Digitalisation of indirect tax demands a holistic approach

As indirect tax administration undergoes the biggest changes since value-added taxes were first implemented decades ago, a comprehensive compliance response will pay long-term dividends.

Across the globe, tax authorities are redesigning methods for assessing and collecting value-added tax (VAT), replacing periodic mostly paper-based compliance reports with e-reporting and e-invoicing. Indirect tax compliance is undergoing the most dramatic changes since the very idea of a VAT first took hold in the 1960s. We are witnessing the development of what the Organisation for Economic Co-operation and Development (OECD) describes as data-driven or digital tax administration. The vision is for a digital transformation in which taxation becomes “more of a seamless and frictionless process over time,” according to an OECD paper. As it happened when digital change swept through other businesses or corporate functions, the transformation of tax is creating a more networked and data-focused environment.

This transformation puts new demands not just on the tax department but on the entire organisation. Tax-related requirements now need to be reflected in all financial systems and business processes and such changes are having a huge impact on the setup of ERP systems and other IT infrastructure. Companies will need to deploy resources in a different manner. Data quality must improve to meet the requirements set by tax authorities.

Indeed, the increasing complexity of tax data requirements and the variation from country to country put a premium on flexible data infrastructure that can cope with new or changing demands. Relevant customer, product and supplier data must be produced correctly and automatically, because that data is now shared directly with the tax authorities. And it is suddenly becoming business critical: Matters of tax compliance take on a new importance when the business needs to issue a valid e-invoice to customers under new indirect tax rules.

Most multinationals are working with new indirect tax compliance requirements in at least some of the countries where they operate. In Latin America, for example, Mexico and Brazil have led the way in closing the gap between theoretical VAT revenues and actual collections and they have relatively mature systems for e-reporting in place. Too often, though, companies may be addressing changes in indirect tax requirements with ad hoc solutions for specific jurisdictions.

As e-reporting and e-invoicing become common in more jurisdictions, including the EU, where new rules are coming under its “VAT in a Digital Age” (ViDA) framework, companies need a more holistic and centralised approach. For tax leaders, we see three key lessons that can help guide the response to evolving requirements from tax authorities moving toward real-time indirect tax compliance.

1. Think digital

When a business or corporate activity is affected by digitalisation—confronted with the possibility and power of data newly available in a structured way—the disruption and the benefit can be significant. Think about how online booking has changed the hotel business or how retail experiences of all kinds have been transformed by e-commerce.

The tax function is a relative latecomer to digitalisation, remaining as a place within the enterprise where one might still find paper returns, Excel spreadsheets, and numerous manual interventions. Tax has typically struggled to keep pace with technology changes. This may be partly due to tax authorities themselves being slow to demand digital compliance, with the absolute growth in tax revenue having made change in this area a low priority for governments. Recently, though, geopolitical pressure and growing budgetary constraints have made increased digitalisation more relevant to help tax authorities address tax evasion and fraud.

With e-reporting and e-invoicing, tax authorities are creating the networked, digital environment necessary to assess tax in a new way. This changes how tax and legal compliance must be managed. Gone are the days of cumbersome manual audits, random sampling methods, and investigations of piles of documents.

In a data-driven environment, the tax authority can simply compare various data sources, which they now access in real time, reading actual numbers out of the taxpayer’s ERP system, for example. When they see gaps or anomalies, they will simply assess additional tax or block refunds—and they will shift the burden of proof onto the taxpayer when there is any disagreement.

To meet such change head on, businesses should adopt a fundamentally different tax compliance strategy—by thinking digitally. Compliance in a digital regime cannot be managed with manual processes. More than that, however, changes in tax compliance should be seen as an opportunity. Lessons learnt from the digitalisation of other businesses and functions are applicable here. A significant digital effort is needed for tax, with software solutions embedded in the business.

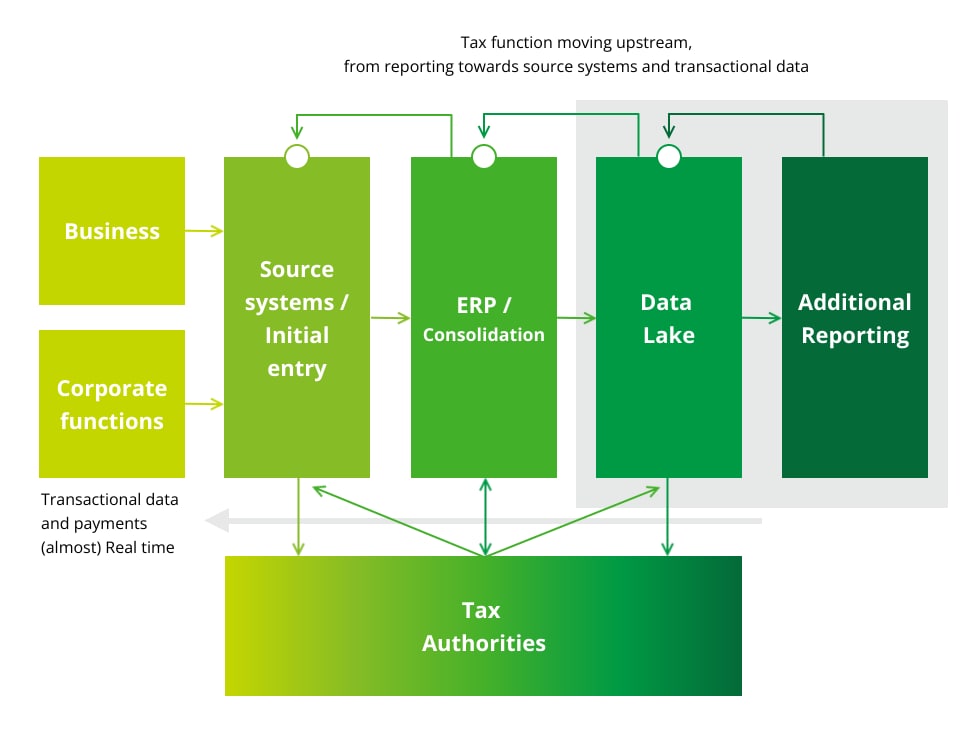

Our view is that digitalisation of indirect tax requires a new mindset. Tax regulatory changes demand a move upstream: Increasingly, tax data requirements need to be tackled at the level of the initial entry, integrated with core business and finance processes, not as a later compliance step.

Tax-related data entry will be initiated upstream and embedded in the finance function through the ERP system. This encompasses most of the key focal areas for tax. Digital tax administration, real-time reporting and transparency will sit within this system. Tax control needs to be both preventive and proactive, as well as automated, before tax authorities analyse it. When tax authorities have access to data in an ERP system or a data lake, the information residing there should be checked in a more integrated way by IT and finance, using properly tailored data analytics tools and automated checks and tests.

Automated processes will replace most of the existing returns-based tax compliance (returns eventually will disappear altogether). Better tax data quality will become paramount as the digital transformation of indirect tax moves forward. Digital audits will become the norm.

2. Act globally

Companies cannot rely on local fixes much longer. Data will increasingly be checked across borders as tax authorities expand their reach and cooperation. For taxpayers, this should reinforce the existing trend toward more central governance for tax processes. Compliance with e-invoicing or e-reporting requirements should not be left solely to local finance and tax teams.

Efficiency and cost, as well as the potential to centralise, provide additional reasons to think globally. Organisations can recognise benefits of scale and greater opportunities for standardisation and automation when they create systems that are consistent globally. Indeed, e-reporting and e-invoicing should drive companies toward consistent and consolidated use of their ERP system—and may enhance the case for upgrading those systems.

The level of global standardisation or consistency that can be expected in e-reporting and e-invoicing rules is not yet clear—so far there is often wide variation. But companies should proactively examine the indirect tax schemes in all their operating jurisdictions and seek solutions that are broadly applicable across as many as possible. We see certain patterns and consistent concepts. From a data point of view, the requirements and structures are not that different across jurisdictions. Choosing a vendor with a good understanding of similarities and differences in requirements in different locations and one with truly global reach, will provide advantages.

The data system improvements most needed to meet the evolving demands of global indirect tax compliance are likely to overlap significantly with the solutions needed to meet other evolving tax challenges. Most notably, the increasing demands of tax authorities as they implement Pillar Two regulations highlight the need for higher quality data and consistent data systems and processes across jurisdictions, similar to what we see in the indirect tax changes with DAC7, CESOP, and e-reporting.

Even companies that operate primarily in the US, which has no VAT system, might benefit from the urgency in a data transformation that is relevant to both indirect tax and Pillar Two changes.

3. Work cooperatively

With the implementation of e-reporting and e-invoicing, indirect tax compliance may no longer fall solely under the tax department’s purview. The stakeholder landscape has changed. As tax requirements become more closely tied to invoicing and supply chain, the entire business process can be affected. Addressing these changes can’t be done by the tax department alone.

The centre of gravity for the indirect tax team is shifting away from returns and reports toward real-time or near-real-time tax data and this will change how resources need to be allocated. E-reporting and e-invoicing puts the spotlight on having the systems and people necessary to ensure the quality of data that now goes directly to tax authorities. The entire transactional dataset—customer location and VAT status, vendor information, and so on—must be accurate.

Data that finance or IT generated in the past, with the expectation that tax would figure out how to make it work, will no longer suffice. To drive the business globally, companies must have e-invoicing in place. Everyone is in this together now: Tax, finance, and IT all must work together to ensure compliance in a rapidly evolving global tax system.