E-invoicing & E-reporting

How to address challenges, seize opportunities, and find solutions in the digital tax era

As invoicing is a critical business process, this digital trend presents both compliance challenges and opportunities for transformation that require your attention. Join us as we explore the realm of e-invoicing and e-reporting.

E-Invoicing & E-Reporting: What and why now?

E-invoicing and e-reporting are rapidly evolving on a global scale, presenting various formats, requirements and entering into force on numerous dates.

E-invoicing and e-reporting are rapidly evolving globally, driven by digital tax obligations that are reshaping business dynamics. Governments are adopting these mandates, shifting from paper-based VAT compliance to data-driven digital tax administration. The OECD envisions a seamless digital transformation in taxation, akin to shifts in other corporate functions. This transformation, termed "fiscalisation," requires businesses to adapt to new digital tax standards for the processing and issuance of invoices. We acknowledge the crucial role of guiding businesses through the complexities of this transformation as they navigate the opportunities and challenges presented by "fiscalisation" in the digital tax era on a global scale.

Read our latest whitepaper: The Netherlands to implement e-invoicing?

Meet our experts

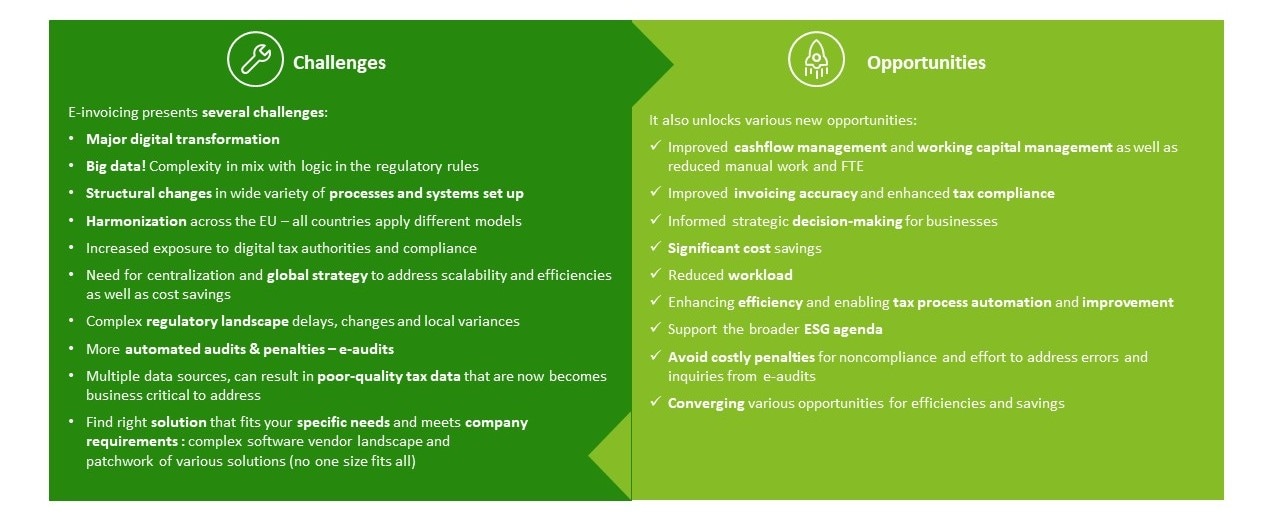

E-Invoicing & E-Reporting: Challenges and Opportunities

Without a clearly defined vision, strategy, and ownership, businesses face implementation challenges, may miss automation opportunities, and could struggle with future compliance, thereby heightening their tax-related risks.

Identifying the optimal approach for your organisation is complex. We invite you to join us in navigating e-invoicing and e-reporting, where we will explore the challenges your business encounters.

E-invoicing presents both challenges and opportunities for your company. While transitioning from traditional paper-based invoicing to electronic formats involves hurdles such as compliance complexities, data quality issues, and technological adaptation, it also offers the potential for streamlined processes, cost efficiencies, and enhanced accuracy. Additionally, it creates an unavoidable regulatory obligation to initiate essential finance and business transformation efforts.

Embracing e-invoicing can lead to improved efficiency, reduced errors, and better financial management, marking a significant shift in modern business transactions. Below, we outline the critical challenges and opportunities that e-invoicing presents in today’s dynamic landscape.

Before commencing your e-invoicing journey, it is essential to reflect on regulatory aspects, the relationship between e-invoicing and e-reporting, global trends, technology choices, strategic approaches, and operational considerations.

Leveraging our extensive experience in the digital tax landscape, we aim to be your strategic and operational partner on this transformative journey. Our solution-agnostic, scenario-based approach is organised into four comprehensive phases tailored to your company's specific opportunities and challenges related to digital tax obligations. Whether you are formulating a centralised strategy, preparing for go-live, or seeking advanced continuous monitoring, we are here to support you every step of the way.

The choices you have – No one size fits all

There are multiple business led factors that need to be considered in developing a robust deployment strategy. We collaborate with businesses to assess how these key factors align with business's operating models and compliance goals and help them in identifying global strategy.

How can we support you?

Empowering Your E-Invoicing Journey: We support businesses depending on their needs throughout their entire or part of the e-invoicing and e-reporting journey.

Opens in new window