courtney Flaherty for leading public relations efforts; and Kavita Majumdar, Pubali Dey, and Aparna Prusty from the Deloitte Insights team for supporting editing and publication of this report.

Editorial (including production and copyediting): Kavita Majumdar, Aparna Prusty, Pubali Dey, and Anu Augustine

Design: Sanaa Saifi, Harry Wedel, and Molly Piersol

Cover artist: Sanaa Saifi and Jim Slatton

Knowledge services: Agni Wagh

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace and defense, chemicals and specialty materials, engineering and construction, industrial manufacturing, mining and metals, oil and gas, power and utilities, and renewable energy sectors.