The new Retail Investment Strategy (RIS) package will usher in significant sweeping changes across the banking, insurance, and investment management sectors.

RIS proposes significant changes to the Packaged Retail and Insurance-Based Investment Products (PRIIPs) Regulation and includes an Omnibus Directive that will amend the following directives:

Markets in Financial Instruments Directive (MiFID) II

Insurance Distribution Directive (IDD)

Undertakings for Collective Investment in Transferrable Securities (UCITS) V Directive

Alternative Investment Fund Managers Directive (AIFMD)

These regulatory changes aim to ensure retail investors can access better investment options and receive fair treatment and value for money in the market.

A closer look

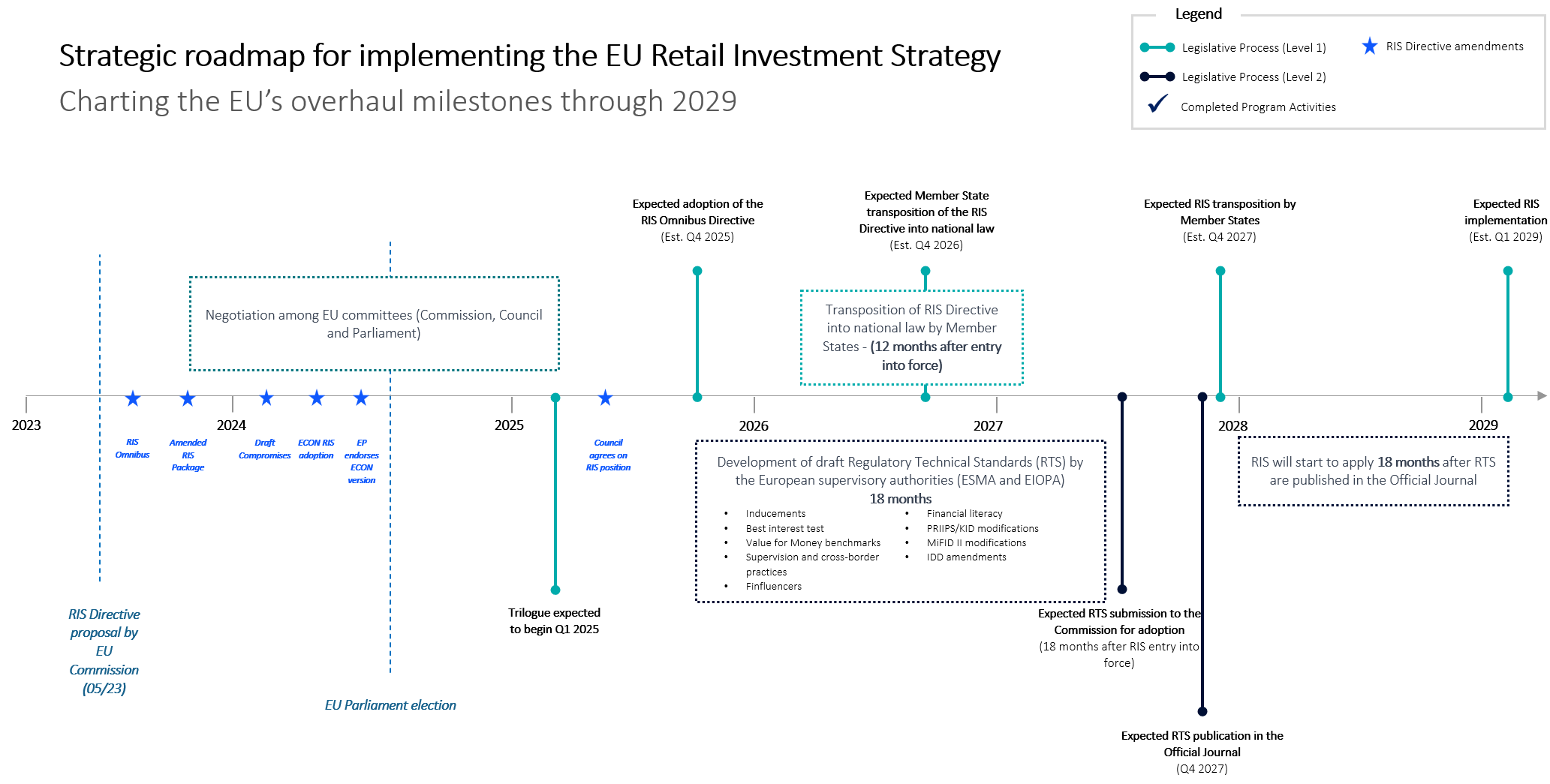

In May 2023, the European Commission launched discussions on the new Retail Investment Strategy (RIS) as a way to offer retail investors safer investment opportunities and address other prevalent issues within the investment industry.

This latest version of the RIS Package was released by ECON parliament committee and then endorsed by European Parliament on 23 April 2024. The package amends several regulations; you can find the anticipated impacts detailed below.

Banking

RIS

New consumer protection tools

Improved suitability with risk, diversification and cost considerations

Identification and warning of risky and complex investment products

Transmission of product data by manufacturers and distributors to national competent authorities (NCA)

Creation of new product benchmarks by the European Insurance and Occupational Pensions Authority (EIOPA) and European Securities and Markets Authority (ESMA)

New minimum knowledge and competence standards required for financial advisors

Rules on information sharing when providing cross-border services

Updates on client reporting to coordinate the disclosures

New obligations around social media promotion through financial influencers, or "finfluencers"

Requirement to archive marketing communication made within the duration of the client relationship

Introduction of insurance product information document (IPID) for life insurance products

After Council’s approval:

Removal of the proposed ban on inducements for execution-only sales

Strengthened safeguards for inducements, including an inducement test and a uniform test specifying the duty for advisors to act in the client's best interest

Enhanced transparency about what payments are considered inducements, their costs, and their impact on investment returns

Overarching principles to prevent conflicts of interest in the case of inducements

Option for Member States to use Union supervisory benchmarks for market comparisons

Requirement for manufacturers and distributors to compare their products to a peer group of similar investment products within the EU

Review of the Value for Money framework seven years after implementation

PRIIPs

New "Product at a glance" section at beginning of the key information document (KID)

Removal of comprehension alert

Dedicated section on sustainability aligned with the Sustainable Finance Disclosure Regulation (SFDR)

More flexibility to include past performance along with performance scenarios in the KID

Prioritization of multi-option products (MOPs) with the requirement to develop a tool to compare different investment options

After Council’s approval:

Enhanced digital access to KIDs to help investors better understand and compare investment products

MiFID

Additional product approval requirements for manufacturers

Peer-group requirements when manufacturing or distributing a PRIIP

Ban on inducement for portfolio management

New €100 threshold for independence impairment

Additional requirements for investment advice to retail investor

After Council approval:

Standardization of investor protection rules across different sectors and EU laws

Measures to ensure fair value and prevent conflicts of interest due to inducements

Increased transparency requirements for costs, charges, and performance

Investment Management

RIS

New consumer protection tools

Improved suitability with risk, diversification and cost considerations

Identification and warning of risky and complex investment products

Transmission of product data by manufacturers and distributors to national competent authorities (NCA)

Creation of new product benchmarks by the European Insurance and Occupational Pensions Authority (EIOPA) and European Securities and Markets Authority (ESMA)

New minimum knowledge and competence standards required for financial advisors

Rules on information sharing when providing cross-border services

Updates on client reporting to coordinate the disclosures

New obligations around social media promotion through financial influencers, or "finfluencers"

Requirement to archive marketing communication made within the duration of the client relationship

Introduction of insurance product information document (IPID) for life insurance products

After Council’s approval:

Removal of the proposed ban on inducements for execution-only sales

Strengthened safeguards for inducements, including an inducement test and a uniform test specifying the duty for advisors to act in the client's best interest

Enhanced transparency about what payments are considered inducements, their costs, and their impact on investment returns

Overarching principles to prevent conflicts of interest in the case of inducements

Option for Member States to use Union supervisory benchmarks for market comparisons

Requirement for manufacturers and distributors to compare their products to a peer group of similar investment products within the EU

Review of the Value for Money framework seven years after implementation

PRIIPs

New "Product at a glance" section at beginning of the key information document (KID)

Removal of comprehension alert

Dedicated section on sustainability aligned with the Sustainable Finance Disclosure Regulation (SFDR)

More flexibility to include past performance along with performance scenarios in the KID

Prioritization of multi-option products (MOPs) with the requirement to develop a tool to compare different investment options

After Council’s approval:

Enhanced digital access to KIDs to help investors better understand and compare investment products

MiFID

Additional product approval requirements for manufacturers

Peer-group requirements when manufacturing or distributing a PRIIP

Ban on inducement for portfolio management

New €100 threshold for independence impairment

Additional requirements for investment advice to retail investor

After Council approval:

Standardization of investor protection rules across different sectors and EU laws

Measures to ensure fair value and prevent conflicts of interest due to inducements

Increased transparency requirements for costs, charges, and performance

UCITS

Clarification of "undue costs" classification and required documentation

Management fees to monitor pricing process and ensure appropriateness of the costs to the value delivered

Investor compensation mechanisms

Market comparisons to be considered in pricing process

New reporting of costs and performance to the national competent authority (NCA)

After Council approval:

Standardization of transparency and disclosure requirements to avoid overlaps

Improved regulatory disclosures to help investors better understand and compare UCITS products

AIFMD

Clarification of "undue costs" classification and required documentation

Management fees to monitor pricing process and ensure appropriateness of the costs to the value delivered

Investor compensation mechanisms

Market comparisons to be considered in pricing process

New reporting of costs and performance to the national competent authority (NCA)

After Council approval:

Alignment of transparency and information requirements with other EU legislation

Enhanced supervisory cooperation to ensure consistent application of rules across the EU

Insurance

RIS

New consumer protection tools

Improved suitability with risk, diversification and cost considerations

Identification and warning of risky and complex investment products

Transmission of product data by manufacturers and distributors to national competent authorities (NCA)

Creation of new product benchmarks by the European Insurance and Occupational Pensions Authority (EIOPA) and European Securities and Markets Authority (ESMA)

New minimum knowledge and competence standards required for financial advisors

Rules on information sharing when providing cross-border services

Updates on client reporting to coordinate the disclosures

New obligations around social media promotion through financial influencers, or "finfluencers"

Requirement to archive marketing communication made within the duration of the client relationship

Introduction of insurance product information document (IPID) for life insurance products

After Council’s approval:

Removal of the proposed ban on inducements for execution-only sales

Strengthened safeguards for inducements, including an inducement test and a uniform test specifying the duty for advisors to act in the client's best interest

Enhanced transparency about what payments are considered inducements, their costs, and their impact on investment returns

Overarching principles to prevent conflicts of interest in the case of inducements

Option for Member States to use Union supervisory benchmarks for market comparisons

Requirement for manufacturers and distributors to compare their products to a peer group of similar investment products within the EU

Review of the Value for Money framework seven years after implementation

PRIIPs

New "Product at a glance" section at beginning of the key information document (KID)

Removal of comprehension alert

Dedicated section on sustainability aligned with the Sustainable Finance Disclosure Regulation (SFDR)

More flexibility to include past performance along with performance scenarios in the KID

Prioritization of multi-option products (MOPs) with the requirement to develop a tool to compare different investment options

After Council’s approval:

Enhanced digital access to KIDs to help investors better understand and compare investment products

IDD

Distributors with cross-border activities to report relevant information for a European database each year in order to enhance supervisory cooperation within EU

Improvements and adjustments of required professional qualifications, particularly for intermediaries providing advice on integration of sustainability preferences into insurance-based investment products.

Development of a European benchmark for insurance-based investment products distributed across multiple Member States

Additional information in the insurance product’s information document for specific life insurance products

Transition from paper to electronic format for information provided to customers

Enhancement of product oversight and governance requirements

Introduction of an annual statement for retail policyholders and update of the pre-contractual information to include personalized information using a standard format and language

Option to impose stricter requirements on insurance intermediaries and undertakings as they relate to inducements,

New requirement to inform, assess and recommend the insurance-based investment products and underlying investment options which best suit the customer’s needs and best interest

Improvement of the assessment of suitability and appropriateness of insurance-based investment products

Restrictions on online insurance distribution practices

Solvency II

Removal of the requirements regarding information provided to the policyholders.

Next steps

Trialogue has started between European Council, Parliament and Commission to agree on final version of the RIS Package. It is expected that the final text will be released and voted on in the second half of 2025.